- Pharmaceuticals

- Autoimmune Diseases Treatment Market

Autoimmune Diseases Treatment Market Size, Share and Growth Forecast, 2026-2033

Autoimmune Diseases Treatment Market by Drug Class (Biologics, Anti-Inflammatory, Immunosuppressants, Corticosteroids), Route of Administration (Injectables, Intravenous, Oral, Topical), Disease Indication (Rheumatic Diseases, Systemic Lupus Erythematosus (SLE), Multiple Sclerosis, Inflammatory Bowel Disease (IBD), Psoriasis), and Regional Analysis for 2026-2033

Autoimmune Diseases Treatment Market Share and Trends Analysis

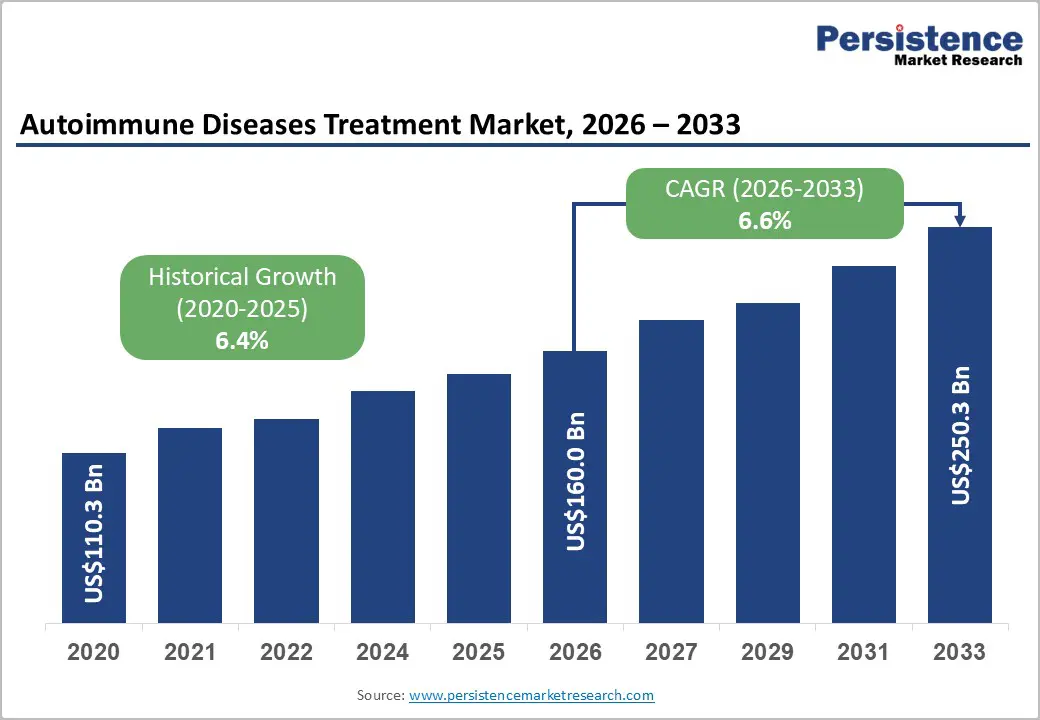

The global autoimmune diseases treatment market size is likely to be valued at US$ 160.0 billion in 2026, and is projected to reach US$ 250.3 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026–2033.

Market expansion is accelerating as the prevalence of chronic autoimmune disorders such as rheumatoid arthritis, psoriasis, inflammatory bowel disease, and multiple sclerosis is increasing worldwide. Improved disease awareness and earlier diagnosis are expanding the number of patients eligible for pharmacological intervention. Healthcare systems are integrating advanced biologic therapies into treatment guidelines, which is elevating average therapy costs and supporting revenue growth. Pharmaceutical companies are allocating sustained research and development (R&D) budgets toward precision immunotherapies that target specific inflammatory pathways.

As clinical data demonstrate improved efficacy and safety profiles, biologic adoption continues to strengthen across major markets. Regulatory agencies are approving new monoclonal antibodies and biosimilars, which is broadening therapeutic options and enhancing market accessibility. Biosimilar entry is improving affordability while preserving treatment penetration across cost-sensitive regions. Advances in diagnostics are enabling earlier identification of autoimmune markers, thereby increasing the addressable patient population.

Although pricing pressures and reimbursement scrutiny are persisting, manufacturers are differentiating through innovation, lifecycle management strategies, and geographic expansion into emerging healthcare markets.

Key Industry Highlights

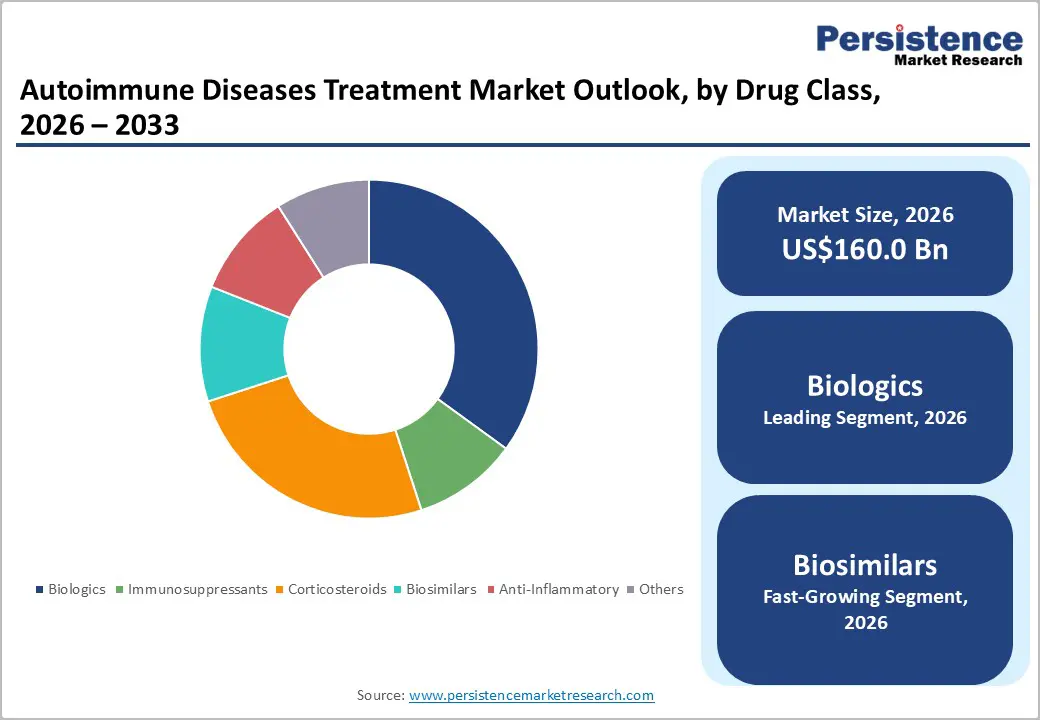

- Dominant Drug Classes: Biologics are projected to account for roughly 48% of revenue in 2026 due to their strong clinical efficacy, while biosimilars are expected to grow the fastest at an approximately 8% CAGR through 2033, driven by patent expiries and cost pressures.

- Leading Routes of Administration: Injectables are expected to lead with around 44% share in 2026, supported by dosing reliability, whereas oral therapies are forecast to grow the fastest at approximately 7.5% CAGR through 2033 due to convenience and innovation.

- Dominant Disease Indication: Rheumatic diseases are set to account for nearly 38% revenue share in 2026, owing to high prevalence and chronic treatment needs.

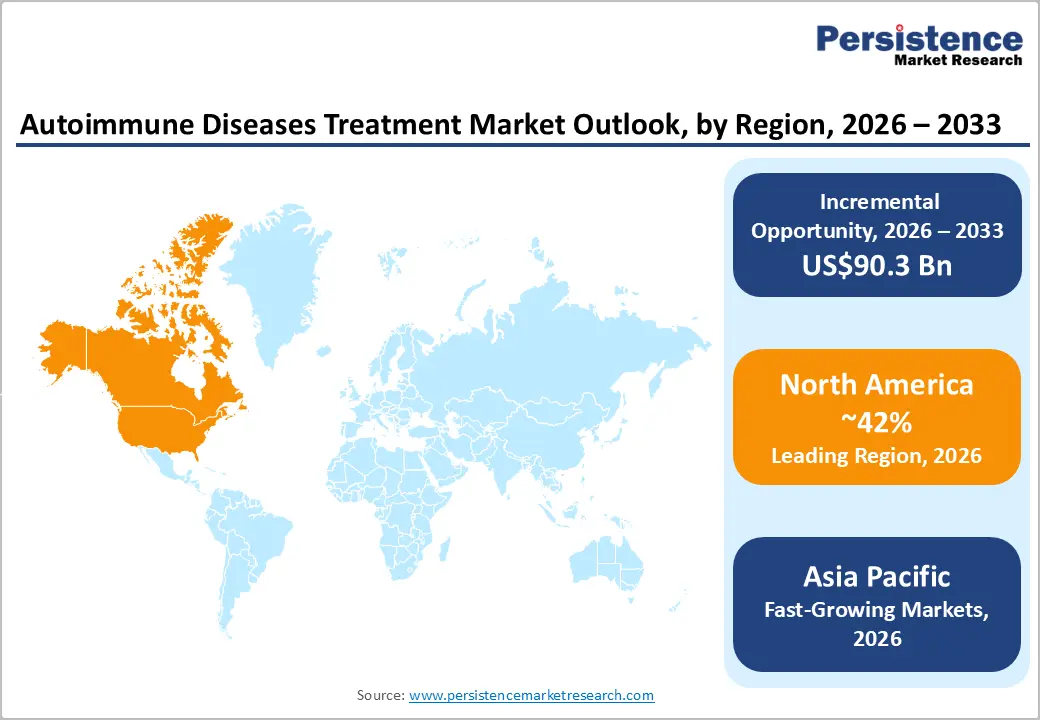

- Regional Dynamics: North America is projected to hold an estimated 42% market share in 2026, aided by supportive reimbursement policies, while Asia Pacific is expected to be the fastest-growing market at 8.2% CAGR through 2033, backed by large underserved patient pools.

- Competitive Environment: Market dynamics are increasingly shaped by biosimilars and precision medicine, with leading players focusing on affordability, lifecycle management, and expansion into high-growth emerging economies.

| Global Market Attributes | Key Insights |

|---|---|

| Autoimmune Diseases Treatment Market Size (2026E) | US$ 160.0 Bn |

| Market Value Forecast (2033F) | US$ 250.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Structural Expansion of the Global Autoimmune Diseases Treatment Market

The growth of the autoimmune disease treatment market is fundamentally driven by the increasing burden of chronic autoimmune conditions worldwide. According to data from the U.S. National Institutes of Health (NIH) and the World Health Organization (WHO), autoimmune diseases affect 8–10% of the population, with incidence rising annually due to aging demographics, environmental exposures, and improved diagnostic methods.

Rheumatoid arthritis impacts over 18 million patients, while the prevalence of inflammatory bowel disease has increased by more than 30% in emerging economies since 2015. These diseases are lifelong and progressive, requiring continuous pharmacological management that sustains long-term demand for both biologic and non-biologic therapies.

Market growth is further reinforced by advances in therapeutics, diagnostics, and healthcare access. TNF inhibitors, IL-17 inhibitors, and monoclonal antibodies account for over 45% of treatment revenues, supported by strong clinical outcomes and improved safety profiles. Between 2018 and 2024, more than 25 autoimmune biologics received regulatory approvals, enabling greater treatment personalization. At the same time, improved diagnostic capabilities, expanding insurance coverage, and broader healthcare access, particularly in Asia Pacific and other high-growth regions, are increasing treatment penetration.

Supportive reimbursement policies, including expanded biologics coverage in developed markets and biosimilar adoption in Europe, are improving affordability while sustaining innovation, collectively driving steady market expansion.

Cost, Regulatory, and Clinical Complexity Constraints on Market Expansion

Market expansion is constrained by high therapy costs and access barriers that reduce uptake and affordability. Many biologic therapies carry substantial annual costs; for some biologics, the list price can range from tens of thousands to over US$ 70,000 per patient per year, significantly outpacing traditional therapies such as methotrexate or corticosteroids. Price variability also persists across regions and brands; for example, cost disparities among biologic agents such as etanercept and infliximab are pronounced in the Indian market, with brand price ratios exceeding 4:1 for certain formulations, making consistent pricing and access difficult.

These financial pressures are compounded by stringent regulatory requirements and clinical complexity that slow innovation and adoption. Biologic and targeted therapy development typically spans 7–10 years from discovery to approval, driven by the need for extensive long-term safety and efficacy data given the risks of immune modulation. In clinical practice, variability in patient response further complicates utilization; analyses show that only 28–32% of patients treated with commonly used biologics such as etanercept or adalimumab achieve effective outcomes in the first year, reinforcing the need for therapy switching and ongoing clinical management.

Moreover, many treatment classes carry safety concerns, such as increased infection risk or immunosuppression-associated adverse events, necessitating cautious prescribing and monitoring. These cost, regulatory, and clinical barriers limit formulary access, slow market penetration in price-sensitive regions, and constrain broader adoption despite significant unmet need.

Innovation, Access Expansion, and Emerging Therapeutic Pathways

Significant opportunities exist for market players to broaden treatment access and advance therapeutic innovation. The expansion of biosimilars continues to reduce costs and improve accessibility, particularly in the Asia-Pacific and Latin America, where treatment penetration remains low despite large patient populations. New biosimilars such as tocilizumab-based agents have received regulatory approvals, expanding affordable treatment options across multiple indications.

Telemedicine, mobile health applications, and remote monitoring tools are increasingly integrated into disease management, helping patients adhere to long-term therapy and enabling clinicians to adjust treatment based on real-time data.

In addition to access innovations, cutting-edge research and novel therapeutic technologies are creating high-value growth avenues. For example, immunology collaborations such as Lilly’s partnership with Repertoire Immune Medicines aim to develop therapies that restore immune function without broad suppression, reflecting a shift toward precision immune modulation. Advancements such as AI-enabled drug discovery and immune cell analysis platforms, for instance, the Adaptive Biotechnologies-Pfizer collaboration, demonstrate how digital and biotech integration can accelerate the development of new treatments and diagnostics.

Furthermore, approvals of novel agents, such as inebilizumab, for rare autoimmune conditions indicate opportunities in unmet and specialty segments. These trends highlight opportunity vectors from cost optimization and access expansion to precision therapies and digital health integration, positioning the market for diversified and sustained growth.

Category-wise Analysis

Drug Class Insights

Biologics are estimated to be the leading drug class, set to contribute approximately 48% to the autoimmune diseases treatment market revenues in 2026, driven by superior clinical outcomes and broad indication coverage. TNF inhibitors and monoclonal antibodies are projected to dominate autoimmune treatment patterns in rheumatoid arthritis, psoriasis, and inflammatory bowel disease (IBD) due to established efficacy and long-term safety. Regulatory approvals, including inebilizumab for generalized myasthenia gravis and IgG4-related disease, are expected to expand clinical indications.

Physician preference for these targeted biologics is likely to maintain high utilization across chronic disease management. Hospital and outpatient channels are anticipated to continue driving revenue. Biologics are projected to remain the largest revenue-generating class throughout the forecast period.

Immunosuppressants and biologic biosimilars are estimated to be the fastest-growing drug classes with a CAGR of 8% through 2033. Growth is expected to be supported by cost-conscious payer strategies and increasing regulatory approvals in emerging and developed markets. New biosimilars, including ustekinumab alternatives for active ulcerative colitis and Crohn's disease, are expected to enhance adoption in cost-sensitive regions. These treatments are projected to enable earlier therapy initiation and continuity of care. The expansion of biosimilars and immunosuppressants is expected to significantly shape future market dynamics while providing cost-effective options for patients.

Route of Administration Insights

Injectables, particularly subcutaneous formulations, are projected to be the leading administration route with an estimated 44% of the autoimmune disease treatment market share in 2026. Physician preference is expected to remain strong due to controlled dosing, predictable pharmacokinetics, and improved patient adherence. Intravenous therapies are likely to continue to play a key role in hospital settings in the management of severe autoimmune conditions. Recent industry developments, including Boehringer Ingelheim’s collaboration with Simcere Pharma to develop an IBD candidate, are expected to reinforce investment in injectable biologics.

Controlled administration and clinical reliability are projected to sustain injectables as the primary revenue contributor in this segment.

Oral therapies are projected to be the fastest-growing route of administration with a CAGR exceeding 7.5%. Growth is expected to be driven by patient convenience, adherence benefits, and innovation in small-molecule and peptide therapies. Johnson & Johnson submitted an NDA for icotrokinra, a once-daily oral peptide targeting IL-23 receptor pathways, which may expand oral treatment options for autoimmune diseases such as plaque psoriasis. Oral therapies are likely to facilitate at-home disease management, reduce hospital visits, and enhance long-term compliance. These trends are expected to make oral therapies a key growth opportunity in the administration route segment.

Disease Indication Insights

Rheumatic diseases are anticipated to dominate with a market share exceeding 38% in 2026, reflecting high prevalence of these diseases, chronic progression, and long-term treatment requirements. Rheumatoid arthritis is expected to continue as the primary revenue contributor. Regulatory and clinical developments in 2025 are projected to reinforce the focus on rheumatic indications, supporting ongoing innovation and competitive positioning. Early intervention strategies and optimized treatment protocols are likely to maintain consistent revenue generation. Rheumatic diseases are projected to remain the leading indication throughout the forecast period.

IBD is likely to be the fastest-growing indication with a CAGR exceeding 7.5% through 2033. Segmental growth is expected to be driven by biologic innovation, expanding diagnosis rates, and updated treatment guidelines emphasizing early intervention. Positive Phase 2 clinical results for a novel oral therapy for ulcerative colitis demonstrated significant efficacy compared with placebo, supporting the adoption of next-generation treatments. Increasing focus on both pediatric and adult IBD management is expected to further expand treatment uptake. These trends indicate that IBD will be a high-growth segment and a key opportunity for market participants.

Regional Insights

North America Autoimmune Diseases Treatment Market Trends

North America is estimated to account for approximately 42% of total autoimmune diseases treatment market value in 2026, supported by advanced healthcare infrastructure and high biologics utilization. In the United States, ongoing industry investments are expanding therapeutic options. For example, the U.S. Food and Drug Administration (FDA) approved inebilizumab as the first treatment for IgG4-related disease, expanding indications for autoimmune therapies and reinforcing biologics leadership. Growing FDA approvals of novel therapies improve treatment access across indications such as neuromyelitis optica and generalized myasthenia gravis.

Strong payer frameworks continue to support long-term use of biologics, maintaining high adoption rates. Specialty care networks and hospital systems further enhance distribution efficiency, ensuring timely patient access to advanced therapies.

The region’s innovation ecosystem is further supported by strategic partnerships and investment initiatives. In January 2026, Eli Lilly entered a major collaboration to develop next-generation autoimmune therapies, indicating sustained R&D momentum in the U.S. market. Venture capital and biotech collaborations also accelerate pipeline expansion and translational research. Consistent reimbursement structures facilitate early adoption of advanced treatments, while physician confidence in targeted biologics continues to drive prescribing.

North America’s role as a clinical development hub positions it for continued market leadership through the forecast period. Ongoing patient awareness programs and post-market surveillance initiatives are expected to further strengthen adoption.

Europe Autoimmune Diseases Treatment Market Trends

Europe is home to robust and highly efficient healthcare systems and coordinated regulatory frameworks that support consistent growth in autoimmune treatments. The European Medicines Agency's (EMA) centralized review process standardizes therapeutic approvals and facilitates cross-border access to innovative therapies. For example, regulatory recommendations in late 2025 extended indications for existing treatments, broadening clinical use across multiple autoimmune conditions.

National health systems in major markets actively promote biosimilar adoption to manage costs without compromising treatment quality. Physician familiarity with biologics and targeted therapies ensures steady adoption across key indications. Comprehensive insurance coverage further enhances patient access, while investments in advanced diagnostics strengthen treatment uptake through earlier disease detection.

Investment activity in Europe reflects a continued focus on innovation and access. Sanofi entered a strategic collaboration with Dren Bio to develop autoimmune therapies, including targeted B-cell depletion treatments, underscoring its commitment to next-generation immunotherapies. These partnerships support pipeline expansion and enable access to differentiated therapies. Pricing negotiations and reimbursement policies maintain cost-effective access to both originator biologics and biosimilars.

Ongoing regulatory harmonization ensures timely approvals, while advanced clinical programs and specialty care networks improve patient reach. These factors contribute to a stable, innovation-driven environment that supports the continued growth of autoimmune disease treatments across the region.

Asia Pacific Autoimmune Diseases Treatment Market Trends

Asia Pacific is projected to be the fastest-growing regional market for autoimmune disease treatments between 2026 and 2033, driven by expanding healthcare access, rising disease awareness, and growing domestic pharmaceutical capabilities. China, Japan, and India are expected to lead regional growth, with regulatory systems increasingly supporting new therapy introductions. China’s National Medical Products Administration approved ebdarokimab for the treatment of moderate-to-severe plaque psoriasis, marking a notable advancement in the availability of autoimmune treatments in the region.

Such approvals increase patient access to advanced therapies and support broader market adoption. Awareness campaigns, improving diagnostic infrastructure, and patient education initiatives further enhance uptake. Expansion of hospital networks and specialty clinics strengthens regional distribution capabilities.

The regional market's growth outlook is brightened by strategic expansion and technological development. For instance, Singapore-based Nanyang Biologics announced plans to list on the Nasdaq, underscoring rising investor confidence and market potential in Asia-Pacific biotech innovation. Moreover, Japan's regulatory environment continues to support new immunology platforms, with multiple licensing and development collaborations bringing advanced therapies into routine clinical practice.

Government healthcare incentives and domestic production capacity expansion improve affordability. These factors, combined with large, untreated patient populations, position the Asia Pacific as a high-growth market. Adoption of innovative therapies and investment in local research are expected to sustain accelerated revenue growth.

Competitive Landscape

The global autoimmune diseases treatment market structure is moderately consolidated, with leading players including AbbVie, Johnson & Johnson, Roche, Pfizer, and Novartis collectively controlling over half of the revenue share in 2026. These established companies leverage extensive clinical trial experience, strong physician networks, and global distribution channels. They continue to invest heavily in R&D for next-generation biologics, biosimilars, and targeted immunotherapies, maintaining leadership in treatment innovation. Strategic pipelines focus on advanced modalities such as monoclonal antibodies, IL-17 and IL-23 inhibitors, and small-molecule oral therapies, supported by robust safety and efficacy data across multiple autoimmune indications.

On the other hand, regional and niche competitors, including Samsung Bioepis, Dr. Reddy’s Laboratories, and Celltrion, are focusing on biosimilars, specialty autoimmune segments, and emerging markets. High regulatory standards, long clinical development timelines, and capital-intensive manufacturing act as entry barriers, limiting the participation of new entrants. However, digital health platforms, telemedicine, and AI-driven clinical monitoring are enabling innovative companies to support therapy adherence and remote disease management. Market consolidation is expected to increase gradually as major players acquire smaller biotech firms, enter licensing agreements, or form R&D collaborations to expand their therapeutic portfolios and geographic reach.

Key Industry Developments

- In February 2026, Biogen’s investigational antibody litifilimab received Breakthrough Therapy designation from the U.S. FDA for the treatment of SLE, recognizing early clinical evidence suggesting substantial improvement over existing therapies. The designation will accelerate development and regulatory review, positioning litifilimab to potentially become a novel targeted therapy if ongoing trials confirm safety and efficacy.

- In January 2026, Novartis announced that the U.S. FDA granted Breakthrough Therapy designation to its investigational monoclonal antibody ianalumab for the treatment of Sjögren’s disease, a serious autoimmune disorder. The designation is intended to accelerate development and regulatory review, and, if approved, ianalumab would become the first targeted treatment for this condition.

- In January 2026, Boehringer Ingelheim licensed SIM0709, a pre-clinical bispecific antibody targeting TL1A and IL-23 pathways, from China’s Simcere Pharmaceutical Group, with potential milestone payments exceeding €1 billion. The agreement grants Boehringer global rights and strengthens its inflammatory bowel disease pipeline by advancing a novel therapeutic designed to address unmet needs in IBD treatment.

Companies Covered in Autoimmune Diseases Treatment Market

- AbbVie Inc.

- Pfizer Inc.

- Johnson & Johnson

- Roche Holding AG

- Novartis AG

- Amgen Inc.

- Bristol Myers Squibb

- Sanofi

- Eli Lilly and Company

- Merck & Co., Inc.

- Biogen Inc.

- UCB Pharma

Frequently Asked Questions

The global autoimmune diseases treatment market is projected to reach US$ 160.0 billion in 2026.

The rising prevalence of autoimmune disorders, technological advances in biologics and targeted therapies, and favorable regulatory and reimbursement frameworks are the primary growth drivers.

The market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Expansion of biosimilars in cost-sensitive markets, untapped patient pools in emerging regions, and advancements in precision medicine and combination therapies represent significant growth opportunities.

Leading players include AbbVie, Johnson & Johnson, Roche, Pfizer, Novartis, Samsung Bioepis, Dr. Reddy’s Laboratories, and Celltrion, among others.