- Consumer Goods

- Refrigerated Prep Tables Market

Refrigerated Prep Tables Market Size, Share, and Growth Forecast, 2026 - 2033

Refrigerated Prep Tables Market by Product Type (Sandwich/Salad Prep Tables, Pizza Prep Tables, Others), Refrigeration Method (Air Cooled, Cold Wall, Liquid Jacket), Configuration Type (Door-Type Units, Drawer-Type Units, Hybrid), and Regional Analysis 2026 - 2033

Refrigerated Prep Tables Market Size and Trends Analysis

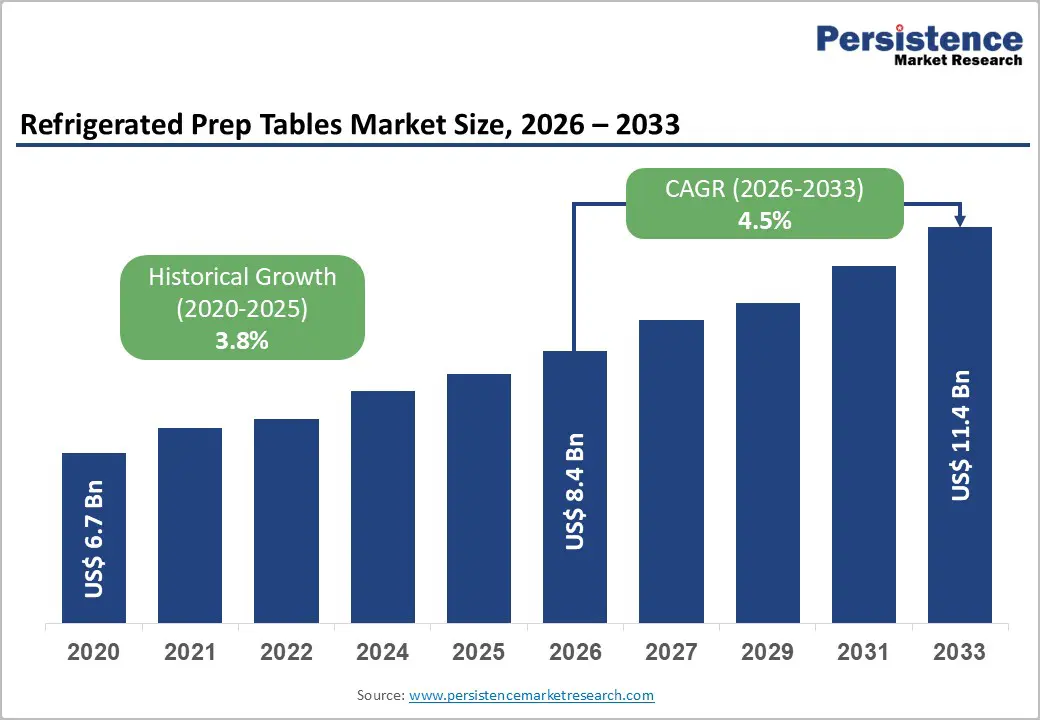

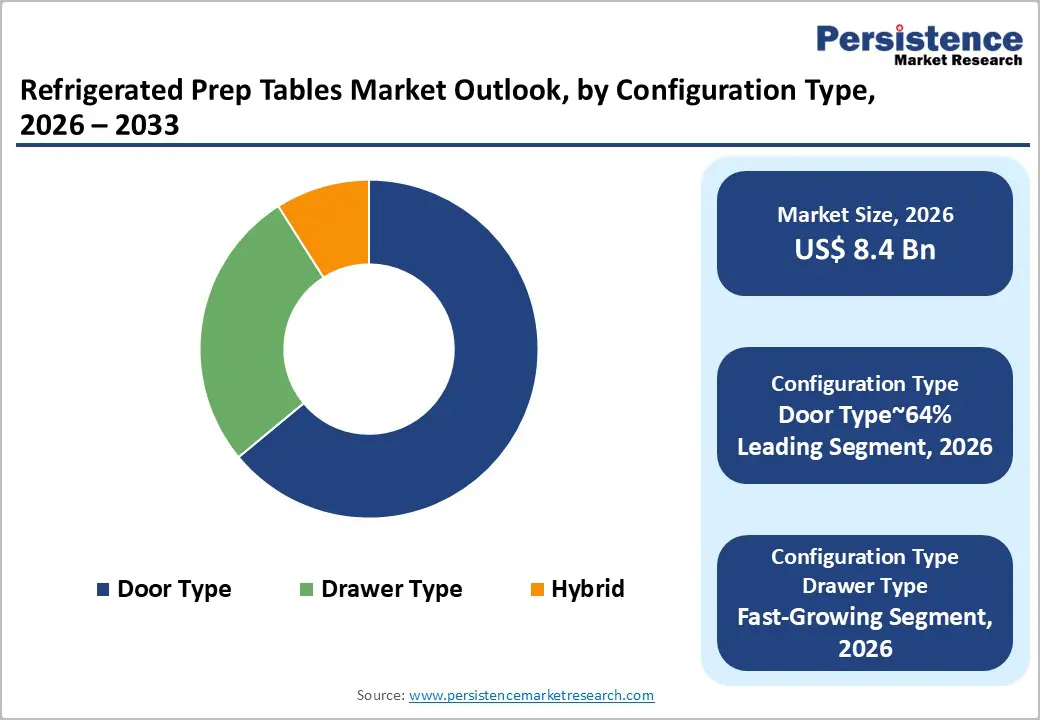

The global refrigerated prep tables market size is likely to be valued at US$8.4 billion in 2026 and is expected to reach US$11.4 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by increasing demand from the Quick Service Restaurant (QSR) sector and rising consumer expectations for fresh and hygienic food.

Expanding urbanization and evolving foodservice trends are encouraging restaurants and commercial kitchens to invest in advanced refrigeration solutions that optimize food preparation and storage efficiency. Stricter global food safety regulations are further motivating operators to adopt high-quality refrigerated prep tables that ensure compliance and minimize contamination risks. Innovations in energy-efficient designs and versatile configurations are enhancing operational flexibility, making these units more appealing across diverse foodservice environments. The market is also benefiting from the growing preference for modular kitchen setups, enabling seamless integration of prep tables into both compact and large-scale operations.

Key Industry Highlights:

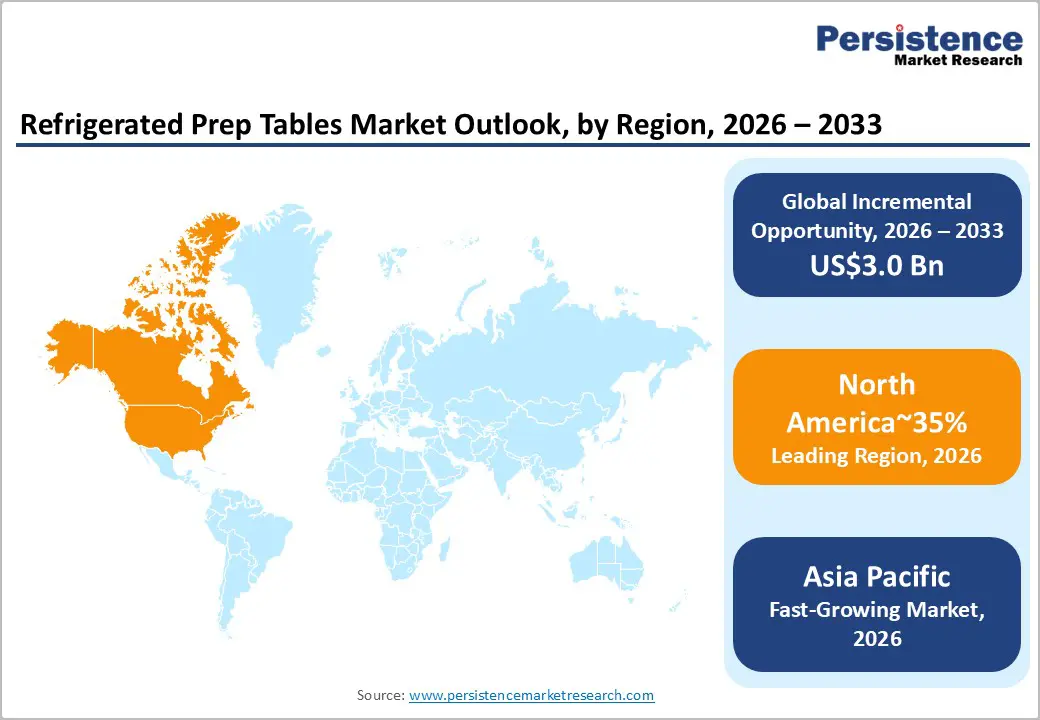

- Leading Region: North America is projected to lead due to high restaurant density, established QSR chains, and widespread adoption of refrigerated prep tables, accounting for approximately 35% of the market share.

- Fastest-Growing Region: Asia Pacific is anticipated to grow the fastest due to rapid urbanization, expansion of foodservice and QSR sectors, and rising consumer demand for ready-to-eat meals.

- Leading Refrigeration Method: The air-cooled segment is expected to dominate with approximately 72%, owing to cost-efficiency, energy savings, and minimal installation requirements.

- Leading Configuration Type: Door-type units are projected to dominate with approximately 64.0%, supported by large storage capacity, ease of access, and reliability in high-volume foodservice environments.

| Key Insights | Details |

|---|---|

| Refrigerated Prep Tables Market Size (2026E) | US$8.4 Bn |

| Market Value Forecast (2033F) | US$11.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Expansion of the Global Foodservice and QSR Sector

The accelerated proliferation of quick-service restaurants and delivery-focused kitchens structurally elevates demand for commercial refrigeration infrastructure. The global proliferation of standardized foodservice formats is structurally increasing demand for refrigerated prep tables in commercial kitchen environments. Expansion of quick-service, fast-casual, and delivery-centric concepts accelerates capital expenditure cycles for kitchen equipment. Revenue growth in emerging markets further supports sustained investment in back-of-house infrastructure. Each new outlet opening generates incremental demand for integrated cold storage and food preparation systems, positioning refrigerated prep tables as operational nodes within high-throughput assembly lines.

Tightening food safety regulations requires continuous cold chain control during ingredient handling. Regulatory bodies impose strict temperature thresholds to reduce contamination risk and associated liabilities. As a result, operators prioritize equipment that maintains thermal stability during peak service periods. This compliance-driven dynamic enhances the strategic importance of prep tables in kitchen design. Across the value chain, outlet expansion reinforces both initial installation demand and cyclical replacement of commercial refrigeration assets.

Technological Advancements in Energy Efficiency and Smart Refrigeration Systems

Technological advances in commercial refrigeration systems are materially improving operational efficiency across professional foodservice environments. Manufacturers are integrating high-efficiency compressors, enhanced insulation substrates, and optimized airflow configurations to reduce thermal variability during repetitive service cycles. These engineering advancements reduce energy intensity in kitchens with extended operating hours and variable load conditions. Given the structural weight of utilities within restaurant operating expenses, incremental efficiency improvements contribute directly to margin preservation across multi-unit operators and franchise systems.

Simultaneously, digital control architectures and sensor-enabled monitoring platforms are reshaping compliance management in temperature-sensitive preparation areas. Real-time diagnostics, automated temperature logging, and predictive maintenance algorithms strengthen operational oversight while minimizing human error. These capabilities reduce unplanned downtime, limit service interruptions, and enhance asset lifecycle performance. Collectively, technological integration is shifting refrigerated prep tables from passive storage units to data-enabled infrastructure components within modern commercial kitchen ecosystems. This digitalization shifts value creation toward lifecycle performance optimization rather than upfront capital pricing. At the market level, the convergence of energy efficiency mandates and smart connectivity standards is structurally upgrading product specifications across the refrigerated prep tables value chain.

Barrier Analysis - Skilled Labor Shortage in Advanced Refrigeration Systems

The escalating shortage of skilled refrigeration technicians is constraining the deployment of advanced prep table infrastructure. The deployment of IoT-enabled refrigeration systems necessitates specialized expertise in controls integration, network configuration, and digital diagnostics. However, many regional service ecosystems lack adequately trained technicians capable of ensuring compliant installation, calibration, and system optimization. This capability deficit constrains commissioning timelines, particularly within rapidly expanding foodservice and cloud kitchen models where speed-to-market is critical.

In addition, the technical complexity of sensor-based monitoring platforms increases lifecycle risk in markets with underdeveloped after-sales support infrastructure. Limited access to skilled maintenance personnel extends servicing intervals and heightens exposure to operational disruptions in high-throughput kitchen environments. As downtime directly affects throughput and revenue realization, these constraints introduce measurable operational volatility. At a broader level, the skills gap embeds latent cost pressures across the value chain, undermining projected efficiency gains from digital refrigeration investments. Labor scarcity structurally moderates the geographic expansion of technologically sophisticated refrigeration platforms.

Technological Complexity Across Digitalization and Refrigerant Engineering

The integration of IoT-enabled monitoring systems introduces significant architectural and interoperability complexities across refrigerated prep platforms. Digital transformation in commercial refrigeration necessitates interoperability among embedded sensors, cloud-based analytics platforms, and legacy kitchen infrastructure. Achieving this system harmonization is often constrained by fragmented software architectures and heightened cybersecurity requirements, which expand compliance and data governance obligations. These integration frictions extend installation lead times and deepen technical dependency within foodservice operations.

The adoption of advanced insulation composites and natural refrigerant technologies increases engineering complexity and the scrutiny of certification. Carbon dioxide (CO2) and propane-based configurations demand specialized component design, pressure management systems, and rigorous safety validation protocols. As environmental regulations continue to evolve, refrigerant selection becomes a moving compliance target, triggering recurring requalification procedures and design modifications. Collectively, these technological barriers elevate capital intensity and constrain seamless scalability across regional markets.

Opportunity Analysis - Development of Modular and Hybrid Preparation Units

The evolution of compact foodservice formats is generating structural demand for multifunctional refrigeration platforms. An unmet demand is emerging for highly adaptable kitchen equipment that delivers multifunctionality within constrained spatial footprints. Hybrid or dual-temperature preparation tables engineered to transition between refrigerated, ambient, or freezer-to-chiller configurations represent a strategic innovation pathway. Such flexibility enhances asset utilization and reduces the need for discrete equipment investments across varied menu formats.

Escalating commercial rents in Tier-1 urban markets intensify the premium placed on equipment with high spatial efficiency, effectively maximizing storage and operational output per square foot. Equipment selection criteria are increasingly influenced by storage capacity relative to occupied floor area. As urban density continues to expand, modular refrigeration platforms are projected to gain incremental market share. Regulatory food safety compliance remains embedded through calibrated temperature zoning and automated monitoring integration. As urban foodservice formats diversify across cloud kitchens and multi-brand facilities, modular and hybrid preparation units structurally expand the addressable specification envelope within commercial refrigeration infrastructure.

Sustainability Driven Equipment Upgrades

Decarbonization mandates and tightening environmental compliance frameworks are accelerating replacement cycles across commercial refrigeration assets. Foodservice operators are subject to increasing oversight regarding energy consumption intensity, refrigerant leakage thresholds, and lifecycle emissions exposure. Regulatory frameworks and environmental reporting standards are expanding compliance requirements across commercial refrigeration assets. This policy environment is contributing to greater adoption of high-efficiency compressor systems and refrigerants with lower global warming potential.

Procurement processes increasingly incorporate energy performance certifications, emissions disclosures, and documented regulatory conformity. As a result, sustainability metrics are becoming embedded within supplier evaluation models, influencing component sourcing strategies and overall system architecture design. The transition toward natural refrigerants and recyclable materials modifies manufacturing cost structures, particularly with respect to compliance testing and certification procedures. Energy-efficient platforms can moderate utility expenditure variability across multi-location restaurant networks. More broadly, sustainability-oriented retrofits are becoming integrated into capital planning frameworks governing foodservice infrastructure investment.

Category-wise Analysis

Refrigeration Method Insights

Air-cooled is anticipated to dominate, accounting for approximately 71% of the market share, supported by its structural suitability for mainstream commercial kitchen installations. Its self-contained architecture requires only standard electrical connectivity and sufficient ventilation, removing the need for integrated plumbing systems and reducing installation complexity. This configuration supports deployment in high-volume restaurant formats where commissioning speed and layout flexibility are operational priorities. Manufacturers, including True Manufacturing, Turbo Air, and Beverage-Air, structure significant portions of their product portfolios around air-cooled platforms engineered for service accessibility and operational reliability. Lower initial capital requirements, standardized maintenance procedures, and compatibility with conventional kitchen infrastructure contribute to sustained adoption across institutional foodservice environments. These attributes collectively reinforce the air-cooled segment's established position within commercial refrigeration procurement cycles.

Air-cooled is also expected to be the fastest-growing segment, driven by engineering refinements that materially enhance thermal consistency and energy performance. Advanced forced-air circulation and air curtain technologies stabilize pan temperatures during repetitive lid openings in high-throughput settings. The integration of electronically commutated fan motors improves airflow precision while lowering operational energy intensity. Suppliers are embedding smarter control systems and enhanced insulation to further optimize lifecycle efficiency. These performance gains compress the total cost of ownership and align with operator priorities centered on energy management and workflow continuity, accelerating upgrade cycles within existing installed bases.

Configuration Type Insights

Door-type units are projected to lead, accounting for approximately 64% of the market in 2026, supported by their structural alignment with high-volume ingredient storage requirements. Its cabinet-based configuration provides substantial refrigerated base capacity, enabling bulk storage of prepped and packaged ingredients within consolidated footprints. This architecture supports operational models in which volume availability outweighs rapid segmented access, particularly in standardized quick-service environments. Manufacturers such as Traulsen, Arctic Air, and Hoshizaki emphasize durability and straightforward mechanical layouts within door-type portfolios. The combination of cost efficiency, maintenance simplicity, and compatibility with legacy kitchen workflows sustains its entrenched deployment across institutional foodservice formats.

Drawer-Type units are expected to be the fastest-growing segment, driven by workflow optimization and ergonomic efficiency within high-throughput kitchens. Drawer-based access minimizes repetitive bending and reduces exposure time during ingredient retrieval, improving task sequencing under peak service pressure. Integration into chef-based configurations enables prep tables to support countertop cooking appliances, consolidating preparation and cooking stations within compact layouts. Advanced rail systems and segmented pan organization enhance portion control and retrieval speed. These operational efficiencies align with evolving kitchen design priorities focused on labor productivity and contamination risk mitigation, accelerating adoption across modern quick service and fast-casual environments.

Regional Insights

North America Refrigerated Prep Tables Market Trends

North America is expected to remain the leading regional market, accounting for approximately 35% of the market share in 2026, supported by its deeply institutionalized foodservice ecosystem and consolidated equipment manufacturing base. Demand is projected to remain anchored in large-scale quick service networks, franchised restaurant chains, and centralized procurement systems that prioritize specification uniformity and lifecycle performance. Competitive intensity is expected to remain concentrated among established commercial refrigeration manufacturers that integrate automated diagnostics, advanced airflow engineering, and labor-optimized configurations. This combination of regulatory alignment, technological depth, and structured distribution networks is anticipated to reinforce North America’s structural leadership within the global refrigerated prep tables market.

The U.S. is projected to function as the regional anchor, shaping procurement standards, refrigerant migration strategies, and innovation trajectories across the broader North American landscape. Supplier operating models such as True Manufacturing, Beverage-Air, and Hoshizaki America are expected to be reinforced. A mature restaurant industry, supported by national franchise operators and standardized supply chains, is positioned to maintain consistent upgrade demand across both new installations and retrofit cycles. Commercial alignment approaches are anticipated to focus on integrated monitoring systems, predictive maintenance capabilities, and labor-efficient mechanical layouts to offset workforce cost pressures.

Asia Pacific Refrigerated Prep Tables Market Trends

Asia Pacific is expected to register the fastest-growing trajectory, driven by rapid urbanization, expanding organized foodservice networks, and manufacturing scale advantages. Rising disposable incomes and westernized dining formats are anticipated to accelerate equipment penetration across metropolitan corridors in China, India, and Southeast Asia. Cost-efficient fabrication ecosystems in China are positioned to sustain competitive pricing structures while supporting regional export flows. Global manufacturers such as Turbo Air, Hoshizaki, and Panasonic Corporation are expected to expand localized production and distribution capabilities to align with fragmented demand patterns and service requirements.

China is projected to anchor regional momentum through its integrated manufacturing base and accelerating quick-service restaurant expansion. Domestic fabrication clusters are likely to reinforce supply-side resilience, enabling shorter lead times and customized configurations tailored to compact urban kitchens. Product adoption is anticipated to tilt toward energy-optimized and dual-temperature platforms that balance affordability with operational flexibility. Competitive intensity is set to remain elevated as domestic producers and multinational brands pursue localized service models and technology integration strategies to capture expanding mid-market demand.

Europe Refrigerated Prep Tables Market Trends

Europe is expected to remain a structurally influential market, supported by regulatory harmonization and advanced sustainability integration across commercial refrigeration infrastructure. The region is positioned to lead in natural refrigerant adoption as implementation of the EU F-Gas Regulation frameworks accelerates the transition away from high global warming potential systems. Ecodesign and Energy Labelling directives are anticipated to institutionalize performance-based procurement, embedding energy intensity thresholds directly into product qualification standards. Manufacturers such as Hoshizaki Europe, Electrolux Professional, and Gram Commercial are expected to align portfolios around propane-based and high-efficiency platforms optimized for compliance-led replacement cycles.

Germany is projected to anchor regional momentum through its strong foodservice base and engineering-led refrigeration ecosystem. National alignment with EU refrigerant phase-down mandates is expected to accelerate retrofit programs across institutional kitchens and organized retail environments. Investment flows are anticipated to focus on smart-grid-responsive refrigeration capable of modulating energy consumption during peak pricing periods. Product specifications are likely to emphasize advanced insulation, inverter-driven compressors, and digital monitoring modules to satisfy stringent energy disclosure requirements. This convergence of regulatory enforcement, technical standardization, and energy optimization is expected to sustain Europe’s leadership in sustainability-driven refrigerated prep table deployment.

Competitive Landscape

The global refrigerated prep tables market is moderately consolidated, with the top five players controlling approximately 45-50% of the global revenue. such as True Manufacturing and Hoshizaki, while Turbo Air, Traulsen, and Unified Brands reinforce upper-tier concentration. The leading cohort collectively controls a substantial share of global revenue, shaping procurement standards through expansive distribution reach and portfolio depth. Brand equity and established service ecosystems further embed these manufacturers within multi-unit restaurant and institutional foodservice contracts. Larger manufacturers are expected to prioritize IoT-enabled diagnostics, automation-ready designs, and energy-optimized platforms to strengthen installed-base retention. Industry behavior is anticipated to remain characterized by selective acquisitions, distribution partnerships, and incremental platform consolidation that reinforce scale advantages without eliminating regional fragmentation.

Key Industry Developments:

- In February 2026, True Manufacturing made the global availability of TSSU-27-08-HC with R290 Hydrocarbon refrigerant. The use of eco-friendly R290 refrigerant ensures compliance with strict environmental regulations while maintaining precise temperatures between 33°F and 41°F.

- In February 2026, Turbo Air Inc. began widespread adoption of the Cold Bunker system for consistent food safety. This forced-air system creates a "cold air-shield" around ingredient pans, maintaining temperatures below 41°F even when lids are left open during busy shifts.

- In July 2025, Electrolux Professional showcased the SkyLine Chill Blast Chiller at India Horeca Expo. The company emphasized that this equipment is designed to "lock in food quality and safety" through rapid, intelligent chilling cycles. The SkyLine ChillS was highlighted for its ability to ensure HACCP compliance, reduce food waste by up to 35%, and maintain the "just-cooked" quality of food.

Companies Covered in Refrigerated Prep Tables Market

- True Manufacturing

- Hoshizaki

- The Middleby Corporation

- Ali Group

- Electrolux Professional

- ITW Food Equipment Group

- Turbo Air

- Beverage-Air

- Traulsen

- Continental Refrigerator

- Blue Star Limited

- Williams Refrigeration

- Foster Refrigerator

- Infrico

- Arctic Air

- Standex International

Frequently Asked Questions

The global refrigerated prep tables market is projected to be valued at US$8.4 billion in 2026 and is expected to reach US$11.4 billion by 2033, supported by expanding QSR networks, stricter food safety standards, and rising demand for energy-efficient commercial refrigeration systems.

The rapid proliferation of QSR and fast-casual formats structurally increases demand for high-throughput, temperature-controlled preparation infrastructure. Each new outlet requires integrated cold storage and ingredient assembly systems, positioning refrigerated prep tables as critical operational assets within standardized kitchen layouts focused on speed, hygiene, and workflow optimization.

The refrigerated prep tables market is forecast to grow at a CAGR of 4.5% from 2026 to 2033, reflecting steady replacement cycles, technological upgrades in energy-efficient platforms, and increasing regulatory compliance requirements across commercial kitchens.

North America leads the market, accounting for approximately 35% share, driven by high restaurant density, strong franchise ecosystems, regulatory enforcement, and widespread adoption of advanced refrigeration systems across institutional and chain-based foodservice operations.

The refrigerated prep tables market is moderately consolidated, with key players including True Manufacturing, Hoshizaki, Turbo Air, Traulsen, Unified Brands, Electrolux Professional, and The Middleby Corporation. These companies compete through distribution scale, energy-efficient engineering, natural refrigerant integration, and the expansion of IoT-enabled monitoring capabilities across commercial refrigeration platforms.