- Healthcare Services

- Sleep Service Providers Market

Sleep Service Providers Market Size, Share, and Growth Forecast, 2025 - 2032

Sleep Service Providers Market by Service (Home Sleep Testing and In-Lab Testing), Indication (Obstructive Sleep Apnea, Insomnia, Circadian Rhythm Sleeping Disorders, Narcolepsy, Rapid Eye Movement (REM) Sleep Disorder, Others), End-User, and Regional Analysis for 2025-2032

Sleep Service Providers Market Share and Trends Analysis

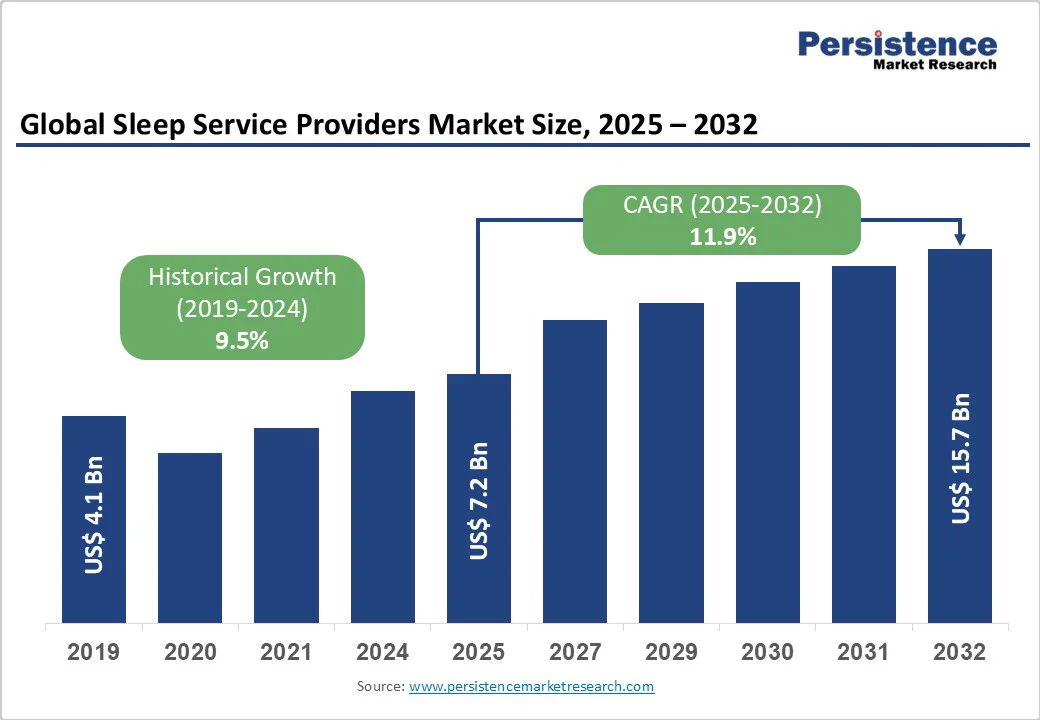

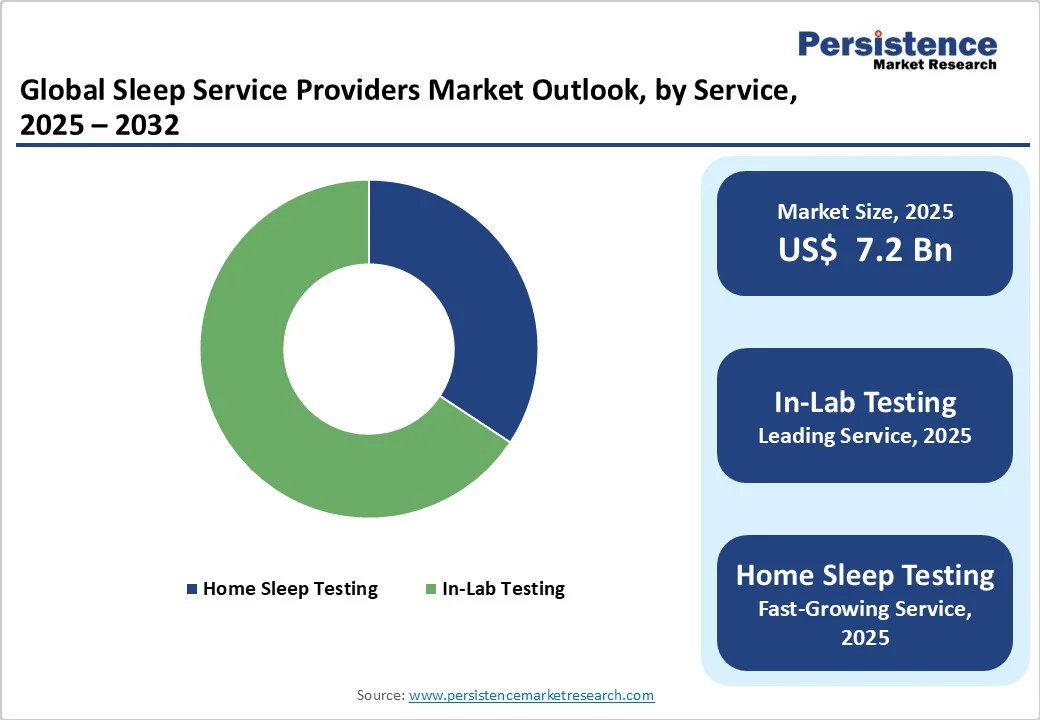

The global sleep service providers market size is likely to be valued at US$ 7.2 billion in 2025, and is projected to reach US$ 15.7 billion by 2032, growing at a CAGR of 11.9% during the forecast period 2025-2032, driven by the increasing prevalence of sleep disorders such as obstructive sleep apnea, insomnia, and narcolepsy. Growing awareness of sleep health and the importance of early diagnosis, coupled with the adoption of advanced diagnostic technologies such as polysomnography and AI-based monitoring, are fueling market growth.

Key Industry Highlights:

- Leading Region: North America is expected to dominate the global market in 2025, owing to a high prevalence of sleep disorders, advanced healthcare infrastructure, strong reimbursement frameworks, and continuous technological innovation.

- Fastest-growing Regional Market: The Asia Pacific market is set to expand rapidly from 2025 to 2032 due to rising awareness of sleep health, rapid urbanization, expanding healthcare facilities, and increased investment in diagnostic technologies.

- Leading Service: In-lab sleep testing is likely to lead the market in 2025 because of its diagnostic accuracy, use of polysomnography, and capability to manage complex sleep disorders.

- Fastest-growing Service: Home sleep testing is slated to be the fastest-growing service segment through 2032, fueled by a growing demand for convenient, cost-effective, and remote diagnostic solutions.

- Notable Opportunity: Increase in sleep R&D is creating significant opportunities in the market, driving innovations in remote sleep monitoring and advanced diagnostic technologies.

| Key Insights | Details |

|---|---|

|

Sleep Service Providers Market Size (2025E) |

US$ 7.2 Bn |

|

Market Value Forecast (2032F) |

US$ 15.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

11.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Diagnostic Tools and Growing Prevalence of Sleep Disorders

The integration of AI and wearable technology in sleep study diagnostics enables more accurate, real-time, and continuous monitoring of sleep parameters such as oxygen saturation, heart rate variability, respiratory effort, and brain activity. AI algorithms analyze this large volume of data to detect abnormalities, predict sleep disorders such as sleep apnea or insomnia, and generate automated diagnostic reports with high precision. This reduces dependency on manual scoring, minimizes errors, and accelerates diagnosis turnaround times.

The growing prevalence of sleep disorders, especially among adults, is a major factor driving the market growth. Modern lifestyles characterized by high stress levels, prolonged sedentary behavior, excessive use of digital devices, and irregular sleep schedules have led to a significant increase in conditions such as insomnia, sleep apnea, and restless leg syndrome. For instance, Oxford University Press reported that around 80.6 million people in the U.S. alone were living with obstructive sleep apnea (OSA) in 2024, highlighting the widespread prevalence of sleep disorders and the growing demand for diagnostic and treatment services.

Underdiagnosis of Sleep Disorders and the Shortage of Skilled Sleep Technologists

Despite significant advancements in sleep diagnostics, underdiagnosis continues to be a major challenge for the sleep service providers market growth. A large number of individuals experiencing sleep disorders remain untreated or misdiagnosed because their symptoms often overlap with other medical conditions, such as cardiovascular disease, depression, or obesity-related complications. This overlap often leads to delayed recognition, misinterpretation of symptoms, and inadequate treatment.

Furthermore, an acute shortage of qualified sleep technologists also poses a significant constraint on this market. With a limited number of trained professionals available to conduct and interpret sleep studies, diagnostic centers often face reduced capacity, resulting in longer wait times for patients seeking evaluation. This is a critical bottleneck that has led to delays in identifying sleep disorders, postponing the initiation of appropriate treatments, and potentially worsening patient outcomes.

Increasing Government Initiatives and Sleep Health Awareness Programs

Supportive government policies, initiatives, and increased funding for sleep disorder research are creating significant growth opportunities in the market. By investing in awareness campaigns, subsidizing diagnostic services, and promoting clinical research, governments are improving both the accessibility and affordability of sleep testing and treatment services. These efforts encourage more individuals to seek timely diagnosis and care, enhance public understanding of sleep health, and stimulate innovation in diagnostic technologies and therapeutic solutions.

Increasing public awareness about the importance of sleep and the risks of sleep disorders presents a significant opportunity in the sleep service providers market. Governments, healthcare organizations, companies, and advocacy groups are running educational programs, screening initiatives, and community outreach campaigns to encourage early diagnosis and treatment. For instance, in March 2025, Philips India launched the Sleep Saviour campaign to promote awareness of sleep health and ensure timely access to therapy for patients, particularly those with OSA in India. By improving knowledge and reducing stigma around sleep disorders, these efforts drive more individuals to seek diagnostic services and therapeutic solutions, thereby expanding the customer base for sleep service providers.

Category-wise Analysis

Service Insights

The in-lab testing segment is projected to dominate the sleep service providers market in 2025, accounting for a revenue share of about 65.7%. The segment’s strong performance is primarily driven due to its diagnostic accuracy, particularly through polysomnography, which provides detailed data on brain activity, heart rate, breathing patterns, and oxygen levels, making it the gold standard for complex sleep disorders such as obstructive sleep apnea. Technological advancements, regulatory oversight, and the rising prevalence of sleep disorders further drive the preference for in-lab testing over home-based alternatives.

Indication Insights

The obstructive sleep apnea tests segment is anticipated to command approximately 44.8% of the sleep service providers market revenue share in 2025. OSA is the most prevalent sleep disorder worldwide, affecting millions of adults globally. For instance, according to ResMed’s Sleep Survey, sleep apnea affects 1 in 3 people, yet an estimated 80% remain undiagnosed. Globally, approximately millions of individuals suffer from obstructive sleep apnea, a chronic condition in which throat muscles relax during sleep, restricting airflow and disrupting normal breathing. Rising obesity rates, sedentary lifestyles, and increased awareness of the health risks associated with untreated OSA (cardiovascular issues, diabetes, daytime fatigue) are fueling the demand for diagnosis and treatment.

End-User Insights

The hospitals segment is expected to lead the market in 2025, capturing around 51% share. This is due to the capacity of hospitals to provide comprehensive sleep diagnostic services, including in-lab testing, polysomnography, and titration studies, which are critical for accurate diagnosis and treatment planning. Hospitals also benefit from having trained sleep specialists, respiratory therapists, and skilled technicians who can manage complex and severe sleep disorders. In addition, these facilities are sufficiently equipped with advanced diagnostic tools and monitoring technologies that ensure high-quality, reliable results.

Regional Insights

North America Sleep Service Providers Market Trends

North America is expected to dominate the sleep service providers market share with about 36.6% in the 2025. The U.S. is poised to lead the regional market due to the high prevalence of sleep disorders such as obstructive sleep apnea and insomnia, coupled with strong awareness of the importance of early diagnosis and treatment. Advanced healthcare infrastructure, widespread availability of specialized sleep centers, and the adoption of advanced diagnostic technologies, including in-lab polysomnography and AI-assisted monitoring, further support market growth.

Moreover, strong R&D investments by universities, medical institutions, and technology companies are driving innovations in wearable sleep diagnostics and data-driven sleep management solutions. For instance, in June 2025, a team of Northwestern investigators developed a wearable, wireless sleep monitoring device capable of providing detailed analysis of various sleep stages, aiming to enhance the detection and management of sleep disorders.

Europe Sleep Service Providers Market Trends

The Europe market is expected to grow steadily during the forecast period 2025-2032, driven by increasing investments in digital health solutions and telemedicine platforms that facilitate remote sleep monitoring and management. Rising research and development activities in sleep therapeutics and diagnostic tools are enabling more efficient and accurate detection of disorders. For instance, in February 2025, a research team led by the University of Cambridge developed comfortable, washable smart pyjamas embedded with printed fabric sensors capable of monitoring breathing by detecting subtle skin movements, even when worn loosely around the neck and chest. These innovative garments enable at-home monitoring of sleep disorders such as sleep apnea without the need for adhesive patches and bulky equipment, marking a significant advancement in non-invasive sleep diagnostics and remote health monitoring.

Apart from the above, the growing number of private sleep clinics and partnerships between hospitals and specialized centers enhance service accessibility. Supportive regulatory frameworks, rising consumer interest in preventive healthcare, and an emphasis on employee wellness programs are propelling the market in the region.

Asia Pacific Sleep Service Providers Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of nearly 14% between 2025 and 2032, fueled by increasing awareness of sleep disorders, rapid urbanization, and rising lifestyle-related health issues such as obesity and stress. Expanding healthcare infrastructure, growing investment in specialized sleep centers, and the adoption of advanced diagnostic technologies, including in-lab polysomnography and portable home sleep testing devices, are further driving growth. In December 2024, for example, researchers from Monash University partnered with experts from India to improve care for individuals with sleep disorders. At a roundtable hosted at Indraprastha Apollo Hospitals, New Delhi, sleep researchers, physicians, and industry representatives established the Australia-India Sleep Health Collaborative Initiative. The initiative aims to strengthen bilateral collaboration, promote the implementation of sleep medicine clinics in India, and develop innovative care models that integrate Ayurvedic principles with modern sleep practices, expanding awareness, accessibility, and adoption of sleep health services.

Competitive Landscape

The global sleep service providers market landscape is highly competitive, with major players such as Circle Health Group, Cleveland Clinic, Competence Center of Sleep Medicine, and Imperial College Healthcare NHS Trust dominating the industry. These companies leverage advanced technologies, extensive service networks, and strong brand recognition to maintain market leadership. They focus on innovations in in-lab and home-based sleep diagnostics, AI-driven monitoring, and integrated patient management solutions. Strategic partnerships with hospitals, research institutions, and insurance providers, along with continuous investment in R&D, enable them to expand service offerings, improve diagnostic accuracy, and enhance patient outcomes, strengthening their competitive edge globally.

Key Industry Developments

- In October 2025, Therap Services introduced a new sleep-tracking option within its health-tracking section, enabling users to view sleep data collected via Therap?Connect. The feature integrates with devices such as smart sleep mats and wearables to capture metrics such as sleep duration, quality, and breathing disturbances. This enhancement is designed to provide care-providers and agencies with deeper insights into individuals’ nightly rest patterns, supporting more holistic health management.

- In June 2025, DarioHealth Corp. and GreenKey Health entered into a strategic commercial agreement to deliver a combined chronic-condition and sleep-health care solution to U.S. payers. The partnership targets the roughly US $150 billion sleep-apnea market, addressing over 29 million Americans with this condition and linking sleep-apnea management with behavioral and cardiometabolic care. The program aims to improve health outcomes, reduce overall healthcare costs and boost productivity by integrating sleep-first diagnostics and management alongside AI-powered chronic-care tools.

- In June 2025, a new survey study presented at the 40th annual Meeting of the Associated Professional Sleep Societies (APSS) showed that patients and sleep medicine professionals differ significantly in their treatment preferences for people who have both obesity and OSA.

Companies Covered in Sleep Service Providers Market

- Circle Health Group

- Cleveland Clinic

- Competence Center of Sleep Medicine

- Imperial College Healthcare NHS Trust

- Interdisciplinary Center of Sleep Medicine

- International Institute of Sleep

- Koninklijke Philips N.V.

- Korea University Medicine

- London Sleep Centre

- MedStar Health

- Millennium Sleep Lab

- OmniSleep Sleep Health

- PM Sleep Lab

- ResMed

- Singapore Neurology & Sleep Centre

- Singular Sleep, LLC

- Sleep Management Institute

- Sleep Dynamics

- Sleep Management Services

- Somnique Sleep Health

- Surrey Sleep Research Centre

- University of Kentucky

- USA Sleep Diagnostic

Frequently Asked Questions

The global sleep service providers market is projected to reach US$ 7.2 billion in 2025.

Rising prevalence of sleep disorders such as obstructive sleep apnea and insomnia, increasing awareness of sleep health, advancements in diagnostic technologies, and expanding sleep centers are driving market growth.

The global market is poised to witness a CAGR of 11.9% between 2025 and 2032.

Growing adoption of AI-powered and wearable sleep monitoring technologies, expansion of home-based sleep testing services, and increasing investments in digital health platforms are creating significant growth opportunities in the market.

Circle Health Group, Cleveland Clinic, Competence Center of Sleep Medicine, and Imperial College Healthcare NHS Trust are some of the key players in the market.