- Transportation & Logistics

- Refrigerated Trailer Market

Refrigerated Trailer Market Size, Share, and Growth Forecast, 2026 - 2033

Refrigerated Trailer Market by Temperature Class (Single-Temperature, Multi-Temperature, Cryogenic), Trailer Capacity (Up to 28 ft , 29–49 ft , Above 49 ft ), Temperature Class (Diesel ICE Units, Diesel-Electric Hybrid Units, Battery-Powered Units, Cryogenic & Alternative-Fuel Units) Industry (Food & Beverage, Pharmaceuticals / Life Sciences, Retail & E-Commerce, Logistics & Transportation, Agriculture / Chemical) and Regional Analysis 2026 - 2033

Refrigerated Trailer Market Size and Trends Analysis

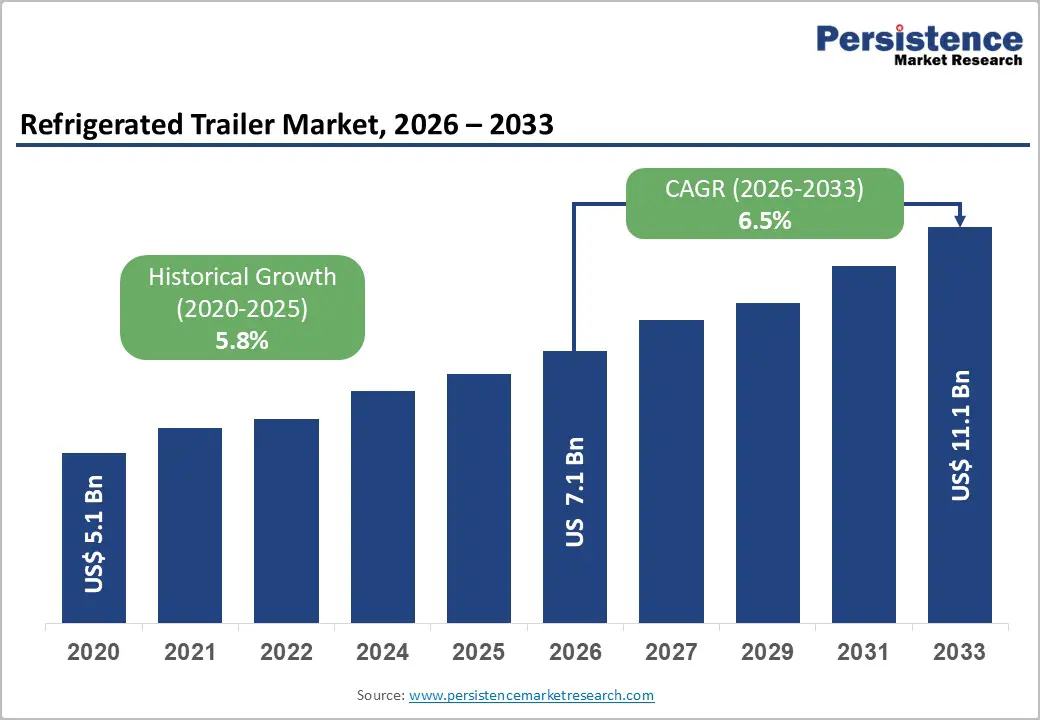

The global refrigerated trailer market size is likely to be valued at US$ 7.1 billion in 2026 and is projected to reach US$ 11.1 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

The market's expansion is driven by three pivotal factors: the accelerating globalisation of perishable goods trade, stringent regulatory mandates for temperature-controlled logistics, and transformative digital innovations in cold chain management. Heightened consumer demand for fresh and frozen products through e-commerce channels, coupled with pharmaceutical industry expansion requiring precise temperature maintenance, establishes the refrigerated trailer market as a critical infrastructure component in modern supply chains.

Key Industry Highlights:

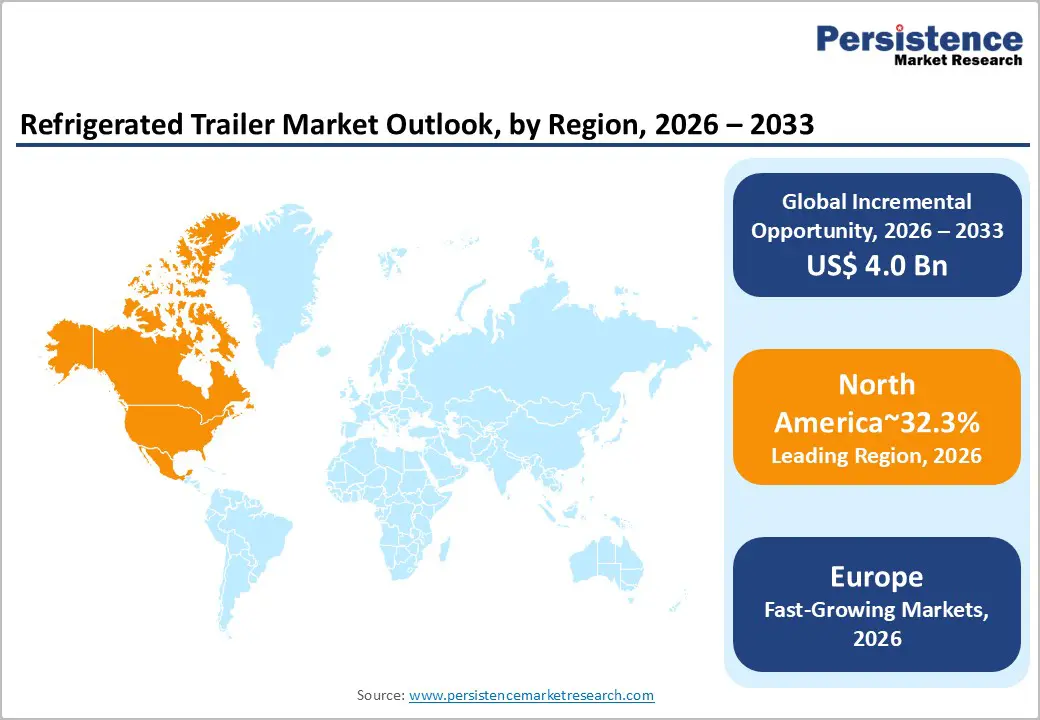

- Regional Leadership: North America leads the global Refrigerated Trailer market with 32.3% share, supported by advanced cold-chain infrastructure, strong food & beverage logistics, and stringent regulatory push toward low-emission refrigerated transport.

- Fastest-Growing Regional Cluster: East Asia emerges as the fastest-growing region with 20% share, driven by rapid e-commerce grocery expansion, urbanisation, and state-backed investment in temperature-controlled logistics networks.

- Strong European Presence: Europe maintains 25.4% share, reinforced by mature cold-chain networks, natural refrigerant adoption under EU F-Gas regulations, and leadership in sustainable refrigerated trailer manufacturing.

- Leading Temperature Class: Single-Temperature trailers dominate with >52% market share, supported by conventional long-haul food & beverage distribution requiring uniform controlled environments.

- Fastest-Growing Temperature Class: Multi-Temperature trailers are the fastest-growing segment, propelled by mixed-load consolidation for retail, pharmaceuticals, and last-mile grocery delivery networks.

| Key Insights | Details |

|---|---|

| Refrigerated Trailer Market Size (2026E) | US$ 7.1 Bn |

| Market Value Forecast (2033F) | US$ 11.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Dynamics

Drivers - Expansion of E-Commerce and Last-Mile Cold Logistics

The e-commerce revolution has fundamentally transformed demand patterns within the Refrigerated Trailer Market, particularly through food and grocery delivery platforms. Global retail e-commerce sales reached US $300.1 billion in the third quarter of 2024, with online grocery experiencing particularly robust expansion in the Asia Pacific at 45% growth between 2021 and 2022. This shift creates operational imperatives for logistics providers to deploy specialised refrigerated transport solutions that ensure product freshness during time-sensitive last-mile deliveries. Specialised refrigerated vehicles with real-time temperature monitoring are now standard requirements rather than competitive advantages.

The refrigerated trailer market has responded by integrating telematics systems, GPS tracking, and environmental sensors that provide continuous cargo monitoring capabilities that have become non-negotiable for major e-commerce operators. Food and beverage cold chain logistics specifically is forecast to expand at a CAGR of around 15 percent through 2030, substantially outpacing broader refrigerated transport growth rates.

Companies are increasingly adopting multi-temperature trailer solutions to consolidate deliveries across diverse product categories in single trips, reducing operational friction and environmental footprint. This structural shift toward distributed, rapid-turnover distribution networks directly correlates with heightened refrigerated trailer adoption and technology specification requirements.

Pharmaceutical Sector Expansion and Temperature-Sensitive Biologics Demand

The pharmaceutical industry's rapid evolution toward biologics, vaccines, and temperature-sensitive therapeutics has fundamentally transformed refrigerated trailer demand dynamics within the Refrigerated Trailer Market. Global pharmaceutical sales are projected to reach USD 1.5 trillion by 2024, with a significant portion comprising temperature-sensitive products requiring stringent cold chain management throughout storage and transportation.

mRNA vaccines, monoclonal antibodies, cell therapies, and gene therapies demand specialised temperature control equipment, creating differentiated demand for advanced refrigerated trailer systems capable of maintaining precise temperature ranges. Thermo King launched its flagship LEGEND trailer refrigeration unit with production in Wujiang, China, on 18 April 2025, featuring intelligent temperature control and 3-in-1 motor technology supporting fuel efficiency and reduced maintenance costs.

The pharmaceutical distribution sector's expansion in Asia Pacific and North America, driven by vaccination campaigns and healthcare infrastructure investments, has substantially increased refrigerated trailer utilisation across logistics networks. The convergence of pharmaceutical market growth, regulatory requirements for temperature integrity, and technological advancement in refrigeration systems has established pharmaceutical logistics as a critical demand for refrigerated trailer innovations.

Global Trade in Perishable Goods and Food Security Infrastructure Investment

International food trade has experienced structural acceleration, with production and consumption increasingly geographically separated. India's food processing sector, valued at US $354.5 billion in 2024 and projected to expand to US $535 billion by FY26, has become a strategic export hub requiring reliable temperature-controlled logistics. India contributed 13 percent of the nation's total exports through food processing and attracted 6 percent of total industrial investment, with FDI inflows of US $13.4 billion between 2000 and June 2025.

The United States food and beverage manufacturing sector generated 16.8 percent of total manufacturing sales in 2021, employing 1.7 million workers, with meat processing representing 26.2 percent of sector sales. European food and beverage services employ 10.9 million people and generated €280.7 billion in value added in 2022, reflecting recovery momentum in post-pandemic trade flows.

China's Belt and Road Initiative has strengthened cross-border refrigerated transport corridors, while rapid urbanisation in the Asia Pacific has amplified demand for fresh produce and speciality foods. The Refrigerated Trailer Market has expanded accordingly to support intercontinental logistics networks, with manufacturers scaling production capacity and developing region-specific configurations to optimize cold chain performance across variable climatic conditions.

Market Restraining Factors - High Capital Investment Requirements and Operational Cost Pressures

Refrigerated trailer procurement, installation, and operational costs represent significant economic barriers limiting adoption, particularly among small-to-medium logistics enterprises and emerging market operators within the Refrigerated Trailer Market. Initial refrigerated trailer investments encompass substantial capital expenditure for specialised equipment, temperature control systems, and integrated telematics infrastructure, with maintenance and operational costs consuming significant operational budgets.

Electricity tariffs in Asia Pacific cold chain operations now represent up to 70 percent of warehouse operational expenses, creating margin compression across integrated cold chain operators. Diesel auxiliary Transport Refrigeration Units (TRUs) can produce between 3 and 15 tonnes of annual CO2 emissions, equivalent to 2 and 9 average vehicles, imposing environmental compliance and regulatory costs on operators.

Opportunity - Electrification and Zero-Emission Refrigerated Transport Solutions Development

The transition toward electric and hybrid refrigeration units represents a transformational growth vector for the Refrigerated Trailer Market. Thermo King's AxlePower zero-direct emission system, introduced in November 2021, integrates fully electric refrigeration units with high-efficiency battery storage and axle energy recovery capability, enabling tractor-independent cold transport. The Kögel-SAF Holland partnership launched the Cool-PurFerro refrigerated trailer in February 2022, featuring a recuperation axle converting kinetic energy into electricity for fully electric cooling devices, reducing CO2 and pollutant emissions while decreasing diesel consumption and operational noise.

In April 2025, Thermo King launched its flagship LEGEND trailer refrigeration unit with the first Asian-made production line in Wujiang, China, incorporating precise temperature control, intelligent operation, and 3-in-1 motor technology that enhances fuel efficiency and reduces maintenance costs.

The emerging segment of electric transport refrigeration units (eTRUs) eliminates diesel reliance and reduces both acoustic and particulate emissions, with battery-powered systems enabling zero-emission urban deliveries. The sustainable refrigeration technology market represents a distinct growth segment demonstrating investment velocity in decarbonised cold chain solutions. Electric TRUs paired with electric vehicle drivetrains create operational synergies, particularly in ultra-low emission zones expanding across major urban centres globally.

Solar-Assisted and Renewable Energy Integration

Solar-powered refrigerated transport solutions have emerged as transformational technology for distributed supply chains. In May 2024, TIP, in collaboration with Sunswap and Chereau UK, initiated a 12-month trial of the 'Endurance' solar-powered, zero-emission refrigerated trailer in the UK, integrating solar panels, modular battery systems, and advanced insulation technology to deliver emission-free cooling with real-time cloud monitoring.

Large-scale retailers have deployed solar-assisted trailers generating approximately 2,000 litres of diesel savings annually per unit, corresponding to over 5 tonnes of annual carbon reduction per trailer. Solar-powered refrigeration systems harness renewable energy for auxiliary cooling units or onboard battery charging, reducing fuel consumption and extending electric TRU operational duration. These solutions prove particularly valuable in developing regions with unreliable grid infrastructure, where off-grid solar refrigeration ensures reliable cold chain maintenance for pharmaceutical and food products.

Multi-Temperature and Flexible Compartment Systems for Mixed-Load Optimization

Multi-temperature refrigerated trailers represent the fastest-growing temperature-class segment within the market, enabling simultaneous transport of frozen, chilled, and ambient products within discrete temperature zones. Advanced dual-evaporator systems permit flexible thermal partitioning, allowing operators to transport mixed product assortments without requiring multiple vehicles per delivery route. This flexibility directly reduces transportation costs per unit of goods while minimizing environmental footprint through consolidated logistics workflows.

In October 2025, Gist deployed the UK's first 44-pallet double-deck reefer trailers from Gray & Adams featuring dual- and single-temperature Carrier refrigeration units with optimised airflow for fuel efficiency and retractable tail-lifts, achieving 10 percent pallet capacity increases with enhanced operational productivity. Multi-compartment systems allow food service distribution centers, supermarket networks, and grocery retailers to optimize inventory flow by consolidating fresh and frozen product movements.

The market opportunity encompasses customizable partition systems, insulated bulkheads, and advanced thermal management, enabling operators to adapt cargo space configurations to distinct load requirements while maintaining regulatory compliance for diverse product categories

Category-wise Analysis

Temperature Class Insights

The Single-Temperature segment maintains market leadership with 52.3% market share in 2026, driven by established applications in conventional food and beverage transport requiring uniform thermal environments. This segment encompasses the largest installed base of operational refrigerated trailers and benefits from mature supply chains, established maintenance networks, and proven technology reliability. Single-temperature trailers continue to dominate long-haul interstate and international food transport operations, where product homogeneity justifies dedicated thermal space allocation.

The multi-temperature segment represents the fastest-growing category, capitalising on emerging logistics models emphasising mixed-load consolidation and last-mile delivery efficiency. Multi-temperature trailers combine independently controlled refrigeration zones within single trailer bodies, enabling operators to transport frozen foods, fresh produce, dairy, and pharmaceuticals within distinct compartments, maintaining precise temperature specifications. This flexibility reduces transportation costs per unit while optimising vehicle utilization rates, factors driving robust adoption across modern distribution networks.

Advanced dual-evaporator systems from manufacturers including Carrier, Thermo King, and specialised European providers have matured sufficiently to achieve mainstream market acceptance. The segment's expansion correlates directly with growth in e-commerce food delivery, retail consolidation, and regional distribution centre models, emphasising operational efficiency.

Industry Insights

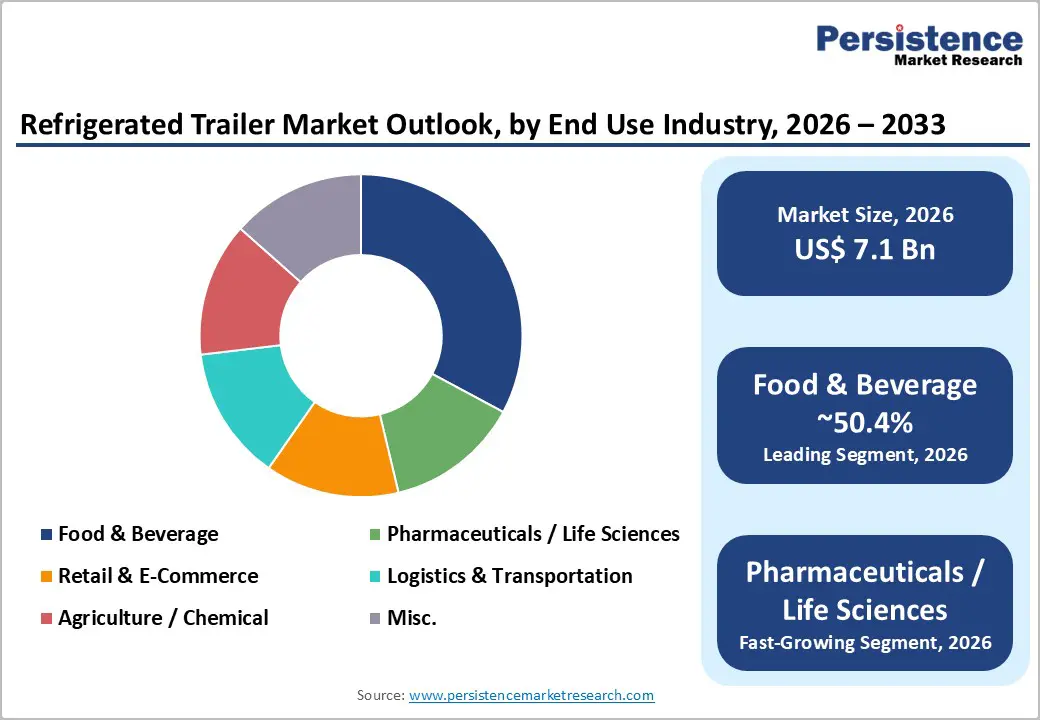

Food & Beverage maintains a dominant market position with 50.4% market share in 2026, encompassing meat processing, dairy distribution, seafood transport, frozen food logistics, and fresh produce movement. This segment's sustainability derives from consistent consumer demand for perishable products, established cold chain infrastructure investment, and stringent food safety regulations requiring temperature-controlled transport.

The European accommodation and food services sector employs 10.9 million people and generated €280.7 billion in value added in 2022, reflecting the scale and complexity of temperature-controlled distribution networks supporting this economic pillar. India's food processing sector contributed 8.8 percent of manufacturing GVA and 13 percent of national exports in 2024, with government initiatives including 41 Mega Food Parks and extensive cold-chain expansion propelling demand for specialized refrigerated transport.

Pharmaceuticals and Life Sciences represent the fastest-growing end-use segment, driven by expanded vaccine distribution networks, complex biologics requiring cryogenic storage, and regulatory mandates for unbroken temperature control. The pharmaceutical sector represents a distinct growth opportunity characterised by higher regulatory barriers, premium pricing structures, and mission-critical reliability requirements.

Regional Insights and Trends

North America Refrigerated Trailer Market Trends

North America commands 32.3% of the global refrigerated trailer market, establishing regional leadership through advanced logistics infrastructure, stringent regulatory frameworks, and substantial perishable goods consumption. The U.S. refrigerated trailer industry held dominant positioning in 2024, driven by rising consumer demand for fresh and perishable goods, particularly within the food and beverage and e-commerce sectors. U.S. food and beverage manufacturing accounted for 16.8 percent of total manufacturing sales, value added in 2021, reflecting substantial industry scale and cold chain infrastructure requirements. California Air Resources Board (CARB) regulations push for low-emission trailers, accelerating electrification initiatives across North American fleets.

The U.S. refrigerated transport market is predicted to outpace Canada through 2032, backed by rapid scaling of cold chain capacity for pharmaceuticals, with emphasis on biologics and mRNA vaccines requiring ultra-low temperature management. Electrification of refrigerated fleets advances through California's Advanced Clean Fleets regulation, with companies including Lineage Logistics piloting electric trailers with solar-assisted Transport Refrigeration Units in Nevada and California. Online grocery shopping surges and home delivery service expansion have significantly boosted refrigerated trailer demand to ensure perishable goods reach consumers in optimal condition.

East Asia Refrigerated Trailer Market Trends

East Asia dominates the global Refrigerated Trailer market with 20.0% share, driven by urbanisation, rising disposable incomes, expanding e-commerce platforms, and substantial government infrastructure investment. China accounts for 30.4% of the Asia Pacific refrigerated transport market share as of 2024, with the country's vast population supporting immense demand for temperature-controlled logistics.

The Made in China 2025 initiative focuses on enhancing supply chain efficiency, particularly in refrigerated transportation, while the Belt and Road Initiative has strengthened cross-border trade routes, amplifying refrigerated transport demand. China's growing demand for premium food products, including dairy, meat, and seafood, propels a continuous requirement for advanced refrigeration solutions. JD.com and Alibaba's expansion of fresh and frozen product categories has driven substantial fleet modernisation across regional logistics providers.

The Asia Pacific refrigerated transport market is substantially exceeding global growth rates. This accelerated trajectory reflects structural economic transformation, rising living standards, and rapid urbanization supporting sustained demand for perishable product distribution. Government policies supporting electrification and zero-emission vehicle adoption, particularly in China and progressive Southeast Asian markets, are driving technology adoption cycles and premium positioning for advanced refrigeration systems.

Europe Refrigerated Trailer Market Trends

Europe maintains a substantial 25.4% global market share, anchored by sophisticated cold chain infrastructure, stringent regulatory regimes, and established manufacturing capabilities concentrated in Germany and France. The European Union's F-Gas Regulation has established global leadership in low-GWP refrigerant adoption, mandating the phase-down of high-GWP refrigerants and driving wholesale industry transition toward natural refrigerants, including CO2 and hydrocarbons. This regulatory leadership has positioned European manufacturers, including Schmitz Cargobull, Kögel Trailer GmbH, Lamberet SAS, and Bernard Krone, at the forefront of sustainable refrigeration technology development.

European regulatory frameworks, including the UK's Clean Growth Strategy and commitment to reducing carbon emissions, have incentivized the adoption of energy-efficient refrigerated trailers and electric-powered solutions. The UK refrigerated trailer market has experienced significant growth, driven by e-commerce food delivery expansion, online grocery shopping, and consumer expectations for rapid, fresh product delivery.

In May 2024, the Endurance solar-powered zero-emission reefer trial in the UK demonstrated renewable energy integration potential, with real-time cloud monitoring ensuring optimal performance. France's established position as a refrigeration technology centre, anchored by Lamberet SAS specialisation in pharmaceutical-grade temperature control systems, has reinforced European leadership in specialised cold chain solutions serving pharmaceutical and sensitive product applications.

Competitive Landscape

The global refrigerated trailer market is moderately consolidated, with a few major players holding significant shares while numerous smaller and regional manufacturers operate alongside them. Leading companies such as The Lincoln Electric Company, Miller Electric Mfg. LLC, Ador Welding Limited, voestalpine Böhler Welding Group GmbH, Carl Cloos Schweisstechnik GmbH, and OTC DAIHEN Inc. dominate through advanced technologies, diverse product portfolios, and strong global distribution networks.

Competition is driven by product innovation, reliability, automation integration, and technical support rather than price alone. While North America and Europe are led by established multinationals, the Asia-Pacific features rising local and cost-competitive players. Mid-tier companies like ACRO Automation Systems and Mitco Weld Products contribute to niche applications and specialised solutions.

Key Industry Developments

- In January 2026, Schmitz Cargobull delivered its 1,000th S.KO COOL refrigerated trailer to NORDFROST GmbH & Co. KG, marking over 30 years of collaboration. NORDFROST, celebrating its 50th anniversary in 2025, continues to lead in frozen food logistics across Germany with advanced double-evaporator refrigerated trailers, enhancing flexibility and efficiency in temperature-controlled transport throughout Europe.

- On 29 October 2025, Gist deployed 44-pallet refrigerated trailers from Gray & Adams, marking the UK’s first 44-pallet double-deck reefer trailers. The 13.6m trailers feature dual- and single-temperature Carrier refrigeration units, optimised airflow for fuel efficiency, and retractable tail-lifts, offering a 10% increase in pallet capacity and enhanced operational productivity for temperature-controlled logistics across the UK and Europe.

Companies Covered in Refrigerated Trailer Market

- Wabash National Corporation

- Schmitz Cargobull AG

- Great Dane LLC.

- Utility Trailer Manufacturing Company

- CIMC Vehicles Group Co., Ltd.

- Kögel Trailer GmbH & Co. KG

- Lamberet SAS

- Fahrzeugwerk Bernard Krone GmbH & Co. KG

- Hyundai Translead, Inc.

- Gray & Adams Ltd.

Frequently Asked Questions

The Global Refrigerated Trailer Market is projected to be valued at US$ 7.1 Bn in 2026.

The Single-Temperature segment is expected to account for approximately 52.3% of the Global Refrigerated Trailer Market by Temperature Class in 2026.

The market is expected to witness a CAGR of 6.5% from 2026 to 2033.

Growth in the Refrigerated Trailer Market is driven by booming e-commerce grocery and last-mile cold logistics, rising pharmaceutical and biological transport needs, and expanding global trade in perishable food, supported by major cold-chain infrastructure investments.

Key opportunities in the Refrigerated Trailer Market lie in zero-emission electric and hybrid refrigeration systems, solar-assisted renewable cooling solutions, and multi-temperature trailer technologies that enable mixed-load optimisation and sustainable cold-chain operations.

Key players in the Refrigerated Trailer Market include Thermo King, Utility Trailer Manufacturing Company, Schmitz Cargobull, Kögel, Wabash National, and Lamberet.