- Medical Devices

- Needle-Free Injectors Market

Needle-Free Injectors Market Size, Share, and Growth Forecast 2026 - 2033

Needle-Free Injectors Market by Injector Type (Disposable, Reusable), Application (Vaccine Delivery, Insulin Delivery, Pain Management, Pediatric Injections, Dermatology & Cosmetic Treatments, Others), End-user (Hospitals & Clinics, Home Care Settings, Ambulatory Surgical Centers, Research Institutes), by Regional Analysis, 2026-2033

Needle-free Injectors Market Share and Trends Analysis

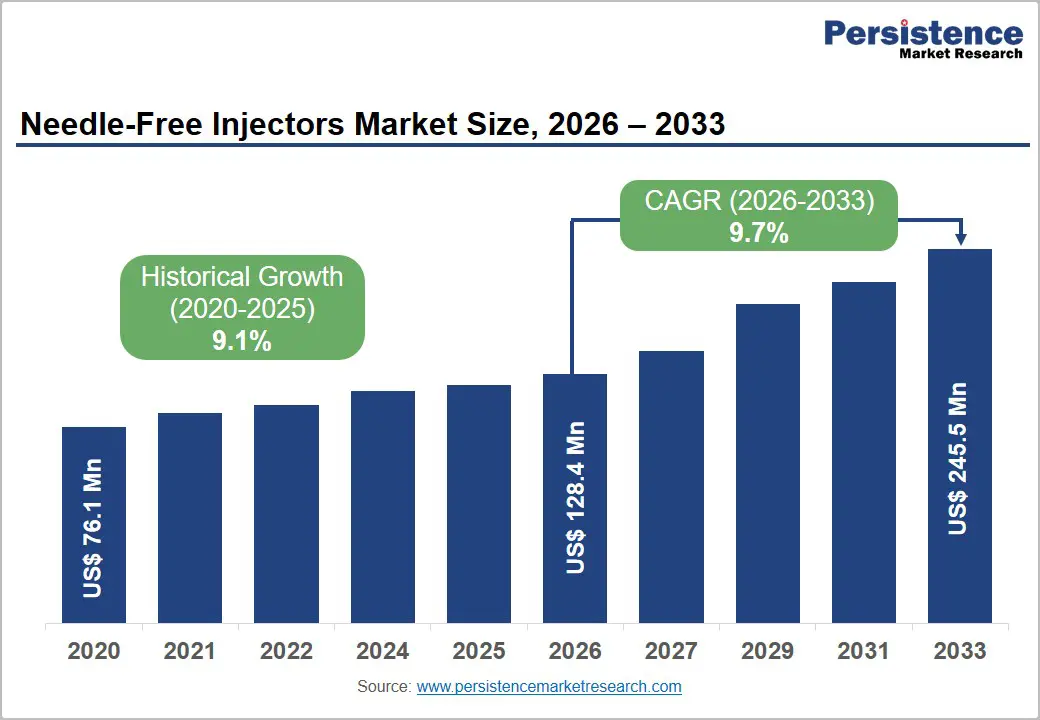

The global needle-free injectors market size is expected to be valued at US$ 128.4 million in 2026 and projected to reach US$ 245.5 million, growing at a CAGR of 9.7% between 2026 and 2033. Contributors include the rise in global vaccine administration programs, the expanding diabetic population with the need for frequent insulin delivery, and rise in patient and healthcare provider preference for needle-free drug delivery solutions that eliminate needlestick injuries. The World Health Organization (WHO) estimates that unsafe injection practices cause approximately 1.7 million hepatitis B infections and 315,000 HIV infections annually, a critical public health imperative that underpins policy-level support for needle-free injection technologies globally.

Key Industry Highlights:

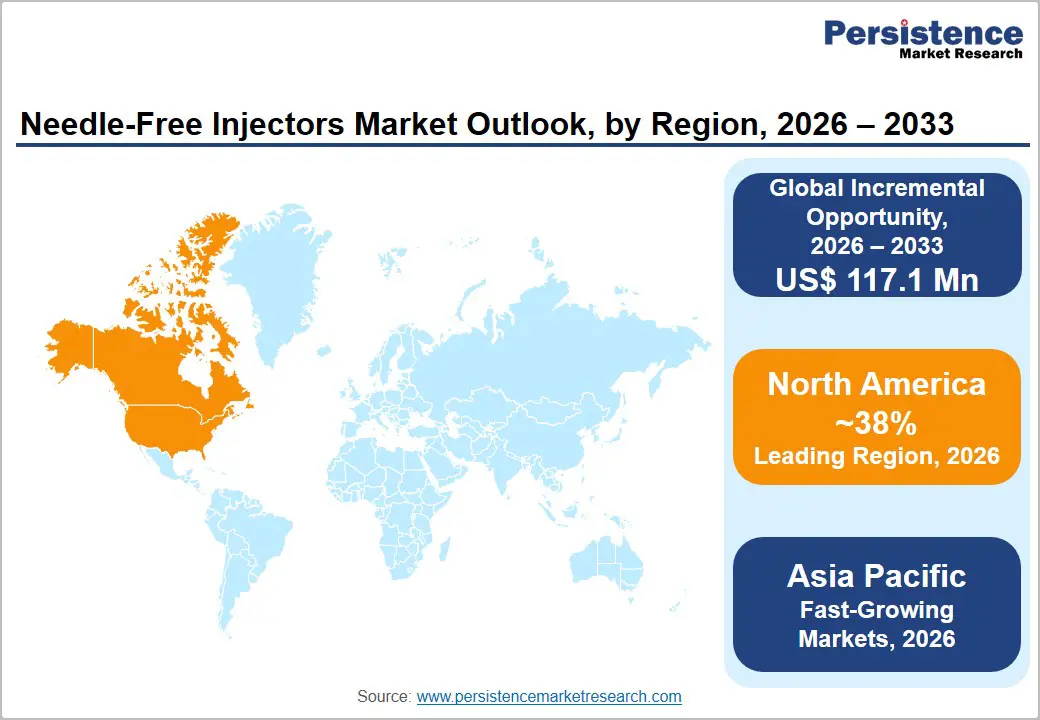

- Leading Region – North America commands approximately 38% of the global needle-free injectors market in 2026, anchored by the U.S. is over 37 million diabetic patients, robust FDA-supported device innovation, and OSHA-driven needlestick injury prevention mandates in healthcare settings.

- Fastest Growing Region – Asia Pacific is the fastest-growing needle-free injectors market through 2033, driven by China's 140 million diabetic patients (IDF), India's large-scale national vaccination programs, and expanding healthcare infrastructure investment across ASEAN member states.

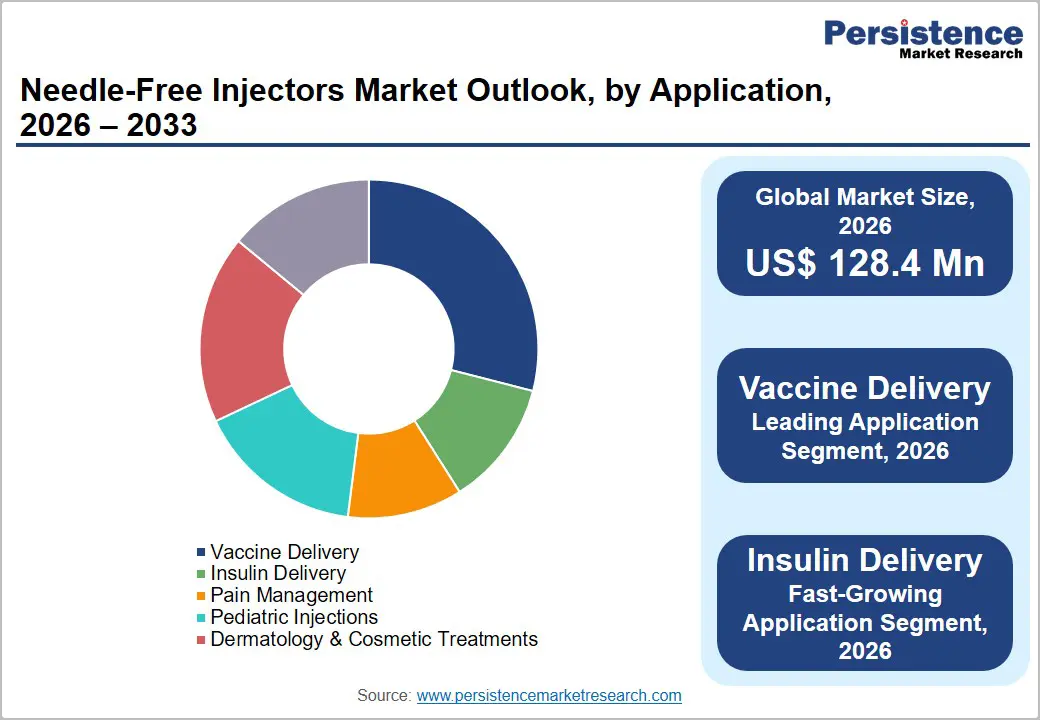

- Dominant Segment – Vaccine delivery leads the application segment with approximately 29% market share in 2026, supported by over 2 billion annual vaccine doses globally (WHO), PharmaJet's WHO-prequalified Stratis system, and Gavi-supported procurement for mass immunization campaigns in LMICs.

- Fastest Growing Segment – Insulin delivery is the fastest-growing application, propelled by the IDF's projection of 783 million diabetic patients by 2045 and documented needle anxiety affecting 20–40% of insulin-dependent patients, creating a large, compliance-driven demand base for needle-free delivery alternatives.

Market Dynamics

Drivers - Expanding Global Immunization Programs Driving Mass Vaccine Delivery Adoption

Large-scale global immunization initiatives are the foremost structural demand driver for needle-free injectors, particularly jet injector systems designed for rapid, high-volume vaccine delivery in mass campaign settings. The WHO and UNICEF estimate that over 2 billion vaccine doses are administered annually through national immunization programs worldwide. PharmaJet's Stratis needle-free injection system the first WHO-prequalified needle-free injector, has been deployed in mass vaccination campaigns across Africa, Asia, and Latin America, validating the technology's scalability and safety profile.

The Gavi, the Vaccine Alliance, has been a key procurement partner for needle-free vaccine delivery in low-income countries. The lessons from COVID-19 mass vaccination drives have further demonstrated the operational advantages of needle-free systems in reducing waste disposal burden and enabling faster throughput per vaccination station.

Rapidly Growing Global Diabetic Population Fueling Insulin Delivery Device Demand

The escalating global diabetes epidemic is creating sustained and expanding demand for needle-free insulin delivery systems. The International Diabetes Federation (IDF) estimates that 537 million adults were living with diabetes in 2021, with projections reaching 783 million by 2045. Needle anxiety is a clinically documented barrier to insulin therapy initiation and adherence, affecting approximately 20–40% of insulin-dependent patients, according to studies published in Diabetes Care. Needle-free insulin jet injectors such as those developed by Antares Pharma and Valeritas Holdings offer a compelling compliance-enhancing alternative, particularly for pediatric diabetic patients and needle-phobic adults. The growing adoption of home insulin self-administration platforms further reinforces the commercial potential of needle-free insulin delivery devices.

Restraints - High Device Cost and Reimbursement Limitations Constraining Patient Uptake

Needle-free injectors carry significantly higher upfront device costs compared to conventional syringes and needle-based auto-injectors. Premium needle-free injector systems can cost between US$ 30 and US$ 300 per device substantially more than disposable needles priced at cents per unit. In many healthcare systems, needle-free injectors are not consistently reimbursed by public or private insurers, requiring patients to bear the cost differential out-of-pocket. This price gap significantly constrains adoption, particularly in price-sensitive emerging markets and among lower-income patient populations in high-income countries who lack supplemental insurance coverage for advanced drug delivery devices.

Variable Drug Delivery Precision and Regulatory Complexity Limiting Clinical Confidence

Needle-free injectors can exhibit variability in drug dispersion depth and bioavailability depending on skin thickness, injection pressure, and formulation viscosity factors that can introduce pharmacokinetic inconsistency relative to conventional needle-based injections. Clinical studies published in the Journal of Pharmaceutical Sciences have noted that intradermal drug delivery depth with jet injectors can vary by up to 2–3 mm across patient subgroups, complicating dose standardization for narrow therapeutic index drugs. Regulatory pathways for novel needle-free devices governed by the FDA as combination products require extensive clinical validation, adding development time and cost that can deter smaller companies from bringing innovative devices to market.

Opportunities - Insulin Delivery: The Fastest-Growing Application Segment with Massive Patient Pipeline

Needle-free insulin delivery represents the fastest-growing application in the needle-free injectors market, offering a transformative opportunity for device manufacturers targeting the 537 million global diabetic patients requiring frequent drug administration. As GLP-1 receptor agonists, including Ozempic (Novo Nordisk) and Mounjaro (Eli Lilly) expand into obesity management and become among the world's best-selling injectable drugs, the commercial case for patient-friendly needle-free delivery platforms intensifies. Antares Pharma's XYOSTED auto-injector platform and next-generation needle-free GLP-1 delivery systems under development represent the commercial frontier. The IDF projects a 46% increase in global diabetes prevalence through 2045, sustaining a multi-decade commercial runway for needle-free insulin and metabolic drug delivery innovation.

Pediatric and Home Care Settings: Untapped High-Growth End-User Segments

Pediatric patients and home care settings represent highly underpenetrated but rapidly growing end-user opportunities for needle-free injectors. Needle phobia affects an estimated 25% of adults and up to 63% of children, according to studies in the Pain journal, making needle-free alternatives a compelling clinical solution for pediatric vaccination, allergy immunotherapy, and growth hormone delivery. The U.S. Centers for Disease Control and Prevention (CDC) notes that childhood immunization compliance is directly impacted by injection-related anxiety, supporting the case for needle-free vaccine delivery in pediatric settings.

In-home care, the WHO, and national health systems are expanding self-administration programs for chronic disease management, creating a growing patient demand for safe, easy-to-use needle-free devices that eliminate sharps disposal risks and enable independent medication adherence.

Category-wise Analysis

Injector Type Insights

Disposable needle-free injectors represent the leading injector type segment, commanding approximately 62% of global revenues in 2026. The dominance of disposable devices is driven by their inherent infection control advantages, eliminating cross-contamination risk between patients, and their suitability for mass vaccination campaigns where single-use sterility is non-negotiable. WHO and UNICEF procurement guidelines for large-scale immunization programs favor single-use injection systems. PharmaJet's disposable Stratis system is a prime commercial exemplar deployed across multiple Gavi-supported immunization campaigns.

Additionally, the rise of pre-filled, unit-dose needle-free injectable presentations for biologics and vaccines in high-income markets is reinforcing disposable device revenue growth, as each pre-filled delivery unit constitutes a separate commercial transaction.

Application Insights

Vaccine delivery is the leading application segment in the needle-free injectors market, accounting for approximately 29% of global revenues in 2025. This leadership reflects the scale and universality of global immunization programs, with the WHO estimating over 2 billion vaccine doses administered annually, and the proven operational advantages of needle-free jet injectors in high-throughput mass vaccination settings. PharmaJet's Stratis system is the only WHO-prequalified needle-free injector, providing a first-mover market advantage in international procurement programs.

In addition, the development of intradermal needle-free delivery for influenza and rabies vaccines, which require lower antigen doses when delivered intradermally, is expanding the clinical application scope and improving dose economy for vaccine manufacturers, further reinforcing this segment's market-leading position.

End-user Insights

Hospitals and clinics represent the leading end-user segment in the needle-free injectors market, accounting for approximately 48% of revenues in 2026. Hospitals serve as primary administration sites for high-volume vaccine campaigns, biologics infusions, and insulin initiation protocols, making them the largest institutional consumers of needle-free injection systems.

The American Hospital Association (AHA) reports over 6,000 registered hospitals in the United States alone, each representing a potential procurement channel for needle-free systems, particularly as needlestick injury prevention programs expand under OSHA regulations. Hospital-based clinical trial sites and vaccination centers further amplify device utilization volumes, reinforcing the segment's revenue dominance across both developed and emerging markets.

Regional Insights

North America Needle-Free Injectors Market Trends and Insights

North America leads the global needle-free injectors market with approximately 38% revenue share in 2026 driven by strong FDA-supported innovation in drug delivery devices, the world's highest insulin-dependent diabetic population density, and proactive needlestick injury prevention legislation under OSHA's Needlestick Safety and Prevention Act. Growing adoption of needle-free platforms in dermatology and cosmetic clinics further diversifies the regional revenue base.

U.S. Needle-Free Injectors Market Size

The United States accounts for approximately 84% of North American needle-free injector revenues in 2026. With over 37 million Americans diagnosed with diabetes (American Diabetes Association) and a robust vaccine delivery infrastructure, the U.S. sustains the highest national demand for needle-free injector systems. Leading device companies, including Antares Pharma and Portal Instruments, are U.S.-headquartered.

Europe Needle-Free Injectors Market Trends and Insights

Europe is the second-largest needle-free injectors market, benefiting from strong public health investment in vaccination programs, rising diabetes prevalence, and harmonized EU MDR 2017/745 regulatory pathways for drug delivery devices. The region's emphasis on healthcare worker safety under EU Directive 2010/32/EU on sharps injuries prevention is reinforcing institutional demand for needle-free alternatives across hospital and clinic settings.

Germany Needle-Free Injectors Market Size

Germany represents approximately 22% of European needle-free injector revenues in 2026. Germany's strong statutory health insurance (GKV) system and high diabetes prevalence affecting over 7 million Germans per the German Diabetes Society (DDG) support robust insulin delivery device demand. Germany also hosts several medical device manufacturers advancing needle-free platform technology for European markets.

U.K. Needle-Free Injectors Market Size

The U.K. accounts for approximately 14% of European revenues in 2026. The NHS has explored needle-free vaccine delivery for national immunization programs, and MHRA-regulated pathways support device innovation. With over 4.3 million diabetic patients in the U.K. (Diabetes UK), insulin delivery applications represent a significant near-term commercial opportunity for needle-free injector manufacturers.

France Needle-Free Injectors Market Size

France contributes approximately 12% of European needle-free injector revenues in 2026. French public health authorities have promoted vaccination programs extensively, and the country's Haute Autorité de Santé (HAS) evaluates combination drug-device products for national reimbursement. Growing cosmetic and dermatology applications of needle-free systems, particularly for hyaluronic acid and mesotherapy delivery, are emerging as an incremental premium revenue stream in France.

Asia Pacific Needle-Free Injectors Market Trends and Insights

Asia Pacific is the fast-growing regional market for needle-free injectors, driven by the world's largest diabetes population in China and India, large-scale national immunization programs, and growing government investments in healthcare infrastructure. China, with over 140 million diabetic patients per IDF data, represents the single largest national addressable market for insulin delivery devices, including needle-free systems. China's NMPA is increasingly approving innovative drug delivery technologies to modernize the country's healthcare delivery capacity.

India Needle-Free Injectors Market Size

India's needle-free injectors market is valued at approximately US$ 6 million in 2026, growing rapidly, driven by its 77 million diabetic population (IDF), large-scale vaccine delivery programs under the Universal Immunization Programme (UIP), and India's position as a leading global vaccine manufacturer. The growing adoption of needle-free systems in private hospital networks is accelerating market penetration.

Competitive Landscape

The needle-free injectors market is characterized by strong competition driven by technological innovation, increasing demand for painless drug delivery, and rising focus on patient safety. Market participants are investing in advanced jet injection technologies, reusable injector systems, and smart drug delivery solutions to improve treatment efficiency and patient compliance. Companies are also expanding their product portfolios for vaccine administration, insulin delivery, and biologics applications. Strategic collaborations, regulatory approvals, and geographic expansion remain key competitive strategies across the industry.

Key Developments

- In December 2025, Intas Pharmaceuticals entered into an exclusive partnership with IntegriMedical to introduce India’s first needle-free injection system for IVF and gynaecology treatments. The collaboration aimed to deploy needle-free injector technology across IVF clinics and gynaecology centres nationwide to improve patient comfort and reduce injection-related pain, anxiety, and treatment fatigue.

- In October 2025, PharmaJet, Inc. announced the development of proprietary needle-free self-injection pens designed for home use and precise self-administration.

- In May 2024, Serum Institute of India acquired a 20% stake in IntegriMedical to boost needle-free vaccine delivery, aiming to expand access in emerging markets.

Global Needle-Free Injectors Market - Key Insights and Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 76.1 Million |

|

Current Market Value (2026) |

US$ 128.4 Million |

|

Projected Market Value (2033) |

US$ 245.5 Million |

|

CAGR (2026-2033) |

9.7% |

|

Leading Region |

North America, ~38% market share (2025) |

|

Dominant Injector Type |

Disposable, ~62% market share (2025) |

|

Top-Ranking Application |

Vaccine Delivery, ~29% market share (2025) |

|

Incremental Opportunity |

US$ 117.1 Million (2026-2033) |

Companies Covered in Needle-Free Injectors Market

- PharmaJet, Inc.

- Inovio Pharmaceuticals, Inc.

- NuGen Medical Devices Inc.

- Crossject SA

- Antares Pharma, Inc.

- Medical International Technology, Inc.

- National Medical Products Inc.

- PenJet Corporation

- Portal Instruments, Inc.

- Endo International plc

- Bioject Medical Technologies Inc.

- Valeritas Holdings, Inc.

- European Pharma Group

Frequently Asked Questions

The global needle-free injectors market is projected to be valued at US$ 128.4 million in 2026.

Increasing preference for painless and safer drug delivery methods, along with growing concerns regarding needle-stick injuries and cross-contamination, is further supporting market growth.

North America leads with approximately 38% share in 2026. The United States dominates regionally, accounting for ~84% of North American revenues, driven by over 37 million Americans with diabetes (American Diabetes Association), FDA-supported device innovation, OSHA needlestick prevention mandates, and headquarters of leading companies Antares Pharma and Portal Instruments.

The fast-growing opportunity is needle-free insulin delivery, with the IDF projecting 783 million diabetic patients by 2045 and documented needle phobia affecting 20–40% of insulin users. Pediatric and home care settings where needle anxiety affects up to 63% of children represent a large underpenetrated segment, as does the growing dermatology and cosmetic treatment application across premium private clinic markets.

The leading companies include PharmaJet, Inc. (WHO-prequalified Stratis vaccine delivery system), Antares Pharma, Inc. (XYOSTED, subcutaneous delivery platforms), Crossject SA (ZEPIZURE emergency injector), Portal Instruments, Inc. (AI-enabled precision injector), Inovio Pharmaceuticals, Bioject Medical Technologies, and NuGen Medical Devices.