- Biotechnology

- Radiopharmaceutical Manufacturing Market

Radiopharmaceutical Manufacturing Market Size, Share, and Growth Forecast, 2026 - 2033

Radiopharmaceutical Manufacturing Market by Radioisotope (Technetium-99m, Other), Technology (Cyclotron-based Manufacturing, Other), Application (Oncology, Others), End-user, and Regional Analysis for 2026 – 2033

Radiopharmaceutical Manufacturing Market Size and Trends Analysis

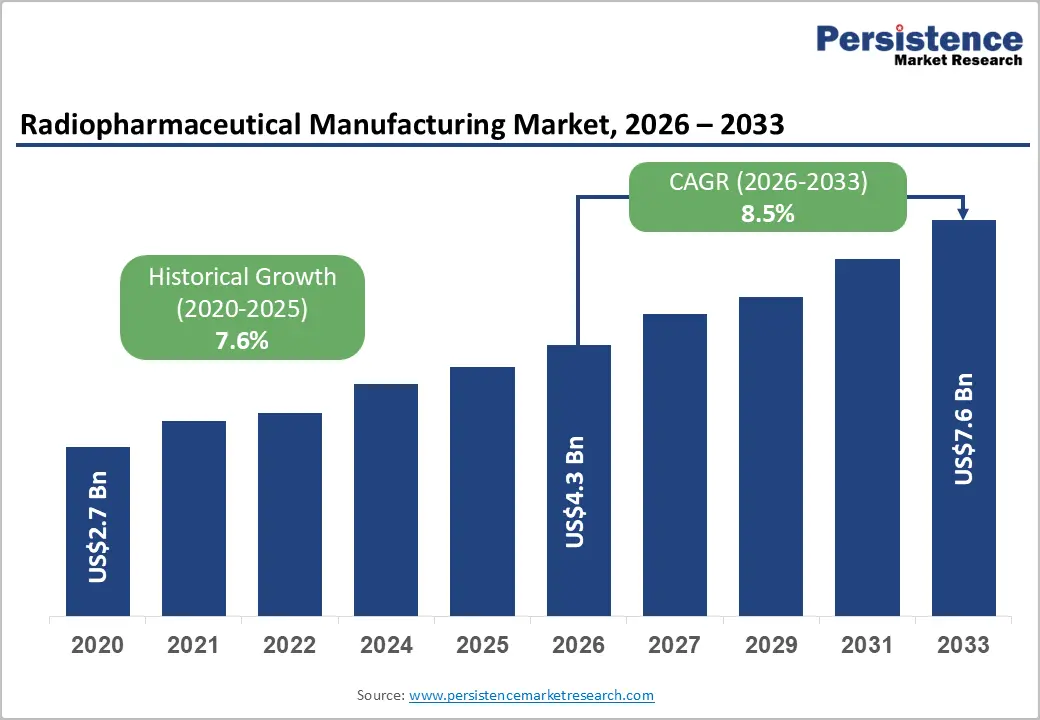

The global radiopharmaceutical manufacturing market size is likely to be valued at US$4.3 billion in 2026, and is expected to reach US$7.6 billion by 2033, growing at a CAGR of 8.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cancer and cardiovascular diseases requiring targeted radionuclide therapy, rapid expansion of precision oncology with theranostic agents, growing demand for Lutetium-177 and Gallium-68 labeled compounds, and rising investments in domestic cyclotron and generator infrastructure to reduce supply shortages.

Growing demand for cyclotron-based manufacturing of Fluorine-18 and Gallium-68, especially in oncology and diagnostic imaging, is accelerating adoption across hospitals and diagnostic centers. Increasing recognition of radiopharmaceutical manufacturing as critical for early diagnosis, personalized treatment, and improved survival in emerging theranostics and nuclear medicine markets remains a major driver of market growth.

Key Industry Highlights:

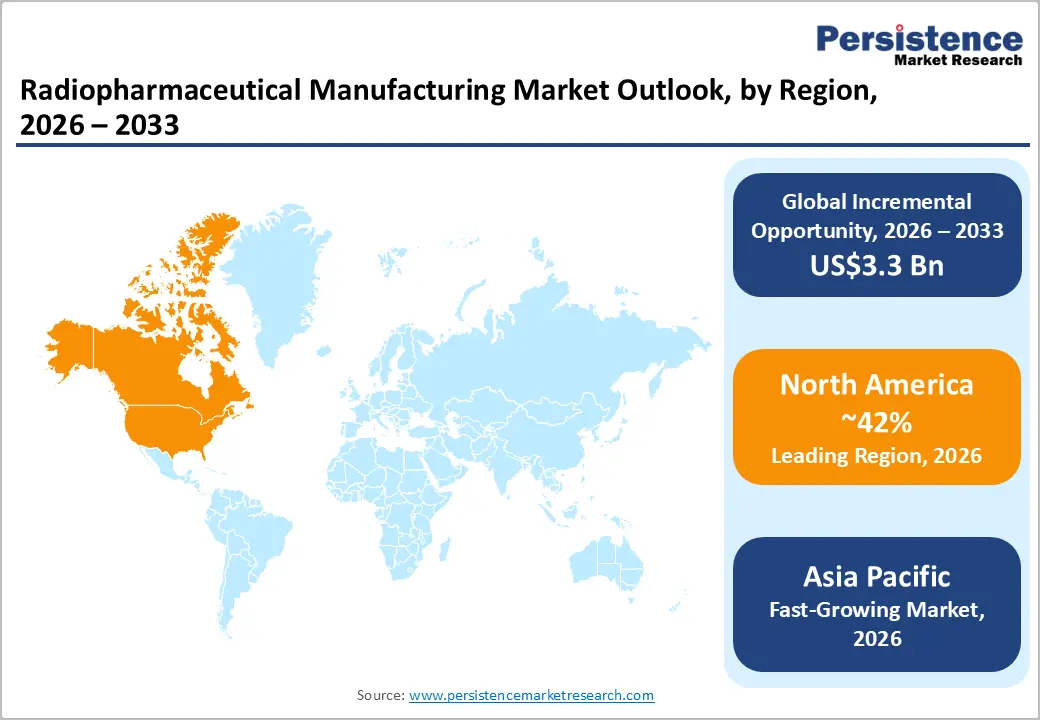

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by advanced theranostic centers, high PET/CT utilization, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising cancer incidence, rapid cyclotron installation, and growing PRRT access in China and India.

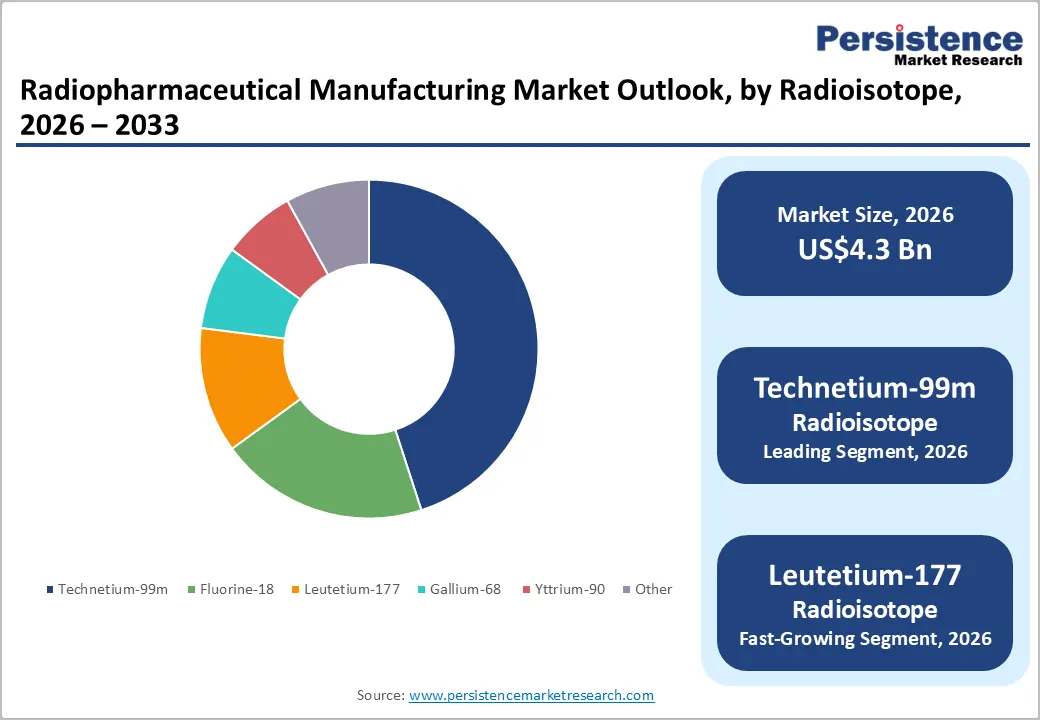

- Dominant Radioisotope: Technetium-99m, to hold approximately 45% of the market share, as it remains the backbone of diagnostic nuclear medicine.

- Leading Technology: Cyclotron-based manufacturing, contributing nearly 42% of the market revenue, due to the highest production of short-lived PET isotopes.

| Key Insights | Details |

|---|---|

| Radiopharmaceutical Manufacturing Market Size (2026E) | US$4.3 Bn |

| Market Value Forecast (2033F) | US$7.6 Bn |

| Projected Growth CAGR (2026-2033) | 8.5% |

| Historical Market Growth (2020-2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Cancer Burden and Theranostics Expansion

The growing global burden of cancer is a major factor accelerating demand in the radiopharmaceutical manufacturing market, particularly for diagnostic and therapeutic isotopes used in nuclear medicine. According to the World Health Organization, approximately 20 million new cancer cases and 9.7 million cancer-related deaths were reported worldwide in 2022, making cancer one of the leading causes of mortality globally. The rising incidence of cancers such as lung, breast, colorectal, and prostate cancers is increasing the need for advanced imaging and targeted treatment technologies that rely on radiopharmaceuticals for precise disease detection and management.

The expansion of theranostics, which integrates diagnostic imaging with targeted radionuclide therapy, is further strengthening demand for radiopharmaceutical production. Theranostic approaches use the same molecular target for both imaging and treatment, enabling clinicians to identify tumors and deliver personalized radiation therapy. As cancer cases continue to grow, this precision-medicine approach is gaining importance in oncology care. Future projections highlight the scale of this opportunity. The World Health Organization estimates that global cancer cases could reach more than 35 million by 2050, representing a 77% increase compared with 2022 levels due to population aging, lifestyle factors, and environmental risks.

Increasing Cyclotron Network and Domestic Production

Expansion of cyclotron infrastructure and increasing domestic production capabilities are strengthening the growth of the radiopharmaceutical manufacturing market. Cyclotrons play a critical role in producing short-lived medical isotopes such as Fluorine-18, Carbon-11, and Gallium-68 that are widely used in positron emission tomography (PET) and single photon emission computed tomography (SPECT) imaging. Government initiatives aimed at strengthening nuclear medicine infrastructure are significantly improving isotope availability for hospitals and diagnostic centers. India has been actively expanding its medical cyclotron network to support local radiopharmaceutical manufacturing.

India operates over 20 operational medical cyclotron facilities across government and private institutions, supporting domestic radiopharmaceutical production. These facilities produce isotopes such as Fluorine-18 for FDG PET scans, which are widely used for cancer detection. Government research centers such as the Variable Energy Cyclotron Centre (VECC) under the Department of Atomic Energy have also strengthened domestic isotope production. The 30 MeV medical cyclotron facility in Kolkata, operational since September 2018, produces radiopharmaceuticals including 18F-FDG, 18F-NaF, and Gallium-68-based tracers for cancer diagnosis and other nuclear medicine applications.

Barrier Analysis – Short Half-Life and Complex Logistics

Short half-life of medical isotopes and complex logistics remain significant challenges in the radiopharmaceutical manufacturing market. Many commonly used isotopes used in nuclear medicine decay rapidly, which means they must be produced, processed, and delivered to healthcare facilities within a very limited time window. Isotopes such as those used in positron emission tomography (PET) imaging often lose their activity within a few hours, making time-sensitive coordination essential across production facilities, transport providers, and hospitals.

Due to this rapid decay, radiopharmaceutical manufacturing facilities are often located close to diagnostic centers or large hospital networks to ensure timely distribution. The need for specialized handling, radiation safety measures, and regulatory compliance also increases operational complexity. In addition, transportation requires shielded containers, trained personnel, and strict adherence to radiation transport regulations.

Shortage of Skilled Nuclear Medicine Professionals

The production and handling of radiopharmaceuticals require highly specialized expertise in radiochemistry, nuclear physics, pharmacy, and radiation safety. Professionals involved in this field must be trained to operate cyclotrons, manage radioactive materials, conduct quality control procedures, and ensure compliance with strict safety and regulatory standards. However, the number of trained experts in nuclear medicine remains limited in many regions, particularly in developing countries.

Skilled personnel are also required in hospitals and diagnostic centers to prepare, administer, and monitor radiopharmaceuticals used in imaging and therapeutic procedures. The lack of adequately trained radiopharmacists, radiochemists, and nuclear medicine technologists can slow the expansion of nuclear medicine services and limit the operational capacity of manufacturing facilities.

Opportunity Analysis – Increasing Clinical Trials and R&D for Novel Radiotracers

Growing scientific research in nuclear medicine is creating significant opportunities for innovation in radiopharmaceutical manufacturing. Research institutions, academic centers, and pharmaceutical companies are increasingly focusing on developing novel radiotracers that can improve disease detection, treatment monitoring, and targeted therapy. These new tracers are designed to bind to specific biological pathways or molecular targets, enabling physicians to visualize disease processes at a much earlier stage compared to conventional imaging techniques.

Clinical trials play a critical role in validating the safety, effectiveness, and diagnostic accuracy of these emerging radiotracers. Through structured clinical studies, researchers evaluate how newly developed isotopes perform in detecting cancers, neurological disorders, and cardiovascular diseases. As nuclear medicine continues to evolve toward more precise and personalized healthcare, radiotracers that target specific receptors, enzymes, or tumor markers are gaining increasing attention. Research efforts are also exploring the use of therapeutic isotopes that can deliver targeted radiation directly to diseased cells while minimizing damage to surrounding healthy tissue. This approach supports the growing concept of targeted radionuclide therapy, where imaging and treatment can be integrated using related compounds.

Advancements in Nuclear Imaging Technologies

Continuous technological improvements in nuclear imaging systems are playing a major role in expanding the use of radiopharmaceuticals for disease diagnosis and monitoring. Imaging modalities such as positron emission tomography (PET) and single-photon emission computed tomography (SPECT) rely on radiotracers to visualize physiological processes inside the body. The integration of these systems with advanced imaging platforms such as PET/CT and SPECT/CT has significantly improved diagnostic accuracy by combining functional imaging with detailed anatomical information. This integration allows clinicians to detect diseases at earlier stages and monitor treatment responses more effectively.

Modern imaging technologies are also enabling the development of new radiotracers designed to target specific biological pathways. These tracers help identify tumors, neurological disorders, and cardiovascular abnormalities with greater precision. Improvements in detector sensitivity, image reconstruction software, and digital imaging technologies have further enhanced image quality while reducing scanning time and radiation exposure for patients.

Category-wise Analysis

Type of Radioisotope Insights

The Technetium-99m segment is anticipated to dominate the market, accounting for 45% of the market share in 2026. Its dominance is driven by its extensive use in diagnostic imaging procedures. Technetium-99m is widely used in nuclear medicine because of its ideal physical properties, including suitable gamma emission and a short half-life that minimizes radiation exposure to patients. It is commonly utilized in imaging procedures related to cardiology, oncology, bone scans, and renal diagnostics.

TechneLite® technetium-99m generator produced by Lantheus Holdings. The TechneLite generator supplies sodium pertechnetate Tc-99m, which is widely used by hospitals and radiopharmacies to prepare multiple diagnostic imaging agents.

The Lutetium-177 segment represents the fastest-growing radioisotope, due to its increasing use in targeted radionuclide therapy. Lutetium-177 emits both beta particles for treatment and gamma radiation for imaging, allowing physicians to monitor treatment progress. It is widely used in targeted therapies for cancers such as neuroendocrine tumors and prostate cancer, where radioligand therapy delivers radiation directly to tumor cells while minimizing damage to surrounding healthy tissues.

Pluvicto, developed by Novartis through its subsidiary Advanced Accelerator Applications. This therapy uses the radioisotope Lutetium-177 to treat patients with PSMA-positive metastatic prostate cancer by delivering targeted radiation directly to cancer cells.

Technology Insights

Cyclotron-based manufacturing is expected to dominate the market, contributing nearly 42% of revenue in 2026, propelled by its critical role in producing short-lived radioisotopes used in diagnostic imaging. Cyclotrons accelerate charged particles to generate medical isotopes such as Fluorine-18, Carbon-11, and Gallium-68, which are widely used in positron emission tomography (PET) scans. The increasing adoption of PET imaging for cancer detection, neurological disorders, and cardiovascular diseases is driving demand for cyclotron-produced isotopes.

The Medical Cyclotron Facility is operated by the Variable Energy Cyclotron Centre (VECC) in India. The facility uses a 30 MeV medical cyclotron to produce radioisotopes such as Fluorine-18, which is used to manufacture the radiopharmaceutical 18F-FDG for PET imaging in cancer diagnosis. The produced radiopharmaceuticals are supplied commercially by the Board of Radiation and Isotope Technology (BRIT) to hospitals and diagnostic centers.

Generator-based production represents the fastest-growing technology, supported by its ability to provide on-site access to short-lived isotopes without the need for complex cyclotron or reactor facilities. Radioisotope generators produce daughter isotopes from longer-lived parent isotopes, allowing hospitals and radiopharmacies to obtain clinically useful tracers when needed. This approach is widely used for isotopes such as technetium-99m and gallium-68, which are commonly applied in diagnostic imaging and targeted nuclear medicine procedures.

GalliaPharm® Germanium-68/Gallium-68 (??Ge/??Ga) generator developed by Eckert & Ziegler Radiopharma GmbH. This generator system produces Gallium-68 on demand through the radioactive decay of the parent isotope Germanium-68. The produced Gallium-68 is then used to prepare PET imaging radiopharmaceuticals for the diagnosis of conditions such as neuroendocrine tumors and prostate cancer.

Regional Insights

North America Radiopharmaceutical Manufacturing Market Trends

North America is projected to dominate, accounting for nearly 42% of the share in 2026, driven by the region’s high PET/CT utilization, advanced theranostic centers, and high public awareness of precision oncology benefits. Distribution systems in the U.S. and Canada provide extensive support for radiopharmaceutical programs, ensuring wide accessibility across Tc-99m, cyclotron-based, and hospital populations. Increasing demand for short-lived, convenient, and easy-to-produce forms is further accelerating adoption, as these formats improve patient throughput and reduce barriers associated with long-distance transport.

Innovation in radiopharmaceutical manufacturing technology, including stable Ga-68 generators, improved cyclotron targetry, and targeted Lu-177 enhancement, is attracting significant investment from both public and private sectors. Government initiatives and FDA campaigns continue to promote use against supply risks, availability concerns, and emerging theranostic opportunities, creating sustained market demand. The growing focus on oncology grades and specialty uses, particularly for hospitals and others, is expanding the target applications for radiopharmaceutical manufacturing.

Europe Radiopharmaceutical Manufacturing Market Trends

Europe shows a steady growth by increasing awareness of theranostic benefits, strong regulatory systems, and government-led nuclear medicine programs. Countries such as Germany, France, the U.K., and Italy have well-established nuclear medicine frameworks that support routine radiopharmaceutical manufacturing use and encourage adoption of innovative cyclotron-based delivery methods. These high-yield formulations are particularly appealing for oncology populations, regulation-conscious centers, and hospital users, improving availability and coverage rates.

Technological advancements in radiopharmaceutical manufacturing development, such as enhanced generator systems, application-targeted delivery, and improved Lu-177 grades, are further boosting market potential. European authorities are increasingly supporting research and trials for manufacturing against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, locally-produced options is aligned with the region’s focus on preventive isotope shortage and patient access.

Public awareness campaigns and promotion drives are expanding reach in both hospitals and diagnostic centers, while suppliers are investing in Ga-68 and novel variants to increase efficacy.

Asia Pacific Radiopharmaceutical Manufacturing Market Trends

Asia Pacific is likely to be the fastest-growing market for radiopharmaceutical manufacturing in 2026, driven by rising cancer incidence, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting manufacturing campaigns to address oncology growth and emerging theranostic needs. Radiopharmaceutical manufacturing is particularly attractive in these regions due to its scalable administration, ease of adoption, and suitability for large-scale hospitals and Tc-99m drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-produce radiopharmaceuticals, which can withstand challenging logistics conditions and minimize shortage dependence. These innovations are critical for reaching domestic centers and improving overall nuclear medicine coverage. Growing demand for cyclotron-based, F-18, and hospital applications is contributing to market expansion. Public-private partnerships, increased oncology expenditure, and rising investment in manufacturing research and cyclotron capacity are further accelerating growth.

The convenience of radiopharmaceutical delivery, combined with improved availability and reduced risk of treatment delay, positions it as a preferred choice.

Competitive Landscape

The global radiopharmaceutical manufacturing market is characterized by competition between well-established radiopharmaceutical companies and emerging regional producers that are expanding their production capabilities. In North America and Europe, companies such as Advanced Accelerator Applications and Telix Pharmaceuticals maintain strong positions through extensive manufacturing networks, advanced research programs, and close collaborations with oncology treatment providers. These companies are actively developing radioligand therapies and diagnostic tracers based on isotopes such as Lutetium-177 and Gallium-68, strengthening their presence in targeted cancer treatment.

In the Asia Pacific region, regional manufacturers are increasing their participation by offering cost-competitive radiopharmaceutical solutions and expanding domestic isotope production. Investments in cyclotron infrastructure are improving the supply of PET imaging isotopes and reducing the risk of shortages. Generator-based technologies allow healthcare facilities to access radioisotopes on demand. Strategic partnerships, acquisitions, and collaborative research initiatives are further helping companies expand manufacturing capacity, strengthen supply chains, and accelerate the commercialization of innovative radiopharmaceutical products.

Key Industry Developments:

- In February 2026, Prostor Pharma received a manufacturing license from the Russian Ministry of Industry and Trade and launched its own radiopharmaceutical production facility in Yekaterinburg. The GMP-compliant site began producing radium-223 chloride for treating prostate cancer patients with bone metastases. The company also planned to introduce lutetium-177 oxodotreotide therapy for neuroendocrine tumors following regulatory approval. Before this launch, Prostor Pharma produced radium-223 under contract with Ural Federal University.

- In January 2024, Novartis received approval from the U.S. Food and Drug Administration (FDA) for the commercial manufacturing of Pluvicto™ (lutetium Lu 177 vipivotide tetraxetan) at its newly established radioligand therapy manufacturing facility in Indianapolis, Indiana, U.S. The company developed the 70,000-square-foot facility specifically for large-scale radioligand therapy production. The site became Novartis’ second radioligand therapy manufacturing location in the U.S. and the largest and most advanced facility of its kind within the company’s global network.

Companies Covered in Radiopharmaceutical Manufacturing Market

- Advanced Accelerator Applications

- Applied Molecular Therapies

- Cardinal Health

- DuChemBio

- Eckert & Ziegler

- Evergreen Theragnostics

- Isotopia Molecular Imaging

- ITM Isotope Technologies Munich

- Nihon Medi-Physics

- Nucleus RadioPharma

- PentixaPharm

- PharmaLogic

- RadioMedix,

- SOFIE

- Telix Pharmaceuticals

Frequently Asked Questions

The global radiopharmaceutical manufacturing market is projected to reach US$4.3 billion in 2026.

Growth of theranostics and targeted radioligand therapies, enabling combined diagnosis and treatment using isotopes such as Lutetium-177 and Actinium-225.

The radiopharmaceutical manufacturing market is poised to witness a CAGR of 8.5% from 2026 to 2033.

Advancements in nuclear imaging technologies (PET/CT and SPECT/CT) supporting the development of new radiotracers and expand clinical applications in cancer, cardiology, and neurology.

Advanced Accelerator Applications, Telix Pharmaceuticals, ITM Isotope Technologies Munich, Eckert & Ziegler, and SOFIE are the key players.