- Automotive

- Refrigerated Vehicles Market

Refrigerated Vehicles Market Size, Share, and Growth Forecast, 2026 - 2033

Refrigerated Vehicles Market by Vehicle Type (Vans, Trucks, Trailers), Application (Food and Beverages, Pharmaceuticals, Chemicals, Others), Temperature (Single Temperature, Multi-Temperature), and Regional Analysis for 2026 - 2033

Refrigerated Vehicles Market Size and Trends Analysis

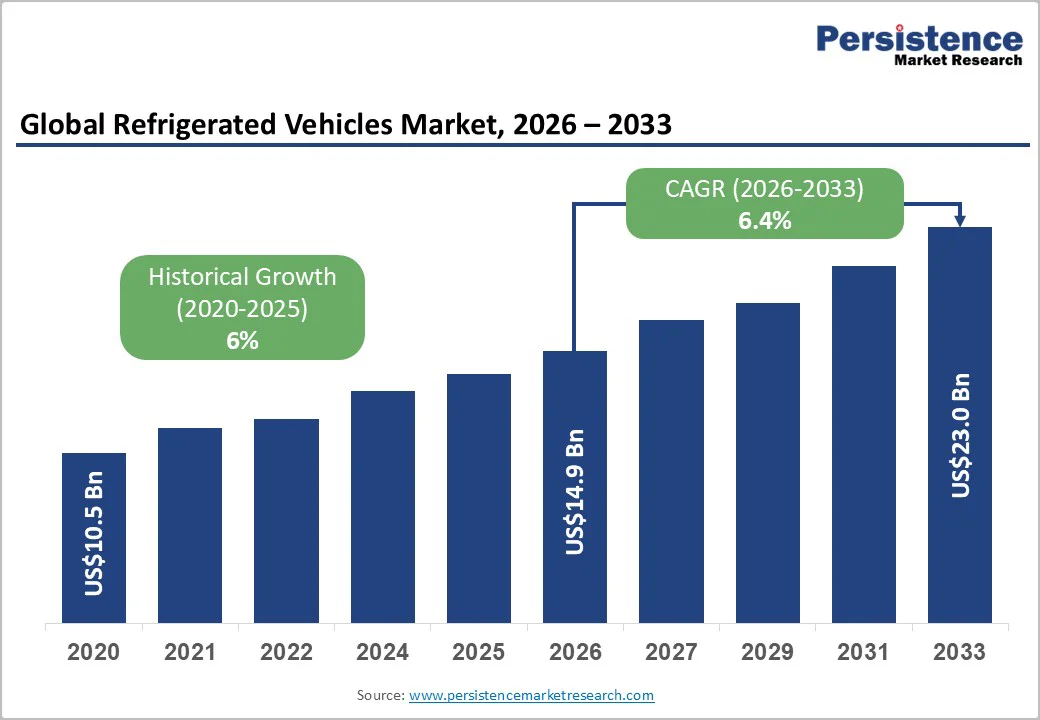

The global refrigerated vehicles market size is likely to be valued at US$14.9 Bn in 2026, projected to reach US$23.0 Bn by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cold chain logistics, rising demand for temperature-controlled transportation in pharmaceuticals, and advancements in multi-temperature technologies.

Rising demand for preserving perishable goods, especially in food, beverages, and chemicals, is driving the adoption of refrigerated vehicles. Innovations in vans and trailers are enhancing efficiency and versatility, while growing recognition of their role in global supply chains is fueling market growth.

Key Industry Highlights:

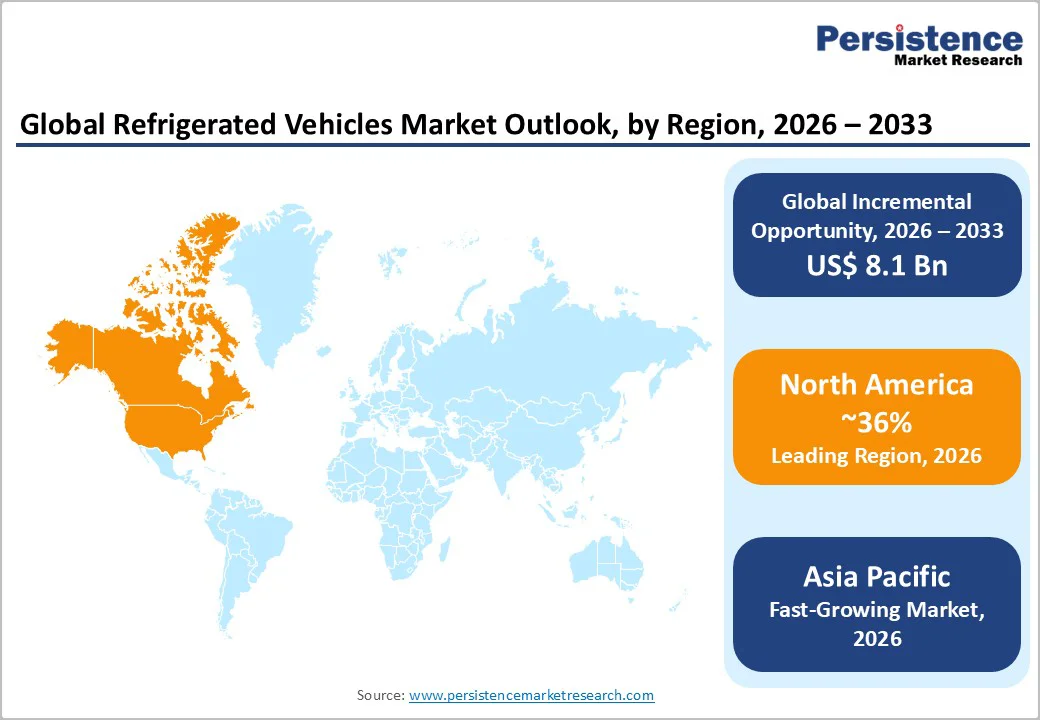

- Leading Region: North America, to command a 36% market share in 2026, due to its highly developed cold-chain infrastructure and strong demand from large food, pharmaceutical, and retail industries.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, due to rising demand for perishable foods, expanding e-commerce, and rapid cold-chain infrastructure development across emerging economies.

- Dominant Vehicle Type: Trucks, to hold 50% of the market share in 2026, and its dominance is driven by long-haul capacity, reliability, and versatility, making it preferred for food transportation.

- Leading Application: Food & beverages, to account for 55% of the market revenue, driven by the constant need to transport perishables such as dairy, meat, seafood, fruits, and vegetables.

- Leading Temperature: Single temperature, to contribute 60% of the market revenue, due to their widespread use in transporting uniform-temperature goods such as dairy, meat, and frozen products.

| Key Insights | Details |

|---|---|

|

Refrigerated Vehicles Market Size (2026E) |

US$14.9 Bn |

|

Market Value Forecast (2033F) |

US$23.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Need for Cold Chain Transportation

The rising prevalence of cold chain logistics is significantly boosting demand for temperature-controlled transportation as global supply chains become more dependent on fresh, frozen, and sensitive goods. Rapid population growth, urbanization, and shifting dietary habits are driving higher consumption of perishable foods such as dairy, meat, fruits, vegetables, and ready-to-eat products. To maintain quality and safety, these goods require reliable refrigerated transport from production sites to retail shelves. The expansion of e-commerce and quick-commerce platforms has also increased the need for efficient last-mile cold chain deliveries.

Beyond food, the pharmaceutical and healthcare sectors are major contributors to growing demand. The rise of biologics, specialty drugs, and temperature-sensitive vaccines, along with widened immunization programs, requires highly controlled transportation conditions. Cold chain regulations have become stricter, pushing fleets to adopt more advanced systems with real-time monitoring and precise temperature management. Global trade is also expanding the movement of perishable items across borders, encouraging countries to invest in modern refrigerated trucks, trailers, and vans.

High Development and Maintenance Costs

High development and maintenance costs remain a major challenge for the refrigerated vehicles market, limiting adoption, especially for small and mid-sized fleet operators. Developing advanced refrigeration units, whether electric, hybrid, or multi-temperature, requires significant investment in specialized components, high-performance insulation, battery systems, and low-GWP refrigerants. These technologies are more expensive than traditional diesel-based systems, making initial purchase prices considerably higher. Manufacturers also face rising R&D expenses as they work to meet stricter environmental regulations, improve energy efficiency, and integrate IoT capabilities.

Maintenance costs add another layer of complexity. Refrigeration units require regular servicing to ensure stable temperature performance, including compressor checks, coolant replacement, battery calibration, and continuous monitoring of digital systems. Any malfunction can lead to cargo spoilage, making preventive maintenance essential but costly. Advanced electric units and telematics-enabled systems often require trained technicians and specialized parts, further increasing service expenses.

Advancements in Electric and IoT-enabled Refrigerated Vehicles

Advancements in electric and IoT-enabled refrigerated vehicles are transforming the global cold-chain industry by improving efficiency, sustainability, and fleet intelligence. Electric refrigeration units are increasingly adopted as countries tighten emission regulations and logistics operators seek cost-effective, low-carbon solutions. Modern electric systems use high-capacity batteries, regenerative braking, and solar-assisted power to maintain consistent cooling without relying on diesel engines. This reduces fuel consumption, operating noise, and maintenance costs while supporting green logistics goals for food and pharmaceutical transport.

IoT integration is reshaping how fleets monitor and manage temperature-controlled shipments. IoT sensors now provide real-time temperature, humidity, and door-status data, ensuring sensitive goods remain within precise conditions throughout transit. Telematics platforms enable fleet operators to track vehicle performance, predict maintenance needs, and optimize routes based on live data, minimizing downtime and product spoilage. These systems also generate automated alerts for deviations, improving regulatory compliance and cargo safety.

Category-wise Analysis

Vehicle Type Insights

Trucks are anticipated to dominate the market, accounting for approximately 50% of the share in 2026, driven by their long-haul capacity, reliability, and versatility, making them the workhorse for food and goods transport. Their enclosed cargo compartments help preserve freshness, protect products from weather, and ensure safe delivery over long distances. For example, companies using trucks from Lamberet SAS, a manufacturer of refrigerated and insulated trucks, ensure perishable foods remain fresh and secure during transit, providing crucial temperature-controlled protection. Such scale and performance make trucks the preferred transport mode for manufacturers handling bulk or perishable shipments.

Trailers represent the fastest-growing segment, supported by their ability to enhance fleet efficiency and handle large, temperature-sensitive loads, especially in pharmaceuticals. Their modular design makes them ideal for multi-temperature operations, improving flexibility across long-haul routes. Ongoing innovations in reefer technology, particularly in North America and Europe, are accelerating adoption by boosting performance, sustainability, and reliability. For example, Schmitz Cargobull, a leading European manufacturer of refrigerated and insulated trailers, is widely used for pharmaceutical and perishable cargo transport, illustrating how advanced trailer technology supports rapid sector growth.

Application Insights

The food and beverages segment is expected to lead the market, holding 55% of the share in 2026, driven by the constant need to transport perishables such as dairy, meat, seafood, fruits, and vegetables. The sector relies heavily on temperature-controlled logistics to maintain freshness and safety. Rising consumption of packaged and frozen foods, along with expanding retail and e-commerce, continues to strengthen its dominance. For example, DHL Supply Chain provides specialized cold-chain logistics solutions for food and beverages, including refrigerated transport and temperature-controlled storage, ensuring product quality from manufacturer to retailer.

Pharmaceuticals are the fastest-growing segment, as strict cold-chain mandates and rising distribution of temperature-sensitive vaccines, biologics, and specialty drugs increase demand for reliable refrigerated transport. The need for controlled environments to maintain product stability, combined with stringent regulatory compliance, is driving rapid adoption. As healthcare supply chains expand, pharma-focused refrigerated vehicles continue to grow quickly.

Temperature Insights

The single-temperature segment is expected to lead the market in 2026, accounting for 60% of total revenue, supported by its extensive use in transporting uniform-temperature goods such as dairy, meat, and frozen products. Their simple design, lower maintenance costs, and operational efficiency make them the preferred choice for basic cold-chain needs. This cost-effectiveness continues to support strong adoption across fleets. For example, Thermo King provides specialized refrigerated transport solutions for the pharmaceutical industry, ensuring precise temperature control for vaccines and biologics during transit, supporting compliance with global cold-chain regulations.

The multi-temperature segment is the fastest-growing segment, due to its ability to handle diverse loads in a single trip, supporting mixed shipments of frozen, chilled, and ambient products. The versatility reduces operational costs and improves delivery efficiency for food, retail, and pharmaceutical sectors. As logistics networks expand, flexible temperature zones are becoming essential for modern cold-chain operations. For example, Schmitz Cargobull offers multi-temperature trailers with separate compartments for frozen, chilled, and ambient goods, enabling efficient and flexible transport across long-haul routes.

Regional Insights

North America Refrigerated Vehicles Market Trends

North America is expected to dominate the market, accounting for 36% of the share in 2026, driven by strong demand for efficient cold-chain logistics across food, pharmaceutical, and retail sectors. The U.S. and Canada have well-developed distribution networks, and increasing consumer reliance on fresh, frozen, and ready-to-eat foods is pushing fleets to expand capacity. Growth in online grocery, meal-kit delivery, and rapid-delivery services is further accelerating the need for reliable refrigerated trucks and vans that can operate efficiently across long distances and varied climates.

Manufacturers in the region are focusing on improving energy efficiency, emission control, and operational flexibility. This has led to rising adoption of electric and hybrid refrigeration systems, advanced insulation materials, and low-GWP refrigerants to meet tightening environmental regulations. Large fleet operators are investing in battery-powered units and solar-assisted refrigeration to reduce fuel consumption and improve sustainability performance. North America is also at the forefront of digital innovation in cold-chain transport. Widespread use of IoT sensors, telematics, predictive maintenance, and real-time temperature monitoring is helping operators reduce downtime, lower spoilage rates, and enhance route optimization.

Europe Refrigerated Vehicles Market Trends

Market growth in Europe is driven by stringent regulatory standards, rising sustainability objectives, and continuous upgrades in cold-chain infrastructure. The region’s mature food and beverage sector further boosts demand, relying heavily on dependable temperature-controlled transport for dairy, meat, seafood, fresh produce, and bakery items. The pharmaceutical sector, especially with the expansion of biologics and temperature-sensitive vaccines, is further strengthening the need for high-precision refrigerated fleets.

European manufacturers are focusing heavily on designing energy-efficient and low-emission vehicles to comply with EU environmental regulations. This is accelerating the adoption of electric, hybrid, and alternative fuel-powered refrigerated trucks and vans, supported by infrastructure improvements and government incentives across several countries. Advanced insulation materials, lightweight trailer construction, and improved compressor technologies are becoming standard as fleets work to reduce operating costs. Digital transformation is another major trend, with fleets increasingly using IoT-enabled telematics, real-time temperature tracking, and predictive diagnostics to improve reliability and reduce product loss.

Asia Pacific Refrigerated Vehicles Market Trends

Asia Pacific is likely to be the fastest-growing market for refrigerated vehicles, driven by rapid expansion in cold-chain logistics, rising consumption of perishable foods, and increasing cross-border trade. Countries such as China, India, Japan, and South Korea are investing heavily in modernizing supply chains to support fresh produce, seafood, meat, dairy, and pharmaceutical distribution. The region’s booming e-commerce sector, particularly in online grocery and quick-commerce delivery, is accelerating the need for temperature-controlled transportation fleets.

Local manufacturers are expanding production capacities and offering cost-efficient refrigerated trucks and vans designed for dense urban environments. Global players are partnering with regional logistics companies to introduce advanced refrigeration units equipped with better fuel efficiency and digital controls. Growing regulatory attention on food safety and vaccine distribution is further pushing fleets to adopt reliable, high-performance cooling systems. Sustainability is emerging as a key focus, with rising interest in electric or hybrid refrigeration units and solar-assisted systems to reduce emissions and operational costs.

Competitive Landscape

The global refrigerated vehicles market is moderately competitive, shaped by a balanced mix of established trailer manufacturers and niche refrigeration specialists. In developed regions such as North America and Europe, major players such as Schmitz Cargobull AG and Thermo King maintain strong leadership through advanced R&D capabilities, well-established distribution networks, and continuous product upgrades focused on fuel efficiency and regulatory compliance. Their dominance is further reinforced by long-term fleet contracts and strong aftermarket support systems.

In Asia Pacific, Carrier Transicold stands out by offering localized, climate-specific solutions tailored to diverse operating conditions and growing cold chain logistics needs. The region’s expanding food exports, rising e-commerce, and pharmaceutical distribution are accelerating demand for high-performance refrigerated vehicles. A major industry shift toward electric and hybrid refrigeration systems is creating new competitive advantages. Companies investing in battery-powered units, low-emission cooling, and solar-assisted technologies are gaining early traction as sustainability regulations tighten.

Key Industry Developments

- In March 2025, Mallaghan, a global leader in airport ground support equipment, launched North America’s first fully electric refrigerated catering truck. This strategic move strengthened Mallaghan’s commitment to aviation sustainability by combining zero-emission performance with precise temperature control for in-flight meal logistics, positioning the company as a pioneer in eco-friendly airport operations.

- In June 2024, GreenPower Motor Company Inc., a leading manufacturer of all-electric, zero-emission medium and heavy-duty vehicles for cargo, delivery, transit, and school bus markets, launched the EV Star REEFERX, an all-electric refrigerated medium-duty delivery truck. This initiative expanded GreenPower’s product portfolio in the temperature-controlled transport segment and supports the company’s strategy to capture growing demand for sustainable, electrified logistics solutions.

Companies Covered in Refrigerated Vehicles Market

- Schmitz Cargobull AG

- Lamberet SAS

- Carrier Transicold

- Wabash National Corporation

- Thermo King

- Mitsubishi Heavy Industries

- Great Dane LLC

- Kogel Trailer GmbH & Co. KG

- Krone Commercial Vehicle Group

- Utility Trailer Manufacturing Company

- Daikin Industries, Ltd.

Frequently Asked Questions

The global refrigerated vehicles market is projected to reach US$14.9 billion in 2026.

The rising prevalence of cold chain logistics and demand for temperature-controlled transportation are the key drivers.

The refrigerated vehicles market is expected to grow at a CAGR of 6.4% from 2026 to 2033.

Advancements in electric and IoT-enabled refrigerated vehicles present major opportunities.

Key players include Schmitz Cargobull AG, Carrier Transicold, Thermo King, Wabash National Corporation, and Mitsubishi Heavy Industries.