- Automation & Robotics

- Radio Shuttle System Market

Radio Shuttle System Market Size, Share, and Growth Forecast, 2026 – 2033

Radio Shuttle System Market by Product Type (Semi-Automatic, Fully Automatic, Manual), Application (Retail, Food & Beverage, Pharmaceuticals, Automotive, Electronics), End-User (Large Enterprises, Small & Medium Enterprises (SMEs)), and Regional Analysis for 2026-2033

Radio Shuttle System Market Share and Trends Analysis

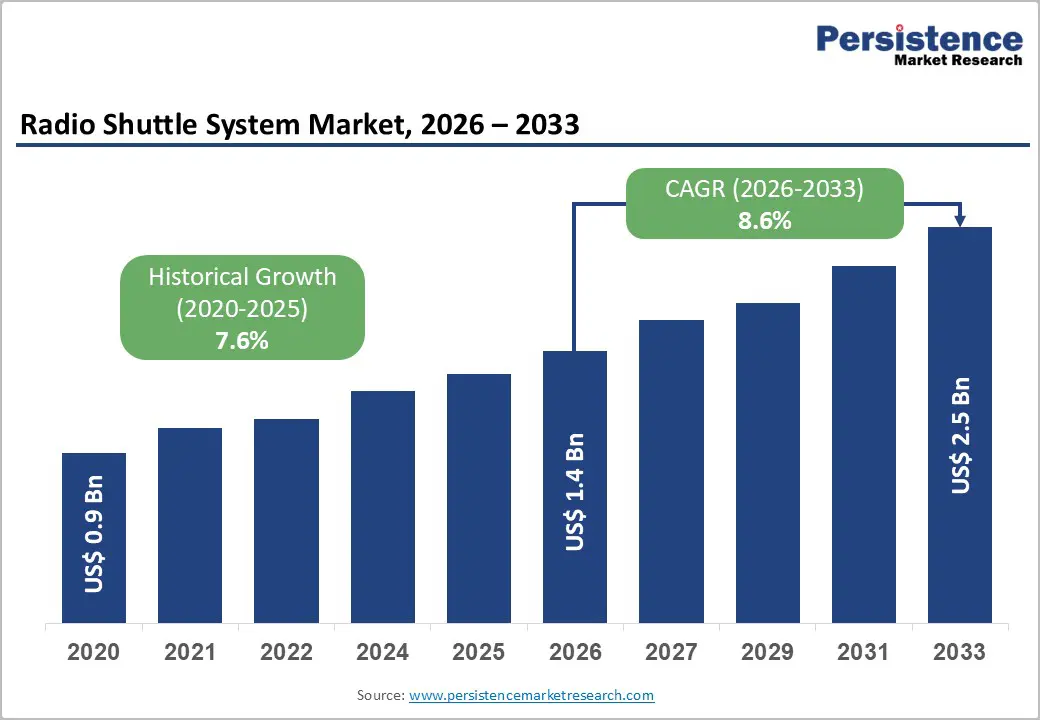

The global radio shuttle system market size is likely to be valued at US$ 1.4 billion in 2026, and is projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 8.6% during the forecast period 2026−2033. The bright outlook of the market is attributable to accelerating warehouse automation adoption across logistics, retail, and manufacturing ecosystems. Expansion of e-commerce distribution networks increases pallet storage density requirements, which elevates demand for compact automated storage technologies. Rapid industrial digitization strengthens integration between warehouse management systems and shuttle-based material handling platforms, improving operational efficiency and asset traceability.

Labor shortages across developed and emerging economies encourage deployment of automated pallet movement solutions that reduce dependence on manual handling. Regulatory emphasis on workplace safety issued by agencies such as Occupational Safety and Health Administration (OSHA) supports automation adoption as firms seek compliance through mechanized material transport. Infrastructure modernization initiatives in Asia Pacific and Middle East industrial corridors stimulate installation of high-density storage systems, enabling scalable logistics networks aligned with global trade expansion.

Key Industry Highlights

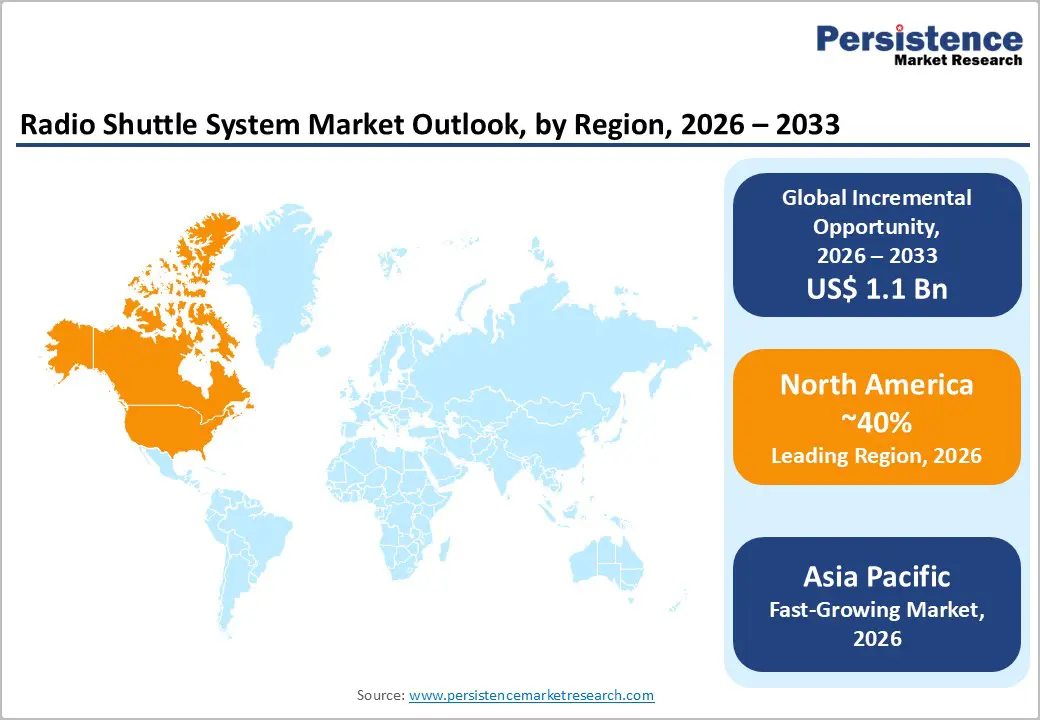

- Dominant Region: North America is projected to hold roughly 39% of the market share in 2026, fueled by heavy investments in scalable high-density storage solutions.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing market from 2026 to 2033, driven by e-commerce growth and widening uptake of IoT-enabled warehouse solutions.

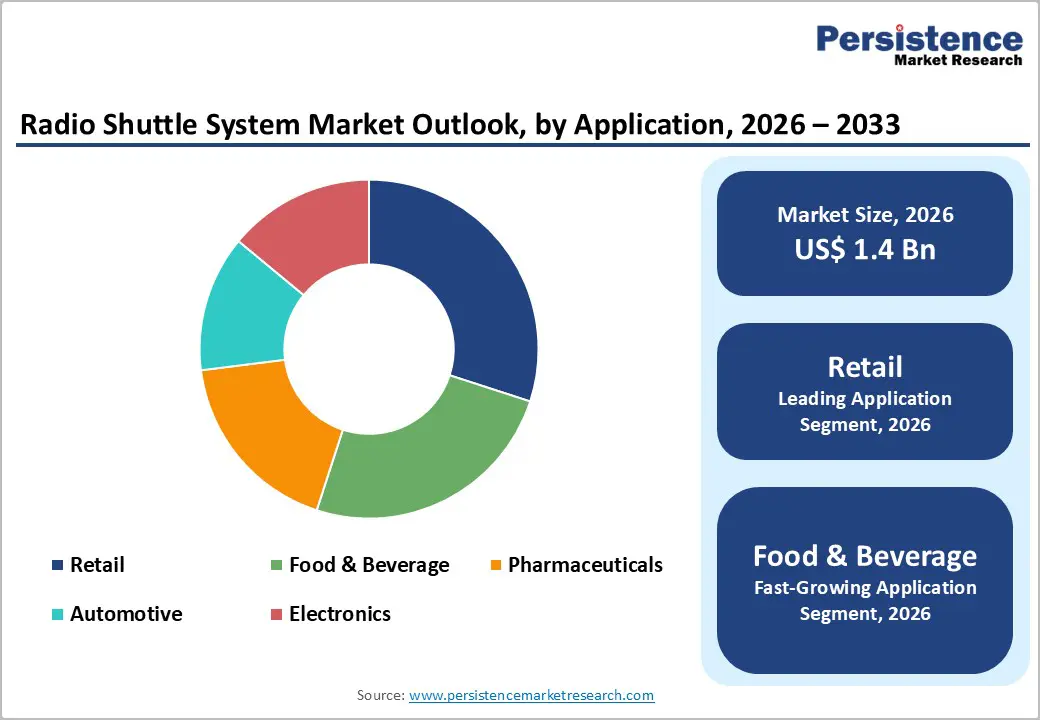

- Leading Application: The retail industry is slated to lead with over 30% market share in 2026, on account of omnichannel fulfilment expansion.

- Fastest-growing Application: The food and beverage industry is expected to grow the fastest through 2033, propelled by cold-chain logistics and stringent food safety standards.

- May 2025: Dematic introduced the FD Shuttle, a locally manufactured, rail-free automated storage and retrieval system (ASRS) for Asia Pacific, designed to deliver high-density storage, flexible configurations, and throughput of up to 1,000 cases per hour.

| Key Insights | Details |

|---|---|

| Radio Shuttle System Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Automation Expansion across Supply Chains

Expansion of automation across supply networks reshapes material-flow architecture, prompting enterprises to deploy high-density storage, synchronized transport, and algorithm-directed inventory movement. Automated manufacturing environments depend on predictable throughput and minimal human intervention, which raises demand for shuttle-based pallet handling capable of integrating with robotics, warehouse control systems, and real-time analytics. Government analysis from NITI Aayog indicates frontier technologies such as AI, robotics, and digital twins elevate efficiency, precision, and adaptability in production ecosystems, reinforcing industrial competitiveness. This transformation reshapes facility layouts toward compact, vertically optimized storage nodes that complement automated picking, sequencing, and dispatch functions. Capital allocation trends reinforce this shift, illustrated by 2025 data showing 36,766 robots ordered in North America, a 6.6 % annual increase, reflecting broad investment in automation infrastructure across sectors.

Supply chain digitization strategies prioritize accuracy, traceability, and rapid order fulfillment, conditions that favor shuttle-based pallet movement integrated with sensors, programmable logic controllers (PLCs), and warehouse execution platforms. Automated environments require consistent cycle times, reduced manual travel distance, and synchronized upstream-downstream material flow, conditions suited to mechanized load transfer systems. Research shows magnetic-levitation conveyor technology with artificial intelligence control improves throughput, reduces downtime, and adapts routing dynamically to production demand, demonstrating operational advantages of automated transport frameworks. Industrial enterprises pursuing lean inventory models and just-in-sequence delivery structures adopt such solutions to maintain production continuity while lowering labor intensity.

Workplace Safety Regulations and Labor Constraints

Regulatory enforcement intensity across industrial facilities elevates automation adoption priorities. Official data from the Health and Safety Executive indicate 680,000 workers sustained workplace injuries during 2024–2025, with 40.1 million working days lost and £ 22.9 billion economic cost, demonstrating material financial exposure linked to unsafe manual operations. Compliance frameworks therefore incentivize infrastructure redesign that reduces human contact with moving loads, high-bay racks, and vehicle pathways. Mechanical handling automation limits fall risk, repetitive strain, and collision exposure, aligning operational processes with statutory safety thresholds and insurer requirements. Warehousing environments illustrate risk concentration; injury rates exceed many sectors and hazards include vehicle incidents, lifting strain, and falls.

Workforce demographics reveal aging personnel and high attrition tied to long hours and limited progression, restricting scalable manual throughput. Talent scarcity constrains facility expansion timelines, prompting management teams to prioritize equipment that sustains output with minimal headcount growth. Automated pallet transport platforms address productivity continuity, scheduling predictability, and training burden reduction, aligning labor economics with operational targets. Regulatory scrutiny, injury-cost exposure, and workforce contraction collectively reshape capital expenditure strategy toward mechanized intralogistics solutions that stabilize performance metrics and reduce compliance risk.

High Initial Capital Investment Requirements

Large-scale automation infrastructure demands substantial upfront funding across equipment procurement, facility redesign, and digital integration layers, creating a financial threshold that limits participation among small and mid-scale enterprises. Capital planning frameworks within industrial organizations prioritize projects with rapid payback visibility, while robotic storage systems involve extended depreciation cycles and complex commissioning stages. Engineering assessments, simulation modeling, and structural reinforcement raise pre-installation expenditure before operational output begins. Financial institutions frequently classify advanced intralogistics technology as specialized industrial assets, leading to stricter lending conditions and elevated collateral expectations.

Operational transition costs further influence investment decisions, as system deployment requires workforce training, software configuration, safety certification, and compatibility validation with warehouse management platforms. Production environments relying on continuous throughput face revenue exposure during installation phases, prompting management teams to defer adoption until financial reserves strengthen. Maintenance agreements, spare component inventories, and periodic software licensing introduce long-term financial obligations that extend beyond acquisition expenditure. Corporate finance divisions evaluate these commitments alongside alternative capital uses such as fleet expansion or capacity scaling, often ranking automation projects lower in priority order.

Integration Complexity with Legacy Infrastructure

Deployment of advanced automated storage platforms faces resistance in facilities operating with aging control architectures, proprietary communication protocols, and fragmented warehouse management environments. Legacy programmable logic controllers, outdated enterprise resource planning platforms, and fixed conveyor logic often lack interoperability layers required for modern robotic orchestration, forcing extensive middleware customization and interface engineering. Technical teams encounter configuration conflicts between real-time motion software and static command structures embedded in older systems, resulting in prolonged commissioning cycles and elevated engineering expenditure. Operational continuity requirements limit modernization windows and constrain adoption timelines in environments heavily reliant on existing infrastructure.

Financial exposure represents another structural barrier. Integration initiatives demand redesign of control logic, network architecture upgrades, and validation testing to prevent disruptions in inventory throughput. Legacy environments generate data silos, raise maintenance spending, and slow digital transformation, demonstrating measurable efficiency drag tied to outdated infrastructure. Skilled engineering resources remain necessary for protocol translation, sensor calibration, and safety certification alignment, increasing dependence on external integrators and lengthening project schedules. Production managers frequently prioritize system stability over architectural replacement due to risk exposure linked to downtime, calibration errors, or synchronization failures across automated handling subsystems.

Expansion of High-Density Warehousing in Emerging Economies

Rapid scaling of warehousing infrastructure across emerging economies is underpinned by structural shifts in logistics and supply chain economics, supported by government policy interventions aimed at reducing systemic inefficiencies. Governments are deploying integrated logistics strategies through frameworks such as India’s National Logistics Policy, which aligns multimodal transport planning and digital platforms to strengthen storage and distribution networks at regional nodes, improve freight movement efficiency, and push logistics costs closer to global benchmarks. These policy-driven enhancements are catalyzing decentralized infrastructure growth in tier2 and tier3 cities, unlocking new catchment areas for goods distribution and improving access to manufacturing hinterlands.

Official data from India’s Ministry of Commerce shows that industrial and warehousing leasing activity reached 20million square feet in the first half of 2025, with year-on-year growth of 33%, driven by third-party logistics and e-commerce occupiers, and robust supply of Grade A space across key markets such as Delhi NCR and Chennai. Emerging economies are simultaneously experiencing rapid consumption growth and digital commerce expansion, which is reshaping distribution strategies toward high-density storage models that optimize throughput and minimize end-to-end supply chain costs. Warehouse networks in these markets are increasingly integrated with national freight corridors and multimodal logistics parks, reducing transit times and enabling scalable service to national and regional markets. Built-for-purpose facilities with enhanced vertical storage and mechanized handling capabilities are preferred over conventional low-density sheds, improving space utilization and lowering per-unit storage costs.

Technological Convergence with Digital Logistics Platforms

Integrating advanced technologies with comprehensive digital logistics platforms unlocks operational synergies between planning, execution and decision-making layers, creating visibility and predictive control across the end-to-end supply chain. Cloud computing and connected sensor networks collect real-time data from vehicles, cargo and infrastructure, enabling adaptive scheduling, remote monitoring and performance analytics that reduce idle time and waste. Platforms that unify data flows support automated dispatch, dynamic routing and resource matching, raising throughput and lowering unit costs while improving service reliability.

The convergence of disparate technologies on unified digital logistics platforms also strengthens strategic planning and risk management functions. Predictive analytics and machine learning models process historical and live data to anticipate demand shifts, capacity constraints and disruption risks, enabling proactive mitigation actions rather than reactive firefighting. Shared platform standards enhance interoperability among carriers, terminals, warehouses and customs, reducing friction in multi-modal transfers and compliance workflows.

Category-wise Analysis

Product Type Insights

Semi-automatic radio shuttle systems are likely to be the leading segment with 58% revenue share in 2026, due to widespread adoption among mid-scale warehouses seeking partial automation without full infrastructure replacement. Semi-automatic platforms require lower capital expenditure compared with fully automated alternatives, which supports accessibility for operators transitioning from manual storage methods. Equipment flexibility allows integration with existing forklifts, reducing training complexity and facilitating operational continuity. Logistics managers often prefer semi-automatic solutions because deployment timelines remain shorter and maintenance requirements remain manageable. Compatibility with conventional warehouse layouts supports rapid installation across diverse facility designs.

Fully automatic radio shuttle systems are expected to witness the fastest growth between 2026 and 2033, as logistics networks prioritize end-to-end automation capable of minimizing human intervention. Fully automated platforms integrate with warehouse management software and robotic transport equipment, enabling synchronized material handling operations. Large distribution centers handling high throughput volumes benefit from automated shuttle fleets capable of continuous pallet movement without operator presence. Digital control systems enhance accuracy in pallet placement and retrieval, improving inventory management reliability. Expansion of smart warehouse initiatives supports adoption of fully automated platforms across large logistics hubs.

Application Insights

Retail industry is poised to lead with a forecasted over 30% of the radio shuttle system market revenue share in 2026, owing to the rapid expansion of omnichannel fulfillment infrastructure and rising demand for high-density storage in urban distribution centers. Retail supply chains require efficient pallet handling to support frequent inventory turnover and seasonal demand variability. Automated shuttle systems enable optimized storage layouts that improve order processing speed and reduce handling errors. Consumer trust in rapid delivery services increases pressure on retailers to maintain accurate inventory visibility, which encourages adoption of automated storage technologies integrated with digital tracking systems.

Food and beverage industry is anticipated to be the fastest-growing segment between 2026 and 2033, driven by stringent product handling standards and growing cold-chain logistics requirements. Temperature-controlled warehouses benefit from automated storage systems that reduce human exposure and maintain consistent environmental conditions. Cultural acceptance of packaged and processed food products increases distribution complexity, requiring efficient pallet movement technologies. Regulatory oversight on food safety encourages use of automated systems that minimize contamination risk through reduced manual handling. Expansion of digital commerce platforms for grocery delivery supports growth of automated storage infrastructure capable of handling high-volume palletized goods with traceability.

Regional Insights

North America Radio Shuttle System Market Trends

North America is anticipated to secure approximately 39% of the radio shuttle system market share in 2026, reflecting robust adoption of automation technologies in distribution and manufacturing operations across the United States, Canada, and Mexico. Advanced integration of warehouse management systems with robotics and sensor networks supports high-density storage and accelerated order fulfillment, enabling significant operational efficiency gains. Investment by large-scale e-commerce and third-party logistics operators in modular storage solutions allows flexible scaling in response to fluctuating demand, reducing capital expenditure per throughput unit. Supply chain digitization, combined with predictive maintenance of automated shuttles, minimizes downtime and maximizes asset utilization, creating a competitive advantage in service reliability and operational cost control.

Strong regulatory support for workplace safety and energy-efficient operations in the United States and Canada contributes to adoption, as automated systems reduce manual handling and optimize energy consumption of storage facilities. Mature industrial infrastructure in Mexico, combined with skilled technical workforce and availability of advanced software platforms, facilitates rapid deployment and integration of shuttle systems into complex logistics networks. Strategic partnerships between technology providers and distribution operators accelerate innovation cycles and deployment, reinforcing market leadership.

Europe Radio Shuttle System Market Trends

Europe demonstrates steady adoption of radio shuttle systems, driven by modernization of logistics networks and the demand for efficient inventory management across Germany, France, the United Kingdom, Italy, and the Netherlands. High penetration of e-commerce and omni-channel retail operations necessitates advanced automated storage and retrieval systems to manage complex order fulfillment processes. Companies increasingly implement modular shuttle systems combined with warehouse management software and robotics to optimize space utilization, reduce cycle times, and support rapid scaling of operations. Integration with energy-efficient designs and predictive maintenance algorithms enhances operational reliability while lowering electricity consumption and maintenance costs.

Regulatory frameworks emphasizing workplace safety, environmental standards, and energy efficiency incentivize the deployment of automation in industrial and distribution facilities. National initiatives, such as Germany’s Industry 4.0 and France’s Industrie du Futur, promote adoption by providing funding, technical support, and standardized protocols for smart factory implementation. Collaboration between technology providers, logistics operators, and research institutions fosters innovation in shuttle designs, software interoperability, and data-driven operational strategies. Availability of skilled technical personnel enables rapid system deployment and fine-tuning, ensuring consistent throughput in high-demand facilities.

Asia Pacific Radio Shuttle System Market Trends

Asia Pacific is forecasted to be the fastest-growing market for radio shuttle systems between 2026 and 2033, propelled by rapid industrial expansion, rising e-commerce volumes, and large-scale investment in modern logistics infrastructure across China, India, Japan, and South Korea. Accelerated adoption of automated storage and retrieval systems addresses increasing warehouse throughput requirements and supports multi-channel distribution demands. Integration of Internet of Things (IoT) sensors and cloud-based warehouse management systems enables real-time monitoring, predictive maintenance, and optimized routing, allowing companies to improve operational efficiency while maintaining low operational costs. Expansion of organized retail and cross-border trade further drives the need for high-density storage solutions capable of handling complex logistics networks.

Government initiatives promoting smart manufacturing and logistics modernization, such as China’s Made in China 2025 strategy and India’s National Logistics Policy, reinforce adoption by providing incentives for automation deployment. Investments in port modernization, industrial parks, and e-commerce fulfillment centers facilitate seamless implementation of high-speed shuttle systems. Skilled workforce availability, growing domestic technology ecosystem, and partnerships between local logistics operators and global technology providers accelerate deployment cycles.

Competitive Landscape

The global radio shuttle system market structure exhibits moderate fragmentation with a combination of large-scale automation corporations and specialized regional system integrators. Leading players such as Daifuku, MURATA MACHINERY, toyota-forklifts.eu, Jungheinrich AG, and Dematic dominate revenue generation through extensive portfolios of high-density storage and retrieval solutions. Competitive advantage in this environment relies on advanced engineering capabilities, seamless software integration, and comprehensive service networks that support installation, maintenance, and system optimization.

Companies focusing on modular, scalable solutions benefit from flexibility to adapt to diverse warehouse layouts, automation requirements, and throughput demands, reinforcing leadership in complex supply chain environments. Regional manufacturers and integrators strengthen presence by delivering tailored solutions addressing local infrastructure, regulatory compliance, and operational preferences. Emphasis on after-sales support, training programs, and rapid deployment services enhances adoption in mid-size and emerging industrial facilities. Collaboration with technology partners accelerates innovation in shuttle mechanics, control software, and predictive maintenance systems.

Key Industry Developments

- In February 2026, Interlake Mecalux announced that it will showcase its latest intralogistics innovations at MODEX 2026, including autonomous mobile robots (AMRs), automated shuttle storage systems, and its Easy Warehouse Management System (Easy WMS) software with AI.

- In December 2025, China-based MAXRAC reported successful completion of more than 20 radio shuttle system installations worldwide as part of expanded international warehouse automation deployment.

- In October 2025, Eurorack launched its WiFi-enabled shuttle robot as a smart warehousing solution, combining high-density racking with remote-controlled robotic pallet handling to boost storage efficiency and cut operational costs for logistics operators.

Companies Covered in Radio Shuttle System Market

- Daifuku Co., Ltd.

- MURATA MACHINERY, LTD.

- toyota-forklifts.eu

- Jungheinrich AG

- Dematic

- Vanderlande Industries B.V.

- Honeywell International Inc

- KION GROUP AG

- Swisslog Holding AG

Frequently Asked Questions

The global radio shuttle system market is projected to reach US$ 1.4 billion in 2026.

Demand for high-density, automated warehouse storage and labor-efficient material handling is driving the market.

The market is poised to witness a CAGR of 8.6% from 2026 to 2033.

Expansion of high-density warehousing in emerging economies and integration with digital logistics platforms present key market opportunities.

Some of the key market players include Daifuku Co., Ltd., MURATA MACHINERY, LTD., toyota-forklifts.eu, Jungheinrich AG, and Dematic.