- Medical Devices

- Health and Wellness Devices Market

Health and Wellness Devices Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Health and Wellness Devices Market by Product Type (Wearable Devices, Medical Devices for Wellness, Therapy & Relaxation Devices, Nutrition & Weight Management Devices, Others), Application (Chronic Disease Management, Fitness and Wellness Monitoring, Personal Care, Mental Health and Stress Relief), End-use, and Regional Analysis for 2025 - 2032

Health and Wellness Devices Market Size and Trends Analysis

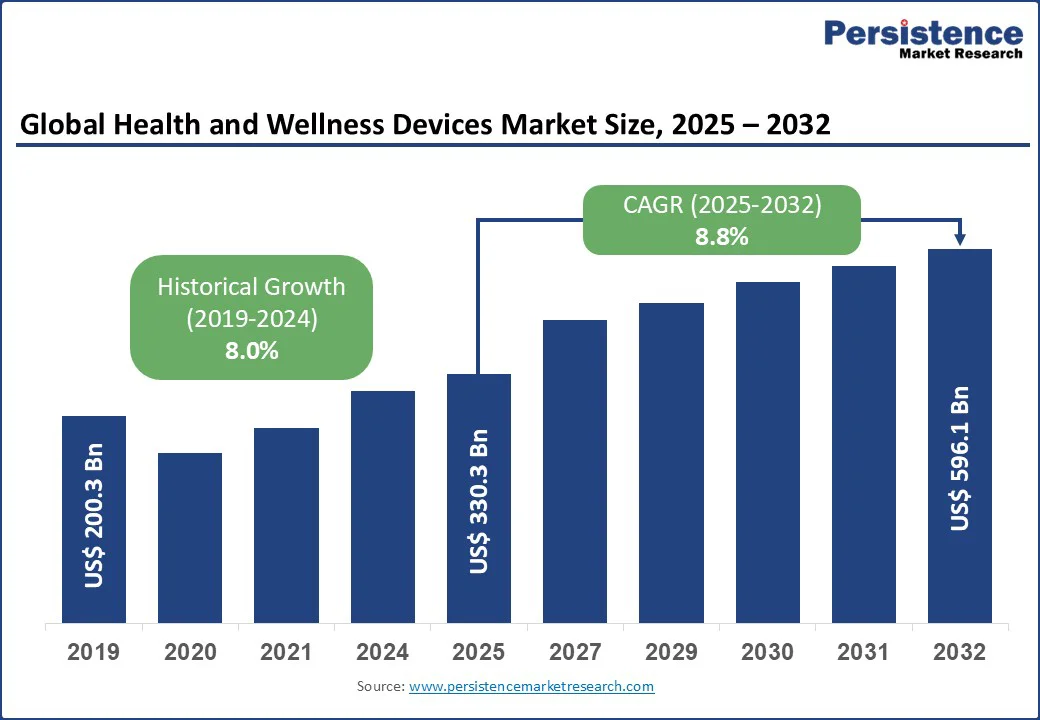

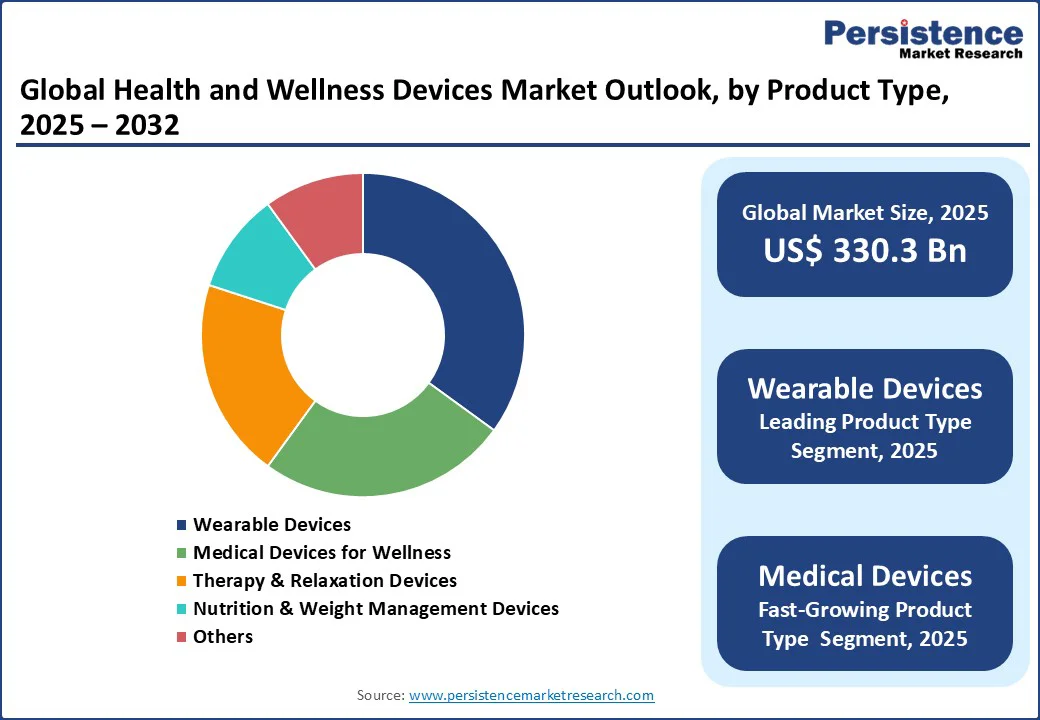

The global health and wellness devices market size is likely to be valued at US$330.3 Bn in 2025 and is expected to reach US$596.1 Bn by 2032, growing at a CAGR of 8.8% during the forecast period 2025-2032.

Key Industry Highlights:

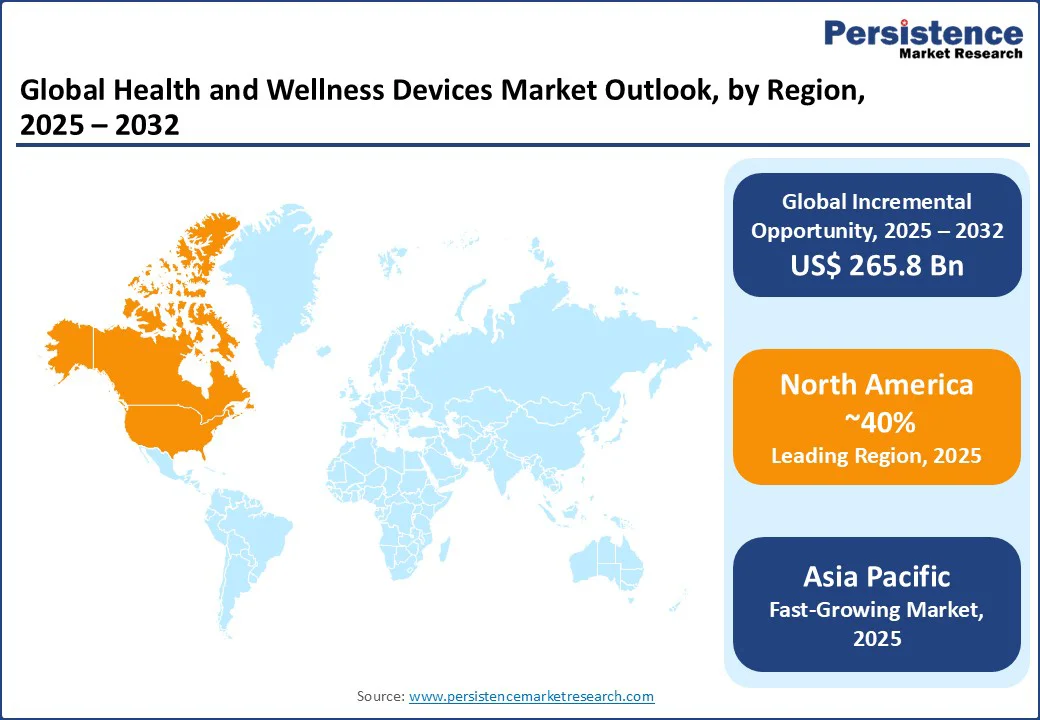

- Leading Region: North America accounts for a 40% share in 2025, driven by high adoption of wearable devices in the U.S.

- Dominant Product Type: Wearable devices account for 50% of the market share in 2025, led by smartwatches and fitness trackers.

- Leading Application: Chronic disease management contributes 35% of revenue, driven by demand for medical devices for wellness.

- Leading End-use: Individual/home users are fueled by consumer demand for fitness and wellness monitoring.

- Key Trend: Integration of AI and IoT in wearable devices for real-time health insights and personalized care.

|

Global Market Attribute |

Key Insights |

|

Health and Wellness Devices Market Size (2025E) |

US$330.3 Bn |

|

Market Value Forecast (2032F) |

US$596.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.0% |

The market's growth is propelled by increasing health consciousness, technological advancements in wearable devices such as smartwatches and fitness trackers, and the growing prevalence of chronic diseases such as diabetes and cardiovascular conditions. The integration of artificial intelligence (AI) and Internet of Things (IoT) in health and wellness devices enhances functionality, enabling real-time health monitoring and personalized insights.

Market Dynamics

Drivers - Increasing Prevalence of Chronic Diseases

The rising prevalence of chronic diseases, such as diabetes, cardiovascular diseases, and obesity, is a primary driver for the health and wellness devices market, as consumers and healthcare providers seek advanced solutions for chronic disease management. According to the World Health Organization (WHO), chronic diseases account for 60% of global deaths, with North America and Europe reporting high incidences of diabetes and cardiovascular conditions. Medical devices for wellness, such as continuous glucose monitors (CGMs) from DexCom Inc., and wearable devices such as heart rate monitors from Garmin Ltd., enable real-time monitoring, improving patient outcomes by up to 25% through early intervention.

For instance, in the U.S., Fitbit’s heart rate trackers have helped users detect atrial fibrillation, leading to timely medical consultations, with over 500,000 users reporting early detection of heart irregularities in 2025. In the Asia Pacific, countries such as China and India see rising demand for nutrition & weight management devices due to increasing obesity rates. The integration of AI in wearable devices provides personalized health insights, driving adoption among individual/home users.

Restraints - High Costs of Advanced Devices

The high cost of advanced health and wellness devices, particularly wearable devices and medical devices for wellness, poses a significant restraint, limiting adoption among price-sensitive consumers and smaller hospitals and clinics. This creates a gap in accessibility between large healthcare institutions in developed countries and smaller providers or consumers in emerging markets.

Premium wearable devices, such as Fitbit smartwatches, can cost US$200–500. In contrast, CGMs and advanced therapy & relaxation devices require ongoing subscription fees, which deter individual/home users in developing regions, including parts of the Asia Pacific. Maintenance and software updates further increase costs, impacting affordability in sports and fitness centers, where budgets are often constrained. While the demand for health and wellness devices continues to grow globally, cost remains a limiting factor, slowing adoption in regions and customer segments where price sensitivity is high.

Opportunities - Expansion of Digital Health Platforms

The expansion of digital health platforms and telehealth services presents a transformative opportunity for the health and wellness devices market, as consumers increasingly rely on connected ecosystems for fitness and wellness monitoring and chronic disease management.

The integration of wearable devices with mobile apps and cloud-based platforms enables real-time data sharing, improving user engagement by 40%. Companies such as Koninklijke Philips NV and Garmin Ltd. are developing IoT-enabled health and wellness devices, offering seamless connectivity with telehealth services.

For instance, Philips’ HealthSuite platform integrates with CGMs and fitness trackers, enabling remote patient monitoring in North America, where 30% of healthcare visits were conducted virtually in 2025. Partnerships with digital health platforms and hospitals, and clinics in Europe and the Asia Pacific enhance market reach, particularly for mental health and stress relief devices, driving growth across diverse applications.

Category-wise Analysis

Product Type Insights

Wearable devices dominate with a 50% market share in 2025, driven by their versatility, affordability, and widespread consumer appeal. Devices such as smartwatches and fitness trackers from Fitbit and Garmin Ltd. are popular among individual/home users for fitness and wellness monitoring, offering features such as heart rate tracking, step counting, and sleep analysis.

Medical devices for Wellness are the fastest-growing segment, driven by rising demand for continuous glucose monitors (CGMs) and blood pressure monitors for chronic disease management. Innovations in non-invasive monitoring technologies, such as Vital Connect’s wearable biosensors, further accelerate adoption among individual/home users seeking convenient health management solutions.

Application Insights

Chronic disease management holds a 35% share in 2025, driven by the need for devices such as CGMs, heart rate monitors, and pulse oximeters to manage conditions such as diabetes and cardiovascular diseases. In North America, 15% of adults use CGMs, boosting demand in hospitals and clinics. The segment benefits from regulatory approvals, such as FDA clearance for DexCom’s G7 CGM, and reimbursement policies in Europe, which cover 50% of CGM costs in countries such as Germany.

Mental health and stress relief is the fastest-growing segment, fueled by the increase in stress-related disorders affecting 30% of the global population. Therapy & relaxation devices, such as neurostimulation systems from OMRON Corporation, are gaining traction among individual/home users in Asia Pacific, supported by mental health awareness campaigns and telehealth integration.

End-use Insights

Individual/Home users dominate with a 55% market share in 2025, driven by consumer demand for wearable devices and nutrition & weight management devices for personal health tracking. In North America, 70% of adults own a fitness tracker, with brands such as Fitbit and Garmin leading due to their user-friendly interfaces and affordability.

Hospitals and Clinics are the fastest-growing segment, fueled by the adoption of medical devices for wellness for chronic disease management. Europe’s advanced healthcare infrastructure, particularly in Germany, supports the integration of CGMs and biosensors in clinical settings.

Regional Insights

North America Health and Wellness Devices Market Trends

North America holds a 40% market share in 2025, with the United States as the primary contributor, driven by a health-conscious population and advanced healthcare infrastructure. The U.S. market benefits from high adoption of wearable devices, with 60% of adults using fitness trackers or smartwatches for fitness and wellness monitoring, according to a 2024 Pew Research study. The high prevalence of chronic diseases, such as diabetes (11% of adults) and cardiovascular conditions (12% of adults), drives demand for chronic disease management devices such as CGMs from DexCom Inc and Abbott. For instance, DexCom’s G7 CGM has seen a 30% adoption rate among diabetic patients in the U.S. due to its non-invasive design and real-time data integration with smartphones.

The U.S.’s Affordable Care Act and private insurance reimbursement policies cover up to 70% of CGM costs, boosting adoption in hospitals and clinics. The rise of telehealth, with 30% of healthcare visits conducted virtually in 2025, enhances demand for wearable devices integrated with platforms such as Teladoc, enabling remote monitoring for mental health and stress relief. The growing popularity of sports and fitness centers, with 25,000 gyms in the U.S., drives demand for nutrition & weight management devices such as smart scales from Withings

Europe Health and Wellness Devices Market Trends

Europe accounts for a 30% share in 2025, with Germany, France, and the UK as leading countries, driven by advanced healthcare systems, aging populations, and increasing health awareness. Germany leads with a 12% regional market share, fueled by high adoption of medical devices for wellness in hospitals and clinics for chronic disease management. The country’s aging population drives demand for CGMs and blood pressure monitors, with Medtronic’s devices seeing a 25% adoption rate in German hospitals. Germany’s Statutory Health Insurance system reimburses 60% of device costs, boosting accessibility.

France is the expected to experience fastest-growth in Europe, driven by rising demand for mental health and stress relief devices, such as neurostimulation systems from OMRON Corporation, amid increasing stress-related disorders. France’s universal healthcare system supports adoption in hospitals and clinics, with 20% of diabetic patients using CGMs.

The UK emphasizes wearable devices for fitness and wellness monitoring, with 50% of adults owning a fitness tracker, driven by NHS programs promoting preventive care. The UK’s focus on mental health, supported by campaigns such as Time to Change, boosts demand for therapy & relaxation devices. The rise of e-commerce platforms and telehealth services in Europe enhances distribution, particularly for individual/home users, driving market expansion across the region.

Asia Pacific Health and Wellness Devices Market Trends

Asia Pacific is the fastest-growing region, with a 25% market share in 2025, led by China, India, and Japan, driven by rapid urbanization, rising healthcare expenditure, and growing health consciousness. China holds the largest share in the region fueled by healthcare reforms and increasing obesity rates driving demand for nutrition & weight management devices such as smart scales from Withing’s. The country’s Healthy China 2030 initiative promotes preventive care, boosting adoption of wearable devices in sports and fitness centers.

India is the fastest-growing country in the region, driven by a growing middle class and medical tourism, increasing demand for wearable devices for personal care, such as skin health monitors from Samsung Electronics. India’s Ayushman Bharat program supports hospitals and clinics in adopting medical devices for wellness, with 15% of diabetic patients using CGMs.

Japan’s aging population fuels demand for chronic disease management devices, with OMRON’s blood pressure monitors seeing a 20% adoption rate in hospitals and clinics. The region’s rapid digitalization, with 50% of Asians using health apps, supports the integration of wearable devices with telehealth platforms, enhancing fitness and wellness monitoring.

Competitive Landscape

The global health and wellness devices market is highly competitive, with key players focusing on innovation, digital integration, and sustainability to capture market share. Companies leverage AI and IoT to develop advanced wearable devices and medical devices for wellness, enhancing user experience and clinical outcomes. Strategic partnerships with telehealth platforms, hospitals and clinics, and sports and fitness centers expand market reach, while mergers and acquisitions strengthen product portfolios.

Key Developments

- In February 2024, Amazfit, a smart wearable brand owned by Zepp Health, a health technology company, introduced the Amazfit Active Smartwatch. The device provides a readiness score, which derives data from stress, heart rate, sleep, respiration, temperature, and HRV. By considering both mental and physical recovery, the score provides personalized suggestions, contributing to overall well-being.

- In April 2024: Dexcom expanded its distribution network in Southest Asia by partnering with post-surgical patients, which was supported by a collaboration with private hospitals chains to reduce readmission rates and enhance care continuity.

Companies Covered in Health and Wellness Devices Market

- OMRON Corporation

- Fitbit

- Garmin Ltd.

- Medtronic

- Abbott

- Koninklijke Philips NV

- DexCom Inc

- GE HealthCare

- Vital Connect, Inc.

- Others

Frequently Asked Questions

The health and wellness devices market are projected to reach US$ 330.3 Bn in 2025, driven by demand for wearable devices and medical devices for wellness.

Rising chronic disease prevalence and AI/IoT integration fuel demand for wearable devices and chronic disease management solutions.

The health and wellness devices market are expected to grow at a CAGR of 8.8% from 2025 to 2032, driven by digital health advancements.

Expansion of digital health platforms and telehealth services offers significant growth potential for fitness and wellness monitoring devices.

Leading players include OMRON Corporation, Fitbit, Garmin Ltd., Medtronic, and Abbott, focusing on innovation and sustainability.