- Semiconductor Materials & Components

- Radio Frequency Components Market

Radio Frequency Components Market Size, Share, and Growth Forecast, 2025 - 2032

Radio Frequency Components Market by Component Type (Power Amplifiers, RF Filters, Antenna Switches, Low-Noise Amplifiers, RF Tunable Devices), Semiconductor Material (Gallium Arsenide, Silicon, Gallium Nitride, Silicon-Germanium), End-use, and Regional Analysis for 2025 - 2032

Radio Frequency Components Market Size and Trends Analysis

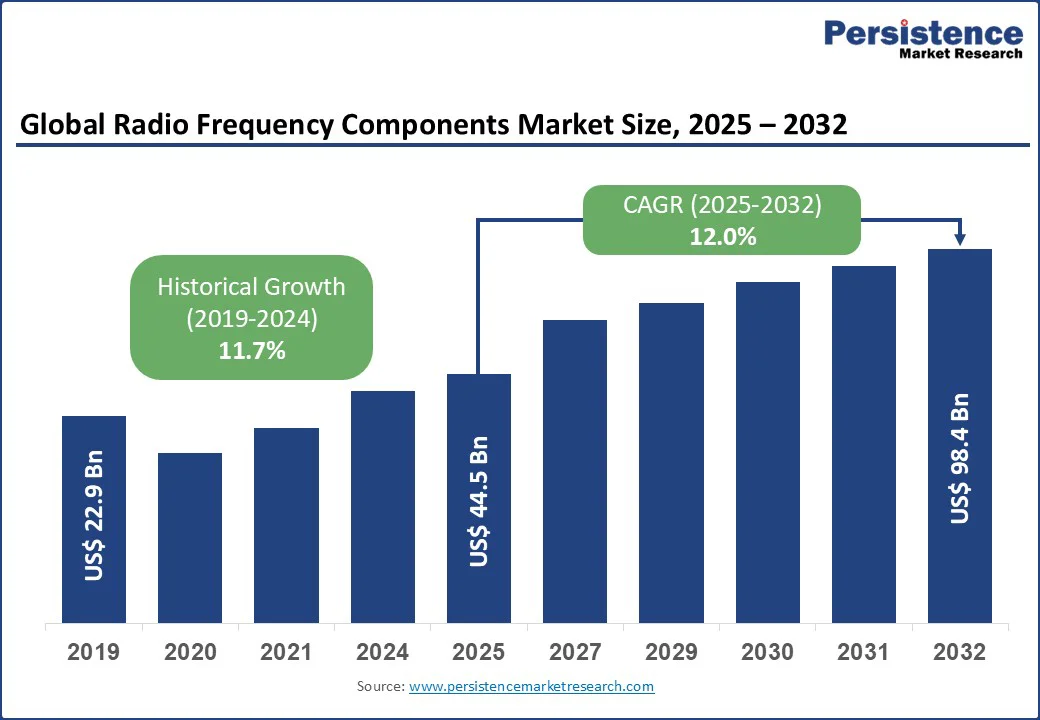

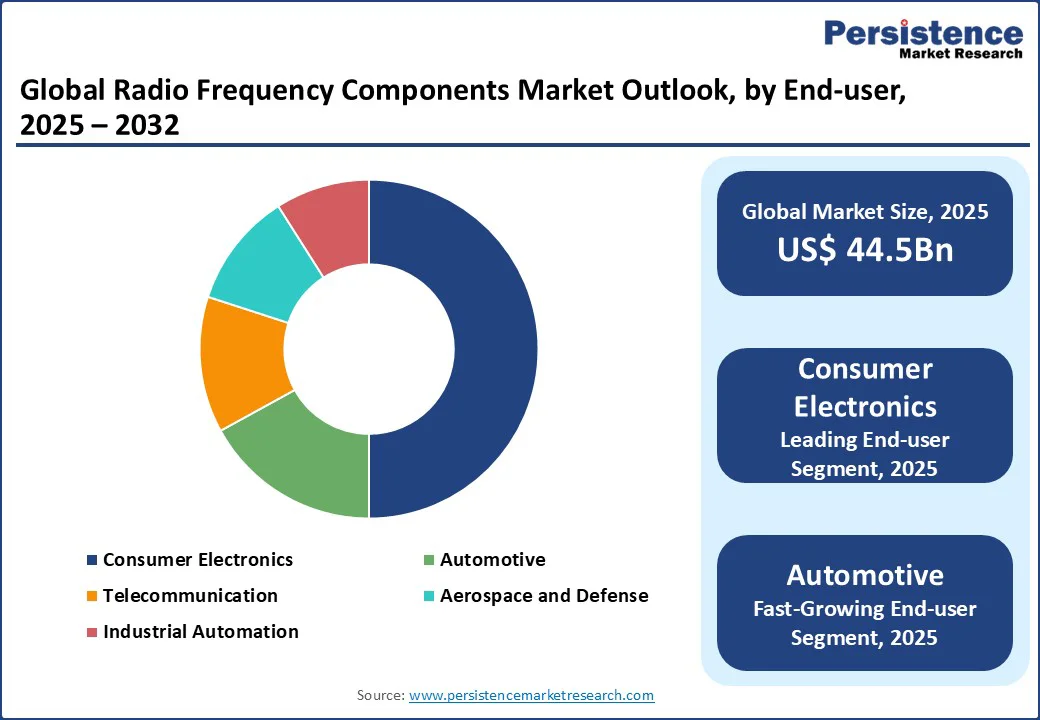

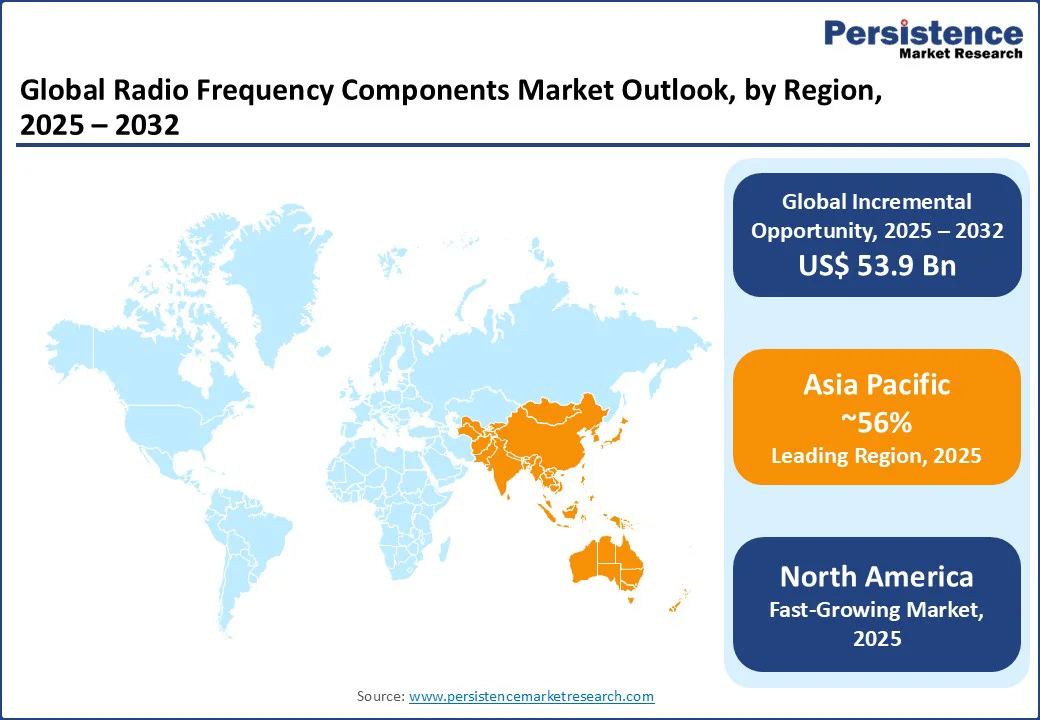

The global radio frequency (RF) components market size is likely to be valued at US$ 44.5Bn in 2025 and is expected to reach US$ 98.4 Bn by 2032, growing at a CAGR of 12.0% during the forecast period from 2025 to 2032.

Key Industry Highlights:

- Leading Region: Asia Pacific holds a 56% share of the RF components market, with countries such as China and Japan leading in production and consumption.

- Fastest-growing Region: North America, driven by advancements in 5G infrastructure and automotive electronics in the United States.

- Dominant Component Type: RF Filters, commanding nearly 36% market share, due to their critical role in 5G and IoT applications.

- Leading End-Use: Consumer Electronics, accounting for over 50% of market revenue, driven by demand for smartphones, wearables, and smart home devices.

|

Key Insights |

Details |

|

RF Components Market Size (2025E) |

US$ 44.5 Bn |

|

Market Value Forecast (2032F) |

US$ 98.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

11.7% |

The radio frequency components market is experiencing significant growth, driven by the increasing adoption of 5G technology, rising demand for advanced consumer electronics, and expanding applications in automotive and aerospace sectors.

Market Dynamics

Driver - Rising Adoption of 5G Technology and IoT Ecosystems

The rising adoption of 5G technology and the rapid expansion of IoT ecosystems are among the primary drivers fueling growth in the RF components market. 5G networks require advanced RF front-end modules, filters, and power amplifiers to support higher frequency bands, including sub-6 GHz and millimeter-wave spectrums. These components are critical to ensure signal integrity, low latency, and seamless connectivity across diverse applications such as smartphones, base stations, and fixed wireless access. The demand for compact and energy-efficient RF solutions is further amplified as device manufacturers aim to deliver high-speed data services without compromising battery performance. For instance, Qualcomm and Qorvo have introduced next-generation RF front-end solutions designed to meet the performance requirements of 5G-enabled smartphones and IoT devices.

The proliferation of IoT devices across industries, including healthcare, smart homes, industrial automation, and automotive, has created a surge in demand for reliable RF components capable of handling dense network environments. Low-power, wide-area RF technologies are essential for connecting billions of devices efficiently. For example, Murata and Analog Devices have developed advanced RF modules that enable connectivity in wearables, autonomous vehicles, and industrial IoT applications. With governments and telecom operators accelerating 5G rollouts globally, and industries embracing IoT for digital transformation, the synergy between these two trends is significantly expanding the addressable market for RF components, making them indispensable to next-generation connectivity solutions.

Restraint - High Development Costs and Complexity of RF Component Design

The RF components market faces challenges due to the high development costs and complexity associated with designing and manufacturing advanced RF components. Developing RF components for 5G and IoT applications requires significant investment in research and development (R&D), specialized equipment, and skilled expertise. For instance, designing RF filters for millimeter-wave frequencies used in 5G networks involves intricate processes to ensure signal integrity and minimize interference, leading to elevated production costs. The complexity of integrating multiple RF components into compact devices, such as smartphones and automotive radar systems, further increases development expenses.

Additionally, the need for compliance with stringent regulatory standards, such as those set by the Federal Communications Commission (FCC) and the European Telecommunications Standards Institute (ETSI), adds to the cost and time required for market entry. Smaller manufacturers and new entrants face significant barriers due to these high costs, limiting their ability to compete with established players such as Qualcomm and Broadcom. Supply chain disruptions, such as shortages of semiconductor materials such as Gallium Nitride and Silicon, also exacerbate production challenges, impacting the scalability and affordability of RF components. These factors collectively restrain market growth, particularly for price-sensitive applications in emerging markets.

Opportunity - Advancements in Semiconductor Materials and Manufacturing Processes

The RF components market presents significant growth opportunities driven by advancements in semiconductor materials and manufacturing processes. Emerging materials such as Gallium Nitride and Silicon-Germanium offer superior performance in terms of power efficiency, thermal stability, and high-frequency capabilities compared to traditional Silicon-based components. For instance, GaN-based power amplifiers, used in 5G base stations and automotive radar systems, provide higher efficiency and power output, enabling compact and energy-efficient designs. Companies such as Qorvo and Analog Devices are investing heavily in GaN technology to meet the demands of 5G and aerospace applications.

Innovations in manufacturing processes, such as advanced packaging techniques and 3D integration, are also enhancing the performance and scalability of RF components. For instance, Murata Manufacturing has developed multilayer ceramic technologies for RF filters, improving signal quality and reducing production costs. These advancements enable manufacturers to produce smaller, more efficient RF components that meet the requirements of modern applications such as autonomous vehicles and smart wearables.

The growing adoption of these technologies, coupled with increasing investments in semiconductor fabrication facilities (fabs), is expected to drive market growth by improving production efficiency and enabling the development of next-generation RF solutions. Companies leveraging these advancements can capitalize on the rising demand for high-performance RF components in 5G, IoT, and automotive sectors.

Category-wise Analysis

Component Type Insights

RF filters dominate the RF components market, expected to account for approximately 36% share in 2025. Their dominance is driven by their critical role in managing signal interference and ensuring high-quality connectivity in 5G networks, IoT devices, and consumer electronics. RF filters are essential for frequency selection in smartphones, base stations, and automotive radar systems, supporting the increasing demand for reliable wireless communication.

Power amplifiers are the fastest-growing segment, propelled by the rising adoption of 5G technology and automotive electronics. Power amplifiers enhance signal strength in high-frequency applications, such as 5G base stations and vehicle-to-everything (V2X) communication systems. The Asia Pacific region, particularly China and Japan, is a key contributor to this growth due to significant investments in 5G infrastructure and smart vehicle technologies.

Semiconductor Material Insights

Gallium arsenide (GaAs) holds the largest market share, approximately 38% in 2025, due to its high electron mobility and efficiency in RF applications. GaAs is widely used in power amplifiers and antenna switches for smartphones, satellite communications, and defense systems, offering superior performance in high-frequency environments.

Gallium nitride (GaN) is the fastest-growing segment, driven by its ability to handle high power and operate efficiently at millimeter-wave frequencies required for 5G and aerospace applications. GaN’s thermal stability and energy efficiency make it ideal for next-generation RF components, with North America and the Asia Pacific leading adoption due to their advanced telecommunications and defense sectors.

End-Use Insights

Consumer electronics lead the RF components market, holding a 50% share in 2025. The segment’s dominance is driven by the proliferation of smartphones, wearables, and smart home devices, which rely heavily on RF components for wireless connectivity. The rise of 5G-enabled devices and IoT ecosystems further fuels demand in this segment.

Automotive is the fastest-growing segment, fueled by the increasing integration of RF components in advanced driver-assistance systems (ADAS), vehicle-to-everything (V2X) communication, and autonomous vehicles. The Asia Pacific region, particularly China and Japan, is a significant driver due to its leadership in electric vehicle (EV) production and smart mobility solutions.

Regional Insights

North America RF Components Market Trends

In North America, the RF components market is experiencing rapid growth, with the United States emerging as a key contributor. The increasing deployment of 5G networks and the rising demand for advanced automotive electronics are driving market expansion. The U.S. is home to major players such as Qualcomm, Broadcom, and Qorvo, which are investing heavily in 5G infrastructure and IoT solutions. The growing adoption of RF components in consumer electronics, such as smartphones and smart wearables, is supported by strong consumer demand and high purchasing power.

The automotive sector in the U.S. is also a significant driver, with RF components being integrated into ADAS and V2X systems for autonomous and connected vehicles. The expansion of e-commerce platforms has made RF-enabled devices more accessible, further boosting market growth. Government initiatives to support 5G rollout and smart city projects are enhancing the adoption of RF components. While North America is not the largest producer, its focus on innovation, premium products, and strategic partnerships ensures steady growth in the RF components market over the forecast period.

Europe RF Components Market Trends

Europe holds a significant share of the RF components market, driven by countries such as Germany, the United Kingdom, and France. Germany leads in automotive applications, with companies such as Infineon Technologies developing RF components for ADAS and electric vehicles. The region’s strong industrial base and focus on Industry 4.0 initiatives are driving demand for RF components in industrial automation and IoT applications.

The United Kingdom and France are key contributors to the telecommunications sector, with significant investments in 5G infrastructure. Europe’s well-established supply chains and advanced semiconductor manufacturing facilities, particularly in Germany, give it a competitive edge. The region’s emphasis on sustainable technologies and regulatory support for energy-efficient RF components further strengthens its market position. Europe’s expertise in high-quality RF component production and its focus on innovation ensure its continued prominence in the global market.

Asia Pacific RF Components Market Trends

Asia Pacific is expected to account for approximately 56% share. It is the largest market semiconductor components, led by China, Japan, and South Korea. China’s dominance is driven by its leadership in 5G network deployment and consumer electronics production. The country is home to major manufacturers such as Huawei and ZTE, which rely on RF components for 5G base stations and smartphones. Japan and South Korea are key players in automotive and consumer electronics, with companies such as Murata Manufacturing and Mitsubishi Electric driving innovation in RF filters and power amplifiers.

The rise of e-commerce platforms and increasing disposable incomes in the region are accelerating the adoption of RF-enabled devices, such as smartphones and IoT gadgets. Favorable government policies supporting 5G rollout and smart city initiatives are further boosting market growth. The availability of cost-effective semiconductor materials and advanced manufacturing capabilities in the Asia Pacific ensures its leadership in the RF components market, with significant expansion opportunities.

Competitive Landscape

The global RF Components Market is highly competitive, characterized by a blend of established multinational leaders and fast-growing regional players. In North America and Europe, companies such as Qualcomm, Broadcom, Skyworks Solutions, Qorvo, Analog Devices, Texas Instruments, Murata Manufacturing, NXP Semiconductors, STMicroelectronics, Infineon Technologies, and Renesas Electronics hold strong positions through extensive R&D, large-scale production capabilities, and strategic collaborations with leading telecom operators and automotive manufacturers. In Asia-Pacific, rapid industrialization, expanding consumer electronics markets, and the rollout of 5G infrastructure attract investments from both international players and regional specialists, including Mitsubishi Electric, Fujitsu, ROHM, and TDK Corporation. Competition is driven by innovation in compact, energy-efficient RF front-end solutions, advanced RF filters, and next-generation devices tailored for 5G and IoT. Sustainability has also become a key differentiator, with companies adopting eco-friendly materials and energy-efficient processes. While global leaders consolidate their dominance, regional and niche firms serve specialized applications, ensuring a dynamic, fragmented, and innovation-driven market landscape.

Key Developments

- In July 2025, Murata Manufacturing began mass production and commercial shipment of the world’s first high-frequency filter leveraging XBAR technology, supporting 5G, Wi-Fi 6E, Wi-Fi 7, and future 6G networks. This filter provides low insertion loss, high attenuation, and wide bandwidth for compact, high-performance wireless devices.

- In August 2025, Qualcomm has not publicly documented an announcement regarding next-generation RF front-end solutions emphasizing energy efficiency and compact design for 5G and IoT has not been found. A relevant development is the inclusion of an optimized RF Front-End in the Snapdragon W5 Gen 2 wearable platform, which reduced the module size by approximately 20% and lowered power consumption.

Companies Covered in Radio Frequency Components Market

- Qualcomm

- Broadcom

- Skyworks Solutions

- Qorvo

- Analog Devices

- Texas Instruments

- Murata Manufacturing

- NXP Semiconductors

- STMicroelectronics

- Infineon Technologies

- Renesas Electronics

- MACOM Technology Solutions

- Mitsubishi Electric

- Fujitsu

- ROHM

- TDK Corporation

- Others

Frequently Asked Questions

The global radio frequency components market is projected to reach US$ 44.5 billion in 2025.

The rising adoption of 5G technology and IoT ecosystems is a key driver.

The radio frequency components market is expected to witness a CAGR of 12.0% from 2025 to 2032.

Advancements in semiconductor materials, such as Gallium Nitride, and manufacturing processes are a key opportunity.

Qualcomm, Broadcom, Skyworks Solutions, Qorvo, and Analog Devices are among the key players.