- Non-food Packaging

- Plastic Rigid IBC Market

Plastic Rigid IBC Market Size, Share, and Growth Forecast, 2026 - 2033

Plastic Rigid IBC Market by Material Type (High Density Polyethylene (HDPE), Low Density Polyethylene (LDPE), Others), Capacity (Up to 500 Liters, 500 to 1000 Liters, Others), End-user (Industrial Chemicals, Others), and Regional Analysis for 2026 – 2033

Plastic Rigid IBC Market Size and Trends Analysis

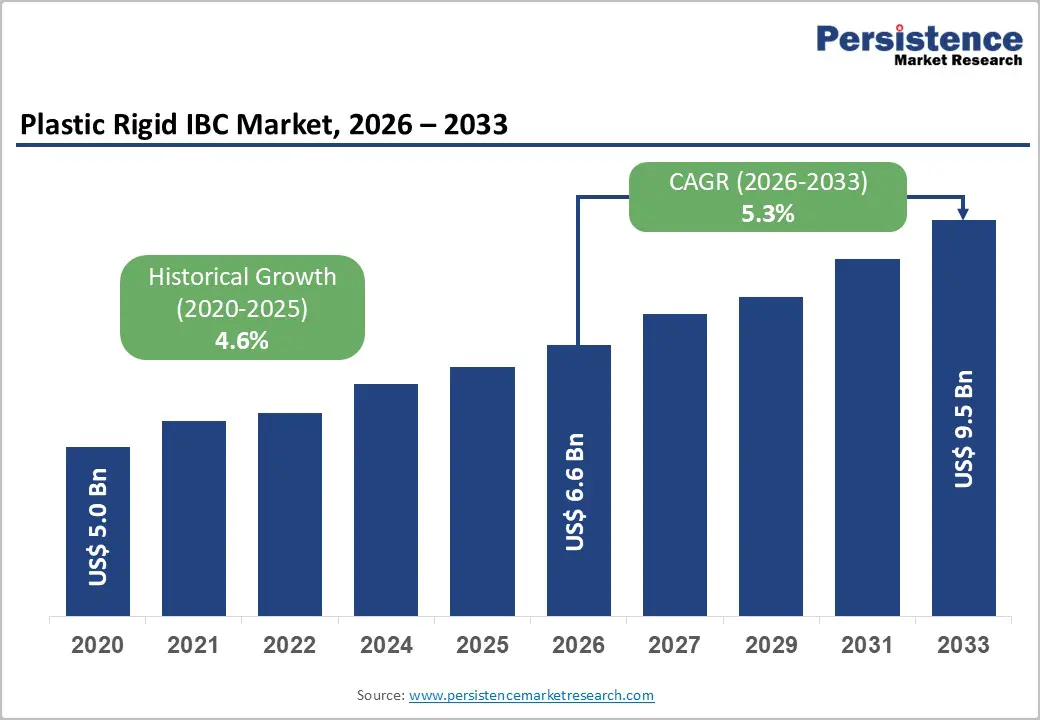

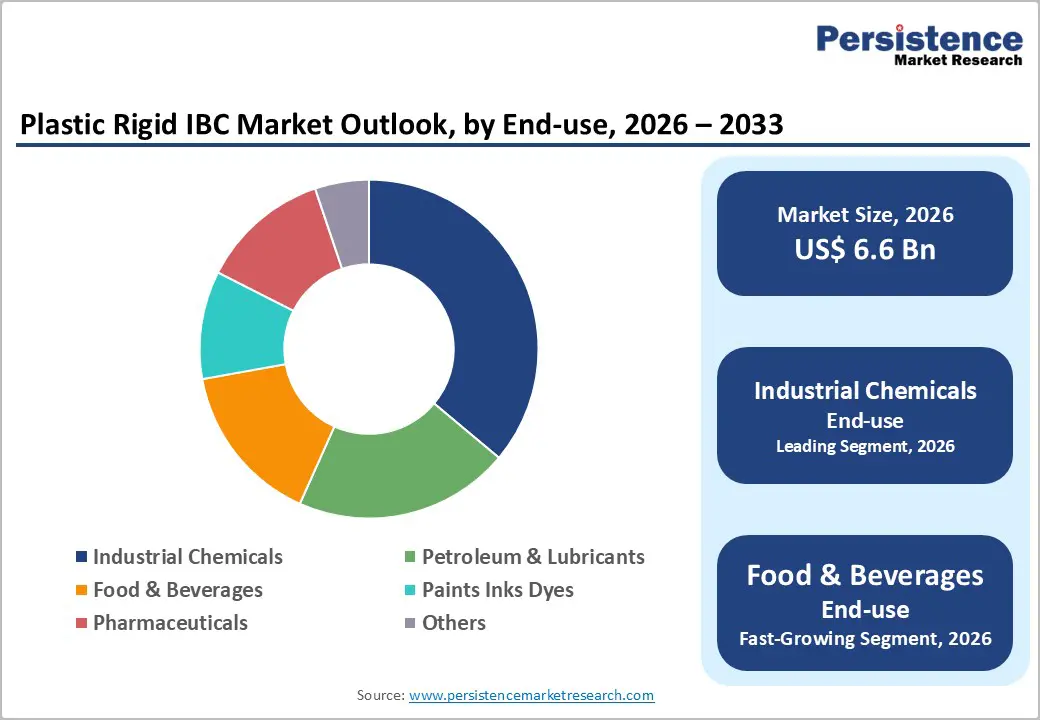

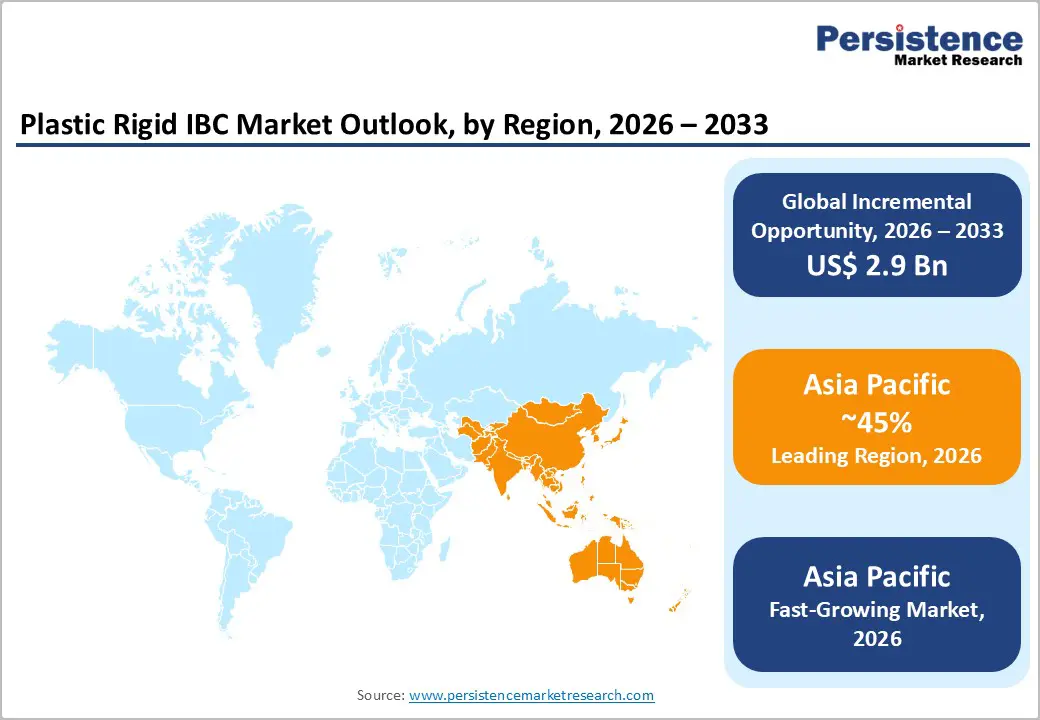

The global plastic rigid IBC market size is likely to be valued at US$6.6 billion in 2026, and is expected to reach US$9.5 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by the increasing prevalence of safe, reusable, and cost-effective bulk liquid packaging solutions across chemical, food & beverage, and pharmaceutical industries, rising demand for HDPE-based intermediate bulk containers that offer superior chemical resistance, durability, and UN/DOT compliance, and growing replacement of steel and composite IBCs with lightweight, corrosion-resistant plastic variants in industrial logistics. Increasing recognition of plastic rigid IBCs as critical for reducing product contamination, minimizing spillage risks, and supporting circular economy goals in emerging bulk liquid handling markets remains a major driver of market growth.

Key Industry Highlights:

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by massive chemical production, rapid food & beverage processing growth, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by expanding manufacturing base, increasing pharmaceutical exports, and rising adoption of reusable packaging solutions.

- Dominant Material Type: High density polyethylene (HDPE), to hold approximately 68% of the market share, as it remains the most cost-effective and chemically resistant option.

- Leading Capacity: 1000 to 1500 liters, contributing nearly 55% of the market revenue, due to an optimal balance between volume and handling ease.

| Key Insights | Details |

|---|---|

|

Plastic Rigid IBC Market Size (2026E) |

US$6.6 Bn |

|

Market Value Forecast (2033F) |

US$9.5 Bn |

|

Projected Growth CAGR (2026-2033) |

5.3% |

|

Historical Market Growth (2020-2025) |

4.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Chemical and Food Processing Volumes

Rising chemical and food processing volumes are becoming a strong growth driver for industrial equipment and materials markets as global production scales up to meet expanding consumption and manufacturing needs. In the chemical sector, increasing output of specialty chemicals, polymers, agrochemicals, and pharmaceuticals is pushing plants to operate at higher capacities and for longer cycles. This intensifies demand for robust processing equipment, corrosion-resistant materials, advanced sealing solutions, and high-purity gases to maintain safety, reliability, and product consistency under harsher operating conditions. As facilities expand or modernize, suppliers that offer durable, low-maintenance solutions benefit from higher replacement rates and new installations.

In food processing, rising urbanization, higher disposable incomes, and changing consumption habits are driving greater production of packaged, ready-to-eat, and processed foods. Higher throughput puts pressure on processing lines to deliver speed without compromising hygiene, quality, or shelf life. This fuels demand for efficient machinery, contamination-free processing environments, advanced packaging systems, and temperature-controlled logistics. Stricter quality and safety requirements further increase the need for reliable materials, sealing systems, and monitoring technologies across the production chain.

Shift Toward Reusable and Sustainable Packaging

Growing environmental awareness and regulatory pressures are driving companies to adopt reusable and sustainable packaging solutions across industries. Consumers increasingly prefer products that minimize environmental impact, prompting brands to rethink materials, design, and lifecycle management of packaging. This trend encourages the use of biodegradable plastics, recyclable materials, and durable containers that can be reused multiple times, reducing single-use waste and conserving natural resources. Companies that integrate sustainability into packaging also enhance brand reputation and align with evolving corporate social responsibility goals.

From an operational perspective, sustainable packaging requires innovation in material science, production processes, and logistics. Lightweight yet strong materials help reduce transportation costs and carbon footprint, while modular or refillable designs support the circular economy models. Manufacturers must balance sustainability with product protection, shelf life, and consumer convenience, making advanced design and testing critical. Retailers and supply chains are also adapting to handle reusable packaging systems efficiently, including collection, cleaning, and redistribution.

Barrier Analysis – High Initial Investment in Reusable IBC Fleets

Implementing a reusable Intermediate Bulk Container (IBC) fleet requires a significant upfront investment, which can be a barrier for many businesses. Unlike single-use containers, reusable IBCs are made of durable materials such as high-grade plastics, stainless steel, or composites, designed to withstand multiple cycles of filling, transport, and cleaning. Procuring a full fleet to support continuous operations can involve substantial capital outlay, including the cost of the containers themselves, storage infrastructure, and handling equipment.

In addition to procurement, companies must invest in cleaning and maintenance systems to ensure hygiene and compliance with industry standards, particularly in food, pharmaceuticals, and chemicals. Training staff to manage the logistics, inspection, and rotation of reusable IBCs adds further cost. While the long-term savings from reduced single-use packaging and lower waste disposal costs are significant, the high initial investment can delay adoption, especially for small and medium enterprises with limited capital budgets.

Cleaning and Recertification Costs

Reusable packaging, such as IBCs or bottles, requires ongoing cleaning and recertification to maintain safety, quality, and regulatory compliance. After each use, containers must be thoroughly cleaned to remove residues, prevent contamination, and avoid chemical reactions or microbial growth. This often involves specialized washing equipment, detergents, sanitizers, and sometimes high-pressure or heat-based cleaning processes, all of which add operational costs.

Beyond cleaning, containers must undergo regular inspection and recertification to ensure they remain structurally sound and leak-free. This may include pressure testing, visual inspection for cracks or deformations, and verification of seals and closures. Any container failing these checks must be repaired or replaced, further increasing expenses. These recurring cleaning and certification processes require trained personnel, dedicated space, and scheduling logistics to keep the reusable system efficient.

Opportunity Analysis – Demand in Food-Grade and Pharmaceutical-Compliant IBCs

The demand for food-grade and pharmaceutical-compliant Intermediate Bulk Containers (IBCs) is growing steadily as industries prioritize safety, hygiene, and regulatory adherence in the storage and transportation of sensitive liquids and powders. Food and pharmaceutical products require strict contamination control, making standard industrial containers unsuitable for handling ingredients, additives, or formulations that are ingested or used in healthcare applications. Food-grade IBCs are designed from materials that are non-toxic, odorless, and resistant to chemical interactions, ensuring that products maintain purity, taste, and safety throughout the supply chain. Similarly, pharmaceutical-compliant IBCs meet rigorous standards for sterility, material compatibility, and traceability, supporting adherence to Good Manufacturing Practices (GMP) and regulatory requirements.

Growth in sectors such as processed foods, beverages, nutraceuticals, and liquid pharmaceuticals has increased the need for robust, hygienic, and leak-proof containers that can withstand multiple handling cycles without compromising quality. Companies are increasingly investing in IBCs with smooth surfaces, airtight seals, and easy-to-clean designs, facilitating both operational efficiency and compliance. Reusable IBCs designed for these sectors support sustainability initiatives while maintaining stringent hygiene standards.

Expansion Chemical and Pharma Sectors

The chemical and pharmaceutical sectors are experiencing significant expansion, driven by rising global demand for specialty chemicals, active pharmaceutical ingredients, and advanced formulations. In the chemical industry, growth is fueled by increasing consumption in industries such as automotive, electronics, agriculture, and construction, which require polymers, resins, solvents, and other specialty chemicals in large volumes. Companies are scaling up production capacities, modernizing facilities, and investing in advanced processing equipment to meet stringent quality and efficiency requirements. This expansion creates opportunities for suppliers of high-performance materials, containment solutions, and process automation technologies.

In the pharmaceutical sector, factors such as growing healthcare needs, rising chronic disease prevalence, and increased access to medicines are driving higher production of both generic and innovative drugs. The expansion extends to biologics, vaccines, and nutraceuticals, which require highly controlled manufacturing environments and compliance with stringent regulatory standards. Pharmaceutical companies are investing in cleanroom infrastructure, automated filling systems, and robust logistics to ensure product integrity.

Category-wise Analysis

Material Type Insights

High density polyethylene (HDPE) is anticipated to dominate the market, accounting for approximately 68% of the market share in 2026. Its dominance is driven by its strength, durability, and chemical resistance, making it ideal for a wide range of industrial and commercial applications. Its lightweight nature and ability to withstand repeated handling and transport make it especially suitable for reusable containers, drums, and IBCs. HDPE also offers excellent resistance to moisture, acids, and most chemicals, ensuring safe storage and transportation of sensitive liquids and powders. Pyramid Technoplast Ltd produces HM?HDPE intermediate bulk containers used across chemical, food, and pharmaceutical industries for safe storage and transport of liquids and semi?solids, leveraging HDPE’s chemical resistance and durability.

Linear low density polyethylene (LLDPE) represents the fastest-growing material type, due to its exceptional flexibility, toughness, and puncture resistance. Unlike HDPE, LLDPE can stretch without breaking, making it ideal for applications requiring thin, durable films, liners, and packaging that can withstand rough handling. Its compatibility with a wide range of chemicals and resistance to cracking under stress enhance its suitability for industrial, food, and chemical containment. Pyramid Technoplast Ltd. manufactures 1,000-liter rigid Intermediate Bulk Containers (IBCs) widely used for transporting chemicals, agrochemicals, and specialty liquids. These containers rely on polyethylene-based materials that provide high durability, chemical compatibility, and resistance to stress cracking during bulk transport and storage.

Capacity Insights

1000 to 1500 liters are expected to dominate the market, contributing nearly 55% of revenue in 2026, with their optimal balance between volume efficiency and ease of handling. These sizes are large enough to reduce transportation and storage costs per unit of product, yet compact enough to allow safe maneuvering with standard forklifts and pallet systems. Industries such as chemicals, food, and pharmaceuticals favor these IBCs for bulk storage and distribution, as they support repeated use while maintaining product integrity. SBD IBC Container 1000L is a 1000?liter intermediate bulk container commonly used for storing and transporting liquids such as chemicals, oils, and food?grade materials. Its size makes it ideal for bulk handling while still being manageable with standard forklifts and pallet systems, combining efficiency with operational practicality.

Up to 500 liters represents the fastest-growing capacity, propelled by their flexibility, ease of handling, and suitability for small- to medium-scale operations. These smaller containers are ideal for businesses that require precise dosing, frequent product rotation, or transportation to locations with limited space. They are widely used in specialty chemicals, pharmaceuticals, and food-grade applications where batch control, hygiene, and contamination prevention are critical. Heavy Duty 500 Liter Plastic Collapsible Bulk IBC Container, which is widely used for storage and transport of liquids in chemical, food, and pharmaceutical settings. Smaller containers such as 500?L IBC are easier to handle manually or with smaller equipment, making them attractive for businesses with limited space or those needing frequent batch changes.

Regional Insights

North America Plastic Rigid IBC Market Trends

North America is fueled by the region’s advanced chemical processing, strong oil & gas logistics, and high public awareness of reusable packaging benefits. Distribution systems in the U.S. and Canada provide extensive support for plastic rigid IBC programs, ensuring wide accessibility across HDPE, 1000–1500 Liters, and industrial chemicals populations. Increasing demand for UN-certified, convenient, and easy-to-clean forms is further accelerating adoption, as these formats improve safety and reduce barriers associated with single-use drums.

Innovation in plastic rigid IBC technology, including stable multilayer HDPE, improved valve delivery, and targeted food-grade enhancement, is attracting significant investment from both public and private sectors. Government initiatives and EPA campaigns continue to promote use against spillage risks, sustainability concerns, and emerging reusable threats, creating sustained market demand. The growing focus on pharmaceutical grades and specialty uses, particularly for industrial chemicals and others, is expanding the target applications for plastic rigid IBCs.

Europe Plastic Rigid IBC Market Trends

Europe is propelled by increasing awareness of reusable packaging benefits, strong regulatory systems, and government-led circular economy programs. Countries such as Germany, France, the U.K., and the Netherlands have well-established chemical and food frameworks that support routine plastic rigid IBC use and encourage adoption of innovative HDPE delivery methods. These high-compliance formulations are particularly appealing for industrial chemicals populations, regulation-conscious logistics firms, and food processors, improving safety and coverage rates.

Technological advancements in plastic rigid IBC development, such as enhanced anti-static linings, application-targeted delivery, and improved 1000–1500 L grades, are further boosting market potential. European authorities are increasingly supporting research and trials for IBCs against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, sustainable options is aligned with the region’s focus on preventive waste reduction and supply-chain efficiency.

Asia Pacific Plastic Rigid IBC Market Trends

Asia Pacific is projected to dominate and be the fastest-growing, capturing 45% share in 2026, driven by rising chemical production awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Indonesia, and Thailand are actively promoting IBC campaigns to address industrial growth and emerging food safety needs. Plastic rigid IBCs are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale industrial chemicals and food & beverages drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy plastic rigid IBCs, which can withstand challenging climatic conditions and minimize leakage dependence. These innovations are critical for reaching domestic chemical plants and improving overall bulk handling coverage. Growing demand for HDPE, 1000–1500 Liters, and industrial chemicals applications is contributing to market expansion. Public-private partnerships, increased industrial expenditure, and rising investment in IBC research and production capacity are further accelerating growth. The convenience of IBC delivery, combined with improved safety and reduced risk of product loss, positions it as a preferred choice.

Competitive Landscape

The global plastic rigid IBC market is shaped by competition between established global container specialists and emerging regional manufacturers. In North America and Europe, leaders such as Mauser Packaging Solutions and Greif dominate through extensive rental networks, strong research and development capabilities, and deep connections with chemical producers. Their focus on innovative HDPE-based IBCs, particularly in the 1000–1500 L segment, enhances chemical compatibility, reduces leakage risks, and supports large-scale integration across complex supply chains.

In the Asia Pacific region, local manufacturers are gaining traction by offering cost-competitive solutions, increasing accessibility for small and medium enterprises, and expanding overall market adoption. Strategic partnerships, collaborations, and acquisitions allow companies to merge expertise, expand production capacity, and accelerate the commercialization of new IBC designs. The introduction of food-grade and pharmaceutical-compliant IBCs addresses hygiene and contamination concerns, enabling broader adoption in sensitive sectors such as beverages, nutraceuticals, and liquid food products.

Key Industry Developments

- In September 2024, Greif, Inc. opened a new facility in Pasir Gudang, Johor, Malaysia, marking a significant milestone in its global operations. The company strengthened its commitment to delivering high-quality industrial packaging solutions while actively contributing to the local economy. The new facility enhanced Greif’s production capacity in the region, enabling it to better serve chemical, food, and industrial clients with advanced HDPE IBCs and other packaging products.

- In March 2024, Mauser Packaging Solutions and RIKUTEC PACKAGING entered into an exclusive partnership to produce and promote sustainable IBC solutions globally. The collaboration combined Mauser’s expertise in sustainable industrial packaging with RIKUTEC’s experience in high-quality multiway container solutions for high-purity applications. Through this partnership, both companies aimed to advance the adoption of environmentally friendly IBCs, enhance product performance, and expand their reach across international markets.

Companies Covered in Plastic Rigid IBC Market

- Snyder Industries

- Mauser Packaging Solutions

- Greif, Inc.

- Schutz Container System

- Berry Global, Inc.

- Sotralentz

- K Tank

- SCHÜTZ Container Systems

- Hoover Ferguson

- Time Technoplast

- Thielmann

Frequently Asked Questions

The global plastic rigid IBC market is projected to reach US$6.6 billion in 2026.

Rising demand for bulk storage and transport solutions in chemicals, pharmaceuticals, and food & beverage industries is driving the adoption of durable, reusable IBCs, particularly HDPE-based and food-grade compliant containers, to ensure safety, efficiency, and regulatory compliance.

The plastic rigid IBC market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Growth in sustainable and reusable IBC solutions presents opportunities for manufacturers to develop eco-friendly, recyclable, and lightweight containers, catering to increasing environmental awareness and stricter global packaging regulations, especially in fast-growing regions such as Asia Pacific.

Mauser Packaging Solutions, Greif, Inc., Schutz Container System, Snyder Industries, and Berry Global, Inc. are the key players.