- Transportation & Logistics

- Refrigerated Trailer Gaskets Market

Refrigerated Trailer Gaskets Market Size, Share, and Growth Forecast 2026 - 2033

Refrigerated Trailer Gaskets Market by Material Type (EPDM, PVC, Neoprene, TPE/TPV, Silicone, Others), Application (Doors, Vents), by Design (Standard, Custom), Trailer Type (Truck Refrigerated Trailers, Refrigerated Shipping Containers, Rail Refrigerated Wagons), Distribution Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Refrigerated Trailer Gaskets Market Size and Trend Analysis

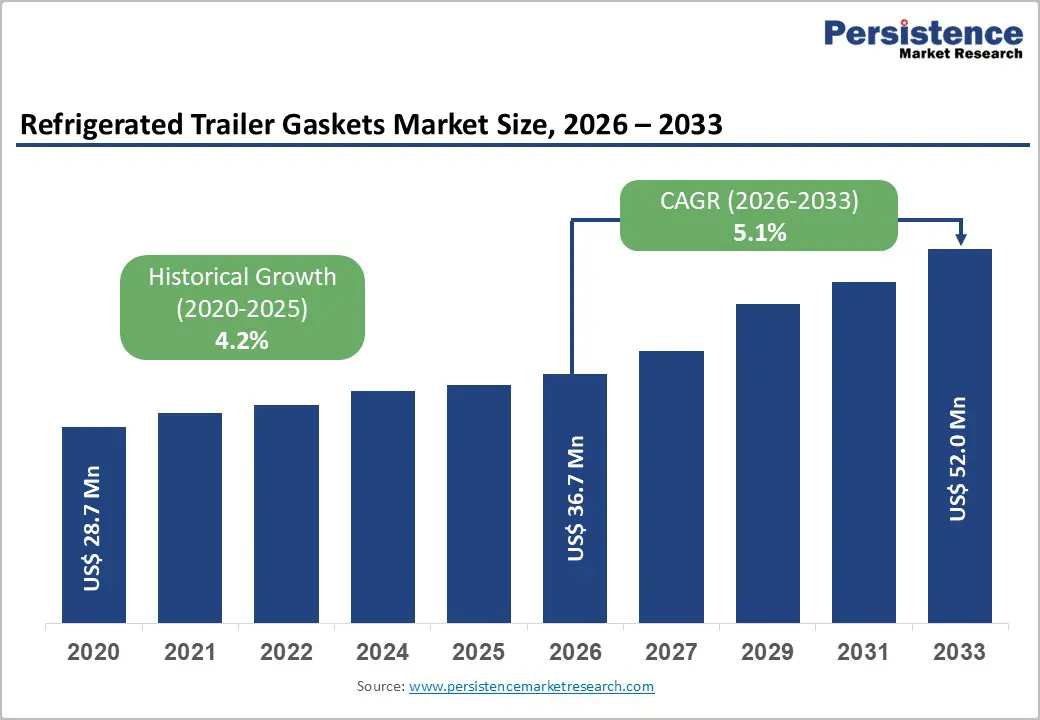

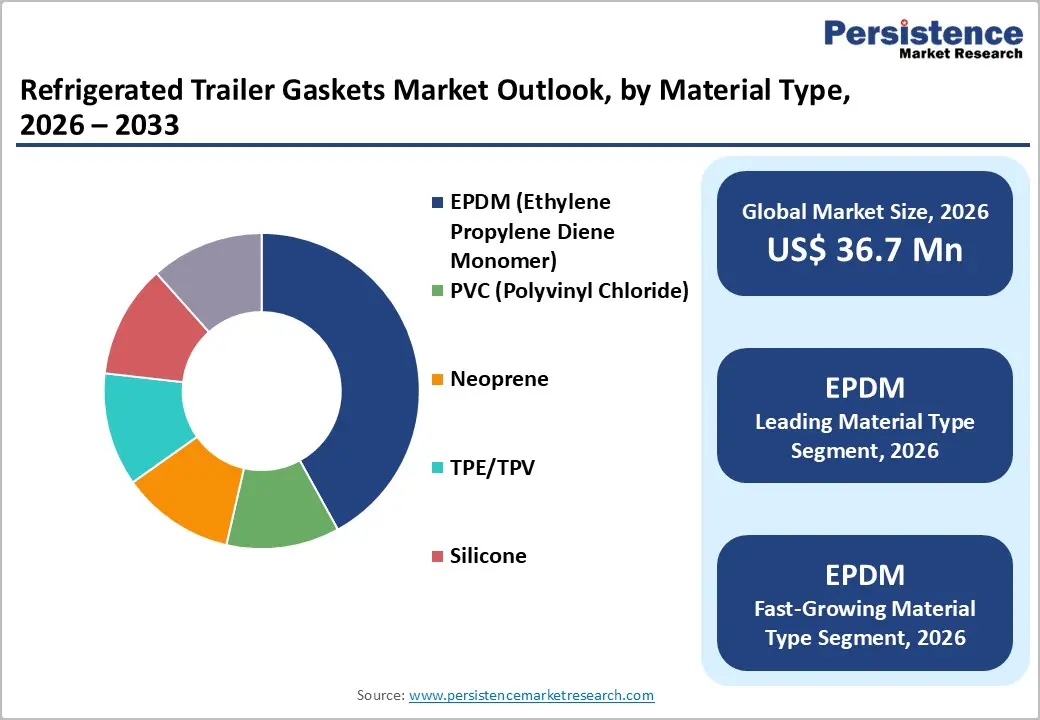

The global refrigerated trailer gaskets market size is expected to be valued at US$ 36.7 million in 2026 and projected to reach US$ 52.0 million by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

Market expansion is primarily driven by accelerating demand for cold-chain logistics infrastructure and stringent food safety regulations worldwide. The increasing adoption of temperature-controlled transportation for perishable goods, pharmaceuticals, and vaccines has necessitated high-performance sealing solutions that prevent thermal bridging and maintain consistent interior temperatures, thereby fueling the demand for advanced refrigerated trailer gaskets.

Key Industry Highlights

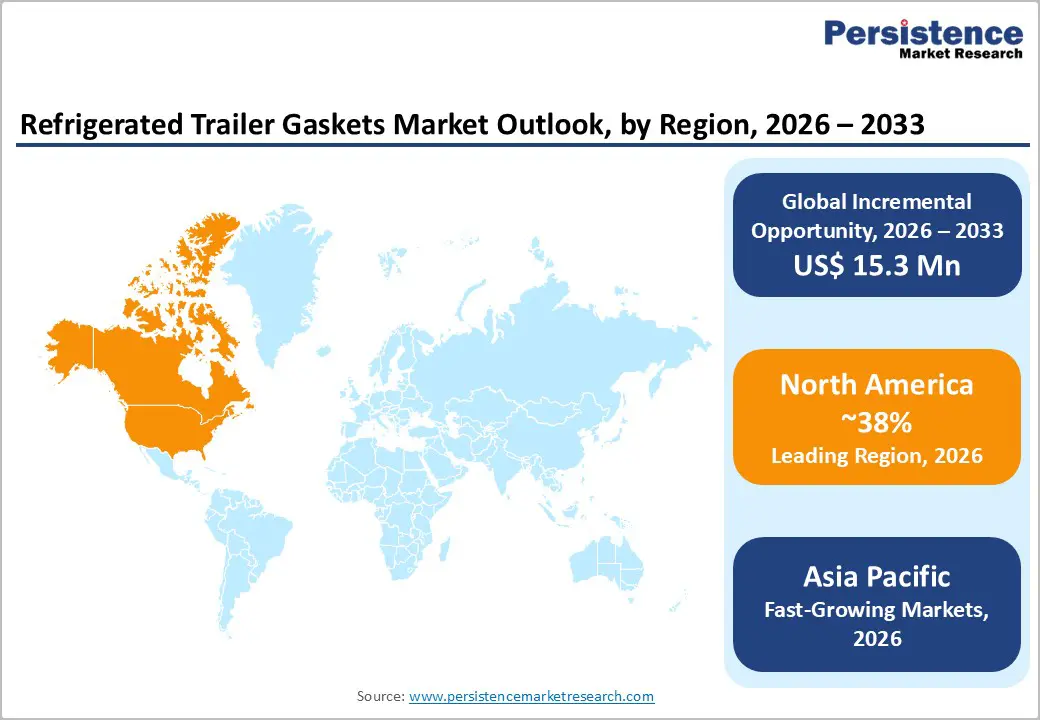

- North America leads the refrigerated trailer gaskets market, with approximately 38% market share in 2025, driven by the region's extensive cold chain infrastructure, stringent food safety regulations under FSMA, and the world's largest refrigerated trucking fleet, which transports over 1.2 billion tons of perishable goods annually.

- Asia Pacific emerges as the fastest-growing regional market with an anticipated CAGR of 6.3% from 2026 to 2033, propelled by rapid cold chain development in China and India, government infrastructure initiatives, expanding e-commerce grocery delivery, and substantial manufacturing capacity advantages supporting both domestic consumption and export markets.

- EPDM (Ethylene Propylene Diene Monomer) dominates the material type category with approximately 42% market share in 2025 and represents the fastest-growing segment at 5.4% CAGR, attributed to superior temperature resistance, extended service life, environmental durability, and alignment with sustainability requirements across transportation applications.

- Refrigerated shipping containers constitute the fastest-growing trailer type segment with 5.8% CAGR from 2026 to 2033, driven by expanding intermodal cold chain logistics, international perishable goods trade growth, and a global reefer container fleet exceeding 6.5 million TEU with approximately 500,000 new units added annually.

- The expansion of e-commerce and online grocery delivery platforms represents the most significant market opportunity, with global online food delivery revenue reaching approximately US$ 340 billion in 2024, necessitating substantial investments in last-mile refrigerated infrastructure and specialized gasket solutions designed for frequent-operation urban delivery applications.

| Key Insights | Details |

|---|---|

| Refrigerated Trailer Gaskets Market Size (2026E) | US$ 36.7 million |

| Market Value Forecast (2033F) | US$ 52.0 million |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.2% |

Market Dynamics

Drivers - Expansion of Global Cold Chain Infrastructure for Food Security

The rapid expansion of cold chain networks across emerging economies is significantly propelling the refrigerated trailer gaskets market. According to the Global Cold Chain Alliance, global cold storage capacity increased by approximately 15% between 2020 and 2024, driven by substantial investments in Asia-Pacific and Latin America. The Food and Agriculture Organization (FAO) estimates that nearly 14% of global food production is lost between harvest and retail due to inadequate cold chain infrastructure, creating substantial demand for reliable refrigerated transport solutions. Governments across developing nations are implementing national cold chain development programs, with India's Ministry of Food Processing Industries allocating over US$ 270 million for integrated cold chain projects under the Pradhan Mantri Kisan Sampada Yojana scheme. This infrastructure development directly drives increased demand for refrigerated trailers and replacement gaskets to ensure temperature integrity throughout the transportation process.

Stringent Regulatory Requirements for Temperature-Sensitive Pharmaceutical Transportation

The pharmaceutical and biopharmaceutical sectors are driving unprecedented demand for high-performance refrigerated trailer gaskets due to increasingly stringent regulatory frameworks. The U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have issued strict guidelines under Good Distribution Practice (GDP) regulations that require validated temperature-control systems for pharmaceutical transportation. The World Health Organization (WHO) reports that approximately 50% of vaccines worldwide are wasted annually due to temperature control failures during transportation and storage. With the global pharmaceutical cold chain market expanding rapidly following COVID-19 vaccine distribution experiences, manufacturers are investing in advanced sealing technologies. The International Air Transport Association (IATA) has updated its Temperature Control Regulations (TCR), requiring enhanced documentation and validation of temperature-controlled shipments, compelling logistics providers to upgrade their refrigerated fleet with superior gasket systems that meet ATP Agreement (Agreement on the International Carriage of Perishable Foodstuffs) standards.

Restraints - High Initial Investment and Maintenance Costs

The significant capital expenditure required for premium gasket materials and custom-engineered solutions presents a considerable barrier, particularly for small and medium-sized logistics operators. Advanced gasket materials such as silicone and specialized TPE formulations can cost 30-50% more than conventional PVC or EPDM options, while custom-designed gaskets for specialized applications command even higher premiums. According to the American Trucking Associations, the average operational cost per mile for refrigerated trucking has increased by approximately 18% since 2020, with maintenance and replacement parts accounting for a significant share of this increase. Many fleet operators in developing markets continue using lower-quality gasket solutions to minimize upfront costs, despite the long-term implications for energy efficiency and cargo protection, thereby constraining the adoption of technologically advanced gasket systems.

Material Degradation and Limited Service Life in Extreme Conditions

Gasket performance degradation from extreme temperature cycling and environmental exposure significantly impacts market growth, particularly in regions with harsh climates. Refrigerated trailer gaskets experience continuous thermal stress, with temperature differentials ranging from -30°C to +50°C, leading to material fatigue, cracking, and compression set. The Society of Automotive Engineers (SAE) research indicates that gasket failure rates increase by approximately 40% in environments with high humidity and salt exposure, which are common on coastal transportation routes. Additionally, incompatibility between certain gasket materials and cleaning chemicals used for sanitization in food-grade applications accelerates material breakdown. The average replacement cycle for trailer door gaskets ranges from 18 to 36 months, depending on usage intensity, creating ongoing maintenance burdens and operational downtime that discourages fleet expansion and modernization initiatives in cost-sensitive markets.

Opportunities - Growing Adoption of E-Commerce and Online Grocery Delivery Platforms

The exponential growth of e-commerce, particularly in perishable goods and online grocery delivery, presents substantial opportunities for refrigerated trailer gasket manufacturers. According to Statista, global online food delivery revenue reached approximately US$ 340 billion in 2024, with projections indicating continued double-digit growth through 2028. Major retailers, including Amazon Fresh, Walmart, Alibaba, and Instacart, are significantly expanding their cold chain logistics capabilities to meet consumer demand for same-day and next-day delivery of fresh and frozen products. The U.S. Department of Agriculture (USDA) reports that online grocery shopping penetration increased from 4% in 2019 to over 12% in 2024, necessitating investments in last-mile refrigerated delivery infrastructure. This trend is driving demand for smaller-format refrigerated vehicles and innovative gasket solutions designed for frequent door operations and urban delivery conditions, creating opportunities for manufacturers to develop specialized products for the quick-commerce segment with enhanced durability and ease of installation.

Technological Advancement in Sustainable and High-Performance Gasket Materials

Innovation in eco-friendly and high-performance gasket materials represents a significant growth opportunity as sustainability becomes a competitive differentiator in the transportation industry. The development of bio-based TPE and recycled rubber compounds aligns with corporate sustainability commitments and emerging environmental regulations, including the European Union's Green Deal, which targets a 55% reduction in greenhouse gas emissions by 2030. Trelleborg AB and other leading manufacturers are investing in advanced polymer technologies that deliver superior thermal insulation while reducing environmental impact. The International Institute of Refrigeration (IIR) emphasizes that improved gasket performance can reduce refrigeration energy consumption by 8-12%, directly contributing to lower operating costs and carbon emissions. Additionally, integrating smart sensors and IoT-enabled monitoring systems into gasket assemblies for real-time temperature and seal-integrity monitoring creates premium product opportunities. Several logistics companies are piloting predictive maintenance programs using sensor data, creating demand for next-generation gasket solutions that support digital transformation initiatives in cold chain management.

Category-wise Analysis

Material Type Insights

EPDM (Ethylene Propylene Diene Monomer) dominates the refrigerated trailer gaskets market, accounting for approximately 42% market share in 2025 and emerging as the fastest-growing material with a projected CAGR of 5.4% from 2026 to 2033. Its leadership is driven by superior resistance to temperature extremes ranging from -50°C to +150°C, along with excellent ozone, UV, and moisture resistance. EPDM gaskets demonstrate 30-40% longer service life than PVC alternatives, reducing replacement frequency in demanding refrigerated transport operations. Strong compression set resistance ensures consistent sealing under continuous pressure, while compatibility with food-grade cleaning agents supports hygiene compliance. Additionally, EPDM’s recyclability aligns with rising sustainability requirements, strengthening its adoption across OEM and aftermarket installations.

Application Insights

Door gaskets represent the most critical application segment, contributing approximately 78% market share in 2025 within the refrigerated trailer gaskets market. Doors account for up to 60% of potential thermal losses, making gasket performance essential for maintaining temperature stability and refrigeration efficiency. Frequent opening cycles and mechanical stress accelerate wear, with typical replacement intervals ranging between 24-30 months, depending on operational intensity. Door gasket failure remains the leading cause of temperature deviation incidents in refrigerated transport, directly impacting cargo quality and fuel efficiency. Compliance with standards such as ISO 1496-2 further reinforces demand for reliable door-sealing solutions, ensuring that this segment continues to generate sustained OEM and aftermarket demand.

Design Insights

Standard design gaskets dominate the market, accounting for approximately 68% of the market in 2025, owing to their cost-effectiveness, immediate availability, and compatibility with mainstream refrigerated trailer models. Nearly 85% of refrigerated trailers utilize standardized door and vent configurations, enabling widespread adoption of off-the-shelf gasket profiles. These designs provide predictable sealing performance and simplify procurement for fleet operators managing large vehicle portfolios. Standard gaskets also allow manufacturers to achieve economies of scale, supporting competitive pricing and consistent supply. Their suitability for routine maintenance and replacement makes them the preferred choice for food and retail cold chain operators prioritizing uptime, operational efficiency, and simplified inventory management across large fleets.

Trailer Type Insights

Truck refrigerated trailers account for approximately 65% of the market in 2025, reflecting their dominant role in regional and long-haul cold-chain logistics. In the United States alone, nearly 380,000 refrigerated trucks are in operation, with the fleet expanding at around 3% annually. These vehicles support diverse applications, including grocery distribution, meat and dairy transport, and pharmaceutical logistics. High utilization rates and frequent door operations lead to accelerated gasket wear, generating recurring replacement demand. As cold chain networks expand alongside rising consumption of frozen and temperature-sensitive products, truck refrigerated trailers remain the primary demand driver for gasket manufacturers globally.

Distribution Channel Insights

The aftermarket segment leads the refrigerated trailer gaskets market, accounting for approximately 58% of the market in 2025, supported by the consumable nature of gaskets and the long trailer service lives of 12-15 years. During this period, door gaskets typically require replacement 4-6 times, depending on usage conditions. Continuous exposure to vibration, temperature cycling, and sanitizing chemicals accelerates wear, necessitating gasket replacement as a routine maintenance activity. The aftermarket comprises fleet maintenance teams, independent repair facilities, and parts distributors, thereby creating diverse demand channels. Predictable replacement cycles and a large installed base of refrigerated trailers ensure stable, recurring revenue for gasket suppliers operating in this segment.

Regional Insights

North America Refrigerated Trailer Gaskets Market Trends and Insights

North America dominates the global refrigerated trailer gaskets market, commanding approximately 38% market share in 2025, underpinned by the region's mature cold chain infrastructure and stringent food safety regulatory framework. The United States accounts for the majority of regional demand, supported by the world's largest refrigerated trucking fleet and extensive interstate commerce in temperature-sensitive products. According to the U.S. Department of Transportation, refrigerated trucks transported over 1.2 billion tons of perishable goods in 2024, with the Food Safety Modernization Act (FSMA) mandating comprehensive temperature controls throughout the supply chain.

The region benefits from a well-established aftermarket distribution network and strong presence of leading gasket manufacturers including Mantaline Corporation and Advanced Plastic Corp. Canada represents a growing market segment, with extreme temperature variations between provinces necessitating high-performance gasket solutions. The Canadian Food Inspection Agency has implemented enhanced sanitary transportation regulations mirroring FDA requirements, driving gasket replacement and upgrade cycles. Innovation in sustainable materials and smart gasket technologies is particularly pronounced in North America, with several manufacturers piloting IoT-enabled monitoring systems for predictive maintenance applications in collaboration with major fleet operators.

Europe Refrigerated Trailer Gaskets Market Trends and Insights

Europe represents a significant market for refrigerated trailer gaskets, characterized by stringent regulatory harmonization and advanced environmental standards. The European Agreement Concerning the International Carriage of Perishable Foodstuffs (ATP) establishes comprehensive requirements for the construction and maintenance of refrigerated vehicles across member states, creating standardized demand for certified gasket solutions. Germany, France, United Kingdom, and Spain constitute the primary markets, collectively accounting for approximately 65% of regional gasket consumption.

According to Eurostat, the European Union cold chain logistics market handled over 280 million tons of temperature-controlled cargo in 2024, with intra-European trade in perishable goods driving sustained demand for refrigerated transport capacity. The European Green Deal and associated Fit for 55 legislative package are accelerating the adoption of energy-efficient refrigeration systems, creating opportunities for advanced gasket technologies that reduce thermal losses. Germany's Federal Motor Transport Authority (KBA) reported approximately 92,000 refrigerated commercial vehicles registered in 2024, reflecting robust fleet renewal activity. The region demonstrates strong preference for EPDM and silicone-based gaskets due to superior environmental performance and compliance with REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) regulations. Brexit implications continue influencing supply chain configurations, with some manufacturers establishing dual production facilities to serve UK and EU markets efficiently while managing regulatory divergence.

Asia Pacific Refrigerated Trailer Gaskets Market Trends and Insights

Asia-Pacific is the fastest-growing regional market for refrigerated trailer gaskets, with a CAGR of 6.3% from 2026 to 2033, driven by rapid cold-chain infrastructure development and expanding middle-class demand for fresh and frozen products. China dominates regional gasket consumption, supported by government initiatives, including the 14th Five-Year Plan, which prioritizes modern logistics infrastructure and food safety improvements. According to the China Federation of Logistics and Purchasing, the country's cold chain logistics market exceeded RMB 500 billion (approximately US$ 70 billion) in 2024, with refrigerated vehicle fleet growing at 8-10% annually.

India represents a high-potential growth market, with the National Centre for Cold Chain Development estimating that less than 10% of perishable goods currently utilize cold chain transportation, indicating substantial infrastructure gaps and development opportunities. The Indian Government’s Agricultural Export Policy targets doubling agricultural exports, necessitating significant investments in cold chains. Japan and South Korea demonstrate mature markets with a focus on technology advancement and replacement demand, while Southeast Asian nations, including Thailand, Vietnam, and Indonesia, are experiencing rapid cold chain expansion driven by e-commerce growth and urbanization. The region benefits from significant manufacturing capacity for gasket production, with companies such as Hebei Shida Seal Group Co., Ltd. and Eaget Group Co., Ltd. leveraging cost advantages while progressively upgrading quality standards to meet international certification requirements for export markets.

Competitive Landscape

The refrigerated trailer gaskets market is characterized by a moderately fragmented structure, with a balanced presence of global suppliers and a large number of regional and niche manufacturers. Competition is primarily driven by product performance, material innovation, and long-term OEM supply agreements, rather than pure brand dominance. Manufacturers increasingly focus on advanced elastomer formulations to enhance thermal efficiency, durability, and resistance to harsh operating conditions.

Business strategies also emphasize value-added services, including technical advisory, installation support, and extended warranty offerings, to improve customer retention. Growth strategies combine organic expansion into new geographies with targeted acquisitions aimed at strengthening production capacity or broadening application-specific portfolios. Meanwhile, competitive pricing and improved compliance capabilities from emerging-market suppliers are intensifying pressure, particularly within the aftermarket segment.

Companies Covered in Refrigerated Trailer Gaskets Market

- Trelleborg AB

- Reddiplex Ltd.

- Conta Flexible Products

- Great Dane

- Mantaline Corporation

- TODCO

- Hebei Shida Seal Group Co., Ltd.

- Stoughton Trailers, LLC

- Advanced Plastic Corp.

- ABCRUBBER INC.

- Lokhen Pty Ltd.

- Fermod Ltd.

- Eaget Group Co., Ltd.

- Rubber-Cal, Inc.

- Hi-Tech Extrusions Inc.

- Wabash National Corporation

- Utility Trailer Manufacturing Company

- Vanguard National Trailer Corporation

- Kinedyne LLC

Frequently Asked Questions

The global market is projected to reach US$ 36.7 million in 2026, driven by expanding cold chain logistics and food safety compliance.

Demand is driven by cold chain expansion (+15% capacity growth from 2020-2024) and stringent food and pharmaceutical transport regulations.

North America leads with around 38% market share in 2025, supported by a large refrigerated fleet and strict food safety regulations.

Rapid growth in e-commerce and online grocery delivery (US$ 340 billion revenue in 2024) is creating strong demand for refrigerated logistics.

Leading companies in the refrigerated trailer gaskets market include Trelleborg AB, Reddiplex Ltd., Conta Flexible Products, Great Dane, Mantaline Corporation, TODCO, Hebei Shida Seal Group Co., Ltd., etc.