- Smart Packaging

- Molded Fiber Packaging Market

Molded Fiber Packaging Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Molded Fiber Packaging Market By Product Type (Trays, Clamshells, Cups and Bowls), by Molded Type (Transfer, Thermoformed), Source Material (Recycled Paper, Virgin Wood Pulp), by End-use (Food & Beverage, Consumer Electronics), and Regional Analysis for 2025 - 2032

Molded Fiber Packaging Market Size and Trends Analysis

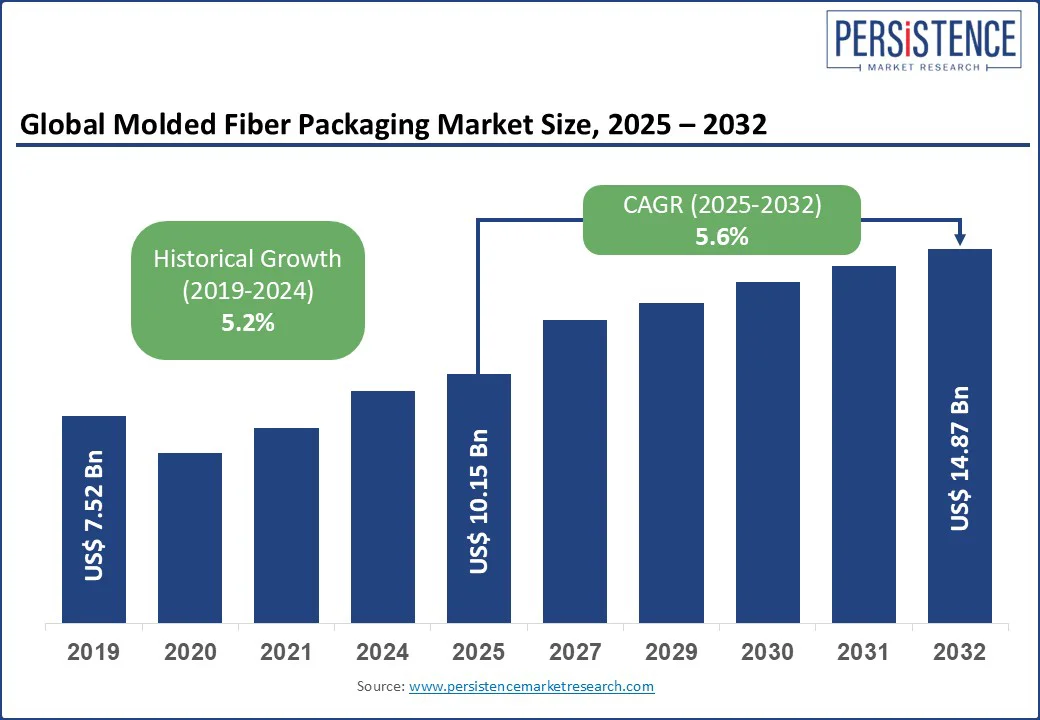

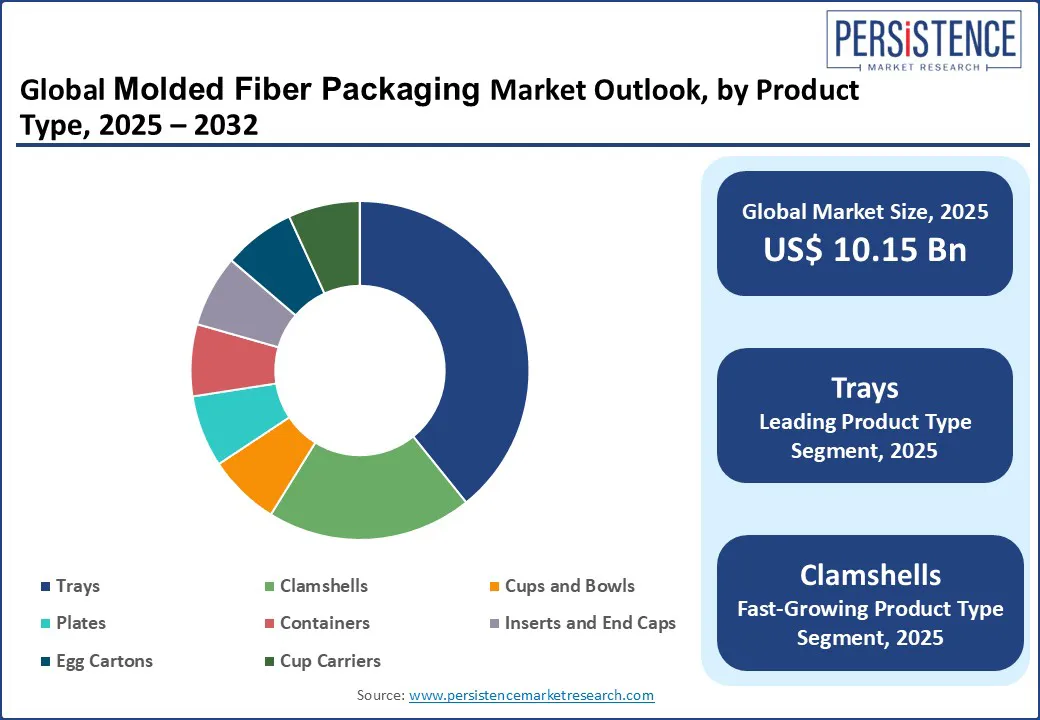

The global molded fiber packaging market size is likely to be valued at US$ 10.15 Bn in 2025 and is expected to reach US$ 14.87 Bn by 2032, growing at a CAGR of 5.6% in the forecast period from 2025 to 2032. Increasing demand for sustainable and biodegradable packaging solutions across industries such as food & beverage, electronics, healthcare, and e-commerce drives the need for molded fiber packaging.

As governments worldwide impose stringent regulations on single-use plastics, businesses are shifting toward eco-friendly alternatives such as molded pulp and fiber-based materials. This environmentally friendly packaging solution offers high recyclability, low carbon footprint, and protective strength, making it an ideal choice for both primary and secondary packaging needs. With the rising consumer awareness around green packaging and the surge in online retail and food delivery services, the market is witnessing accelerated adoption. Furthermore, technological advancements in thermoforming and dry-molding processes are enhancing product quality and expanding application areas, thereby fueling the future potential of the sustainable molded fiber packaging market.

Key Industry Highlights:

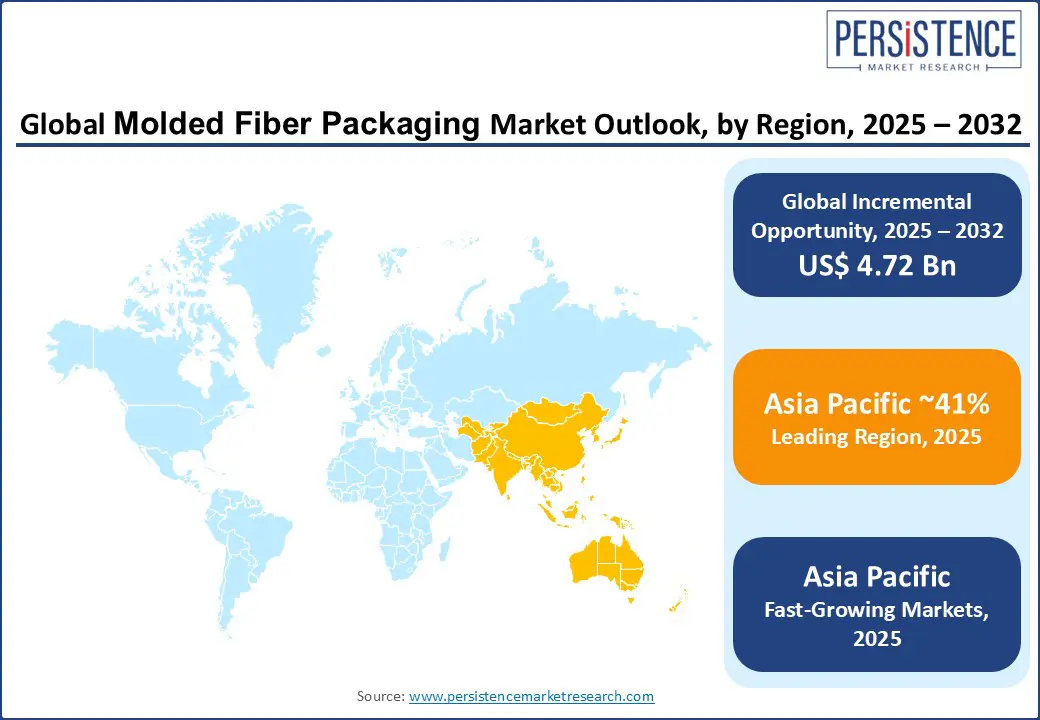

- Asia Pacific leads the market with over 41% share, driven by the rising use of agro-waste pulp and growing demand in foodservice and e-commerce sectors.

- The thermoformed molded fiber segment is growing rapidly in electronics and cosmetics, offering premium, plastic-free packaging alternatives.

- Huhtamaki, PulPac, and Zume are advancing dry-molded fiber and PFAS-free coatings, reducing water use and improving sustainability.

- Custom molded pulp inserts for electronics and healthcare are replacing foam and plastic, driven by performance and ESG goals.

- The industry is shifting toward automation and barrier-coated molded fiber, positioning it as a key player in circular packaging solutions.

- Growing interest in plantable and biodegradable seedling trays opens new applications in sustainable agriculture and horticulture.

|

Market Attribute |

Key Insights |

|

Global Molded Fiber Packaging Market Size (2025E) |

US$ 10.15 Bn |

|

Market Value Forecast (2032F) |

US$ 14.87 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.2% |

Market Dynamics

Driver - Increasing Use of Customized Thermoformed Wet-Press Molded Pulp Inserts in Electronics and Healthcare Driving the Market Forward

The adoption of biodegradable graphene-oxide coatings in molded fiber disposables is accelerating demand from fast-food and grocery sectors. Companies are integrating PFAS-free coatings of graphene oxide and bio-based films, to create grease-and moisture-resistant molded pulp clamshells and trays that maintain food safety compliance and compostability. Scalable technologies such as PulPac’s Dry Molded Fiber and Scala machines eliminate water slurry tanks, reduce production CO2 and increase line speeds tenfold, making sustainable molded fiber lids and cutlery packs commercially viable alternatives to plastic.

Molded dry-formed pulp trays for e-commerce are gaining traction as online retailers demand recyclable protective packaging that fits automated fulfillment lines. Advanced molding tools now produce high-precision protective trays with a smooth cosmetic finish in under two weeks, enabling brands to meet PFAS-free, moisture-resistant, and sterile packaging standards.

Restraint - Supply Chain Bottlenecks in Dry-Molded Fiber Production Increase Raw Material Volatility and Inflate Costs

Supply chain bottlenecks in dry-molded fiber production increase raw material volatility and inflate costs. Over 65% of pulp packaging relies on recycled paper, and recycled fiber prices have spiked by 35% due to inconsistent waste collection and competition from tissue mills. Mid-sized producers struggle to secure high-quality recycled pulp, disrupting supply chains for precision-cut lid and insert molds. These volatile supplies force manufacturers to slow runs or replace materials, eroding margins.

The scaling of thermoformed wet-press molded pulp production for e-commerce is being hindered by energy and equipment constraints. Drying consumes nearly half of all process energy, and retrofitting advanced infrared dryers costs at least US$ 3 Mn per line, beyond reach for most SMEs. Meanwhile, tooling complexity remains high: designing intricate product-protection inserts demands costly custom molds, with defect rates up to 20% from fiber variability. These factors limit cost-effective scaling and keep molded fiber trays behind plastics in capacity expansion.

Opportunity - Expansion of Graphene-Oxide Coated Food-Safe Molded Pulp Trays Opens a New Frontier in Extended-Shelf-Life Packaging for Perishables

Expansion of graphene-oxide-coated food-safe molded pulp trays opens a new frontier in extended-shelf-life packaging for perishables. Graphene’s impermeability to gases and water makes it ideal for developing biodegradable, moisture-resistant clamshells and trays that can replace aluminum barriers. This innovation positions molded fiber packaging as a premium, sustainable substitute in food retail and delivery, meeting consumer demand for both freshness and eco-friendliness. Custom-fit molded fiber pulp inserts for consumer electronics are also gaining traction as brands like Apple and Dell shift to shock-absorbent pulp trays for device protection. This meets e-waste mandates and supports circular economy initiatives while leveraging automation to enable precision molding at scale.

Development of plantable biodegradable seedling pulp trays using agricultural and textile waste offers a next-wave opening in sustainable agriculture packaging. Biotech firms are blending cotton/textile waste or straw/bagasse fibers into suction-molded pulps or hot-pressed biodegradable resin blends (e.g., starch), creating trays that double as planting pots after seed germination. These sustainable planting pulp trays support root development, biodegrade naturally in soil, and reduce nursery plastic waste, aligning with circular farming and regenerative agriculture trends.

Category Wise Analysis

Product Type Insights

Trays remain the dominant segment, accounting for over 40% of market share due to high demand from egg packaging, fresh produce, and quick-service restaurants. The shift toward eco-friendly molded fiber produce trays are prominent in Europe and North America, where grocers seek to eliminate plastic clamshells. Clamshells and hinged containers are the fastest-growing product types, especially in the takeaway food molded fiber packaging segment. Major fast-food chains are switching from Styrofoam to moisture-resistant clamshells with custom branding

Molded Type Insights

Transfer molded fiber packaging leads due to its cost-efficiency, especially in high-volume food and industrial packaging applications. It is widely used in egg cartons, cup carriers, and protective industrial pulp molds, benefiting from existing automation and low-tool costs.

Thermoformed molded fiber packaging, while more expensive, is growing rapidly in the electronics and cosmetics sectors. This method enables high-precision molding and smoother surfaces, ideal for premium molded fiber inserts for electronics and personal care. Dry-molded fiber (DMF) is also emerging as this process allows high-speed molded fiber cutlery and lids production without water, dramatically reducing energy and cycle time.

Source Material Insights

Recycled paper and corrugated waste dominate the raw material landscape, providing cost-effective pulp for trays and general-purpose packaging. Non-wood pulp (e.g., bamboo, wheat straw, sugarcane bagasse) is gaining traction as brands focus on molded fiber packaging made from agro-waste to reinforce their sustainability credentials.

End-use Insights

Food & beverage holds the largest market share of 50%, with molded fiber widely used in egg trays, fast-food clamshells, and coffee cup holders. Consumer shift toward compostable molded pulp food containers is driving demand, supported by retail and foodservice bans on Styrofoam and PET.

Consumer electronics is the fastest-growing end-use category. Brands are adopting custom-molded fiber electronic packaging inserts that meet anti-static and shock-absorption standards while eliminating the need for plastic foams. Healthcare and pharma are emerging users of sterile molded fiber medical packaging, including kidney trays and disposable surgical containers.

Regional Insights

Asia Pacific Molded Fiber Packaging Market Trends

Asia Pacific leads the molded fiber packaging market, accounting for over 41% of the global market share, and is projected to maintain its dominance through 2032. This growth is driven by rising demand for biodegradable molded trays and clamshells in countries such as China, India, and Indonesia. China alone contributes more than half of the regional revenue due to its vast e-commerce network and food delivery ecosystem, where molded pulp packaging is replacing EPS foam. India is emerging as a key growth engine, propelled by the increasing adoption of non-wood pulp packaging made from sugarcane bagasse and wheat straw. The region is also seeing rapid deployment of dry-molded fiber technologies to support high-speed food container manufacturing.

North America Molded Fiber Packaging Market Trends

The U.S. market is expanding steadily, accounting for a substantial share based on high demand. Growth is supported by state-level bans on Styrofoam containers and the increasing use of molded fiber inserts for consumer electronics and healthcare devices. Major retailers and QSR chains in the U.S. are rapidly shifting toward molded pulp packaging for food service and online retail, creating steady demand for trays and clamshells with compostable coatings. Canada is following suit with strong municipal composting infrastructure and is projected to see a CAGR of over 6% during the forecast period.

Europe Molded Fiber Packaging Market Trends

Europe remains an innovation-driven market for molded fiber packaging. Countries such as Germany, France, and the Netherlands are pushing for plastic-free supermarket aisles, boosting demand for graphene-coated pulp food trays and premium thermoformed fiber cartons. The EU’s Packaging and Packaging Waste Regulation (PPWR) is accelerating the transition toward fully recyclable, fiber-based packaging, especially in the food, cosmetics, and consumer electronics sectors. While the growth rate is moderate, Europe's regulatory landscape and consumer demand for sustainable solutions make it a critical market for high-value applications.

Competitive Landscape

The global molded fiber packaging market is moderately fragmented, with a mix of large multinational companies and regional players focusing on sustainable packaging innovation. Competition is intensifying as demand grows for thermoformed pulp packaging, PFAS-free coatings, and automated dry-molding technologies that deliver higher speed and lower energy consumption.

Huhtamaki Oyj leads globally with major investments in dry-molded fiber technology and sustainable foodservice trays. Brodrene Hartmann A/S dominates egg packaging in Europe and Latin America, expanding into precision industrial molds. Pactiv Evergreen and Genpak LLC focus on PFAS-free food containers and trays for QSRs and retail. PulPac AB and Zume Inc. are reshaping the market with automated dry-molded fiber systems, reducing energy and water use. Strategic moves like CKF’s acquisition of UFP’s molded fiber division reflect growing consolidation in the market

Key Industry Developments

- In January 2024, Huhtamaki expanded its collaboration with PulPac to deploy dry-molded fiber technology across Europe and North America. This partnership supports scalable production of plastic-free food trays and lids, reducing water use by up to 95%.

- In March 2023, Zume Inc., in collaboration with Solenis, introduced a fully compostable, PFAS-free coating for molded fiber food containers. The technology is now used in packaging for global restaurant and foodservice clients.

Companies Covered in Molded Fiber Packaging Market

- Huhtamaki Oyj

- Brodrene Hartmann A/S

- Pactiv Evergreen Inc.

- Genpak LLC

- Fabri-Kal

- CKF Inc.

- UFP Technologies, Inc.

- Zume Inc.

- PulPac AB

- Asia Pulp & Paper (APP)

- Papacks GmbH

- Henry Molded Products Inc.

- EnviroPAK Corporation

- Keiding Inc.

- Protopak Engineering Corp.

- Sabert Corporation

- Western Pulp Products Company

Frequently Asked Questions

The molded fiber packaging market is projected to be valued at US$ 10.15 Bn in 2025.

The molded fiber packaging market is expected to reach approximately US$ 14.87 Bn by 2032.

Key trends include the rise of dry-molded fiber technology, demand for PFAS-free food-safe coatings, and increasing use of agro-waste pulp materials like bagasse and wheat straw.

Trays hold the largest share by product type, with a market share of 40% in 2025.

The molded fiber packaging market is expected to grow at a CAGR of 5.6% from 2025 to 2032, driven by rising demand for sustainable and biodegradable packaging across industries.

Some of the major players with strong portfolios include Huhtamaki Oyj, Brodrene Hartmann A/S, Pactiv Evergreen Inc., PulPac AB and Zume Inc.