- Medical Devices

- Huber Needles Market

Huber Needles Market Size, Share, and Growth Forecast, 2025 - 2032

Huber Needles Market By Product Type (Straight Huber Needles, Curved Huber Needles), Application (Dialysis, Blood Transfusions, IV Cancer Treatment, Home Parenteral Nutrition, Others), End-user, and Regional Analysis from 2025 - 2032

Huber Needles Market Size and Trends Analysis

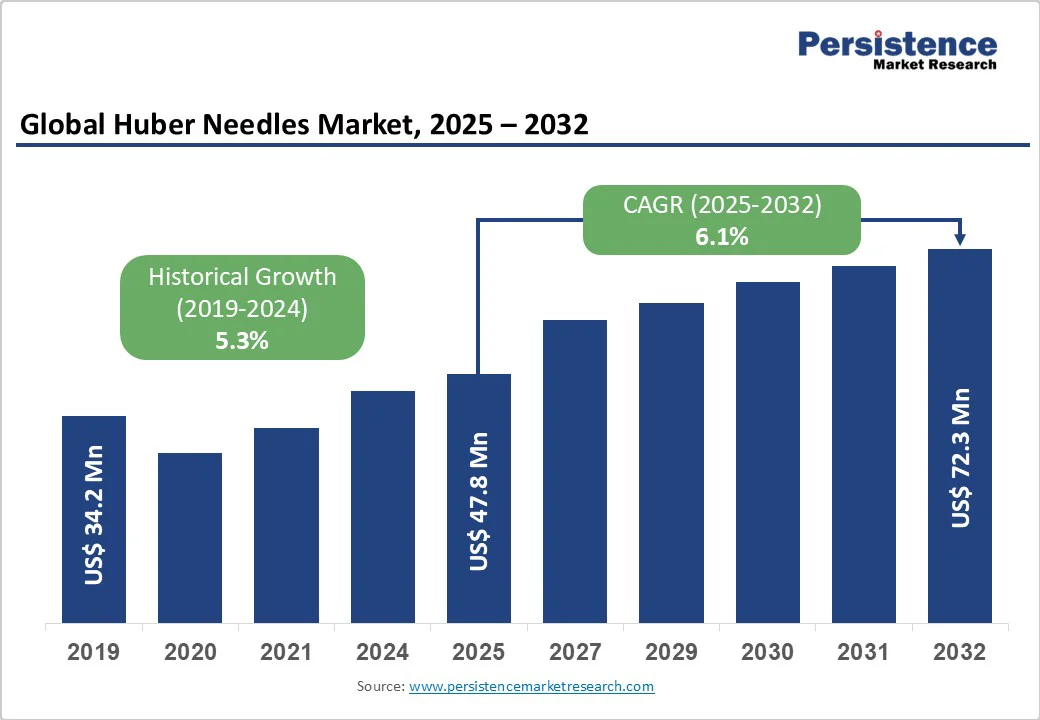

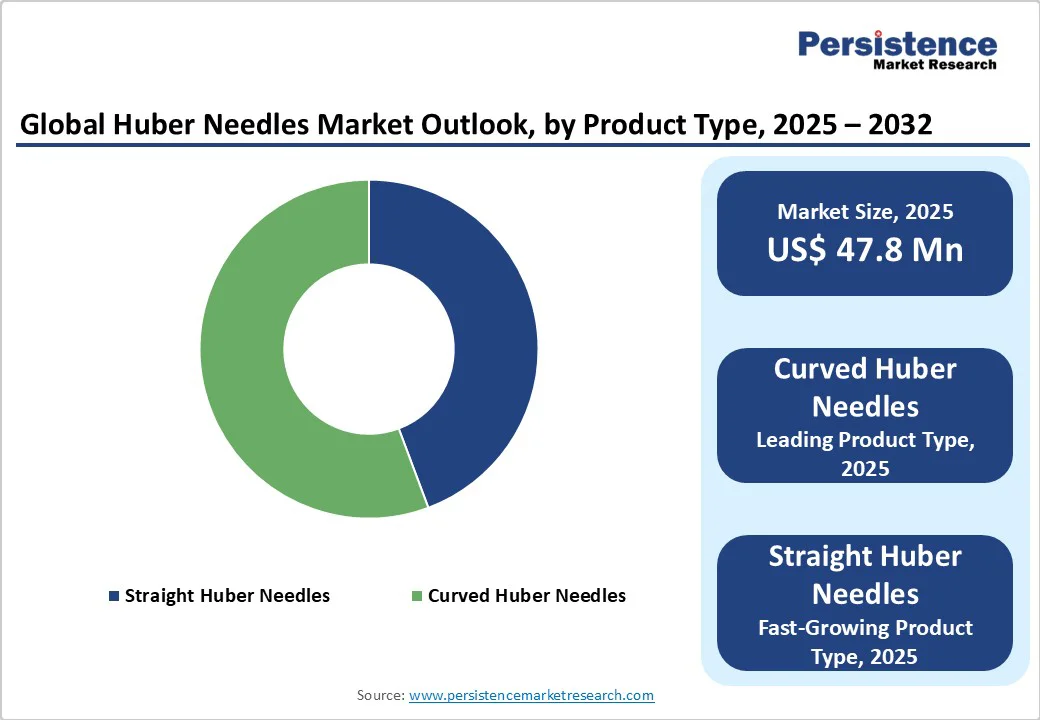

The global Huber needles market size is likely to be valued at US$47.8 Million in 2025 and is expected to reach US$72.3 Million by 2032, growing at a CAGR of 6.1% during the forecast period from 2025 to 2032, driven by the increasing prevalence of chronic diseases requiring long-term intravenous therapies, the expansion of hospitals and outpatient care centers, and growing adoption of minimally invasive infusion techniques. Advancements in needle design, stricter safety regulations, and expanding healthcare infrastructure in developing regions are further driving the market growth.

Key Industry Highlights

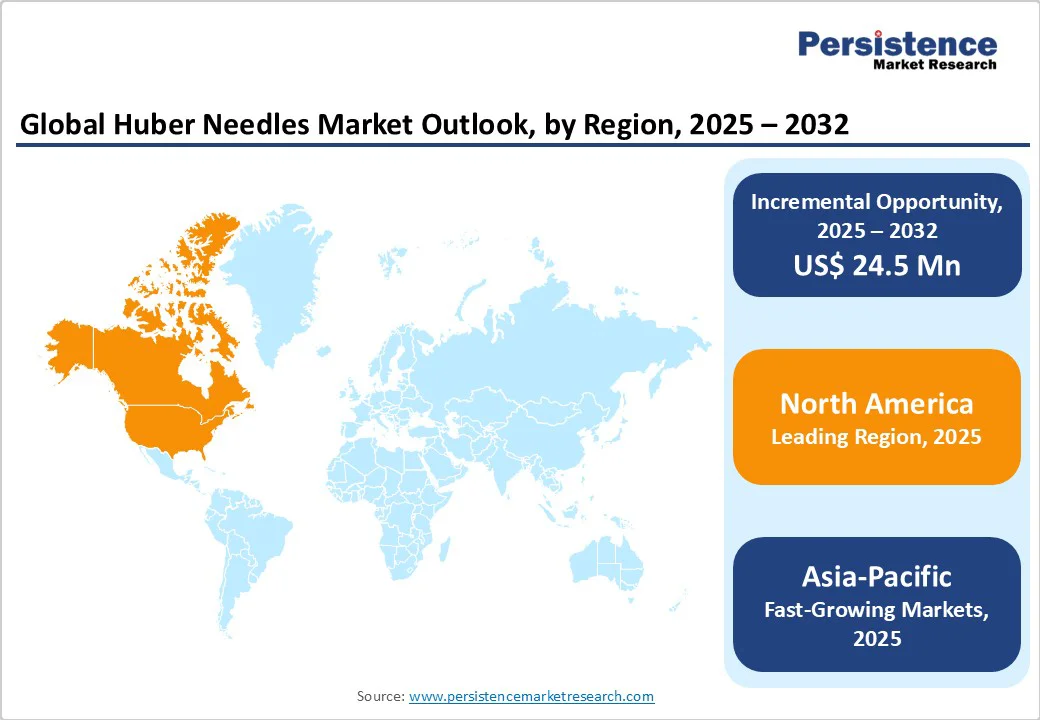

- Leading Region: North America dominates the market with a revenue share of 42.2% in 2024, driven by a strong presence of the biopharmaceutical and medical device industries, high healthcare spending, and stringent regulatory standards.

- Fastest-growing Region: Asia Pacific is the fastest-growing market for Huber needles with a revenue share of 20.1% in 2024, driven by the rising prevalence of chronic diseases requiring long-term intravenous therapies, increasing adoption of home healthcare and outpatient infusion services, and expansion of hospital networks and specialty infusion centers.

- Fastest-growing Application Segment: Home parenteral nutrition is the fastest-growing segment, driven by increasing prevalence of chronic diseases such as cancer, Crohn’s disease, and gastrointestinal disorders, and the expanding availability of safe, easy-to-use Huber needle systems that enable comfortable and effective home administration of parenteral nutrition and other intravenous therapies.

- Market Drivers: Increasing prevalence of chronic diseases requiring long-term intravenous therapies, rising demand for home healthcare and outpatient infusion services, growing adoption of minimally invasive infusion techniques, and expansion of healthcare infrastructure in emerging regions are driving market growth.

| Key Insights | Details |

|---|---|

|

Huber Needles Market Size (2025E) |

US$47.8 Mn |

|

Market Value Forecast (2032F) |

US$72.3 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

6.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Cancer Prevalence and Long-term IV Therapies

The increasing prevalence of cancer and chronic diseases requiring long-term intravenous (IV) therapy is a key growth driver. Huber needles are vital for accessing implanted ports in chemotherapy, parenteral nutrition, and long-term antibiotic treatment. For instance, in 2024, the American Cancer Society reported 2,001,140 new cancer cases in the U.S. alone, significantly expanding the number of patients dependent on port-based infusion therapies. Moreover, rising incidences of chronic conditions such as Crohn’s disease, cystic fibrosis, and severe infections requiring extended IV antibiotics are adding to this demand.

With more patients shifting from inpatient to outpatient and home-based infusion therapy, the need for safe, durable, and easy-to-use Huber needles is expected to grow steadily across both developed and emerging healthcare systems.

Needlestick Injuries and Catheter-related Bloodstream Infections

A major restraint to the market is the risk of needlestick injuries and catheter-related bloodstream infections. Healthcare workers face exposure to blood-borne pathogens such as HIV and hepatitis B/C, leading to occupational hazards and liability concerns. According to the Centers for Disease Control and Prevention, about 385,000 sharps-related injuries occur annually among hospital-based healthcare personnel in the U.S., while the WHO reports millions of cases worldwide due to insufficient safety protocols.

Beyond immediate injury risks, improper insertion of Huber needles into ports can damage septa, increasing the likelihood of infection and complications for patients. In regions with limited staff training or reliance on non-safety-engineered devices, the problem intensifies, prompting facilities to explore alternative vascular access methods such as peripherally inserted central catheter (PICC) lines and central venous catheters. These risks not only raise healthcare costs but also slow widespread adoption of Huber needles, especially in resource-constrained settings.

Home-infusion and Outpatient Oncology Programs

The expansion of home-infusion therapy and outpatient oncology centers is creating growth opportunities for the market. Increasingly, patients opt for ambulatory and home-based care to minimize hospital stays, reduce costs, and enhance quality of life. Huber needles are essential for accessing implanted ports during chemotherapy, parenteral nutrition, and long-term IV treatments outside hospital settings.

For example, the National Home Infusion Association reports that over 3.2 million patients receive home-infusion therapy annually in the U.S. The growth of outpatient oncology centers, fueled by rising cancer prevalence and advancements in infusion therapies, further boosts market growth. These facilities often establish bundled procurement contracts with suppliers, ensuring steady utilization of Huber needles.

Category-wise Analysis

Product Type Insights

The curved Huber needle segment dominated the needles market in 2024, accounting for the largest revenue share of 55.7%. The segment’s strong performance is primarily driven by its ergonomic design, which allows easier access to implanted ports while minimizing septum damage and coring.

Curved needles are widely preferred in oncology and long-term infusion therapies due to enhanced safety, reduced patient discomfort, and compatibility with safety-engineered features. Their adoption in hospitals, outpatient oncology centers, and home-infusion programs has further boosted the market growth.

Application Insights

The IV cancer treatment segment dominated the needles market in 2024, accounting for the largest revenue share. This is due to the rising global incidence of cancer, which increases the demand for chemotherapy and other intravenous treatments requiring repeated, safe vascular access. Huber needles are widely used with implantable ports to deliver these therapies efficiently while minimizing pain and infection risks, making them the preferred choice in oncology settings. Their non-coring design helps preserve the integrity of the port septum, minimizing complications such as infection, leakage, or tissue damage, factors crucial for cancer patients requiring multiple infusions.

Regional Insights

North America Huber Needles Market Trends

North America remains the largest globally, led by the U.S., due to the high prevalence of chronic diseases requiring long-term intravenous therapies, such as cancer and gastrointestinal disorders. Strong healthcare infrastructure, widespread adoption of advanced infusion technologies, and a large number of hospitals, oncology centers, and home care providers further drive demand. Supportive government healthcare policies, higher healthcare spending, and growing awareness of minimally invasive treatment boost market growth in the region.

For instance, in January 2025, BD (Becton, Dickinson and Company), a global medical technology company, announced additional investments in its U.S. manufacturing network to expand capacity for critical medical devices, including syringes, needles, and IV catheters, addressing ongoing healthcare system needs. As part of its 2024 investment of over US$10 Million, new needle and syringe production lines were installed at BD plants in Connecticut and Nebraska. One line is fully operational, with additional lines expected to start in the coming months.

Europe Huber Needles Market Trends

The Europe market is expected to grow steadily, driven by the increasing prevalence of chronic diseases such as cancer and gastrointestinal disorders, which require long-term intravenous therapies. Growth is further supported by the expansion of outpatient care centers, rising adoption of minimally invasive infusion techniques, and continuous technological advancements in needle design. Government initiatives to improve healthcare infrastructure, coupled with increasing patient awareness and demand for safer, more efficient infusion devices, are also contributing to a steady market growth across the region.

Asia Pacific Huber Needles Market Trends

Asia Pacific is projected to grow at the fastest CAGR from 2025 to 2032, fueled by the rising prevalence of chronic diseases, increasing demand for home healthcare and outpatient infusion services, and expanding healthcare infrastructure in developing regions. Growth is also supported by government initiatives to improve patient care, rising awareness of minimally invasive treatment options, and the adoption of advanced medical devices and technologies across hospitals and clinics in the region.

Competitive Landscape

The global Huber needles market is highly competitive, with major players such as BD, Nipro Europe Group Companies, B. Braun Medical Inc., McKesson Medical-Surgical Inc., ICU Medical, Inc., and Boen Healthcare Co., Ltd leading the market through extensive product portfolios, strong global distribution networks, and continuous innovation in needle design and safety features.

These companies focus on developing advanced, ergonomically designed Huber needles, including curved and straight variants, to enhance patient comfort and procedural efficiency. Strategic initiatives such as mergers & acquisitions, capacity expansions, and collaborations with hospitals, oncology centers, and home healthcare providers further strengthen their market presence and drive growth in the Huber needles sector.

Key Industry Developments

- In 2025, Nipro introduced the SAFETOUCH Huber Needle Set, integrating a non-coring Huber needle with an easy-activate safety device.

- In February 2025, Mekon released a new range of safety Huber needles and Huber sets (winged, safety-mechanism versions) to target improved safety, color-coded sizing, and Y-port configurations.

- In January 2025, BD announced a manufacturing investment of over US $10 million in its U.S. plants in Connecticut and Nebraska to expand production of critical devices, including Huber needles.

Companies Covered in Huber Needles Market

- BD

- Nipro Europe Group Companies

- B. Braun Medical Inc.

- Exelint International, Co.

- Vygon

- AngioDynamics, Inc.

- McKesson Medical-Surgical Inc.

- ICU Medical, Inc.

- Ningbo Jumbo Medical Instrument Co., Ltd.

- Anhui Tiankang Medical Technology Co., Ltd

- Perfect Medical Ind.Co., Ltd.

- Boen Healthcare Co., Ltd.

- ISCON SURGICALS LTD.

Frequently Asked Questions

The Huber needles market is projected to be valued at US$47.8 Million in 2025.

The Huber needles market growth is being driven by rising cancer and chronic disease prevalence, growing long-term IV treatments, and increased demand for safe, minimally invasive infusion solutions.

The global market is poised to witness a CAGR of 6.1% between 2025 and 2032.

Expansion of home healthcare and outpatient infusion services, adoption of advanced infusion technologies, and increasing healthcare infrastructure in emerging regions create significant growth opportunities in the Huber needles market.

BD, Vygon, Nipro Europe Group Companies, and B. Braun Medical Inc. are some of the key players in the Huber needles market.