- Food Ingredients & Additives

- Passion Fruit Market

Passion Fruit Market Size, Share, and Growth Forecast, 2025 - 2032

Passion Fruit Market By Nature (Organic, Conventional), Form (Fresh, Frozen, Others), Packaging, End-user, and Regional Analysis for 2025 - 2032

Passion Fruit Market Size and Trends Analysis

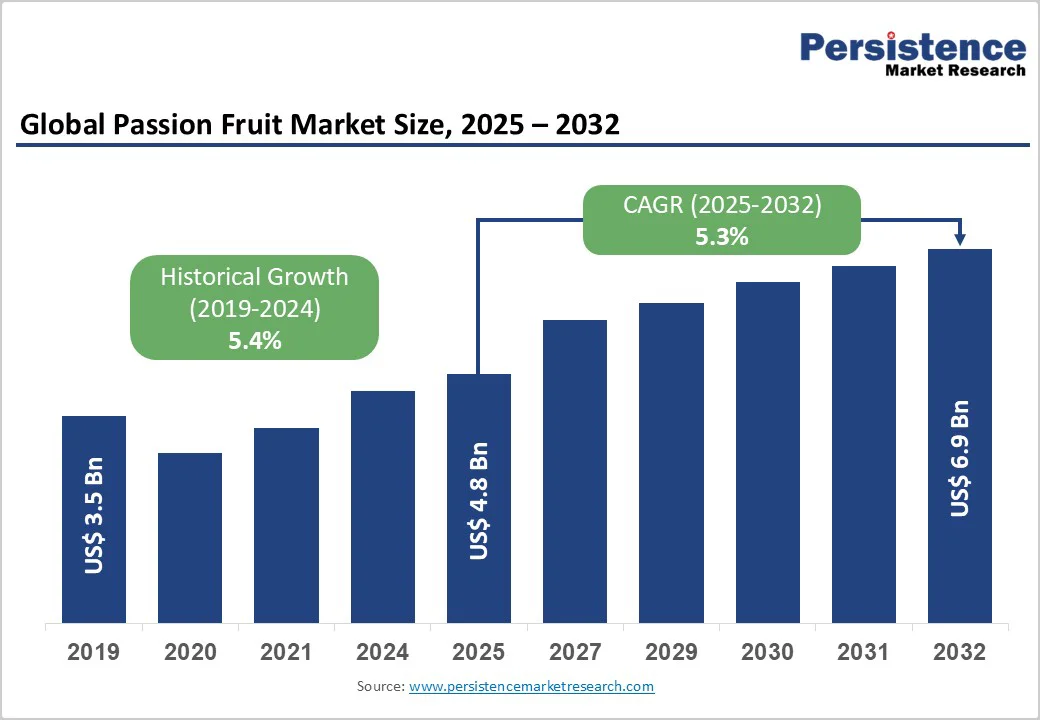

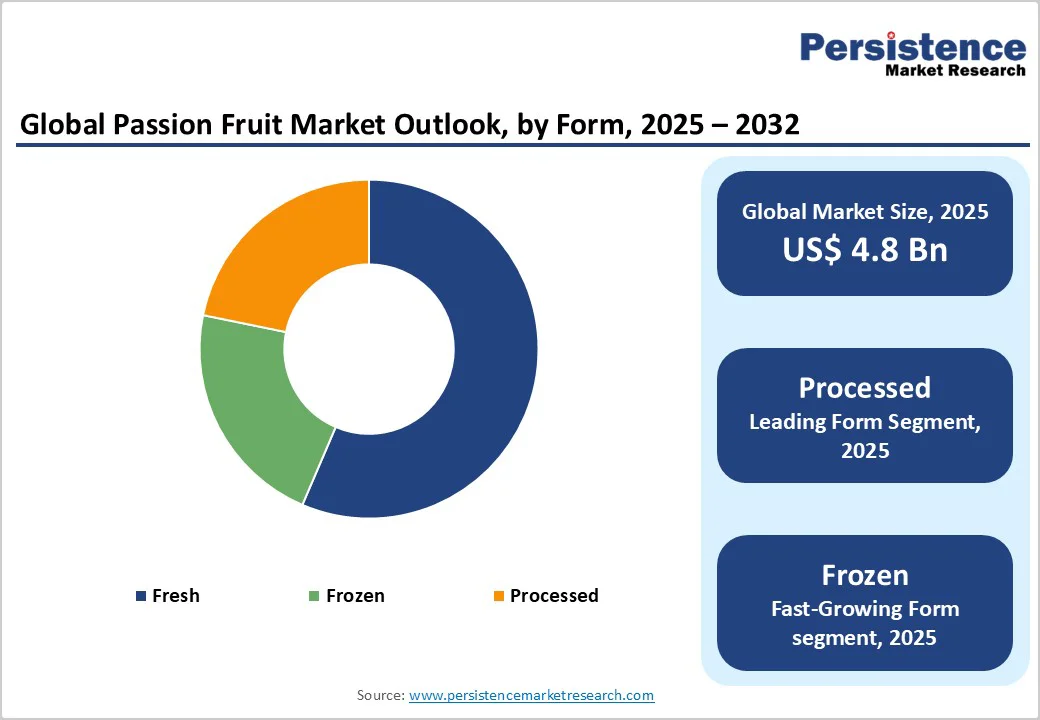

The global passion fruit market size is likely to be valued at US$4.8 Billion in 2025 and is expected to reach US$6.9 Billion by 2032, growing at a CAGR of 5.3% during the forecast period from 2025 to 2032, driven by the rising demand for exotic flavors in beverages and bakery, growing consumer interest in natural and functional ingredients, and increased usage of processed passion fruit ingredients, including purees, concentrates, and extracts, by beverage and nutraceutical manufacturers.

Key structural risks include the climate sensitivity of production, seasonal supply variations, and supply-chain bottlenecks that periodically constrain raw material availability.

Key Industry Highlights

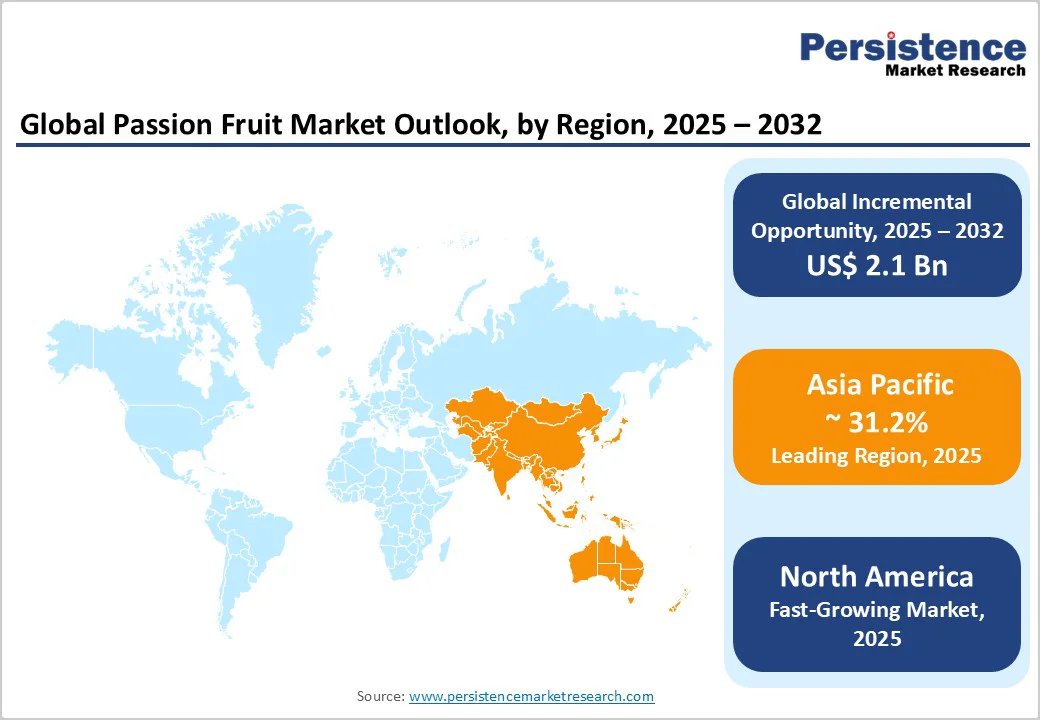

- Leading Region: Asia Pacific dominates production and processing with a market share of 31.2%, especially in Vietnam, Thailand, and China, with the largest share of global supply.

- Fastest-growing Region: North America, strong growth in demand for passion fruit derivatives, particularly in premium beverages and health-focused products.

- Investment Plans: Increased investments in frozen and processed product capabilities, cold-chain logistics, and organic certification to ensure supply consistency and quality.

- Dominant Form: Processed (juice/pulp/concentrate), leading the market with 57.6% of market share, driven by beverage and food ingredient demand.

- Leading End-user: The food and beverage sector accounts for over 59% of the total market revenue, driven by the extensive use of passion fruit puree and concentrate in juices, smoothies, yogurts, desserts, and confectionery products.

| Key Insights | Details |

|---|---|

| Passion Fruit Market Size (2025E) | US$4.8 Bn |

| Market Value Forecast (2032F) | US$6.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Exotic, Natural Flavors and Functional Ingredients

The global demand for natural, exotic fruit flavors continues to fuel market growth. Passion fruit’s aromatic profile and strong nutritional appeal, as a source of vitamin C and antioxidants, have increased its inclusion in RTD beverages, smoothies, yogurts, and functional shots.

Processed ingredient markets, particularly purees and extracts, are expanding faster than fresh fruit markets due to scale efficiencies in beverage and ingredient manufacturing. This steady ingredient demand supports processor investment and drives contracted supply from producing countries.

Verticalization of Processing and Premiumization of Product Offerings

Processors and consumer goods firms are investing in premium, traceable ingredient supply chains such as certified organic purees, cold-pressed pulps, and standardized extracts. Growth is strongest in processed and premium categories, incentivizing capacity expansion near producing regions and investment in cold-chain logistics.

These improvements reduce post-harvest losses and allow year-round supply through frozen or concentrated formats. Evidence shows processors are capturing a growing share of total industry value through such vertical integration.

Geographic Diversification of Production and Newer Origins

Traditionally concentrated in South America (notably Brazil and Ecuador), production has expanded across Asia (Vietnam, Thailand, China) and parts of Africa. Favorable climates, lower costs, and government export programs have accelerated this diversification.

Global production is estimated at 1.2-1.5 million tonnes annually, with Asia showing rapid growth. While this diversification stabilizes global supply, it introduces varietal and quality heterogeneity that affects pricing and contract terms.

Barrier Analysis - Climate Vulnerability and Crop Diseases

Passion fruit yields are highly sensitive to temperature, rainfall variability, and pollinator activity. Climate projections suggest reductions in suitable cultivation areas under adverse scenarios. Viral and fungal diseases also depress yields, causing supply and price volatility. Historical data show year-on-year yield swings of 10-25% in key producing regions, forcing processors to rely on forward contracts and inventory buffers that increase costs.

Fragmented Supply Chains and Post-Harvest Losses

High post-harvest losses, inefficient handling, and limited cold-chain infrastructure in producing countries reduce value capture. Smallholder-dominated production leads to inconsistent quality and fragmented sourcing. Processors attempting contract farming face higher working-capital needs and traceability costs, raising breakeven levels and constraining scalability.

Opportunity Analysis - Growth in Processed Ingredients and Premium Substitution

Processed segments, purees, concentrates, and extracts are expanding faster than fresh fruit as beverage and confectionery companies increase fruit content and natural flavors. Analyses show these submarkets are set to grow rapidly, potentially adding hundreds of millions of USD in value by 2032. Processors investing in quality assurance and organic certification can secure premium pricing and long-term supply agreements.

Expansion in Cosmetics and Nutraceuticals

Passion fruit derivatives rich in antioxidants and skin-care actives are gaining traction in cosmeceuticals and nutraceuticals. The growing acceptance of botanical ingredients and supportive regulatory trends present a secondary growth corridor. This segment could deliver a low double-digit percentage uplift to processed market value as partnerships between extractors and cosmetic formulators mature.

Category-wise Analysis

Form Insights

Processed passion fruit products, such as juice, pulp, and concentrate, dominate with a market share of 57.6%, serving as essential ingredients in beverages, desserts, and dairy applications. Their long shelf life and transport efficiency ensure year-round availability, making them vital for large-scale production and export.

Consistency, ease of blending, and suitability for aseptic packaging make these products highly preferred by global beverage brands. Companies such as Caribbean Natural Products, Dennick Fruitsource, and Omega Ingredients lead this space, supplying standardized flavor bases and natural extracts. The processed segment delivers the highest value per tonne due to added transformation and stability advantages.

Frozen pulps and IQF (Individually Quick Frozen) formats are the fastest-growing form segment. They preserve fresh-like flavor and nutrition while offering flexibility and cost-efficiency for manufacturers. Growth is supported by expanding cold-chain infrastructure in Latin America, Africa, and Asia, and by demand from smoothie, bakery, and foodservice industries seeking premium, minimally processed fruit.

Producers such as Tropifruit (Colombia) and Quicornac (Ecuador) are expanding frozen capacity to meet export demand, especially from European and Japanese dessert makers. The frozen segment’s freshness and convenience position it for stronger growth than fresh fruit sales.

End-user Insights

The food and beverage sector accounts for over 59% of total market revenue in 2025, driven by the use of passion fruit puree and concentrate in juices, smoothies, yogurts, and confections.

Major beverage and dairy manufacturers, such as Innocent Drinks, Minute Maid, and Naked Juice, integrate passion fruit blends for exotic and functional flavor appeal. Its high acidity, aroma, and nutrient profile also support its use in functional and clean-label beverages targeting health-conscious consumers. Rising global demand for tropical flavors ensures the continued dominance of this segment.

The cosmetics and nutraceuticals segment is smaller but expanding rapidly as natural, plant-based actives gain popularity. Passion fruit seed oil, rich in linoleic acid and antioxidants, is incorporated into skincare and haircare formulations by ingredient suppliers such as BASF, Clariant, and Hallstar.

In nutraceuticals, standardized extracts containing polyphenols and piceatannol are used in supplements for metabolic and cardiovascular health by firms such as Nektium and Naturex. Growing consumer interest in sustainability and natural wellness is propelling this segment’s high-margin growth potential.

Regional Insights

North America Passion Fruit Market Trends - Premiumization and Functional Beverage Expansion

North America is a leading consumer market for passion fruit ingredients, particularly for premium beverages, natural flavorings, and functional products. The U.S. drives regional demand due to its large foodservice sector, advanced beverage R&D, and strong consumer acceptance of exotic flavors.

Passion fruit puree and concentrate are widely used in smoothies, RTD (ready-to-drink) beverages, tropical cocktails, and flavored waters. Canada and Mexico play supporting roles, contributing niche consumption markets and acting as logistic hubs for imported ingredients.

The key market drivers include the rising popularity of clean-label and functional beverages, the proliferation of RTD products, and the premiumization of tropical flavors. Regulatory standards under the FDA and USDA emphasize labeling, allergen control, and validation of health claims, favoring certified and traceable suppliers.

Investment trends show growing interest in refrigerated logistics, cold-chain infrastructure, and organic ingredient lines, often supported by private equity. In the U.S., passion fruit has moved from an exotic niche to a near-mainstream flavor in beverage and food products.

Imports of processed passion fruit, particularly puree and concentrate from Latin America, have increased to meet growing demand from smoothie bars, cafés, and health-focused beverage brands. Consumer trends toward functional and clean-label products continue to boost the segment growth.

Europe Passion Fruit Market Trends - Sustainability, Traceability, and Regulatory-Driven Quality Focus

Europe represents a mature but increasingly premiumized market for processed passion fruit ingredients. Germany, France, the U.K., and Spain are the largest consumers, supported by well-developed dairy, beverage, and retail sectors. Processors and flavor houses are emphasizing sustainably sourced passion fruit purees and seed oils to meet consumer and retailer requirements, reflecting Europe’s strong focus on traceability and sustainability.

Market growth is driven by clean-label trends, innovation in craft beverages and RTD products, and the post-pandemic recovery of foodservice operations.

Stringent EU regulations regarding food, beverage, and cosmetic ingredients, including residue limits, safety standards, and labeling compliance, elevate entry barriers, encouraging partnerships between certified suppliers and major retailers. Investments in Europe focus on traceability, certification, and farmer-support programs to ensure consistent quality and compliance.

Germany acts as a gateway for processed passion fruit into Europe, with ports like Hamburg serving as key import and distribution hubs. German beverage and dairy manufacturers prioritize precision, premium flavors, and standardized ingredient quality, making processed passion fruit concentrates and purees highly sought after for both industrial and retail applications.

Asia Pacific Passion Fruit Market Trends - Production Scale-Up, Export Growth, and Agro-Processing Investment

Asia Pacific dominates production and processing with a market share of 31.2% in 2025. Leading countries include China, Vietnam, Thailand, and India, which serve both local consumption and export markets.

For example, Vietnam’s Nafoods Group operates a closed value chain for passion fruit, processing over 25,000 tons annually and exporting to more than 70 countries. Regional growth is supported by rising disposable incomes, urbanization, expanded cold-chain infrastructure, and government-backed agro-processing initiatives.

Export diversification is also a key driver, with Vietnam recently securing protocols for exporting fresh and processed passion fruit to China and Australia. Investments are concentrated on processing facilities, particularly freezing, pulp, and concentrate lines, as well as contract farming to ensure supply stability.

Vietnam is among the world’s top ten passion fruit exporters, with export turnover increasing by roughly 300% over the past five years. The Gia Lai province has expanded cultivation from approximately 4,200 hectares to a projected 20,000 hectares by 2025 under a MoU with Nafoods, reflecting the region’s focus on large-scale, export-oriented production.

Competitive Landscape

The global passion fruit market features fragmented primary production but moderate consolidation in processing and ingredient supply. Smallholders dominate cultivation, while processors and global ingredient houses capture higher margins through certification and traceability. Key players include Passi AG, Caribbean Natural Products, Dennick Fruitsource, Fratelli Indelicato, Omega Ingredients, AGRANA, and Quicornac.

Top strategies include vertical integration through contract farming, premiumization via organic and traceable product lines, and diversification into cosmetics and nutraceuticals. Firms differentiate through certifications, standardized extract profiles, and long-term supply agreements with major food and beverage manufacturers.

Key Industry Developments

- In January 2025, FreshPassion Inc. debuted a Premium Health-Focused Drinks Line, which incorporates passion fruit in a range of functional beverages designed for health-conscious consumers seeking natural, exotic flavors.

- In February 2025, Passion Foods International introduced an Eco-Friendly Sustainable Packaging Initiative, which focuses on reducing plastic use by transitioning to biodegradable materials for their passion fruit juice and puree products.

Companies Covered in Passion Fruit Market

- Döhler Group

- AGRANA Beteiligungs‑AG

- SunOpta Inc.

- Kiril Mischeff Ltd

- SVZ International B.V.

- Aseptic Fruit Purees

- Citrofrut S.A. de C.V.

- The Kraft Heinz Company

- Nestlé S.A.

- Symrise AG

- Ingredion Incorporated

- Dole Food Company, Inc.

- Goya Foods, Inc.

- Tree Top Inc.

- Quicornac S.A.

- Sucorrico S.A.

- Capricorn Food Products India Ltd.

- Jain Irrigation Systems Ltd.

- Shimla Hills Offerings Pvt. Ltd.

- Ariza B.V.

Frequently Asked Questions

The passion fruit market size is projected to reach an estimated US$4.8 Billion in 2025.

The passion fruit market is projected to reach US$6.9 Billion by 2032.

Key trends include the growing demand for organic, clean-label products, sustainable packaging solutions, and a rise in health-conscious consumers seeking functional and exotic beverages.

The leading segment is passion fruit juices and purees, particularly those targeting the premium and health-focused beverage categories.

The passion fruit market is expected to grow at a CAGR of 5.3% from 2025 to 2032.

Major players include TropiFresh Ltd., FreshPassion Inc., Passion Foods International, and Kernow Organic Ltd.