- Healthcare IT

- Radiology Information Systems Market

Radiology Information Systems Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Radiology Information Systems Market by Component (Software, Hardware, Services), Deployment (Web-based, Cloud-based, On-premise), Platform, End-user, and Regional Analysis from 2025 to 2032

Radiology Information Systems Market Share and Trends Analysis

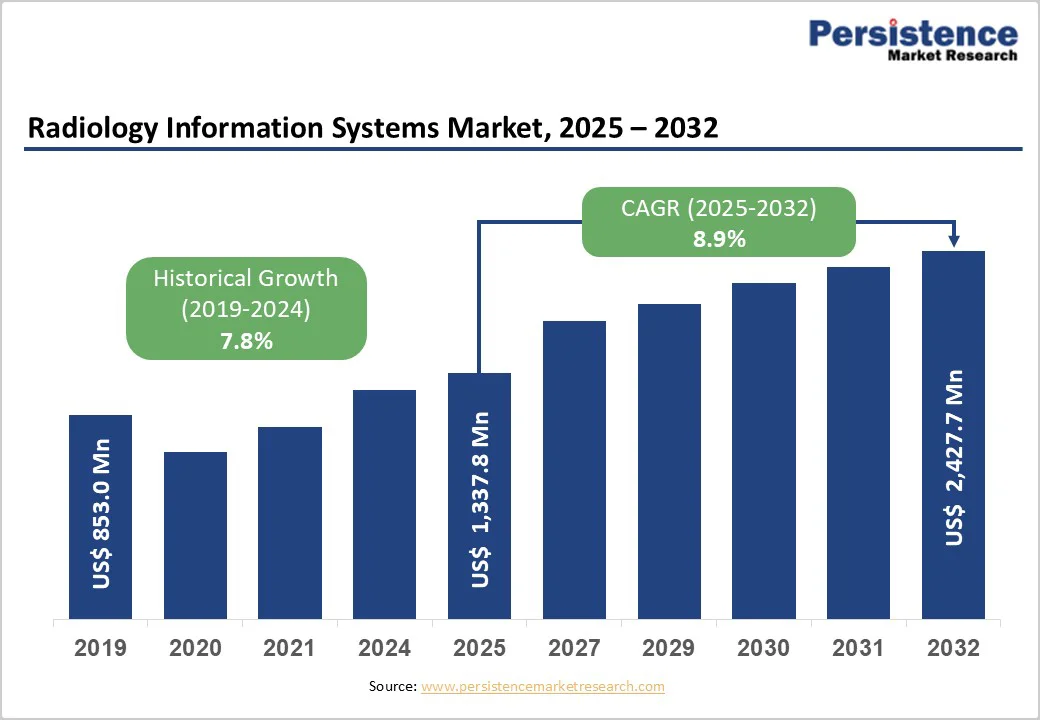

The global radiology information systems market size is estimated to reach US$ 1,337.8 million in 2025 and is projected to reach US$ 2,427.7 million, growing at a CAGR of 8.9% between 2025 and 2032. The global market is gaining momentum due to the increased investments in healthcare information technology. Cloud-based RIS platforms that enable seamless image sharing and data management are attracting significant attention from key market players aiming to enhance clinical workflows.

Key Industry Highlights

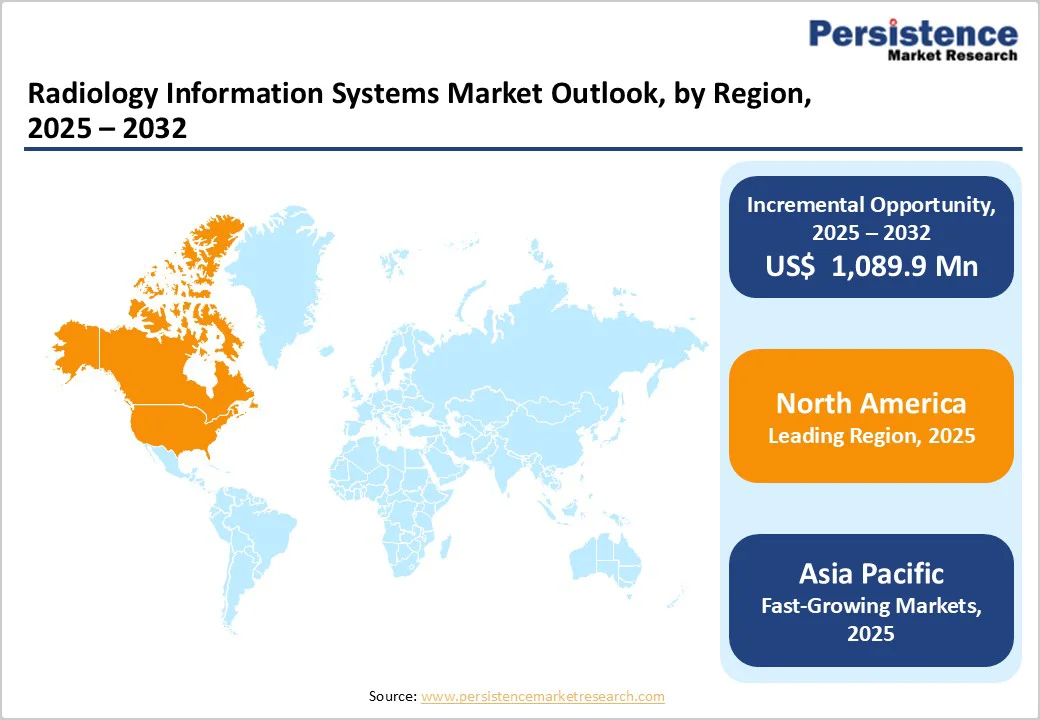

- Leading Region: North America dominates the global market with 42.6%, driven by advanced healthcare IT infrastructure, rapid adoption of AI-enabled workflows, and strong government support for interoperability.

- Fastest-Growing Region: Asia Pacific market is expected to grow rapidly with a CAGR of 11.1% in the forecast period, fueled by expanding imaging infrastructure, adoption of cloud-based RIS, and increasing radiologist shortages.

- Leading Component: Software lead with 51.2% share, supported by AI-powered workflow automation, advanced reporting tools, and integrated PACS connectivity, enabling real-time data management across departments.

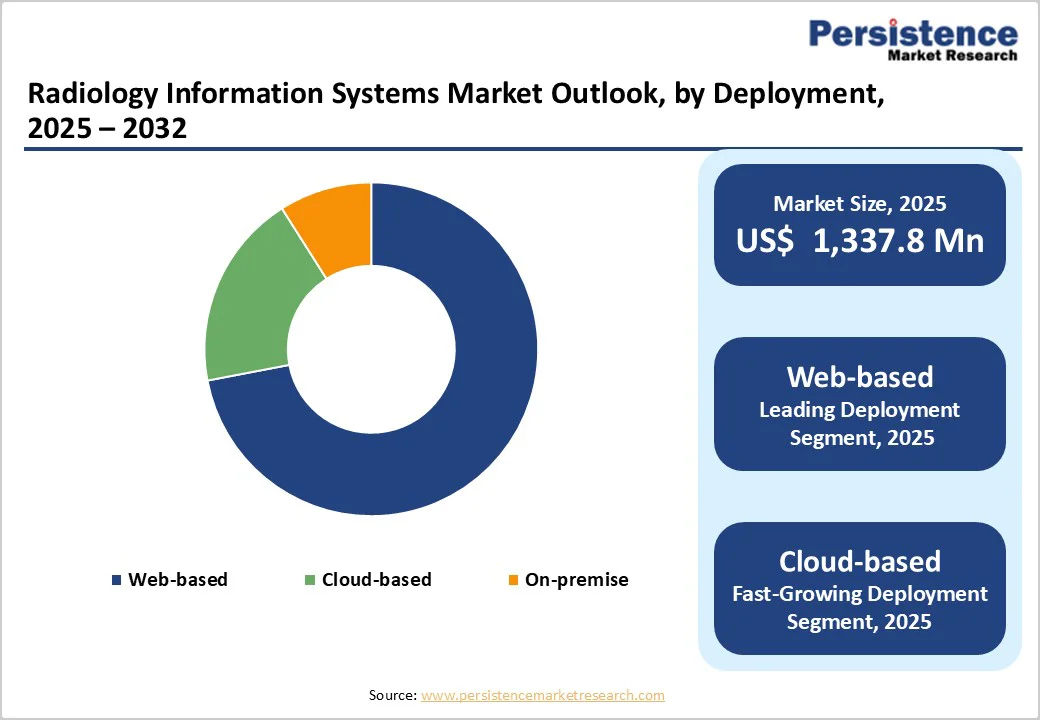

- Leading Deployment: Web-based deployment leads with 72.5%, driven by its browser-accessible interface that allows seamless integration with existing RIS/PACS, supports multi-site access, and reduces complexity in IT management, offering flexibility over purely cloud or on-premises setups.

- Leading Platform: Integrated platforms lead with 68.2% share due to unified PACS, RIS, and billing modules, which enhance interoperability, improve efficiency, and provide a single database for patient imaging records.

- Leading End-user: Hospitals dominate as primary end-users, benefiting from RIS integration to manage large patient volumes, streamline imaging workflows, and enable advanced diagnostic and interventional radiology services.

- Increasing integration of artificial intelligence in RIS is improving diagnostic accuracy, automating report generation, optimizing radiologist workflow, and accelerating market growth globally.

- Adoption of standards such as HL7 and FHIR ensures seamless integration with EHRs and PACS, enhancing data consistency, reducing errors, and improving patient care coordination.

- Increasing demand for diagnostic imaging due to aging populations and higher chronic disease prevalence drives RIS adoption to manage large-scale imaging workflows efficiently.

| Key Insights | Details |

|---|---|

|

Global Radiology Information Systems Market Size (2025E) |

US$ 1,337.8 Million |

|

Market Value Forecast (2032F) |

US$ 2,427.7 Million |

|

Projected Growth (CAGR 2025 to 2032) |

8.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.8% |

Market Dynamics

Driver - Technological Advancements, AI Integration, and Interoperable Systems

The global radiology information systems market is driven by the increasing adoption of integrated electronic health records (EHRs) and Picture Archiving and Communication Systems (PACS) in hospitals and imaging centers. RIS allows centralized storage and management of imaging and patient data, streamlines workflows, reduces manual errors, and enhances patient care. Advanced platforms now incorporate artificial intelligence (AI) to automate report generation, assign cases based on radiologist expertise, and detect anomalies, optimizing efficiency and decision-making.

In June 2024, Konica Minolta Healthcare Americas partnered with Apollo Enterprise Imaging Corp to enhance its Exa® Platform, integrating PACS, RIS, and billing solutions via the cloud-based Apollo Repository for Clinical Content (arcc) using Amazon Web Services’ HealthImaging (AHI), enabling longitudinal, image-enabled electronic medical records (EMRs).

In another example, RamSoft and RADPAIR introduced AI-driven radiology report generation via the OmegaAI platform, delivering cloud-native, browser-based reporting solutions for faster and more accurate diagnostics.

Additionally, DeepHealth launched its integrated cloud-native portfolio in Italy, combining AI-powered workspaces for lung, breast, prostate, and brain health. Collectively, these innovations enhance interoperability, workflow automation, and diagnostic precision, making RIS a cornerstone of modern radiology worldwide.

Restraints - High Implementation Costs, Regulatory Compliance, and Integration Challenges

Despite its transformative potential, the global radiology information systems market faces adoption challenges. High installation and infrastructure costs pose barriers, particularly for new entrants and smaller healthcare facilities, often leading them to collaborate with larger providers or outsource imaging services, which may increase patient expenses.

Technical hurdles in integrating RIS with existing systems such as PACS, EHRs, and other imaging software create data silos and workflow inefficiencies. Compliance with regulatory standards—such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States, the Personal Information Protection and Electronic Documents Act (PIPEDA) in Canada, and the General Data Protection Regulation (GDPR) in Europe—requires secure storage, encryption, audit trails, and role-based access controls.

Additionally, user adoption and training challenges, data migration complexities during system transitions, and limited platform flexibility for customized workflows further constrain market growth. Addressing these obstacles is critical for healthcare facilities to maximize operational benefits while ensuring patient-centered care.

Opportunity - AI-Powered Workflows, Cloud-Based Solutions, and Flexible Customization

Opportunities in the global radiology information systems market are centered on interoperability, AI integration, and flexible customization. Advanced RIS platforms adopting standards such as Health Level Seven (HL7) and Fast Healthcare Interoperability Resources (FHIR) enable seamless data exchange with PACS and EHRs, improving workflow efficiency and patient care.

Vendors provide built-in compliance tools for regulatory adherence, including audit trails, encryption, and user access controls, ensuring secure handling of sensitive patient data. Flexible RIS solutions support diverse workflows across mobile imaging centers, multi-location clinics, and specialized diagnostic facilities, allowing modifications to user interfaces, reporting templates, and data fields.

By consolidating imaging and patient data in a single worklist or database, RIS reduces manual tasks, enhances data accuracy, and enables radiology departments to manage higher patient volumes efficiently. The growing demand for AI-assisted diagnostics, cloud-based deployment, and integrated radiology workflows presents substantial growth potential for market players, enabling them to deliver scalable, patient-centered solutions.

Category-wise Analysis

By Component Insights

Software is expected to capture a leading 51.2% share of the global radiology information systems market by 2025. Advanced software solutions integrate PACS, billing, and reporting functionalities, enabling seamless data management, automation of routine tasks, and AI-assisted diagnostic workflows. These tools enhance accuracy, reduce manual errors, and streamline radiology department operations. The growing demand for AI-powered report generation, decision support, and real-time imaging access across multiple devices is further driving software adoption, making it the most preferred component for hospitals and imaging centers seeking efficiency, interoperability, and improved patient outcomes.

By Deployment Insights

Web-based deployment is projected to dominate the global radiology information systems market in 2025, capturing nearly 72.5% share. Its browser-accessible interface allows seamless integration with existing hospital IT systems and multi-site access. Facilities can manage imaging workflows without relying on complex on-premises infrastructure.

While cloud-based RIS offers benefits such as remote access, scalability, and frequent updates, web-based platforms remain preferred due to immediate deployment, cross-platform compatibility, and minimal IT overhead. Hospitals and diagnostic centers benefit from centralized data access, flexible workflow management, and enhanced collaboration, making web-based deployment the leading choice for RIS adoption globally.

By Platform Insights

Integrated platforms are expected to account for a leading 68.2% share of the global radiology information systems market by 2025. These solutions combine Radiology Information Systems (RIS) with Picture Archiving and Communication Systems (PACS), creating a single worklist at patient registration. This integration improves workflow efficiency across radiology, billing, and administrative functions while supporting emergency department operations.

By providing centralized access to imaging data and reports, integrated platforms reduce redundancies, enhance data accuracy, and facilitate real-time collaboration among radiologists and physicians. The combined capabilities make integrated solutions highly attractive for hospitals and multi-specialty imaging centers.

By End-user Insights

Hospitals are projected to lead the global radiology information systems market with a 73.4% share by 2025. High patient volumes, multi-department imaging workflows, and the need for efficient data management drive RIS adoption. Hospitals benefit from centralized scheduling, reporting, and imaging storage, reducing operational inefficiencies and enabling faster, accurate diagnoses.

Integration with PACS, EHRs, and AI-assisted tools further enhances productivity and clinical decision-making. Additionally, regulatory compliance requirements and the demand for standardized reporting encourage hospitals to adopt advanced RIS platforms. Consequently, hospitals remain the primary end-users, setting the pace for RIS deployment worldwide.

Regional Insights

North America Radiology Information Systems Market Trends

By 2025, North America is projected to capture nearly 42.6% of the global radiology information systems (RIS) market, driven by an increasing number of radiologists, rapid adoption of advanced software solutions, and strategic collaborations in healthcare IT.

In March 2024, the US Health Information Technology (IT) Final Rule became effective, implementing the Electronic Health Record (EHR) Reporting Program provision of the 21st Century Cures Act. This rule mandates algorithm transparency, cross-vendor data exchange, and updates certification criteria to enhance interoperability, improve access to electronic health information (EHI), and reduce costs for health IT developers.

In June 2024, Konica Minolta Healthcare Americas partnered with Comp-Ray, Inc., a Christie Innomed company, to expand sales and services of the Exa Platform, integrating Picture Archiving and Communication System (PACS), RIS, and billing modules, offering speed, security, and flexibility across healthcare settings.

In December 2024, Radin Health showcased its AI-powered All-in-One Radiology Workflow Management Solution at RSNA ’24 in Chicago, IL, highlighting seamless interoperability, automated study distribution, and AI-enabled reporting. Building on this momentum, GE HealthCare and DeepHealth, Inc. announced in November 2025 the expansion of their AI collaboration across imaging modalities, further driving RIS adoption. These innovations collectively strengthen North America’s leadership in RIS deployment.

Europe Radiology Information Systems Market Trends

Europe is expected to account for approximately 29.4% of the global RIS market by 2025, fueled by AI integration, regulatory support, and collaborative innovations. In January 2024, Vertex in Healthcare launched the UK-based VRIS platform, streamlining radiology workflows, enhancing report turnaround, and providing actionable intelligence for resource allocation. In February 2024, DeepHealth partnered with Incepto, Europe’s leading platform for AI in medical imaging, expanding access to clinical AI and RIS software across European healthcare providers.

Additionally, the European Congress of Radiology (ECR) 2024 showcased product innovations and refined techniques, emphasizing the digital transformation of imaging services. At ECR 2025 in February, DeepHealth introduced AI-powered radiology informatics solutions, including the Diagnostic Suite™ PACS and SmartMammo™, enhancing interpretive workflows for cancer screening. Simultaneously, Sectra and Siemens Healthineers AG collaborated to enable seamless access to NAEOTOM Alpha class photon-counting CT (PCCT) images within Sectra’s diagnostic application.

Furthermore, regulatory support also played a critical role: Europe’s Health Data Space (EHDS) regulation, adopted January 2025, mandates interoperable EHRs across EU states, ensuring privacy and promoting innovation. These strategic partnerships, technological advancements, and regulatory mandates are driving Europe’s RIS market growth and adoption.

Asia Pacific Radiology Information Systems Market Trends

Asia Pacific is projected to reach at a CAGR of 11.1% over the forecast period, driven by increasing awareness, AI adoption, and expansion of imaging infrastructure. In July 2024, DeepHealth, a subsidiary of RadNet, Inc., opened its Bengaluru office to develop AI-powered solutions for disease detection and diagnostic support, enhancing radiology outcomes in India.

In June 2025, SPARK Radiology launched SPARK.ai, an AI-integrated platform to automate radiology reporting, address workflow inefficiencies, and alleviate the severe radiologist shortage, where one radiologist interprets 100 scans daily.

In October 2025, Superhealth and United Imaging Healthcare signed a strategic INR 2,500 crore agreement to equip 100 hospitals with AI-ready MRI, CT, mammography, and digital X-ray systems, establishing service hubs and creating over 1,000 skilled jobs.

Furthermore, in November 2025, Konica Minolta Healthcare Americas presented Dynamic Digital Radiography (DDR) at RSNA 2025, highlighting low-dose, motion-based imaging innovations. Together, these initiatives underscore rapid technological adoption and infrastructure expansion, positioning the Asia Pacific as a high-growth RIS market.

Competitive Landscape

The global radiology information systems market is highly competitive, driven by continuous innovation in AI-powered diagnostics, cloud-based platforms, and integrated RIS-PACS solutions. Market players focus on strategic partnerships, technological collaborations, and expanding geographic presence to enhance workflow efficiency, ensure regulatory compliance, and address growing demand for centralized, scalable imaging data management across hospitals and diagnostic centers.

Key Industry Developments:

- In July 2025, RadNet, Inc., a leading diagnostic imaging and digital health provider, acquired iCAD, Inc., a global AI-powered breast health solutions company, integrating its technology and regulatory expertise into DeepHealth to enhance AI-driven imaging workflows and clinical screening efficiency.

- In October 2025, QT Imaging Holdings partnered with Intelerad Medical Systems to deploy InteleShare Research PACS and Cloud PACS, integrating QT Imaging’s radiation-free Breast Acoustic CT Scanners with a secure cloud platform for efficient, compliant data storage and sharing.

Companies Covered in Radiology Information Systems Market

- Cerner Corporation

- Oracle

- GE HealthCare

- Esaote SPA

- Seimens Healthineers AG

- Koninklijke Philips N.V.

- DeepHealth

- deepc GmbH

- eRAD

- Advanced Data Systems

- PaxeraHealth

- Optomed

- Reapmind Innovations Pvt Ltd

- ScienceSoft USA Corporation

- IMAGE Information Systems Europe GmbH

- Fujifilm

- Suvarna Technosoft

- Intelerad

- RamSoft

- Healthray

- Epic Systems Corporation

Frequently Asked Questions

The global radiology information systems market is projected to be valued at US$ 1,337.8 Million in 2025.

Rising adoption of AI-enabled workflows, increasing imaging volumes, and demand for seamless integration with EHR and PACS systems drive global RIS market growth.

The global radiology information systems market is poised to witness a CAGR of 8.9% between 2025 and 2032.

Expansion in emerging markets, cloud-based deployments, and AI-powered workflow optimization present significant growth opportunities for RIS solutions globally.

Major players in the global are Cerner Corporation, Oracle, GE HealthCare, Esaote SPA, Seimens Healthineers AG, Koninklijke Philips N.V., and others.