- Media & Entertainment

- Internet Radio Market

Internet Radio Market Size, Share, and Growth Forecast, 2026 - 2033

Internet Radio Market by Component (Software, Hardware, Services), Content Type (Music Streaming, Podcasts, Sports, Talk Shows), End-user (Residential, Commercial), and Regional Analysis for 2026 - 2033

Internet Radio Market Share and Trends Analysis

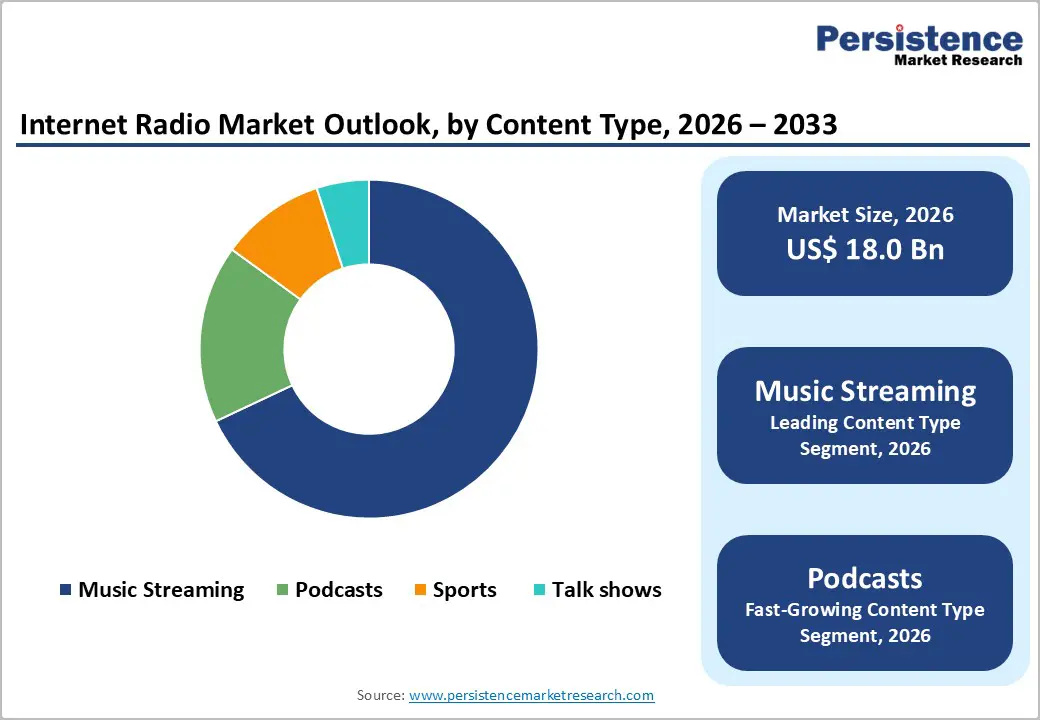

The global internet radio market size is likely to be valued at US$ 18.0 billion in 2026, and is projected to reach US$ 39.0 billion by 2033, growing at a CAGR of 12.5% during the forecast period 2026 - 2033.

The market's robust expansion stems from accelerating smartphone penetration, advancing 5G infrastructure deployment, and evolving consumer preferences toward personalized audio content. The convergence of artificial intelligence-powered recommendation engines with streaming technologies has fundamentally transformed listener engagement, while integration with connected vehicles and smart home devices expands consumption touch points beyond traditional platforms.

Key Industry Highlights

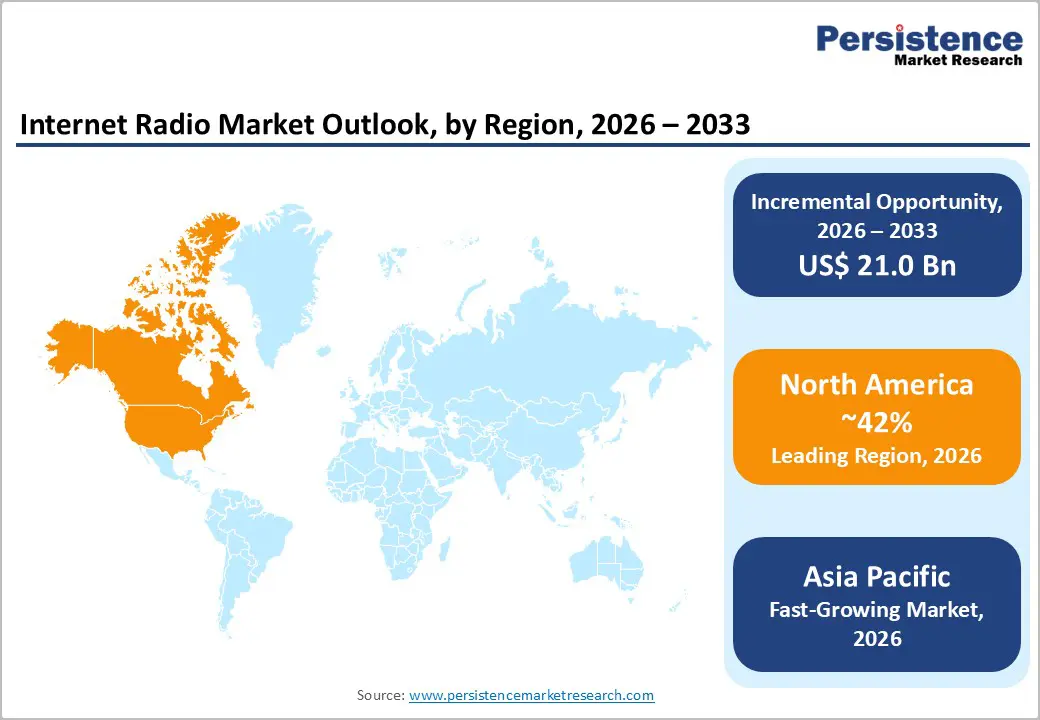

- Dominant Region: North America is poised to capture about 42% market share in 2026, owing to a high-functioning broadband infrastructure and deep smartphone penetration.

- Fastest-growing Market: Asia Pacific is set to be the fastest growing through 2033 as a result of favorable demographics, rapid digitalization, and smartphone-first consumption patterns.

- Leading & Fastest-growing Component: Software is likely to lead with an estimated 62% revenue share in 2026, whereas services are slated to be the fastest-growing during the 2026 - 2033 forecast period.

- Leading & Fastest-growing Application: Music streaming is anticipated to dominate at 68% in 2026, while podcast is expected to post the highest CAGR between 2026 and 2033.

- Major Driver: Technological innovation in personalization and AI-driven content curation is reshaping how listeners discover and engage with internet radio.

- Prominent Opportunities: Asia Pacific, Latin America, and Africa present substantial untapped growth opportunities for internet radio, supported by expanding middle classes and improving digital infrastructure.

- October 2025: ATC Labs unveiled its next-generation Aideal Audio™ platform, featuring real-time AI upgrades for Perceptual SoundMax™ audio processors and Web Radio with automated profile suggestions and genre-sensitive music processing.

| Key Insights | Details |

|---|---|

| Internet Radio Market Size (2026E) | US$ 18.0 Bn |

| Market Value Forecast (2033F) | US$ 39.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 28.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancement in Personalization and AI-Driven Content Curation

Technological innovation in personalization and AI-driven content curation is reshaping how listeners discover and engage with internet radio. Advanced artificial intelligence and machine learning systems now interpret behaviors such as listening patterns, skip tendencies, and genre preferences to deliver highly tailored recommendations and dynamic stations. Major platforms have introduced personalized radio features across multiple markets, showing that refined curation can significantly increase daily engagement and listening time. For example, in June 2025, LG launched Radio Optimism, a 24/7 AI-powered digital radio station, where users input names, stories, genres (such as punk or EDM), and vibes to generate personalized songs with album art for loved ones. These innovations have elevated music experience to a level that feels closely aligned with individual tastes, narrowing the gap between passive radio listening and fully on-demand streaming.

-The growing adoption of voice-activated smart speakers has removed many of the traditional barriers to accessing internet radio. Listeners can launch stations, switch genres, or discover new content through simple voice commands, integrating streaming audio into daily routines at home and in workplaces. This frictionless access, combined with increasingly relevant recommendations, strengthens user retention and deepens loyalty to specific platforms. As satisfaction rises, positive user experiences often lead to stronger word-of-mouth, helping platforms attract new listeners more efficiently and gradually reduce customer acquisition costs.

Copyright Licensing Complexities and Escalating Royalty Costs

The internet radio industry faces persistent challenges arising from complex copyright licensing frameworks and rising royalty obligations. Recent increases in digital streaming royalty rates have put direct pressure on platform profitability, forcing operators to reconsider pricing, monetization strategies, and catalog breadth. Navigating multiple rights holders and collective management organizations across different jurisdictions adds substantial administrative workload and legal exposure, especially for services that depend on large, global music libraries. Securing licenses for music and other audio content often involves lengthy negotiations, detailed reporting requirements, and ongoing audits, turning licensing into a core operational hurdle rather than a routine back-office task.

-These costs and complexities disproportionately affect smaller platforms and new market entrants that lack the scale and bargaining power of established players. Higher upfront and recurring licensing expenses can deter innovation, limit experimentation with niche formats, and discourage expansion into new markets. Larger, well-capitalized incumbents can more easily absorb royalty increases and manage cross-border licensing portfolios, leading to a gradual consolidation of market power in their favor. Challenges intensify when platforms expand internationally, as they must secure separate licenses in each territory while dealing with differing regulations, contract structures, and currency risks, all of which add further uncertainty to long-term planning and investment decisions.

Emerging Market Penetration and Localized Content Development

Asia Pacific, Latin America, and Africa present substantial untapped growth opportunities for internet radio, supported by expanding middle classes and improving digital infrastructure. In these regions, markets such as China and India are driving adoption through localized platforms that prioritize regional languages, popular local genres, and culturally familiar formats. Broadcasters and media companies are increasingly digitizing their content libraries, enabling new partnerships for streaming rights, simulcasting, and co-branded channels that extend the reach of traditional radio into digital environments. As connectivity improves and smartphones become more affordable, listener bases grow quickly, laying a foundation for long-term audience monetization.

-Rising disposable incomes in these markets support growth in both advertising revenue and paid subscriptions, as brands seek targeted audio inventory and consumers become more willing to pay for enhanced experiences such as ad-free listening or exclusive content. Platforms that invest early in local language catalogs, regional music ecosystems, and culturally relevant programming can build strong brand affinity and user loyalty before global competitors fully scale their offerings. Aligning product design, pricing models, and partnerships with local preferences and regulatory environments further strengthens strategic positioning and helps secure durable leadership in these high-growth markets. For example, in November 2025, Spotify launched three new Premium plans in India that feature a combination of ad-free offline music, lossless audio, AI DJ, AI playlists, and DJ software integration for up to 3 accounts.

Category-wise Analysis

Component Insights

Software is poised to be the leading component in 2026 with an estimated 62% of the internet radio market revenue share. The leadership reflects by technology-intensive nature of streaming services and the centrality of software architecture to performance and monetization. Platforms depend on advanced content delivery networks, recommendation algorithms, user interfaces, backend management, and analytics to deliver seamless, personalized experiences across mobile, desktop, and connected devices. Investments also span advertising technology, including programmatic ad insertion, dynamic creative optimization, and attribution, often delivered via cloud and software-as-a-service models that lower entry barriers and intensify competition while driving continuous feature innovation for end-users.

Services are likely to be the fastest-growing during the 2026-2033 forecast period. The expansion of internet radio services is driving growing demand for specialized professional and managed services that can address rising operational complexity across international markets. Platforms increasingly rely on experts in copyright management, regulatory compliance, localization, and performance optimization to support multi-country operations and diverse content portfolios. In July 2025, for example, BBC Sounds restricted access for listeners outside the U.K., but BBC radio stations remained available live via third-party platforms such as TuneIn and Sonos. High-margin opportunities are emerging around technical integration and white-label deployments for broadcasters, automotive manufacturers, and hospitality providers, while consulting services help traditional broadcasters navigate digital transformation, hybrid distribution, and monetization strategies. Ongoing maintenance and support contracts then create recurring revenue streams with attractive economics for service providers.

Content Type Insights

Music streaming is slated to be the dominant content form holding an estimated 68% of the internet radio market revenue in 2026, aided by the broad cross-demographic appeal of music and its suitability for extended passive listening during commuting, work, exercise, and at home. Major platforms now provide vast, genre-spanning catalogs and compete increasingly on the quality of curation, where human-programmed playlists and AI-driven recommendations lift engagement, retention, and monetization. The segment benefits from relatively mature royalty and licensing frameworks with labels and publishers, growing adoption of premium ad-free tiers with enhanced audio features, and social tools such as playlist sharing and collaborative listening that reinforce network effects and lower acquisition costs.

Podcasts are expected to be the fastest-growing segment during the 2026 - 2033 forecast period. The rapid expansion is supported by strong growth in professionally produced content, greater participation from celebrities and influencers, and improved in-platform discovery features that make shows easier to find and follow. The ecosystem has shifted toward higher production values, serialized storytelling formats, and exclusive licensing arrangements that attract mainstream audiences and deepen engagement beyond early adopters. Internet radio platforms now invest heavily in acquisitions, creator partnerships, and exclusive distribution, recognizing podcasts’ superior engagement, strong advertising performance, and ability to support granular audience segmentation across themes such as true crime, business, comedy, health, and education, all reinforced by relatively low production costs that sustain long-tail catalog expansion.

End-user Insights

Residential is expected to occupy the top position with an approximate 74% of the revenue share in 2026. Residential end-users comprise individuals who access internet radio services via smartphones, tablets, computers, smart speakers, and connected TVs within the home. This segment has expanded as internet radio becomes embedded in daily routines, supporting use cases such as morning listening, cooking, relaxation, social gatherings, sleep soundscapes, and work-from-home productivity. Demographically, usage spans all age groups, with younger listeners showing particularly strong engagement with podcasts and social discovery features. Residential growth remains robust, supported by rising smart-home device adoption, richer personalization, and expanding original content libraries tailored to diverse household preferences.

Commercial is anticipated to be the fastest-growing segment during the 2026 - 2033 forecast period. The commercial end-user segment covers business streaming services for retail, hospitality, restaurants, fitness centers, healthcare facilities, corporate offices, and automotive manufacturers that integrate audio into connected vehicles. For example, a 2025 industry study showed that AM/FM radio dominates in-car audio with 56% of total listening time across brands and 85% of ad-supported audio. These applications address specific needs such as enhancing ambient environments, reinforcing brand identity through curated programming, improving customer experience, and supporting employee productivity. Unlike residential plans, commercial licensing models are structured around factors such as venue size, concurrent streams, and commercial usage rights, with added value from analytics that inform dwell times, customer behavior, and multi-location management, while integrations with point-of-sale and CRM systems position streaming as a broader business enablement tool.

Regional Insights

North America Internet Radio Market Trends

At around 42%, North America is set to command a significant portion of the internet radio market share in 2026, with the United States generating most regional revenue due to mature broadband infrastructure, high smartphone penetration, and deeply embedded digital entertainment habits. Canada contributes additional growth through bilingual content offerings and supportive digital media policies under its broadcasting and telecommunications regulatory frameworks. Core growth drivers include technological leadership in streaming infrastructure, where regional platforms lead in audio quality enhancement, AI-based personalization, and voice-activated discovery interfaces that now anchor usage across smartphones, smart speakers, and connected vehicles.

Furthering aiding the regional market is the fact that the U.S. is home to one of the most advanced programmatic advertising ecosystems globally, which supports strong monetization of digital audio inventory and sustained investment in original content and user experience innovation. Competitive dynamics in North America feature large technology companies that leverage integrated devices, operating systems, and broader ecosystems, alongside specialized pure-play audio providers that compete on content depth, curation quality, and superior interface design. Investment priorities increasingly focus on advanced audio technologies, AI-driven discovery and recommendation, and tighter integration with connected vehicle platforms and smart-home ecosystems, which collectively expand listening occasions and reinforce North America’s role as the leading, innovation-driven region for internet radio.

Europe Internet Radio Market Trends

Europe is a major market for internet radio services, with growth reinforced by strong digital infrastructure, multilingual audiences, and dense urban populations that favor mobile and broadband-based listening. Markets such as Germany, the United Kingdom, France, and Spain act as core demand centers, combining high connectivity with sophisticated media ecosystems and well-developed public and commercial broadcasting traditions. Key structural drivers include regulatory harmonization under European Union Digital Single Market policies, which simplifies cross-border content licensing, and the impact of GDPR, which, despite adding compliance obligations, has reinforced consumer trust in data-driven personalization for platforms that adopt privacy-by-design approaches.

Germany’s leadership is closely linked to deep integration of streaming into connected car ecosystems, with premium original equipment manufacturers (OEMs) embedding audio platforms as standard features and helping to normalize in-vehicle IP listening. The United Kingdom stands out for strong podcast and digital audio adoption, supported by the BBC’s extensive digital offerings and an active independent creator community that continually refreshes the content pipeline. The broader regulatory environment emphasizes cultural diversity through European and local content quotas and clearer digital licensing rules, encouraging investment in original, language-specific programming and lossless audio infrastructure, even as higher rights costs and privacy-compliant advertising technology requirements increase operational complexity for both global and domestic platforms.

Asia Pacific Internet Radio Market Trends

The Asia Pacific market is anticipated to emerge as the fastest-growing over the 2026-2033 period. The growth is supported by favorable demographics, rapid digitalization, and smartphone-first consumption patterns that often leapfrog traditional desktop usage. Regional growth is fueled by declining mobile data prices, widespread 4G and 5G deployment, and a young, highly connected population that spends more time on digital entertainment. Manufacturing cost advantages enable affordable device production, making internet-capable smartphones and connected hardware accessible to lower-income users. Government-led digital infrastructure programs, combined with expanding app ecosystems, provide a strong foundation for streaming service scalability across both major metropolitan areas and fast-growing secondary cities.

-China is characterized by powerful domestic platforms embedded in super-app ecosystems, Japan exhibits more mature, quality-focused subscription behavior, and India stands out for hyper-growth driven by vernacular content and mobile-first access. Regulatory environments vary widely from tightly controlled markets to relatively open, innovation-oriented regimes shaping partnership structures, licensing models, and the extent of foreign participation. Across the region, strategic priorities emphasize vernacular content production, integration with local payment methods such as mobile wallets and carrier billing, and close collaboration with telecom operators for bundling and device distribution, enabling a gradual shift from ad-supported to premium tiers as middle-class incomes rise.-

Competitive Landscape

The global internet radio market strucutre has remained moderately consolidated, with major platforms such as Spotify Technology S.A., Apple Inc., Amazon.com, Inc., and YouTube Music together capturing around 58% of total market share. These companies have continued to strengthen their dominance by combining brand loyalty, diversified catalogs, and seamless integration across devices. The competitive landscape has expanded to include established media networks, digital-first platforms, and niche content providers, all vying to appeal to specific listener segments through unique audio formats, curated playlists, and interactive experiences. As traditional broadcasting and on-demand streaming continue to converge, players that can personalize content delivery while maintaining reliability and global reach will have positioned themselves most effectively for growth.

Leading participants have consistently invested in product innovation and technology enhancement to enhance engagement and customer retention. AI and machine learning (ML)-driven recommendation systems, spatial audio, and adaptive bitrate streaming have already transformed how audiences consume audio content. Many companies are now applying these technologies to create contextual listening experiences tailored to user behavior, time of day, and mood. Over the next few years, firms that integrate creativity with data intelligence will have achieved a sustainable competitive edge, deepening relationships with advertisers and listeners alike while transitioning the market toward more immersive, socially connected, and revenue-diversified audio ecosystems.

Key Industry Developments

- In September 2025, YouTube began testing AI “hosts” in the YouTube Music app through its new YouTube Labs program, where virtual DJs add stories, trivia, and commentary between songs on radio and mixes to deepen listening and discovery.

- In August 2025, Apple Music partnered with TuneIn to make its six 24/7 live radio stations, including Apple Music 1, Apple Music Hits and Apple Music Country, available beyond Apple’s own ecosystem to TuneIn’s 75 million monthly users via smart speakers, headphones and connected cars.

- In June 2025, Tencent Music Entertainment has agreed to acquire leading Chinese audio platform Ximalaya in a cash-and-stock deal worth about US$ 2.4 billion, aiming to strengthen its position in China’s fast-growing online audio market.

Companies Covered in Internet Radio Market

- Spotify Technology S.A.

- Apple Inc.

- Amazon.com, Inc.

- Alphabet Inc./YouTube Music

- Tencent Music Entertainment

- SiriusXM Holdings Inc.

- iHeartMedia, Inc.

- Deezer S.A.

- Pandora Media, LLC

- Gaana

- JioSaavn

- NetEase Cloud Music

- Anghami

- Audiomack

- TuneIn, Inc.

Frequently Asked Questions

The global internet radio market is projected to reach US$ 18.0 billion in 2026.

Rising smartphone and internet penetration, growing demand for personalized on‑demand audio, and increased use of smart speakers and connected vehicles for streaming are driving the market.

The market is poised to witness a CAGR of 12.5% from 2026 to 2033.

Fusing western music styles with localized content, smart‑device and connected‑car integration, and advanced adtech for highly targeted, data‑driven audio advertising are opening lucrative opportunities.

Spotify Technology S.A., Apple Inc., Amazon.com, Inc., and YouTube Music are some of the key players in the market.