- Medical Devices

- Sleep Apnea Diagnostic Systems Market

Sleep Apnea Diagnostic Systems Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Sleep Apnea Diagnostic Systems Market by Product (Polysomnography (PSG) Devices, Ambulatory PSG Monitoring Devices, Clinical PSG Monitoring Devices, Sleep Apnea Screening Device, Nasal Flow Sensors, and Others), End-user (Hospitals, Sleep Centers and Clinics, and Home Care Settings), and Regional Analysis from 2026 - 2033

Sleep Apnea Diagnostic Systems Market Share and Trends Analysis

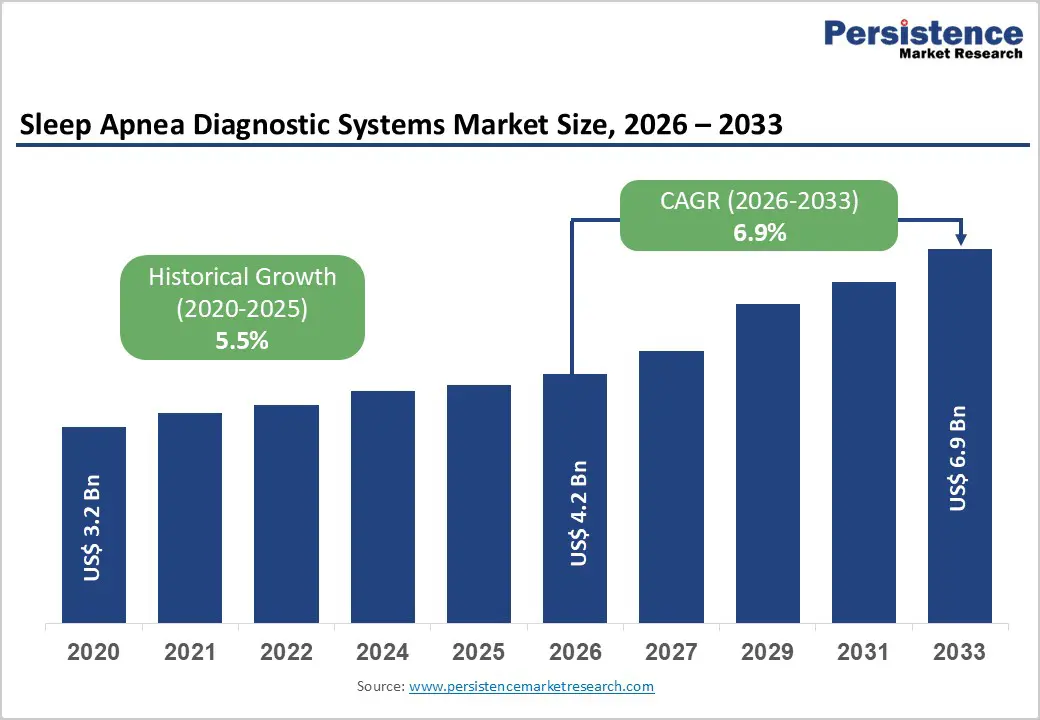

The global sleep apnea diagnostic systems market size is estimated to grow from US$ 4.2 Bn in 2026 to US$ 6.9 Bn by 2033. The market is projected to record a CAGR of 6.9% during the forecast period from 2026 to 2033.

Global demand for sleep apnea diagnostic systems is increasing steadily, driven by the rising prevalence of obstructive and central sleep apnea, growing awareness of sleep-disordered breathing, and increasing rates of obesity and aging populations. Expanding adoption of advanced diagnostic techniques, improved sensor technologies, and precise preoperative and sleep study planning is supporting sustained market growth.

Higher diagnostic volumes for in-lab polysomnography and home sleep testing, coupled with increasing healthcare expenditure and expanding access to specialized sleep centers and hospital-based sleep laboratories, are further accelerating demand. Continuous innovation in portable PSG systems, AI-assisted data analysis, cloud-based reporting, and wearable monitoring devices is improving diagnostic accuracy, reducing patient burden, and enhancing long-term care management. In addition, increasing focus on home-based testing, telemedicine integration, and digital and remote reporting workflows is further propelling the global sleep apnea diagnostic systems market.

Key Industry Highlights:

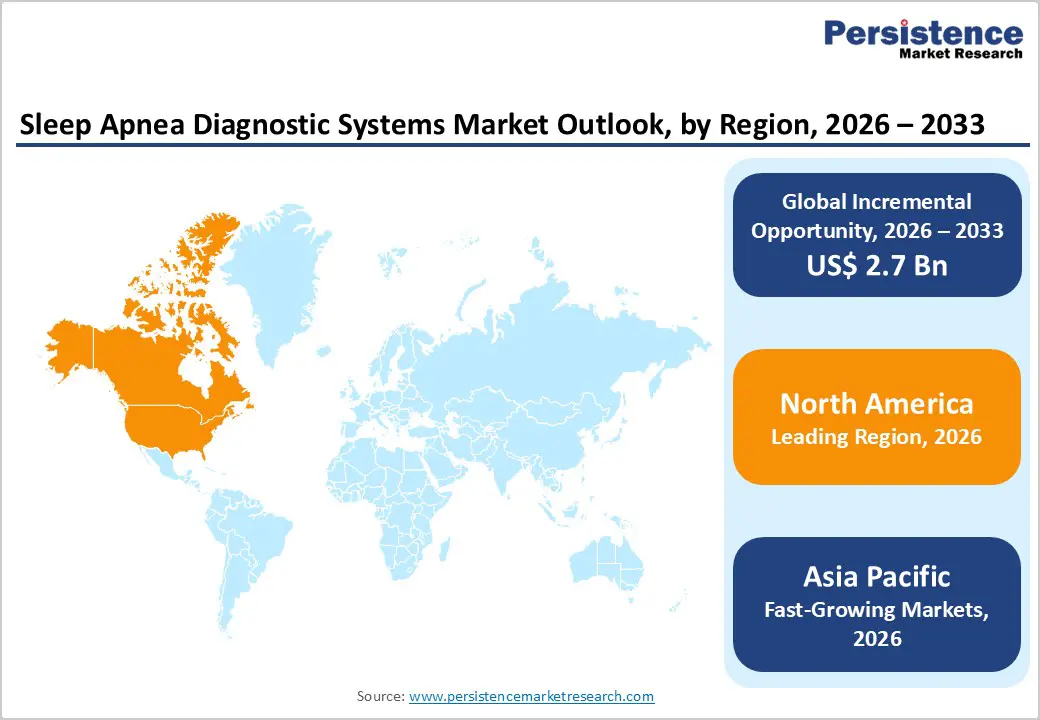

- Leading Region: North America holds the largest share at 48.1%, supported by advanced healthcare infrastructure, high diagnosis and testing rates, early adoption of innovative sleep apnea diagnostic technologies, and the strong presence of leading manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large undiagnosed patient population, rising awareness of sleep disorders, improving healthcare infrastructure, and increasing investments in sleep care services.

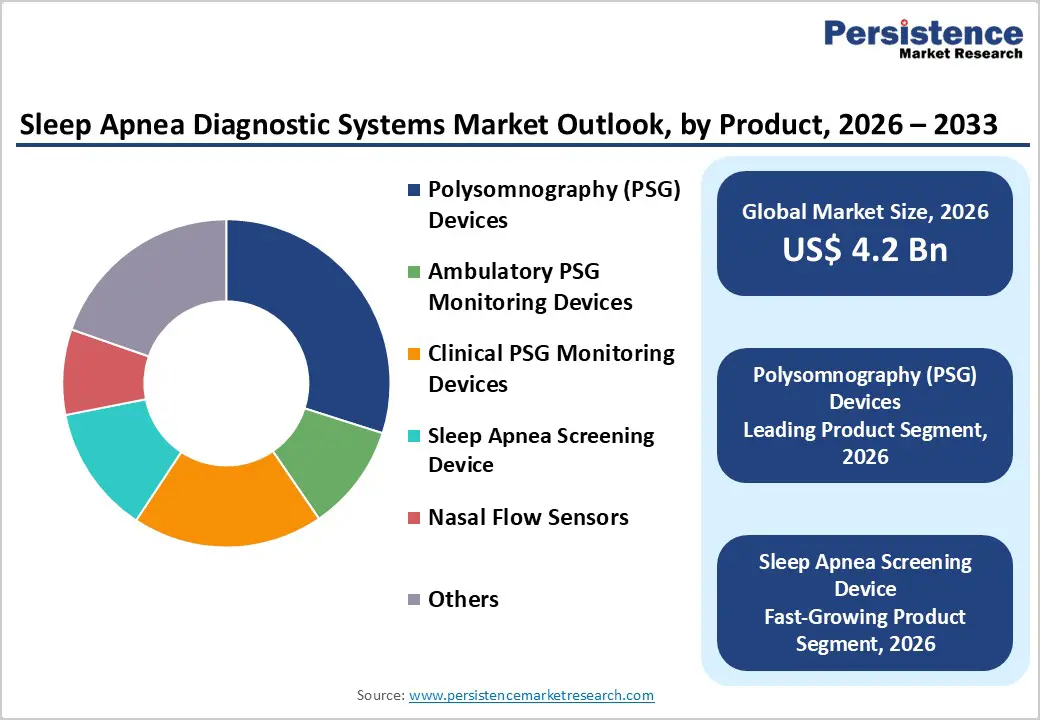

- Leading Product Segment: Polysomnography (PSG) devices dominate the market due to their broad applicability across adult and pediatric patients with sleep apnea.

- Fastest-Growing Product Segment: Sleep apnea screening devices are expanding rapidly as clinicians increasingly adopt them for home-based and preliminary testing where full PSG is not feasible.

- Leading End-user: Hospitals remain the top end-user, driven by high volumes of complex sleep studies and access to advanced diagnostic infrastructure.

- Fastest-Growing End-user: Sleep centers and clinics are scaling quickly as demand rises for specialized testing, follow-up care, and outpatient sleep management services.

| Key Insights | Details |

|---|---|

|

Sleep Apnea Diagnostic Systems Market Size (2026E) |

US$ 4.2 Bn |

|

Market Value Forecast (2033F) |

US$ 6.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5 % |

Market Dynamics

Driver - Rising Prevalence, Technological Advancements, and Awareness Driving Market Growth

The global sleep apnea diagnostic systems market is witnessing robust growth driven by rising disease prevalence, rapid technological advancements, and increasing awareness among patients and healthcare providers. The incidence of obstructive and central sleep apnea is climbing globally, driven primarily by factors such as obesity, aging populations, sedentary lifestyles, and co-morbid conditions like cardiovascular disease and diabetes. For instance, in 2023, according to ResMed, approximately 936 million people worldwide are affected by sleep apnea across all severities. Of these, over 200 million women are estimated to have mild obstructive sleep apnea, representing about 13.4% of females aged 30–70. In the U.S., more than 54 million individuals are affected by the condition. This expanding patient pool is fueling demand for accurate, timely, and accessible diagnostic solutions. Simultaneously, public health initiatives, clinician-driven screening programs, and educational campaigns are enhancing awareness about the importance of early diagnosis and treatment, resulting in higher adoption rates of diagnostic systems across hospitals, sleep centers, and home-care settings.

Technological innovation is further amplifying market growth by improving the convenience, accuracy, and efficiency of sleep apnea diagnostics. Portable and home-based polysomnography (PSG) systems, wearable monitoring devices, and remote patient monitoring solutions are enabling diagnosis outside traditional sleep laboratories. AI-enabled analytics, cloud-based reporting platforms, and integrated software solutions are enhancing data interpretation, reducing manual errors, and enabling personalized treatment planning. These technological advancements, combined with rising awareness and screening initiatives, are not only expanding the reach of diagnostic services but also driving greater adoption in both developed and emerging markets, reinforcing sustained market growth globally.

Restraints - High Costs and Underdiagnosis Challenges in Sleep Apnea Diagnostics

The high cost of advanced sleep apnea diagnostic equipment remains a major restraint on market growth, particularly in price-sensitive regions. Polysomnography (PSG) systems, both in-lab and portable, involve significant capital investment, sophisticated sensors, and integrated software platforms, making them expensive for hospitals, sleep centers, and individual patients. Home sleep testing devices, while relatively more affordable, still require procurement of reliable monitoring kits and technical support, which can limit adoption in markets with constrained healthcare budgets. Additionally, ongoing maintenance, calibration, and software subscription costs further add to the financial burden for healthcare providers. These high costs often limit the penetration of advanced diagnostic technologies in developing regions, restricting access to accurate and timely sleep apnea evaluation.

Moreover, underdiagnosis and low awareness in many low- and middle-income countries exacerbate the challenge. Many patients remain undiagnosed due to limited access to specialized sleep laboratories, a lack of trained clinicians, and insufficient public health education regarding sleep disorders. Cultural perceptions, low prioritization of sleep health, and minimal insurance coverage also contribute to delayed diagnosis. As a result, a significant portion of the population with sleep-disordered breathing remains untreated, leading to higher rates of comorbidities such as hypertension, cardiovascular diseases, and impaired cognitive function. Addressing these issues is crucial to expanding the reach and impact of sleep apnea diagnostic systems globally.

Opportunity - Emerging Opportunities in Wearable and Home-Based Sleep Apnea Diagnostics

The rapid development of wearable and connected diagnostic technologies is creating significant growth opportunities in the sleep apnea diagnostic systems market. Advanced wearable devices, including wristbands, headbands, and smart patches, equipped with sensors for airflow, oxygen saturation, heart rate, and respiratory effort, enable continuous, non-invasive patient monitoring in real-world settings. Integration with IoT-enabled platforms allows seamless data collection, storage, and analysis, facilitating remote monitoring and early detection of sleep-disordered breathing. These innovations enhance patient convenience, improve adherence to diagnostic protocols, and provide clinicians with detailed insights for personalized treatment planning. Additionally, AI-enabled analytics and cloud-based reporting enhance the accuracy and efficiency of diagnostics, making wearable solutions an attractive complement to traditional in-lab polysomnography systems.

Furthermore, the shift toward home-based sleep testing is gaining momentum, driven by patient preference for comfort, privacy, and convenience. Home sleep apnea testing (HSAT) devices, often portable and easy to use, allow patients to conduct sleep studies in their natural environment, reducing the need for overnight hospital visits. Telemedicine integration further supports remote interpretation of results and follow-up consultations, expanding access to underserved populations and rural regions. This transition not only alleviates pressure on sleep laboratories but also lowers overall diagnostic costs, increasing adoption rates. Together, wearable and home-based diagnostic solutions are redefining sleep apnea management and expanding market opportunities.

Category-wise Analysis

By Product, Polysomnography (PSG) Devices Dominate Globally Due to Comprehensive Diagnostic Capability

The polysomnography (PSG) devices segment is projected to dominate the global sleep apnea diagnostic systems market in 2026, accounting for a revenue share of 42.6%. This leadership is primarily driven by PSG’s role as the clinical gold standard for diagnosing obstructive and central sleep apnea, given its ability to simultaneously monitor multiple physiological parameters, including airflow, respiratory effort, oxygen saturation, EEG, and cardiac activity. PSG devices are widely used across both adult and pediatric populations for accurate disease severity assessment and therapy planning. The rising prevalence of obesity, aging populations, and increasing awareness of sleep-disordered breathing are reinforcing demand. Technological advancements such as portable and ambulatory PSG systems, improved sensor accuracy, AI-assisted data interpretation, and cloud-based reporting platforms further enhance adoption. Strong reimbursement support in developed markets and expanding access in emerging economies continue to sustain PSG’s dominant global position.

By End-user, Hospitals Dominate Globally Due to High Diagnostic Volumes and Advanced Infrastructure

The hospitals segment is projected to dominate the global sleep apnea diagnostic systems market in 2026, accounting for a revenue share of 58.2%. This dominance is driven by the high volume of in-lab polysomnography and complex sleep studies conducted in hospital settings, which require advanced diagnostic infrastructure and multidisciplinary clinical expertise. Hospitals are equipped with dedicated sleep laboratories, trained sleep specialists, respiratory therapists, and access to advanced imaging and monitoring technologies. Strong investment in diagnostic equipment, ability to manage complex and comorbid cases, and integration with broader respiratory and cardiology services further reinforce hospital leadership. Additionally, centralized procurement models, long-term supplier agreements, and a preference for comprehensive, high-end diagnostic platforms significantly contribute to hospital-led revenue generation.

Regional Insights

North America Sleep Apnea Diagnostic Systems Market Trends

North America is expected to dominate the global Sleep Apnea Diagnostic Systems market with a value share of 48.1% in 2026, led primarily by the U.S. The region benefits from a well-established healthcare infrastructure, high awareness and diagnosis rates of obstructive and central sleep apnea, and widespread access to advanced diagnostic technologies. Favorable reimbursement policies for in-lab polysomnography and home sleep apnea testing under public and private insurance programs continue to support strong adoption across hospitals and sleep centers. Early uptake of technologically advanced solutions, including portable PSG systems, wearable sensors, and AI-enabled data analytics platforms, further drives diagnostic volumes.

Market growth is also boosted by the strong presence of leading global manufacturers, active R&D investments, and standardized clinical guidelines supporting early diagnosis. In addition, increasing use of telemedicine, cloud-based reporting, and remote patient monitoring improves diagnostic efficiency and patient compliance. Supportive regulatory pathways and collaborations between academic institutions, sleep laboratories, and industry players continue to accelerate innovation and commercialization, sustaining North America’s market leadership.

Europe Sleep Apnea Diagnostic Systems Market Trends

Europe's sleep apnea diagnostic systems market is expected to grow steadily, supported by an aging population, rising prevalence of obesity-related sleep disorders, and increasing awareness of the clinical and economic burden of untreated sleep apnea. Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate consistent diagnostic volumes, driven by universal healthcare coverage, structured referral pathways, and strong primary care involvement. High acceptance of both in-lab polysomnography and home sleep testing solutions supports balanced market growth. Expansion is further encouraged by the adoption of advanced diagnostic systems offering improved signal accuracy, integrated software platforms, and interoperability with electronic health records.

Favorable regulatory frameworks, reimbursement support, and public healthcare funding enhance accessibility across multiple European markets. Ongoing collaboration between academic research centers, sleep clinics, and device manufacturers continues to advance clinical validation and innovation. Additionally, integration of digital health tools, standardized diagnostic protocols, and outcome-based care models is improving efficiency and long-term patient management across the region.

Asia Pacific Sleep Apnea Diagnostic Systems Market Trends

Asia Pacific Sleep Apnea Diagnostic Systems market is expected to register a relatively higher CAGR of around 8.7% between 2026 and 2033, driven by expanding healthcare infrastructure and a rapidly growing undiagnosed patient population. Large populations, rising obesity rates, and increasing awareness of sleep-related disorders are fueling demand across China, India, Japan, South Korea, and Southeast Asia. Improving access to sleep laboratories, growth of private hospitals, and rising investments in diagnostic capabilities are accelerating adoption.

Government-led initiatives promoting early screening, non-communicable disease management, and broader insurance coverage are supporting market expansion in several countries. Cost-effective diagnostic devices, local manufacturing, and regional distribution partnerships are improving affordability in price-sensitive markets. Global players are increasingly focusing on localization strategies, clinician training, and channel expansion. The gradual adoption of portable diagnostic systems, digital reporting platforms, and telemedicine-enabled sleep diagnostics is expected to strengthen long-term growth prospects across Asia Pacific.

Competitive Landscape

The global sleep apnea diagnostic systems market is highly competitive, with strong participation from companies such as Koninklijke Philips N.V., BD, Braedon Medical Corporation, Advanced Brain Monitoring Inc., SOMNOmedics AG, and ResMed. These players leverage extensive global distribution networks, strong brand recognition, and continuous innovation in diagnostic technologies, sensor accuracy, data analytics, and connected sleep monitoring platforms to address a broad spectrum of sleep-disordered breathing conditions.

Rising demand for early diagnosis, home-based sleep testing, and improved diagnostic accuracy is driving product innovation and portfolio expansion. Manufacturers are increasingly focused on portable and ambulatory PSG systems, advanced airflow and respiratory effort sensors, AI-enabled data interpretation, and cloud-based reporting platforms. Key strategic priorities include clinician and sleep technologist training, integration of digital health and tele-sleep solutions, expansion across emerging markets, and strengthening long-term partnerships with hospitals, sleep laboratories, and specialty clinics to maintain competitive positioning and support sustained market growth.

Key Industry Developments:

- In December 2025, SleepRes Inc. received FDA 510(k) clearance for its Kricket PAP device to treat obstructive sleep apnea in patients over 66 pounds. The device uses Kairos Positive Airway Pressure technology to enhance comfort and adherence and is approved for home, hospital, and sleep center use, offering a patient-friendly alternative to conventional PAP therapies.

- In August 2025, Nyxoah announced FDA approval of its Genio system for adults with moderate to severe obstructive sleep apnea (AHI 15–65). The wearable device delivers bilateral hypoglossal nerve stimulation as an alternative to CPAP therapy and has previously received CE marking in the EU.

Companies Covered in Sleep Apnea Diagnostic Systems Market

- Koninklijke Philips N.V.

- BD

- Braedon Medical Corporation

- Advanced Brain Monitoring Inc.

- SOMNOmedics AG

- Resmed

- BMC

- Natus Medical Incorporated

- CAIRE Inc.

- Beacon Bio Dx, LLC. (d.b.a. CleveMed)

- Medtronic

- Invacare Corporation

- Koike Medical Co., Ltd.

- SleepMed

- Others

Frequently Asked Questions

The global sleep apnea diagnostic systems market is projected to be valued at US$ 4.2 Bn in 2026.

Rising prevalence of sleep apnea due to obesity and aging, increasing awareness and screening, and technological innovations in portable and AI-enabled diagnostic tools are primary growth drivers.

The global sleep apnea diagnostic systems market is poised to witness a CAGR of 6.9% between 2026 and 2033.

Integration of telemedicine and remote monitoring capabilities into diagnostic systems presents a significant growth opportunity.

Koninklijke Philips N.V., BD, Braedon Medical Corporation, Advanced Brain Monitoring Inc., SOMNOmedics AG, and Resmed are some of the key players in the sleep apnea diagnostic systems market.