- Medical Devices

- Vaccine Delivery Devices Market

Vaccine Delivery Devices Market Size, Share, and Growth Forecast 2026 - 2033

Vaccine Delivery Devices Market by Device (Syringes, Jet Injectors, Others), by Route of Administration (Intradermal, Intramuscular, Subcutaneous, Others), by End-user (Hospitals, Clinics/Ambulatory Care Centers, Vaccination Centers, Homecare/Self-Administration Settings, Others), by Regional Analysis, 2026 - 2033

Vaccine Delivery Devices Market Share and Trends Analysis

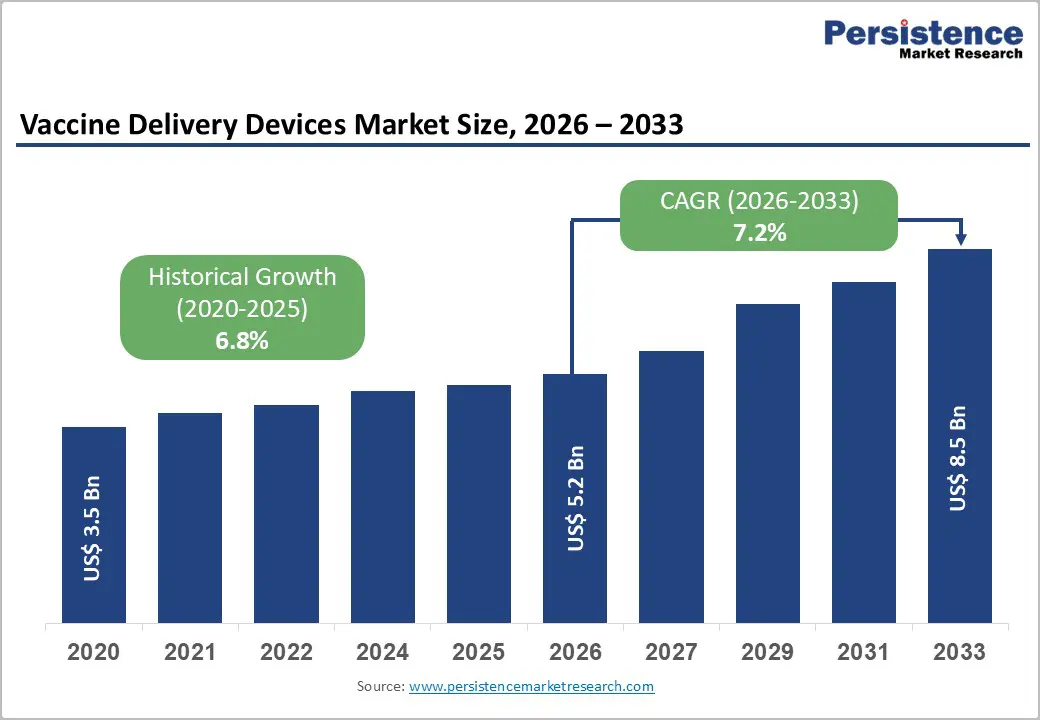

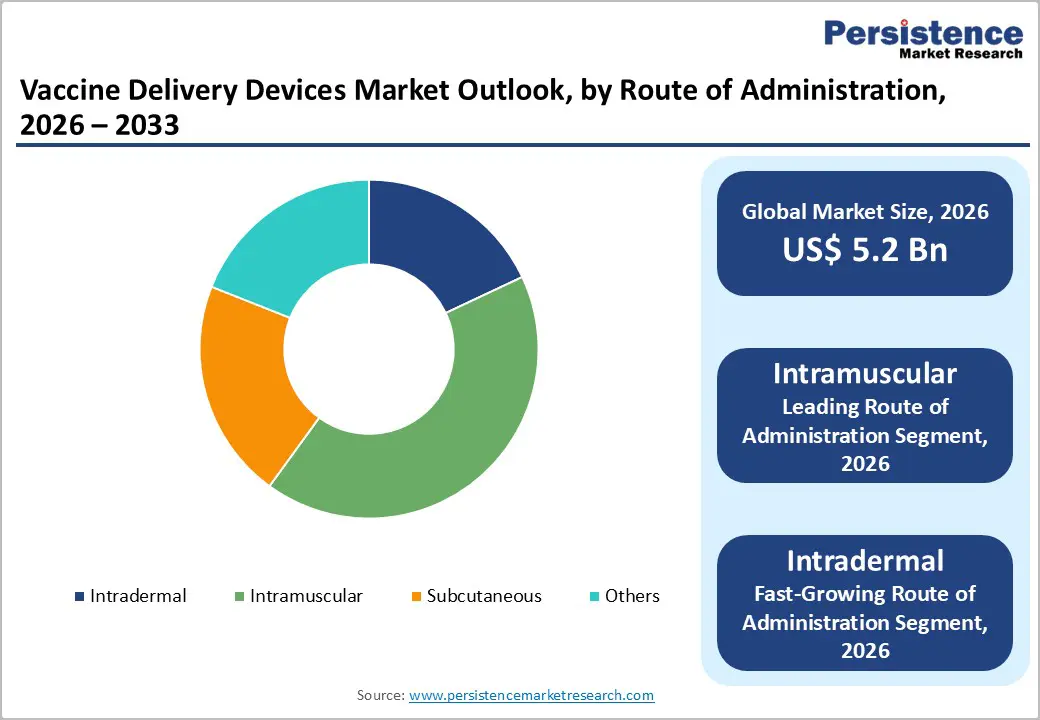

The global vaccine delivery devices market size is expected to be valued at US$ 5.2 billion in 2026 and projected to reach US$ 8.5 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

The vaccine delivery devices market is experiencing robust growth driven by rise in global immunization initiatives and technological innovations in administration mechanisms. The increasing prevalence of vaccine-preventable diseases, coupled with government-led vaccination programs and expanding healthcare infrastructure in developing regions, significantly propels market expansion. Advanced delivery technologies, including needle-free injection systems, prefilled syringes, and auto-disable syringes are gaining substantial market traction due to their superior safety profiles, reduced needle-stick injury risks, and improved patient compliance. The World Health Organization (WHO)s emphasis on safe injection practices and cold chain management has further accelerated the adoption of modern vaccine delivery solutions across healthcare facilities globally.

Key Industry Highlights:

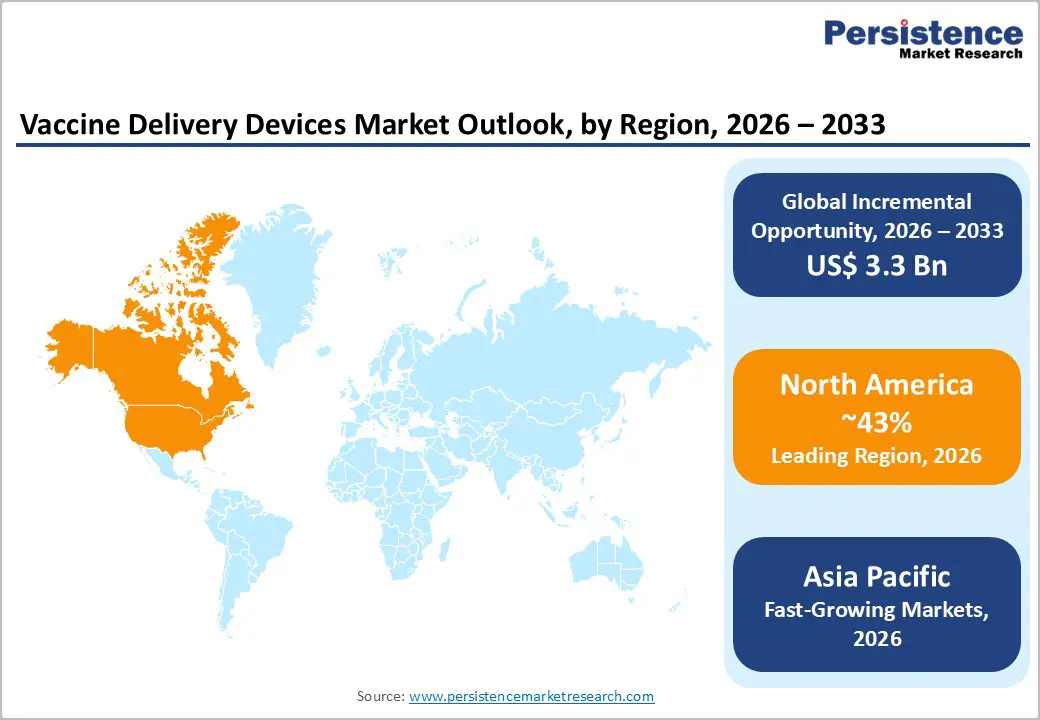

- North America leads the vaccine delivery devices market with ~43% share in 2025, supported by advanced healthcare infrastructure, strict safety regulations, strong pharmaceutical manufacturing, and sustained government investment in immunization programs.

- Asia Pacific is the fastest-growing region, registering over 8.2% CAGR through 2032, driven by large populations, rising healthcare spending, expanding local vaccine production, and improving cold-chain infrastructure.

- Syringes remain the dominant device type with ~64% market share in 2025, while jet injectors are the fastest-growing segment, supported by enhanced safety, needle-free delivery, and higher patient acceptance.

| Global Market Attributes | Key Insights |

|---|---|

| Vaccine Delivery Devices Market Size (2026E) | US$ 5.2 billion |

| Market Value Forecast (2033F) | US$ 8.5 billion |

| Projected Growth CAGR (2026-2033) | 7.2% |

| Historical Market Growth (2020-2025) | 6.8% |

Market Dynamics

Drivers - Rising Global Immunization Campaigns and Disease Prevention Initiatives

Worldwide vaccination programs have expanded significantly, driven by increasing awareness of preventable diseases and government healthcare initiatives. The WHO and GAVI (Global Alliance for Vaccines and Immunization) have intensified vaccination efforts against infectious diseases including influenza, polio, and hepatitis. Approximately 16 billion injections are administered annually globally for immunization, with demand expected to surge further. Developing nations in Asia Pacific and Latin America are witnessing exponential increases in vaccination coverage, particularly following the COVID-19 pandemic, which demonstrated the critical importance of rapid, efficient vaccine distribution systems. Governments are increasingly investing in immunization infrastructure, creating substantial demand for reliable, user-friendly vaccine delivery devices that enhance healthcare worker productivity and patient safety.

Technological Innovations in Advanced Delivery Systems

Innovation in vaccine delivery technology represents a transformative growth driver reshaping market dynamics. Needle-free jet injectors, microneedle patches, and prefilled syringe systems have demonstrated superior clinical outcomes compared to traditional needle-and-syringe administration. PharmaJet Inc.'s Stratis needle-free jet injector received FDA approval in 2024 for the AFLURIA influenza vaccine, marking the first FDA-approved needle-free delivery system for inactivated influenza vaccination. These technological advances improve vaccine efficacy, enhance patient acceptability, and reduce healthcare costs through dose-sparing capabilities.

Restraints - Cold Chain Infrastructure Limitations in Resource-Constrained Settings

Maintaining strict cold chain management remains a significant market restraint, particularly in developing regions with inadequate refrigeration infrastructure. WHO guidelines require vaccines to be maintained at 2°C to 8°C throughout storage and distribution, with freezing or heat exposure causing permanent vaccine potency loss. Limited access to digital data loggers and automated temperature monitoring systems creates blind spots in the supply chain, potentially rendering millions of doses ineffective. Addressing infrastructure deficiencies requires substantial capital investment that many developing nations struggle to allocate, thereby constraining market growth in resource-limited environments.

High Capital and Regulatory Compliance Costs for Device Manufacturers

Regulatory requirements for vaccine delivery devices impose substantial financial burdens on manufacturers, particularly during product development and market approval processes. FDA, EMA (European Medicines Agency), and WHO prequalification pathways demand extensive clinical trial data, quality control documentation, and manufacturing facility validation. Development of novel delivery systems requires investment of US$ 20-50 million for clinical validation and regulatory approval. Small and medium-sized enterprises struggle to afford these expenditures, limiting market competition and innovation. Additionally, post-market surveillance requirements, ongoing quality monitoring, and compliance with evolving international standards ISO 13320 and ISO 11040 series create ongoing operational costs. Manufacturers must also maintain separate production facilities for different regulatory jurisdictions, further escalating expenses and reducing profitability margins across emerging markets.

Opportunities - Rapid Adoption of Needle-Free Technology and Self-Administration Capabilities

Needle-free injection systems represent the fastest-growing market segment with exceptional expansion potential. The intradermal delivery route, administered via needle-free jet injectors, is experiencing CAGR of 8.5% to 9.8% during the 2025-2032 forecast period, significantly outpacing traditional syringes. PharmaJet's Tropis system, the first needle-free technology achieving WHO prequalification, has successfully administered polio vaccines to over 10 million children in developing nations. Patient preference studies demonstrate overwhelming acceptance of self-administered needle-free systems, particularly in developed markets where needle phobia affects approximately 10% of the population. The self-administration capability unlocks opportunities in homecare settings, workplace vaccination programs, and mass vaccination campaigns, enabling decentralized immunization delivery that bypasses traditional healthcare facility constraints.

Category-wise Analysis

Device Insights

Syringes represent the leading device segment, commanding approximately 64% market share in 2025. Traditional glass and plastic syringes remain the dominant delivery mechanism due to their universal compatibility, cost-effectiveness, and established regulatory frameworks. Modern syringe innovations including prefilled syringes with integrated safety features address growing healthcare system requirements for injection safety and product stability. Auto-disable syringes, which prevent reuse through mechanical locking mechanisms, have become standard in immunization programs following WHO recommendations to eliminate bloodborne pathogen transmission through needle reuse. Studies demonstrate that auto-disable syringes have prevented transmission of HIV and Hepatitis B in millions of vaccination procedures. Major manufacturers including Becton Dickinson & Company, Gerresheimer AG, and SCHOTT AG dominate the syringe market through continuous product refinement.

Route of Administration Insights

Intramuscular delivery commands the leading market position with 42% market share in 2025, as most licensed vaccines worldwide are administered intramuscularly into the deltoid muscle. This route has been extensively validated across decades of clinical practice, providing predictable immunogenic responses and broad applicability across diverse vaccine formulations.

Intramuscular vaccination remains the standard recommendation by CDC (Centers for Disease Control and Prevention) and WHO for routine immunization programs. The intradermal route leverages the skin's abundant antigen-presenting cells and Langerhans cell populations, facilitating superior immunological priming. PharmaJet's Tropis needle-free intradermal system demonstrates particular promise, particularly for vaccines including polio and tuberculosis where precision placement is critical. Healthcare systems increasingly recognize intradermal delivery's potential to stretch vaccine supplies during supply constraints and pandemics, driving accelerated adoption of specialized delivery devices capable of consistent intradermal placement.

End-user Insights

Hospitals and ambulatory care centers represent the largest end-user segment, accounting for approximately 58% market share in 2025. These healthcare facilities conduct routine immunizations for pediatric, adult, and travel-related vaccinations, requiring high-volume, reliable vaccine delivery systems. Dedicated vaccination centers, operated by public health agencies and private healthcare providers, prioritize operational efficiency and patient safety through advanced delivery device adoption.

These facilities increasingly implement needle-free injection systems to reduce healthcare worker injury rates and enhance patient satisfaction. Homecare and self-administration settings represent an emerging opportunity, driven by patient preference for convenient home-based healthcare delivery. COVID-19 pandemic experiences demonstrated feasibility of home vaccination programs, encouraging government and private initiatives to expand at-home immunization options. Development of patient-friendly, self-administered vaccine delivery devices positions this segment as the fastest-growing end-user category through 2033, particularly in developed markets with established home healthcare infrastructure.

Regional Insights

North America Vaccine Delivery Devices Market Trends and Insights

North America maintains dominant market leadership with 43 % global market share in 2025, driven by robust healthcare infrastructure, stringent regulatory frameworks, and advanced manufacturing capabilities. The United States leads regional market development through FDA approval of innovative technologies including PharmaJet's needle-free jet injector for influenza vaccination, which received clearance enabling AFLURIA vaccine administration without needles. Healthcare worker needlestick injury prevention drives substantial device adoption, as occupational safety regulations mandate implementation of safety-engineered devices. Studies indicate approximately 3.62 needlestick injuries per 100,000 vaccinations among healthcare workers in developed markets, creating regulatory pressure for needle-free alternatives.

Asia Pacific Vaccine Delivery Devices Market Trends and Insights

Asia Pacific represents the fastest-growing regional market with projected CAGR exceeding 8.2 % through 2032, driven by massive populations, expanding healthcare coverage, and indigenous pharmaceutical manufacturing growth. India dominates regional vaccine production, supplying approximately 87% of vaccines procured across the WHO South-East Asia Region, creating substantial demand for modern delivery devices compatible with high-volume immunization programs. Indigenous manufacturers, including Bharat Biotech International Limited, Serum Institute of India, and Indian Immunologicals Ltd, increasingly integrate advanced delivery systems into manufacturing operations to enhance vaccine efficacy and market competitiveness.

Competitive Landscape

The vaccine delivery devices market is highly competitive and volume driven, characterized by strong price competition, large-scale manufacturing capabilities, and long-term supply contracts with governments and global health agencies. Market participants focus on cost efficiency, regulatory compliance, safety-engineered designs, and high-capacity production to secure institutional tenders. Innovation is increasingly centered on needle-free systems, intradermal delivery, and dose-sparing technologies to improve patient compliance and reduce needlestick injuries.

Key Developments:

- In January 2026, AptarGroup, Inc., global leader in drug delivery and consumer product dosing, dispensing, and protection technologies, announced that its innovative nasal vaccine delivery solutions, LuerVax® and Spray Divider™, were utilized in CastleVax’s Phase II clinical trial of CVAX-01, a next-generation intranasal COVID-19 vaccine candidate.

Companies Covered in Vaccine Delivery Devices Market

- Becton Dickinson & Company

- Bioject Medical Technologies, Inc.

- Inovio Pharmaceutical Inc.

- PharmaJet

- Vaxxas

- Gerresheimer AG

- SCHOTT AG

- Corium International, Inc.

- 3M

Frequently Asked Questions

The global vaccine delivery devices market is expected to be valued at US$ 5.2 billion in 2026.

Rising global immunization campaigns supported by WHO and GAVI initiatives, increasing prevalence of vaccine-preventable diseases, government-led vaccination program expansions, and technological innovations in advanced delivery systems including needle-free jet injectors, prefilled syringes, and microneedle patches represent the primary growth drivers accelerating vaccine delivery devices market expansion worldwide.

North America maintains dominant regional market leadership with approximately 43% global market share in 2025, driven by advanced healthcare infrastructure, stringent regulatory frameworks enforced by the FDA, established pharmaceutical manufacturing capabilities, substantial government immunization program investments, and widespread adoption of safety-engineered vaccine delivery devices.

Needle-free jet injection technology and self-administered vaccine delivery systems represent the fastest-growing market opportunities, with intradermal delivery routes experiencing, propelled by dose-sparing capabilities, WHO prequalification achievements for systems like PharmaJet's Tropis, clinical evidence of superior immune responses, and rising patient preference for painless vaccination alternatives.

Major market players include Becton Dickinson & Company, Bioject Medical Technologies, Inc., Inovio Pharmaceutical Inc.,etc.