- Medical Devices

- Microneedle Drug Delivery Systems Market

Microneedle Drug Delivery Systems Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Microneedle Drug Delivery Systems Market by Type (Hollow, Solid, Coated, Dissolving, and Others), by Material (Metal, Silicon, Polymer, and Others), by Application (Drug Delivery, Vaccine Delivery, Pain Management, Cancer Therapy, Dermatology, and Others) by End User (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, and Home Care Settings), and Regional Analysis from 2026 to 2033.

Microneedle Drug Delivery Systems Market Share and Trend Analysis

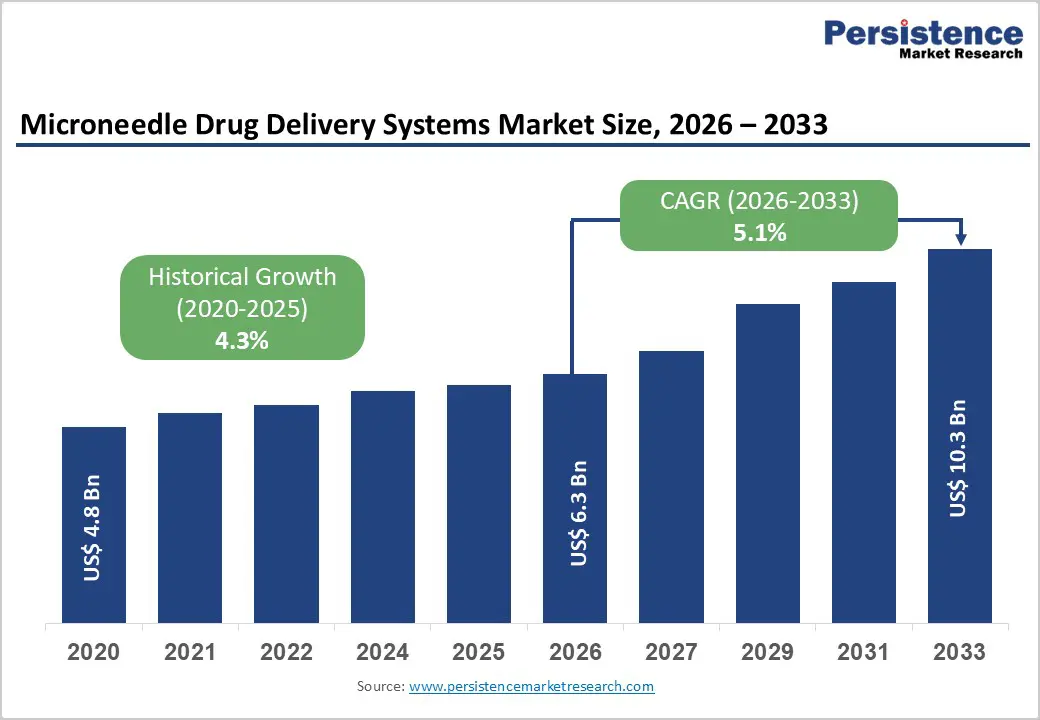

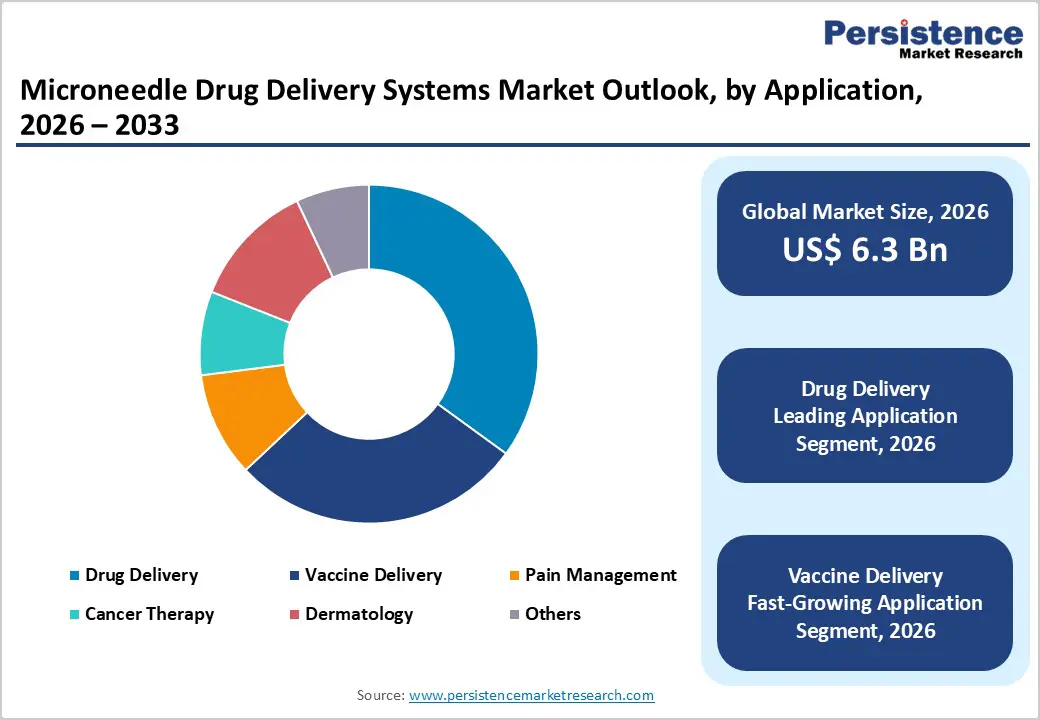

The global microneedle drug delivery systems market size is estimated to grow from US$ 6.3 Bn in 2026 to US$ 10.3 Bn by 2033. The market is projected to record a CAGR of 5.1% during the forecast period from 2026 to 2033.

Global demand for microneedle drug delivery systems is increasing steadily, driven by the rising prevalence of chronic diseases, growing preference for minimally invasive therapies, and expanding adoption of patient-centric drug administration technologies across hospitals, clinics, and home care settings. Increasing use of self-administration platforms, growing demand for painless delivery of biologics and vaccines, and the need for precise and controlled dosing are supporting sustained market growth across both developed and emerging healthcare systems. Higher utilization of polymer-based and dissolving microneedles, integration with wearable and smart delivery devices, and expanding applications in diabetes management, oncology, dermatology, and immunization programs are further accelerating demand. Continuous advancements in microneedle design, mechanical strength, drug-loading efficiency, and large-scale manufacturing are improving safety, reliability, and clinical acceptance. In addition, rising investments in healthcare infrastructure, preventive care, and innovative drug delivery technologies are further propelling the global microneedle drug delivery systems market.

Key Industry Highlights

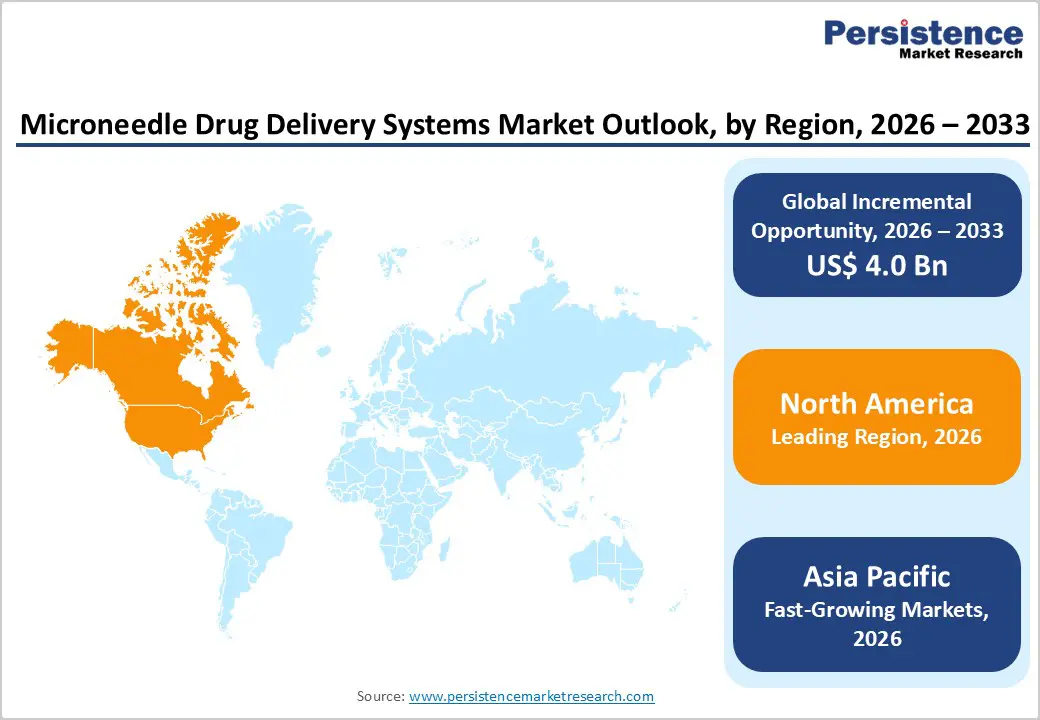

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, early adoption of novel drug delivery technologies, strong reimbursement frameworks, and the presence of major microneedle system developers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid healthcare infrastructure development, rising chronic disease burden, increasing adoption of self-administered therapies, and growing government healthcare investments.

- Leading Material Segment: Metal dominates the market due to its durability, mechanical strength, and widespread use in hollow and solid microneedle systems for clinical drug delivery.

- Fastest-Growing Material Segment: Silicon are expanding rapidly as demand rises for precision-engineered microneedles, complex geometries, and advanced fabrication techniques.

- Leading Application Segment: Drug Delivery remains the most widely adopted application, driven by its critical role in chronic disease management, biologic therapies, and patient-friendly administration.

- Fastest-Growing Application Segment: Vaccine Delivery is scaling quickly as healthcare systems increasingly adopt painless, needle-free platforms for mass immunization and preventive care programs.

| Key Insights | Details |

|---|---|

| Microneedle Drug Delivery Systems Market Size (2026E) | US$ 6.3 Bn |

| Market Value Forecast (2033F) | US$ 10.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver – Rising Chronic Disease Prevalence and Shift Toward Patient-Centric Drug Delivery

The rising incidence of chronic conditions such as diabetes, cancer, cardiovascular disorders, and autoimmune diseases is significantly accelerating demand for advanced drug delivery approaches that improve treatment adherence and therapeutic outcomes. Minimally invasive delivery methods are increasingly favored as healthcare systems move away from conventional injections that cause pain, needle anxiety, and compliance issues. Microneedle-based systems address these challenges by enabling painless, precise, and controlled delivery of drugs and biologics directly through the skin. Growing emphasis on self-administration and home-based care further strengthens adoption, particularly for long-term therapies requiring frequent dosing.

Technological advancements in polymer science, microfabrication, and biodegradable materials have enhanced safety, dose accuracy, and scalability, making microneedles suitable for a broad range of applications, including vaccines, insulin, hormones, and oncology drugs. Rising awareness among clinicians and patients regarding improved bioavailability and reduced systemic side effects is supporting clinical acceptance. Additionally, healthcare providers are increasingly prioritizing solutions that reduce healthcare worker burden and needle-stick injuries. Expanding immunization programs and global focus on preventive care are also reinforcing demand. Collectively, these factors are driving sustained adoption of microneedle systems as a viable alternative to traditional drug delivery routes.

Restraints – Manufacturing Complexity, Cost Pressures, and Regulatory Challenges

The market adoption is restrained by technical, financial, and regulatory hurdles associated with microneedle drug delivery technologies. Manufacturing precision is critical, as needle geometry, mechanical strength, and drug-loading uniformity directly impact safety and performance. Scaling production while maintaining consistent quality requires specialized equipment and expertise, leading to higher manufacturing costs. These expenses can limit affordability, particularly in cost-sensitive healthcare markets.

Regulatory pathways for combination products that integrate medical devices with pharmaceutical formulations remain complex, often requiring extensive clinical validation and long approval timelines. Variability in regulatory requirements across regions further complicates global commercialization. Stability concerns for biologics and vaccines within microneedle matrices also necessitate rigorous testing, increasing development costs. From a clinical perspective, limited long-term real-world data in certain therapeutic areas can slow physician adoption. Additionally, integration into existing treatment protocols and reimbursement uncertainty may discourage healthcare providers from rapid uptake. These combined challenges can delay market penetration, particularly among smaller pharmaceutical companies and healthcare systems with constrained budgets.

Opportunity – Expansion in Vaccines, Biologics, and Emerging Healthcare Markets

Substantial opportunities are emerging as microneedle platforms expand beyond traditional drug delivery into vaccines, biologics, and personalized therapies. Growing global focus on immunization preparedness has highlighted the need for scalable, needle-free delivery technologies that simplify logistics and improve patient acceptance. Microneedles offer advantages such as dose sparing, reduced cold-chain dependency, and ease of administration, positioning them well for mass vaccination programs.

Furthermore, Emerging markets present another significant growth avenue as governments invest in healthcare infrastructure, preventive care, and access to advanced therapeutics. Rising middle-class populations and increasing health awareness are accelerating demand for convenient and less invasive treatment options. Continued innovation in dissolving and polymer-based microneedles is enabling compatibility with complex biologics and controlled-release formulations. Partnerships between pharmaceutical companies and device manufacturers are also unlocking co-development opportunities and faster commercialization. As personalized medicine gains traction, microneedle systems capable of precise, patient-specific dosing are expected to gain wider acceptance, creating long-term opportunities for differentiation, recurring revenue, and technological advancement across global healthcare systems.

Category-wise Analysis

By Type, Hollow Microneedles Lead Due to Precise and Controlled Intradermal Drug Administration

The hollow segment is projected to dominate the global microneedle drug delivery systems market in 2026, accounting for a revenue share of 26.0%. This leadership is driven by the ability of hollow microneedles to deliver liquid formulations with high dose accuracy and controlled flow directly into the dermal layer, closely mimicking conventional injections while minimizing pain. Hollow microneedles are particularly suited for biologics, vaccines, insulin, and oncology drugs that require precise dosing and rapid systemic absorption. Their compatibility with existing injectable formulations reduces reformulation complexity for pharmaceutical companies, accelerating adoption. Increasing demand for intradermal vaccination, therapeutic drug delivery, and clinical use in hospitals further supports growth. Additionally, advancements in microfabrication and improved needle strength are enhancing reliability and safety, reinforcing the hollow segment’s dominant position within the market.

By Application, Drug Delivery Leads Due to Its Central Role in Chronic Disease and Biologic Therapies

The drug delivery segment is expected to dominate the global microneedle drug delivery systems market in 2026, accounting for a revenue share of 35.0%. This dominance is driven by the growing use of microneedles for systemic delivery of therapeutics aimed at improving treatment adherence, dosing accuracy, and patient comfort. Microneedle-based drug delivery is increasingly adopted for insulin, hormones, immunotherapies, and pain management drugs, particularly in chronic disease management. The shift toward self-administration and home-based care is accelerating demand for minimally invasive delivery platforms that reduce dependency on healthcare professionals. Additionally, microneedles enhance bioavailability of drugs that face limitations with oral or topical administration. Rising prevalence of diabetes, cancer, and autoimmune disorders, combined with increasing focus on patient-centric drug delivery technologies, continues to position drug delivery as the most revenue-generating application segment.

By End User, Hospitals Dominate Due to High Clinical Adoption and Advanced Treatment Infrastructure

The hospitals segment is projected to dominate the global microneedle drug delivery systems market in 2026, accounting for a revenue share of 47.1%. Hospitals serve as the primary setting for advanced drug administration, vaccination programs, oncology treatments, and post-surgical pain management, resulting in consistent utilization of microneedle-based delivery systems. High patient volumes, availability of trained healthcare professionals, and integration of novel delivery technologies into standardized treatment protocols support adoption. Hospitals are also early adopters of innovative drug delivery platforms for biologics and vaccines, particularly during large-scale immunization initiatives. Furthermore, the presence of specialized departments and inpatient care facilities facilitates controlled introduction of microneedle systems before broader rollout into outpatient and homecare settings. Expansion of tertiary care hospitals and multispecialty medical centers, especially in emerging economies, continues to reinforce hospitals as the leading end-user segment.

Region-wise Insights

North America Microneedle Drug Delivery Systems Market Trends

North America is expected to dominate the global microneedle drug delivery systems market with a value share of 46.7% in 2026, led primarily by the United States. The region benefits from a highly developed healthcare infrastructure, strong adoption of advanced drug delivery technologies, and a growing emphasis on patient-centric treatment approaches. High prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders drives sustained demand for innovative and minimally invasive drug delivery solutions. Hospitals and healthcare providers in North America actively adopt microneedle platforms to improve treatment compliance, reduce needle-stick injuries, and enhance patient comfort.

Favorable reimbursement frameworks and rapid regulatory pathways support commercialization of new microneedle-based products. The presence of leading medical device and pharmaceutical companies accelerates technological innovation and large-scale manufacturing. Additionally, increasing focus on biologics, vaccines, and personalized medicine further strengthens long-term market leadership across the region.

Europe Microneedle Drug Delivery Systems Market Trends

The Europe microneedle drug delivery systems market is expected to grow steadily, supported by robust public healthcare systems, rising chronic disease burden, and strong regulatory oversight. Countries including Germany, the U.K., France, Italy, and the Nordic nations demonstrate increasing adoption of advanced drug delivery technologies across hospital and clinical settings. Aging populations and growing prevalence of cancer, diabetes, and autoimmune disorders are driving demand for safer and more efficient drug administration methods.

Europe’s strong emphasis on patient safety, clinical efficacy, and quality assurance supports consistent adoption of validated microneedle platforms. Public healthcare funding ensures broad access to innovative therapies, maintaining stable demand across regions. Additionally, government-backed vaccination programs and preventive healthcare initiatives are encouraging the use of minimally invasive delivery systems. Continued investment in healthcare modernization, digital health integration, and pharmaceutical innovation is expected to support sustained market expansion across Europe.

Asia Pacific Microneedle Drug Delivery Systems Market Trends

The Asia Pacific microneedle drug delivery systems market is expected to register a relatively higher CAGR of around 7.0% between 2026 and 2033, driven by rapid healthcare infrastructure expansion and rising demand for advanced treatment solutions. Large populations in China, India, Japan, and Southeast Asia, combined with increasing prevalence of diabetes, cancer, infectious diseases, and cardiovascular conditions, are significantly boosting demand for innovative drug delivery technologies. Governments across the region are investing heavily in hospital expansion, vaccination programs, and access to modern medical devices.

Growing medical tourism in countries such as India, Thailand, and Malaysia further supports adoption of patient-friendly delivery systems. Cost-sensitive markets are encouraging development of scalable and affordable microneedle platforms by regional manufacturers. Improving insurance coverage, rising healthcare awareness, and increasing penetration of self-administered therapies are expected to sustain strong long-term growth across the Asia Pacific region.

Market Competitive Landscape

The global microneedle drug delivery systems market is highly competitive, with strong participation from companies such as 3M, BD, B. Braun SE, NanoPass., Terumo Corporation, and Cardinal Health. These players leverage extensive global distribution networks, strong brand presence, and continuous innovation in microneedle design, materials, and patch-based delivery platforms to enable safe, minimally invasive, and patient-friendly drug and vaccine administration across clinical and homecare settings.

Rising demand for painless drug delivery, growing prevalence of chronic diseases, increasing focus on self-administration, and expanding use of microneedles in vaccines, biologics, and oncology therapies are driving portfolio expansion and competitive differentiation. Companies are prioritizing improved drug bioavailability, enhanced dose accuracy, scalable manufacturing, and integration with wearable or smart delivery platforms. Strategic initiatives include partnerships with pharmaceutical companies, expansion in emerging healthcare markets, and sustained R&D investment to support next-generation dissolving and hollow microneedle technologies, reinforcing long-term market growth.

Key Industry Developments:

- In January 2026, an study conducted at McGill University in Montreal reported that IVF hormones could potentially be administered using a painless microneedle patch, offering a more comfortable and patient-friendly alternative to traditional injections. This approach could simplify fertility treatment regimens and improve adherence for patients undergoing assisted reproductive therapy.

- In January 2024, researchers at Tyndall National Institute introduced a smart wearable microneedle drug delivery device concept designed to enable controlled, on-demand drug administration and real-time health monitoring, highlighting the potential to significantly advance personalized and remote healthcare delivery.

Companies Covered in Microneedle Drug Delivery Systems Market

- 3M

- BD

- B. Braun SE

- NanoPass.

- Terumo Corporation

- Cardinal Health

- Nitto Denko Corporation

- Zosano Pharma Corporation

- Corium International, Inc.

- Raphas Co., Ltd

- Valeritas Inc.

- heraJect Inc.

- Vaxxas Pty Ltd

- Microdermics Inc.

- Others

Frequently Asked Questions

The global microneedle drug delivery systems market is projected to be valued at US$ 6.3 Bn in 2026.

Increasing prevalence of chronic diseases alongside rising demand for painless, minimally invasive, self-administered drug delivery solutions.

The global microneedle drug delivery systems market is poised to witness a CAGR of 5.1% between 2026 and 2033.

Expanding applications in vaccine delivery, personalized therapies, and adoption in emerging markets due to improving healthcare infrastructure.

3M, BD, B. Braun SE, NanoPass., Terumo Corporation, and Cardinal Health are some of the key players in the microneedle drug delivery systems market.