- Healthcare Services

- Sleep Monitoring Apps Market

Sleep Monitoring Apps Market Size, Share, and Growth Forecast, 2026 - 2033

Sleep Monitoring Apps Market by Device Type (Wearable Devices, Non-wearable Devices), By Features (Basic Sleep Tracking, Sleep Staging, Heart Rate Monitoring, Respiratory Monitoring), and Regional Analysis for 2026 - 2033

Sleep Monitoring Apps Market Size and Trends Analysis

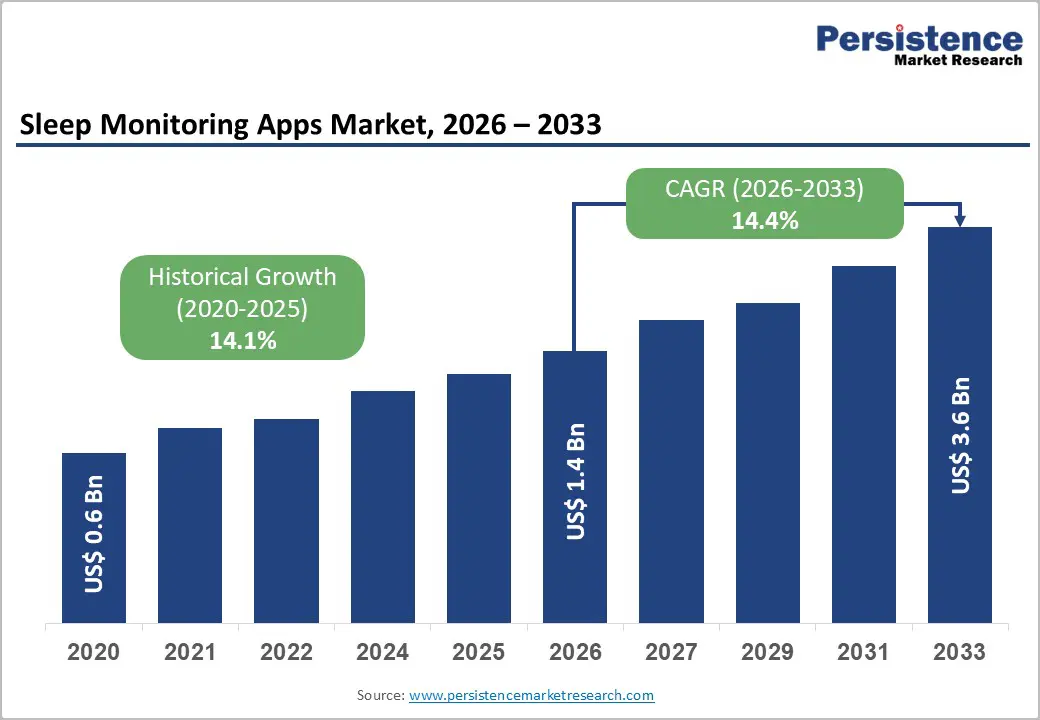

The global sleep monitoring apps market size is likely to be valued at US$1.4 billion in 2026 and is expected to reach US$3.6 billion by 2033, growing at a CAGR of 14.4% during the forecast period from 2026 to 2033, driven by the rising prevalence of sleep disorders, increasing consumer awareness of sleep health, and growing adoption of smartphones and wearable devices.

The widespread penetration of smartphones, smartwatches, and fitness wearables has accelerated adoption by enabling convenient, non-invasive sleep tracking. Advancements in AI-powered analytics, cloud computing, and sensor technologies are improving data accuracy and enabling greater personalization, allowing individuals to obtain actionable insights without relying on traditional clinical sleep studies. These developments, coupled with the increasing emphasis on preventive healthcare and wellness-driven lifestyles, are shaping the future of health monitoring.

Key Industry Highlights:

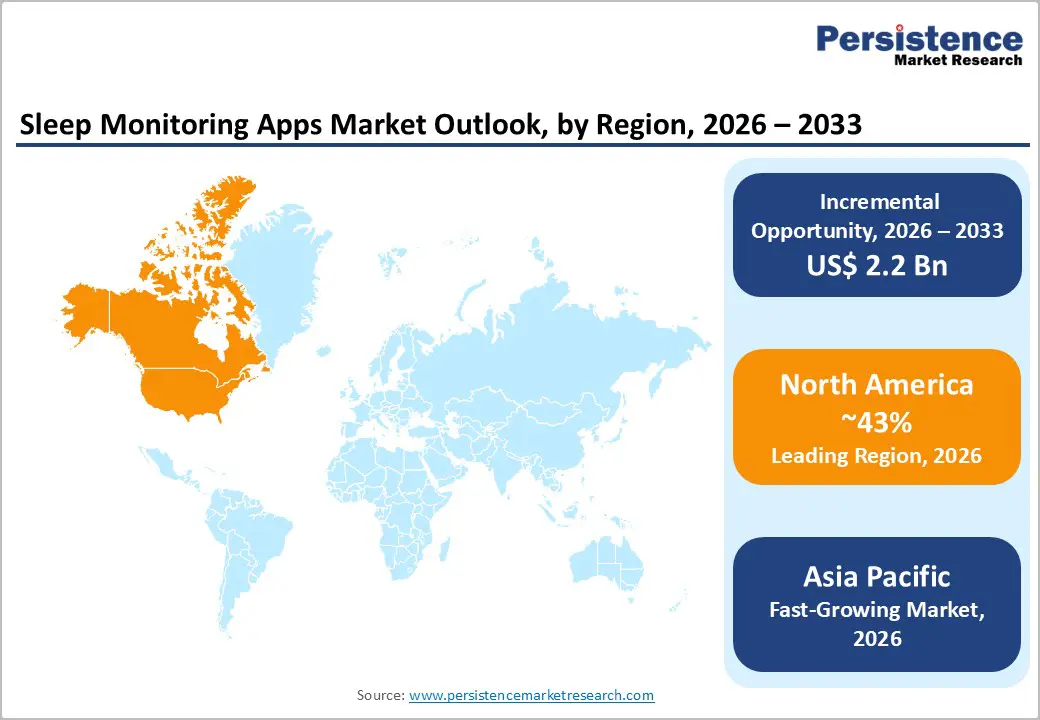

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 43% in 2026, driven by strong digital health adoption, high sleep disorder awareness, and widespread wearable usage.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the sleep monitoring apps in 2026, supported by rapid smartphone penetration, growing health awareness, and strong adoption across China, Japan, India, and ASEAN countries.

- Leading Device Type: Wearable devices are projected to represent the leading device type in 2026, accounting for 75% of the revenue share, due to widespread adoption of smartwatches and fitness bands for continuous and accurate sleep monitoring.

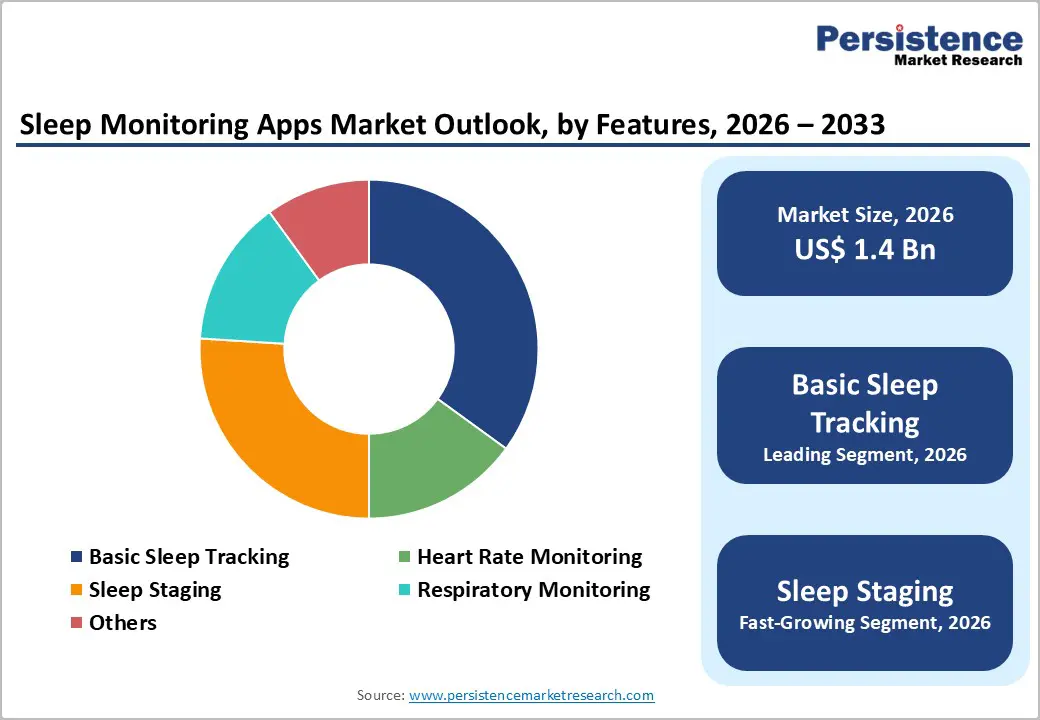

- Leading Features Type: Basic sleep tracking is anticipated to be the leading features type, accounting for over 50% of the revenue share in 2026, supported by easy accessibility and broad usage through smartphone-based applications.

| Key Insights | Details |

|---|---|

| Sleep Monitoring Apps Market Size (2026E) | US$1.4 Bn |

| Market Value Forecast (2033F) | US$3.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 14.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Sleep Disorders and Growing Health Awareness

Conditions such as insomnia, sleep apnea, restless leg syndrome, and circadian rhythm disruptions are becoming increasingly common due to stressful lifestyles, extended screen exposure, irregular work schedules, and urbanization. Many adults experience chronic sleep deprivation, which is strongly linked to cardiovascular disease, obesity, diabetes, depression, and reduced productivity. In May 2024, the U.S. Centers for Disease Control and Prevention (CDC) reported that approximately 35% of U.S. adults are getting less than the recommended seven hours of sleep per night, highlighting a widespread issue of chronic sleep deprivation. This growing burden has significantly increased public awareness about the importance of sleep as a critical pillar of overall health, alongside diet and physical activity. Consumers are proactively seeking digital tools that help them understand, track, and improve sleep quality. Sleep monitoring apps offer an accessible, cost-effective, and non-invasive alternative to clinical sleep studies, making them attractive for early detection and self-management.

The growing adoption of cloud-based platforms and IoT-integrated technologies is another key driver shaping the market. Modern sleep apps increasingly rely on cloud infrastructure to store, process, and analyze large volumes of sleep data collected from smartphones, wearables, and connected devices. Cloud integration enables real-time data synchronization, long-term trend analysis, and seamless updates, enhancing user experience and scalability. IoT connectivity allows sleep apps to integrate with smartwatches, fitness bands, smart rings, and home-based sensors such as under-mattress monitors and smart beds. This interconnected ecosystem improves data accuracy by combining multiple physiological parameters, including movement, heart rate, breathing patterns, and ambient conditions.

Accuracy Limitations of Consumer-Grade Apps

Clinical sleep diagnostics, such as polysomnography, measure brain activity, eye movement, muscle tone, and respiration simultaneously, whereas most consumer sleep monitoring apps rely on indirect signals, including motion tracking, heart rate variability, and audio-based snoring detection. These proxy indicators can misclassify sleep stages, underestimate wake periods, or fail to accurately detect conditions such as obstructive sleep apnea. Differences in device sensors, smartphone placement, wearable fit, and user movement patterns contribute to inconsistent results. Users may receive misleading sleep scores or recommendations, which can reduce confidence in the app's reliability. This accuracy gap limits the use of consumer-grade apps for medical decision-making and restricts their acceptance among clinicians.

The perceived accuracy limitations of sleep monitoring apps directly affect user trust, long-term engagement, and broader market adoption. Many users abandon apps after short-term use when tracked results conflict with subjective sleep experiences or clinical diagnoses. This trust gap is especially pronounced among individuals with chronic sleep disorders who require precise monitoring to manage symptoms effectively. From a healthcare perspective, physicians often hesitate to integrate consumer sleep data into treatment plans due to variability and a lack of standardized validation protocols. This restricts collaboration between app developers and medical institutions, limiting reimbursement opportunities and clinical partnerships.

Aging Population and Corporate Wellness

As life expectancy rises across both developed and emerging economies, older adults are becoming more prone to sleep-related disorders such as insomnia, sleep apnea, restless leg syndrome, and fragmented sleep patterns. These issues stem from physiological changes, chronic conditions, and medication use. As a result, there is an increasing demand for accessible, continuous, and non-invasive tools to monitor sleep health among seniors. Sleep monitoring apps, especially when integrated with wearables and home-based sensors, enable long-term tracking of sleep trends without the need for frequent clinical visits. These solutions support early identification of irregular sleep patterns, helping caregivers and healthcare providers manage risks for cardiovascular disease, cognitive decline, and falls.

Recent research, such as a study funded by the National Heart, Lung, and Blood Institute (NHLBI) in March 2024, highlights the strong link between poor sleep and chronic conditions such as cardiovascular disease and diabetes. The observational study, which included over 3,000 adults, found that those who regularly experienced insomnia or frequent sleep disruptions were significantly more likely to report these chronic conditions compared to those who enjoyed adequate sleep. This underscores the importance of sleep quality for overall health, particularly in managing cardiometabolic risks, and emphasizes the need for solutions such as sleep-monitoring apps to help identify sleep disruptions early.

Sleep monitoring apps are also becoming a vital component of corporate wellness initiatives. As employers increasingly recognize the impact of sleep quality on productivity, mental health, and employee engagement, there is growing investment in digital wellness solutions. Poor sleep is linked to absenteeism, burnout, reduced concentration, and higher healthcare costs, underscoring the importance of sleep monitoring for businesses. These apps are being integrated into corporate health platforms, helping employees track sleep patterns, manage stress, and improve overall well-being. Partnerships between app developers, insurers, and employers are expanding access to these tools through subsidized subscriptions and incentive-based programs, further driving their adoption in the workplace.

Category-wise Analysis

Device Type Insights

Wearable devices are expected to lead the market, accounting for approximately 75% of revenue in 2026, due to their ability to deliver continuous, real-time sleep and health data. Smartwatches and fitness bands equipped with motion, heart rate, and blood oxygen sensors have become integral to everyday health tracking, positioning wearables as the preferred choice for sleep monitoring. The convenience of overnight monitoring without manual input further strengthens adoption among consumers seeking accuracy and ease of use. For example, Apple Watch, which integrates sleep monitoring with the Apple Health ecosystem, offers users consolidated wellness insights and reinforces wearable dominance within the market.

Non-wearable devices are likely to represent the fastest-growing segment in 2026, driven by increasing demand for non-intrusive and contact-free sleep tracking solutions. These devices, such as bedside monitors, under-mattress sensors, and smart beds, appeal to users who find wearables uncomfortable or disruptive during sleep. This segment is gaining traction among older adults and households prioritizing convenience and minimal user intervention. Non-wearable solutions are increasingly positioned as family-wide or shared health-monitoring tools rather than as individual devices. For example, Withings Sleep Analyzer, an under-mattress sensor that connects to a mobile app to provide detailed sleep insights without requiring the user to wear any device, highlights the strong growth potential of this segment.

Features Type Insights

Basic sleep tracking is projected to lead the market, capturing around 50% of revenue share in 2026, driven by its simplicity, accessibility, and broad appeal. These features typically include sleep duration, sleep-wake cycles, and overall sleep patterns, making them easy for entry-level users to understand. Basic tracking functions are often available through smartphone-only apps, reducing adoption barriers by eliminating the need for additional hardware. This accessibility has driven widespread usage among first-time users and individuals primarily focused on general wellness rather than clinical insights. Its low learning curve and minimal setup requirements contribute to sustained popularity across diverse age groups. For example, Sleep Cycle, which offers intuitive sleep duration and pattern tracking through a smartphone app, demonstrates why basic sleep tracking continues to dominate feature-based segmentation.

Sleep staging is expected to be the fastest-growing segment in 2026, as technological advancements in AI and sensor fusion allow for more accurate and detailed analysis of sleep phases, including light, deep, and REM sleep, offering users deeper insights into their sleep health. Advancements in artificial intelligence and sensor fusion have significantly improved the interpretation of complex physiological signals, increasing user confidence in advanced analytics. The integration of advanced features also supports personalized recommendations, coaching, and long-term health correlations, enhancing perceived value. For example, Fitbit Sleep Stages, which combines sleep phase analysis with heart rate data through its app ecosystem, illustrates how advanced monitoring features are driving rapid growth and deeper engagement in the market.

Regional Insights

North America Sleep Monitoring Apps Market Trends

North America is anticipated to be the leading region, accounting for a market share of 43% in 2026, driven by the rapid adoption of advanced digital health technologies and a strong focus on preventive wellness. A 2024 survey between May 16 and May 24, by the American Academy of Sleep Medicine found that 36 % of U.S. adults have been diagnosed with a sleep-related disorder, including insomnia and obstructive sleep apnea, making sleep disorders a significant health issue. Consumers are increasingly using mobile and wearable devices to gain insights into sleep quality, patterns, and disturbances as part of broader health management. Wearable integration with smartphones, cloud analytics, and AI-driven personalized recommendations are key technological trends shaping the market. Growing awareness of the health impacts of poor sleep, such as links to cardiovascular disease, obesity, and mental health issues, has also accelerated consumer interest in sleep apps. Partnerships between app developers and healthcare providers are facilitating the integration of sleep data into clinical workflows, supporting remote patient monitoring and telehealth services.

Innovation and competitive dynamics are also significant trends in the North America sleep monitoring apps market, with both established tech companies and specialized startups driving rapid development of new features and services. Many players are expanding beyond basic sleep tracking to offer sophisticated functionalities such as sleep staging, respiratory analysis, and integration with broader health platforms. For example, ResMed’s myAir program extends beyond standard tracking by providing personalized sleep therapy feedback linked to its connected CPAP devices, catering to users with clinically diagnosed sleep apnea. Regulatory support, including FDA clearances and health data standards, is reinforcing consumer trust and encouraging investment in clinically relevant capabilities.

Europe Sleep Monitoring Apps Market Trends

Europe is likely to be a significant market for sleep monitoring apps in 2026, as increasing recognition of sleep quality as a cornerstone of overall wellness has encouraged users to adopt digital solutions that monitor sleep duration, patterns, and disturbances. This trend is particularly strong in countries such as the U.K., Germany, France, and the Nordic markets, where lifestyle-related stress and irregular sleep cycles are common among working populations. Europe’s stringent regulatory landscape, including GDPR and the Medical Device Regulation (MDR), ensures robust data privacy and security standards, enhancing user trust in sleep apps. National health initiatives and public wellness programs also promote sleep health as part of preventive healthcare, strengthening demand for tools that can be used at home without clinical intervention.

Innovation and cross-platform integration continue to shape the Europe sleep monitoring apps market, as developers enhance analytical capabilities and expand functional offerings. Advanced features, such as sleep staging, heart rate monitoring, and respiratory pattern analysis, are increasingly incorporated to provide deeper insights into users’ sleep health. These capabilities appeal to consumers looking for more than basic duration tracking, especially those managing long-term wellness goals. For example, Philips has strengthened its footprint in the European sleep tech space with its Philips SleepMapper app, which complements the company’s range of connected sleep solutions by helping users track sleep trends and gain personalized suggestions.

Asia Pacific Sleep Monitoring Apps Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the sleep monitoring apps market in 2026, driven by consumers increasingly embracing digital health technologies and prioritizing wellness. Rising smartphone penetration, expanding internet access, and growing middle-class health awareness are key drivers shaping market trends. Many users are turning to sleep monitoring apps as cost-effective, non-invasive tools to understand sleep quality amid busy urban lifestyles, long working hours, and rising stress levels. Governments across the region, including China, India, Japan, and ASEAN countries, are investing in digital health initiatives and supportive policies that foster the adoption of mobile health solutions. Local health campaigns that highlight the importance of sleep for overall wellness are creating greater demand for sleep tracking tools, particularly among younger and tech-savvy demographics.

Innovation and strategic partnerships are further catalyzing market expansion in the Asia Pacific sleep monitoring apps landscape, with companies enhancing analytics, accuracy, and user experience. Advanced capabilities such as sleep staging, heart rate monitoring, and AI-driven insights are increasingly expected by consumers seeking comprehensive health data beyond basic activity logs. Regional firms and players are collaborating to tailor solutions that address unique market needs, balancing technological sophistication with affordability. For example, Xiaomi, a major electronics and consumer tech brand, integrates sleep-tracking features into its Mi Fit and Zepp Life apps that sync with its smart bands and smartwatches, providing users across Asia Pacific with accessible and reliable sleep insights.

Competitive Landscape

The global sleep monitoring apps market exhibits a moderately fragmented structure, driven by the coexistence of many established tech firms and numerous specialized developers competing for market share. The sector blends wellness-focused relaxation apps with data-centric sleep analytics platforms, ranging from basic sleep duration tracking to advanced multi-parametric monitoring. Consumer preferences for personalized insights, AI-powered recommendations, and seamless integration with wearable ecosystems are shaping competitive dynamics. Developers are enhancing interoperability with smartwatches, smartphones, and home sensors while emphasizing user experience and data privacy.

Key players such as Sleep Cycle, Calm, Pillow, and Headspace have built strong brand recognition and compete by driving innovation, forming strategic partnerships, and ensuring broad platform support. These companies focus heavily on AI advancements, collaborations with wearable device manufacturers, and aggressive marketing to increase their visibility. They also utilize subscription models, freemium approaches, localized content, and unique features such as guided sleep sessions or clinical-grade analytics to retain users and build loyalty. As competition intensifies, success in the evolving sleep monitoring app market will increasingly depend on cross-platform compatibility, enhanced accuracy, and adherence to regulatory standards.

Key Industry Developments:

- In December 2025, Emma Up, the AI sleep coaching app from Emma The Sleep Company (the world’s largest D2C sleep brand), launched a new sound-based sleep tracking feature that provides personalized lifestyle insights and actionable steps to improve sleep quality without requiring additional devices. Developed in collaboration with sleep experts from Oxford University, the app leverages AI to analyze sleep sounds, delivering more accurate insights than traditional wearables or generic sleep apps. Emma Up addresses these challenges by offering hyper-personalized coaching programs tailored to individual sleep patterns and lifestyle habits, helping users achieve sustainable improvements.

- In June 2025, Sleep Cycle, a leading sleep technology company, announced the launch of a clinical study to validate its upcoming AI-powered smartphone feature for screening and monitoring obstructive sleep apnea (OSA) without requiring additional hardware or wearables. The study, conducted at Sleep Testing Australia clinics in Brisbane and Adelaide with approximately 700 participants, aims to test the accuracy of the app’s proprietary audio analysis algorithm in detecting OSA. Obstructive sleep apnea affects an estimated 950 million adults worldwide, with nearly 80% of cases undiagnosed. Sleep Cycle’s solution leverages smartphone microphones and AI to detect subtle sleep-related breathing patterns, offering a scalable, accessible alternative to traditional clinical sleep studies.

Companies Covered in Sleep Monitoring Apps Market

- Sleep Cycle

- Sleep as Android

- Pillow

- Sleep Better

- Sleep Genius

- Timeshifter

- Calm

- Sleep Stories

- Relax Melodies

- Noisli

Frequently Asked Questions

The global sleep monitoring apps market is projected to reach US$1.4 billion in 2026.

The sleep monitoring apps market is driven by the increasing prevalence of sleep disorders, heightened health awareness, and the growing use of smartphones and wearable devices for easy, non-invasive sleep tracking.

The sleep monitoring apps market is expected to grow at a CAGR of 14.4% from 2026 to 2033.

Key market opportunities include the expanding aging population, the rise of corporate wellness programs, the growing adoption of AI-driven and IoT-connected solutions, and the increasing penetration of smartphones and wearables in emerging markets.

Sleep Cycle, Sleep as Android, Pillow, Sleep Better, Sleep Genius, Timeshifter, Calm, and Sleep Stories are the leading players.