- Food Ingredients & Additives

- Passion Fruit Puree Market

Passion Fruit Puree Market Size, Share, and Growth Forecast, 2025 - 2032

Passion Fruit Puree Market By Product Type (Conventional, Organic, Others), Form (Frozen Single-Strength Puree, Aseptic Shelf-Stable Puree, Others), Application, and Regional Analysis for 2025 - 2032

Passion Fruit Puree Market Size and Trends Analysis

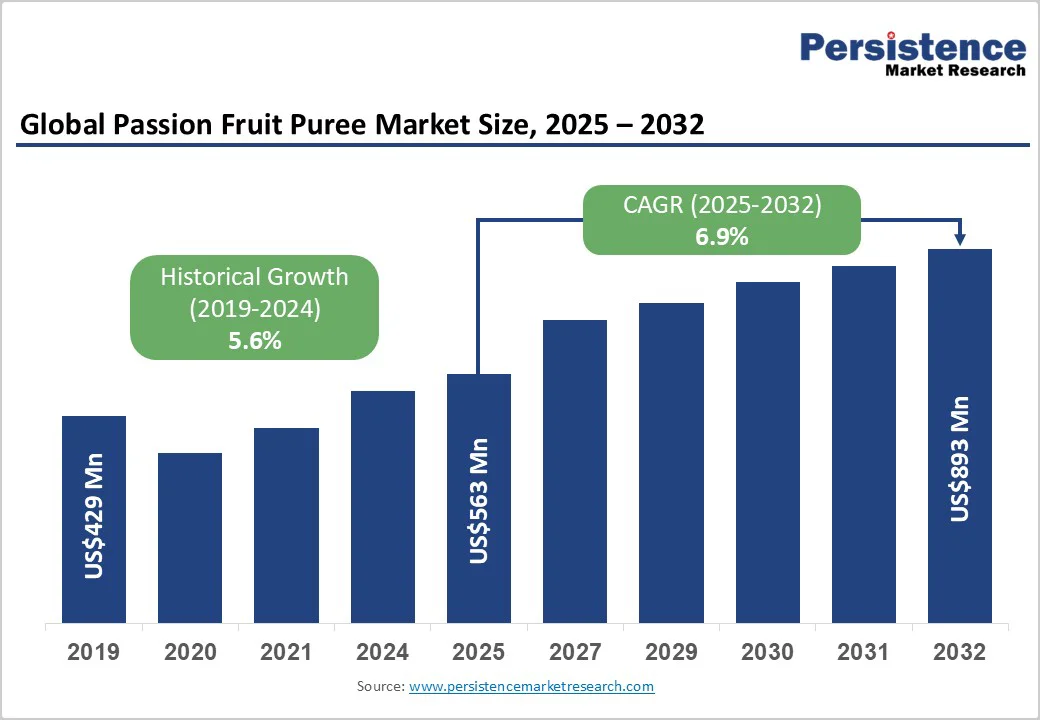

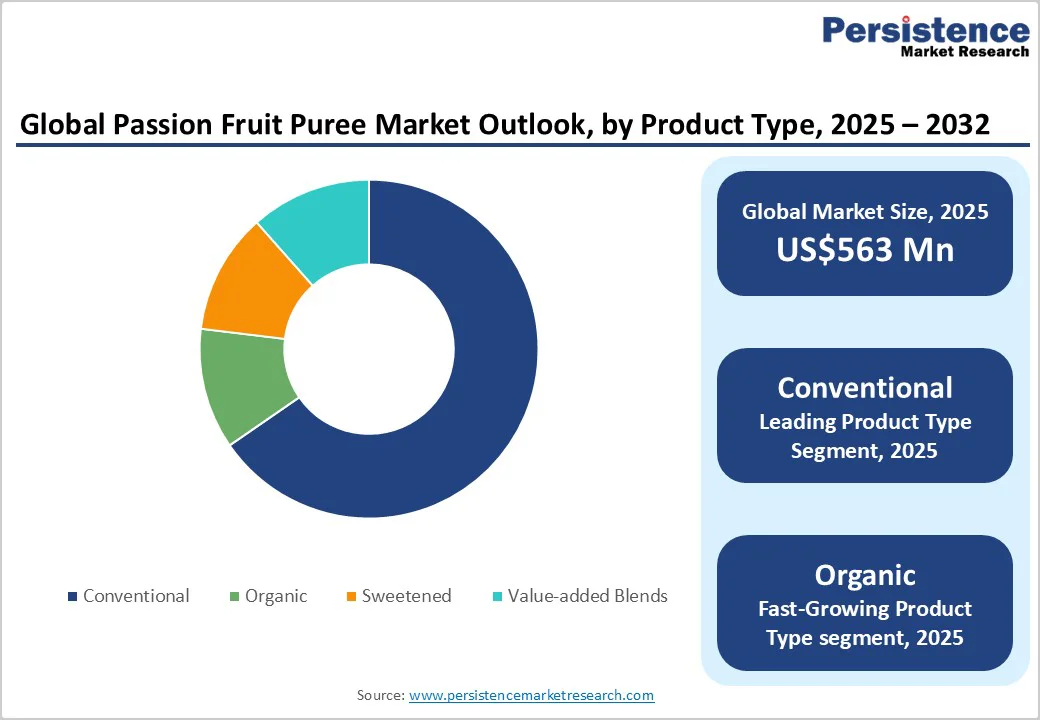

The global passion fruit puree market is likely to be valued at US$563 Million in 2025 and is expected to reach US$893 Million by 2032, growing at a CAGR of 6.9% during 2025 - 2032, driven by rising consumer demand for natural, tropical flavors and clean-label fruit ingredients in beverages and dairy applications.

Producers are expanding aseptic and frozen-puree capacity for a consistent supply, while volatility in Ecuador and Colombia drives vertical integration. Market estimates vary by the inclusion of concentrates and derivatives.

Key Industry Highlights

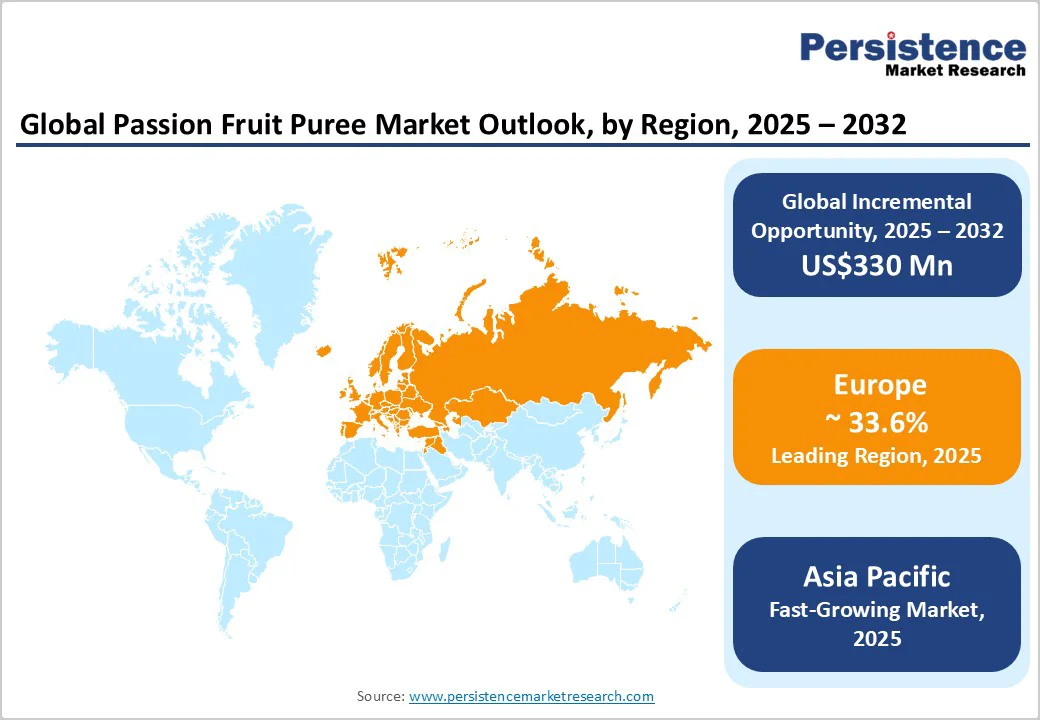

- Leading Region: Europe currently holds the largest market share at 33.6% of the global revenue, driven by established demand from the beverage, patisserie, and premium dessert sectors in France, Germany, and the U.K.

- Fastest-growing Region: Asia Pacific, led by expanding tropical beverage consumption and new juice-blend innovations in China, India, and Indonesia.

- Investment Plans: Global processors such as AGRANA Fruit, SVZ International, and Polpaico are investing in aseptic filling and cold chain infrastructure across Latin America and Southeast Asia (2024 - 2026) to secure year-round raw fruit availability and optimize export logistics.

- Dominant Product Type: Conventional puree remains the leading type, accounting for over 67.3% of the total market share due to its stability, cost competitiveness, and compatibility with multi-application industrial processing, making it the reference standard for beverage and dairy manufacturers globally.

- Leading Application: Beverages dominate the application landscape, contributing to 44.5% of the market share supported by high incorporation in RTD juices, smoothies, and functional beverages, with robust uptake across both retail and HoReCa channels.

| Key Insights | Details |

|---|---|

| Passion Fruit Puree Market Size (2025E) | US$563 Mn |

| Market Value Forecast (2032F) | US$893 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Health and Natural-Ingredient Demand in Beverages and Dairy

Consumer preference for “real fruit” and clean-label formulations is the strongest demand driver. The growing popularity of tropical, antioxidant-rich fruits is fuelling launches in ready-to-drink (RTD) beverages, smoothies, flavored yogurts, and functional shots, categories expanding faster than traditional sodas. Beverage manufacturers increasingly source single-strength and aseptically filled passion-fruit purees to achieve clean-label claims and maintain flavor authenticity.

Expansion of Aseptic Processing and Shelf-Stable Formats

Technological advances, particularly aseptic filling, high-pressure processing, and frozen IQF systems, are widening the market’s reach by enabling year-round availability, longer shelf life, and ambient distribution. Aseptic purees retain sensory quality without preservatives, appealing to beverage and brewing customers.

This shift reduces seasonality constraints and lowers logistics costs, allowing broader use in dairy, bakery, sauces, and alcoholic beverages. Supplier portfolios show strong investments in aseptic capacity, confirming measurable incremental uptake in non-seasonal product categories.

Asia Pacific Emerges as a Key Growth Hub

The Asia Pacific region shows above-average growth for tropical fruit ingredients, driven by urbanization, premiumization in beverages, and cold-chain expansion. China, India, and ASEAN countries are emerging as significant consumption hubs for exotic fruit purees.

The region’s expanding RTD beverage, dairy dessert, and quick-service restaurant segments support rapid growth. This shift helps offset maturity in North America and Europe while creating local sourcing-to-manufacture opportunities within Asia.

Barrier Analysis - Raw-material Supply Volatility and Concentration Risks

Global passion-fruit supply remains heavily dependent on a few producing countries. Weather disruptions, crop diseases, and yield fluctuations in Ecuador and Colombia cause price spikes and procurement uncertainty. Export disruptions often force buyers to hold additional inventory or substitute with alternative fruits. This geographic concentration elevates supply-chain risk and margin pressure for puree manufacturers.

Price Sensitivity and Competition from Flavorings and Concentrates

In cost-sensitive beverage categories, formulators often replace purees with cheaper fruit concentrates or artificial flavorings to maintain price competitiveness. This limits penetration of puree in mass-market drinks, creating a two-tier market, where premium clean-label products expand while cost-driven segments rely on lower-priced alternatives. The resulting segmentation restrains overall volume growth despite strong demand in premium niches.

Premium Beverages, Craft Alcohol, and RTD Innovations

Passion-fruit puree’s aromatic and acidic profile positions it ideally for premium cocktails, craft beers, hard seltzers, and functional beverages. Market analyses identify the beverage sector as the leading value driver for puree producers.

Even capturing a minor share of the global RTD beverage expansion represents a substantial incremental opportunity. Partnerships between puree suppliers and beverage co-packers offer accelerated entry into high-margin, innovation-driven channels.

Organic and Certified Clean-Label Lines

The growing consumer willingness to pay for organic, non-GMO, and fair-trade fruit products presents a profitable niche. Certified organic purees command price premiums in North America and Europe. Suppliers that maintain traceable, certified sourcing programs can secure long-term supply contracts with premium beverage and dairy brands.

The organic segment, although smaller in absolute volume, is expanding faster than conventional products, creating an attractive growth tier within the overall market.

Category-wise Analysis

Product Type Insights

Conventional passion fruit puree dominates the global market, accounting for about 67.3% of total industry volume in 2025. Typically unsweetened and single-strength, it is supplied frozen or aseptic to balance cost efficiency, flavor integrity, and versatility.

Widely used across beverages, bakery, and dairy, conventional puree serves as a staple ingredient for both industrial and artisanal production. Major suppliers such as SVZ and AGRANA use purple and yellow passion fruits sourced from Ecuador, Colombia, Brazil, and Peru, freezing the pulp immediately after extraction to preserve nutrients.

Organic and certified clean-label passion fruit purees are the fastest-growing segment, reflecting rising demand for transparency, sustainability, and ethical sourcing. Producers emphasizing farm partnerships and traceable origin labeling are securing long-term contracts with premium brands.

The Perfect Purée of Napa Valley offers organic, traceable options for chefs and beverage developers, while Ponthier’s “Pure Origine” line showcases single-origin fruits from Ecuador and Vietnam, reinforcing trust and quality assurance among European buyers.

Application Insights

The beverage sector accounts for over 44.5% of global passion fruit puree demand, making it the largest application segment. The puree’s vibrant color, tropical acidity, and aromatic intensity make it ideal for juices, smoothies, RTD drinks, mocktails, and yogurt beverages. Its rich Vitamin C and polyphenol content reinforces clean-label positioning and antioxidant benefits, appealing to health-conscious consumers.

Leading brands such as Tropicana’s Tropical Mix and Innocent Drinks’ Passion Power feature passion fruit prominently, while Yili and Amul have launched passion fruit yogurt drinks to capitalize on tropical flavor trends. In the foodservice sector, The Perfect Purée, Monin, and Oregon Fruit Company supply aseptic and frozen purees for cocktails and smoothies, with aseptic formats preferred for ease of storage and portion control.

Rapid growth is emerging in the craft alcoholic and RTD cocktail category, driven by younger consumers seeking authentic, fruit-forward beverages.

Passion fruit’s tangy profile is favored by brewers and mixologists alike. U.S. brands such as Dogfish Head Brewery and Anderson Valley Brewing use it in tropical beers and sours, while Bacardi’s Tropical Fusion and Absolut’s Passion RTD highlight natural puree flavoring. Its stability and preservative-free blending make aseptic puree ideal for alcoholic, low-ABV, and alcohol-free mocktail innovations.

Regional Insights

North America Passion Fruit Puree Market Trends -Premiumization & Aseptic Innovation Drive U.S.-Led Growth

North America, dominated by the U.S., is a key value market for passion-fruit puree, propelled by strong consumer demand for premium beverages and desserts. Domestic producers such as The Perfect Purée of Napa Valley, Oregon Fruit Company, and Kerr by Ingredion cater to foodservice, craft beverage, and specialty dairy channels.

Imports from Latin America complement domestic output, ensuring supply continuity. Growth drivers include the expanding RTD and craft-cocktail segments, a sophisticated foodservice industry, and rising adoption of aseptic formats in beverage manufacturing. Canada and Mexico serve as important trade partners and logistics corridors.

The regulatory environment, led by the FDA and USDA standards, demands rigorous traceability and organic certification documentation. Non-GMO and fair-trade labelling are growing differentiators. The regional competitive landscape blends local specialists with global ingredient suppliers, encouraging strategic collaborations such as co-packing agreements and joint innovations.

Investments in aseptic filling lines, cold-storage expansion, and certified sourcing remain key strategic trends. Recent developments include U.S. suppliers launching freeze-dried and aseptic passion-fruit ranges for beverage innovation, underscoring premiumization and versatility.

Europe Passion Fruit Puree Market Trends - Mature Premium Market Anchored by France and Industrial Hubs

Europe is the leading market with a market share of 33.6% and represents a mature but high-value market for fruit purees, with France, the U.K., and Germany as primary consumption centres and Spain and the Netherlands as processing hubs.

Leading producers such as Ponthier, Ravifruit, AGRANA/Dirafrost, and Döhler serve both domestic and export markets. France leads through its artisan pastry and high-end foodservice segments; Germany focuses on large-scale industrial ingredient supply; and the U.K. and Spain act as key import and blending centers.

Key growth drivers include premium bakery innovation, private-label premiumization in dairy and desserts, and demand for traceable clean-label ingredients. The regulatory framework under EU food law enforces harmonized labeling, residue limits, and traceability requirements, raising compliance costs but enhancing consumer confidence.

Europe’s market structure combines specialist frozen-puree houses and large ingredient corporations, leading to moderate consolidation. Investment activity is strongest in organic certification, B2B formulation services, and cold-chain expansion for export markets. Sustainability commitments and traceable sourcing have become major commercial differentiators.

Asia Pacific Passion Fruit Puree Market Trends - Fastest-Growing Market Fueled by Café Culture & RTD Innovation

Asia Pacific is the fastest-growing regional market for passion-fruit puree, driven by rising disposable incomes, modernized retail infrastructure, and an expanding RTD beverage base. While historical volumes were modest, APAC’s growth outpaces all other regions.

China shows strong demand for imported premium fruit ingredients, while India and ASEAN are witnessing growth in dairy drinks, juices, and artisanal desserts. Japan and South Korea remain major premium consumers, often sourcing through local distributors.

Drivers include urbanization, café culture expansion, and Western-inspired beverage innovation. Quick-service and coffee chains increasingly use fruit purees in tropical beverage lines. Regulatory diversity across APAC poses operational challenges, and additional restrictions, import documentation, and labelling differences elevate entry costs.

Halal and organic certifications are crucial in Southeast Asia and the Middle East export pathways. The competitive landscape is fragmented, with both regional producers and multinational suppliers building local partnerships. Investments in regional filling lines, distribution hubs, and certified processing are accelerating. Aseptic and shelf-stable formats are central to addressing infrastructure constraints and expanding market penetration.

Competitive Landscape

The global passion fruit puree industry consists of specialist processors and global ingredient houses. Frozen puree supply remains fragmented, supported by numerous regional producers, while aseptic supply is more consolidated among multinational ingredient firms.

Major suppliers leverage distribution networks, co-pack partnerships, and technical services to maintain share. Variations in reported market share across research firms stem from differing definitions of puree versus concentrate products.

Dominant strategic priorities include premiumization (organic, single-origin), diversification of formats (frozen and aseptic), and supply-chain integration through farm partnerships. Leading firms differentiate via formulation support, technical services, and co-packing collaborations that foster customer loyalty and recurring contracts.

Key Industry Developments

- In December 2024, the Perfect Purée of Napa Valley announced a partnership with Döhler to launch a co-branded freeze-dried and premium puree line for beverage and hospitality markets, signalling deeper collaboration between regional specialists and global ingredient suppliers.

- In April 2025, Döhler North America completed the acquisition of Premier Juices to strengthen its natural fruit-based product offerings and supply chain presence in the North American region.

Companies Covered in Passion Fruit Puree Market

- AGRANA Fruit

- SVZ International

- Kiril Mischeff

- Aseptic Fruit Purees

- Shimla Hills Offerings Pvt. Ltd.

- Tree Top Inc.

- Doehler GmbH

- Dennick Fruitsource Ltd.

- Capricorn Food Products India Ltd.

- Oregon Fruit Products LLC

- Kiril Mischeff Ltd.

- Ariza BV

- Prodalim Group

- Polpaico

- Verger Delporte

- Ponthier SAS

- Ravifruit (Andros Group)

- Quicornac S.A.

- Diana Food (Symrise Group)

- Cobell Ltd.

Frequently Asked Questions

The passion fruit puree market size is estimated at US$563 Million in 2025.

By 2032, the passion fruit puree market is projected to reach US$893 Million, expanding at a CAGR of 6.9% from 2025 to 2032.

Key trends include the shift toward organic and clean-label fruit purees, the adoption of aseptic packaging for longer shelf stability, and the rising use in craft beverages and functional foods.

The conventional puree segment leads the passion fruit puree market, contributing over 68% of the total global volume in 2025 due to its cost efficiency, versatility, and wide availability across industrial applications.

The passion fruit puree market is anticipated to grow at a CAGR of 6.9% between 2025 and 2032.

Prominent players include AGRANA Fruit, SVZ International, Doehler GmbH, Tree Top Inc., and Andros Group (Ravifruit).