- Advanced Materials

- Graphene Market

Graphene Market Size, Share, and Growth Forecast 2026 - 2033

Graphene Market by Material (Graphene Nanoplatelets, Graphene Oxide, Reduced Graphene Oxide, Others), End‑user (Electronics, Aerospace & Defense, Energy, Automotive, Others), Analysis, 2026 - 2033

Graphene Market Size and Trend Analysis

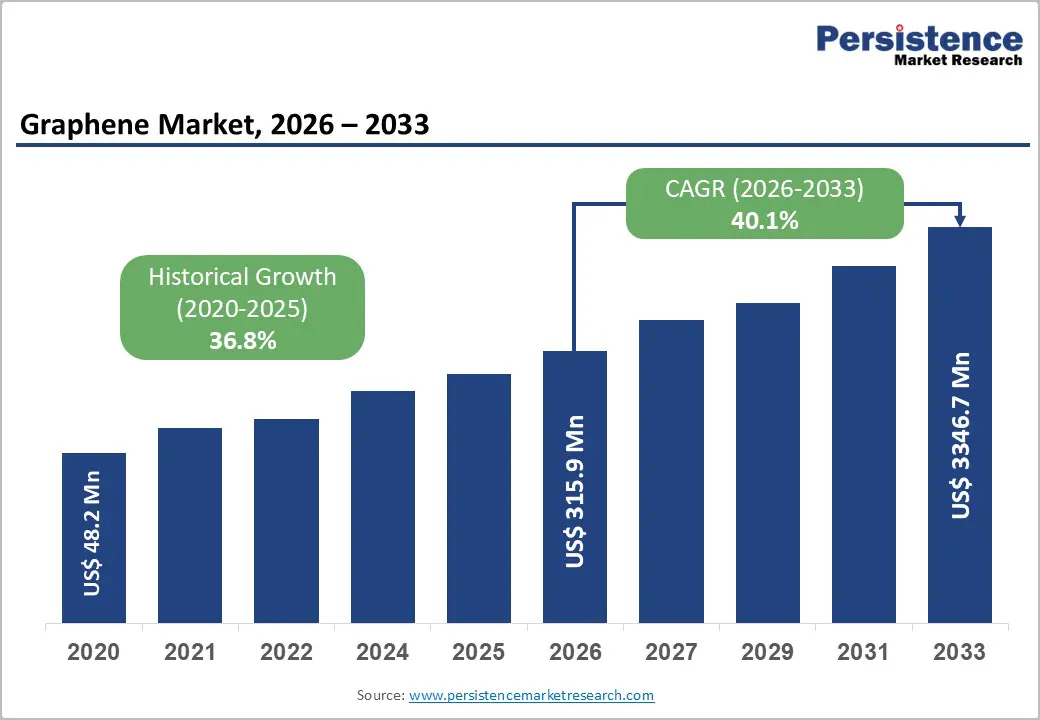

The global Graphene Market size is likely to be valued at US$ 315.9 Million in 2026 and is expected to reach US$ 3,346.7 Million by 2033, growing at a CAGR of 40.1% during the forecast period from 2026 to 2033. This explosive growth is driven by graphene’s unique combination of high electrical conductivity, exceptional mechanical strength, and thermal stability, which is enabling breakthrough applications in electronics, energy storage, aerospace, and automotive sectors.

Key Industry Highlights:

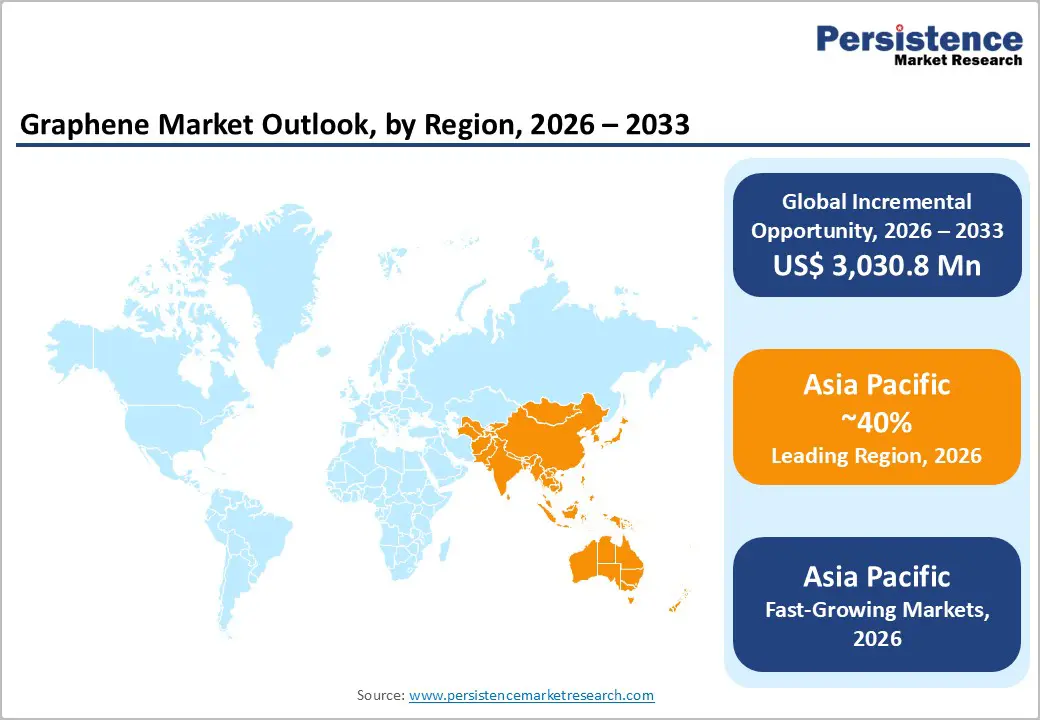

- Leading Region: Asia Pacific leads the Graphene Market is likely to account for 40% share in 2026 due to large electronics and automotive manufacturing bases, rising R&D investment, and strong government support for nanomaterials innovation in China, Japan, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by expanding EV and renewable-energy markets, increasing electronics production, and growing adoption of graphene-enhanced composites.

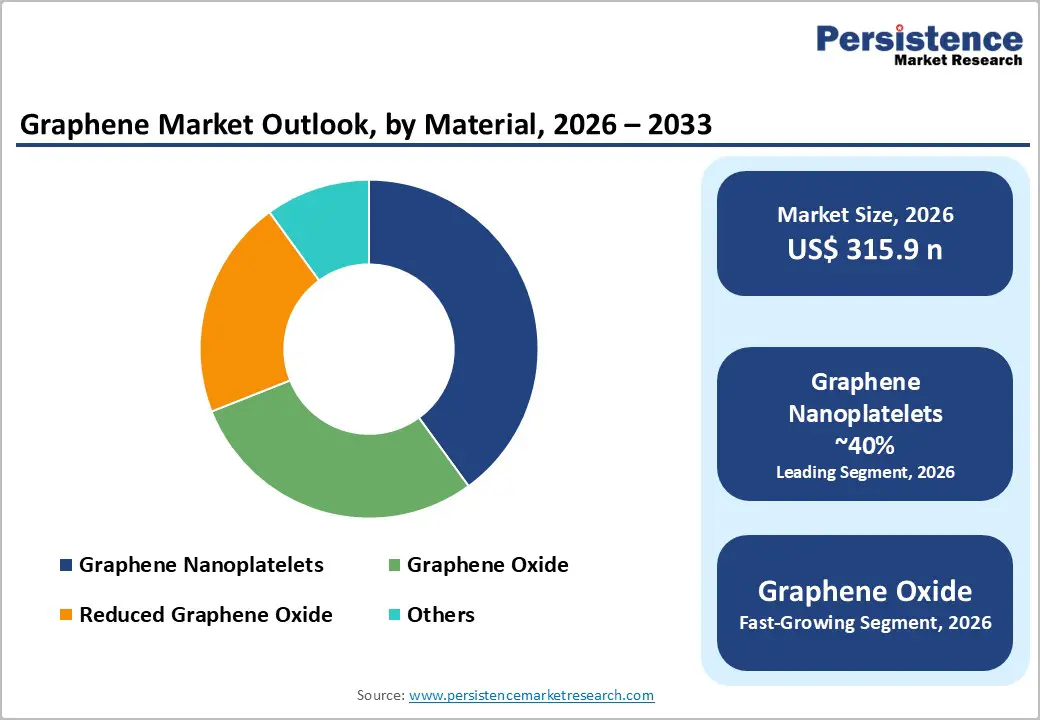

- Dominant segment: Graphene nanoplatelets dominate the material category, capturing an estimated 40% share due to their versatility in polymer composites, coatings, and conductive inks across multiple industries.

- Fastest-growing segment: The energy end-user segment is the fastest-growing, projected to capture 25% of the graphene market by value, driven by integration into batteries, supercapacitors, and grid-scale storage systems.

- Key Opportunity: The integration of graphene into next-generation batteries and supercapacitors for electric vehicles (EVs) and renewable-energy storage represents a major opportunity, particularly in North America, Europe, and Asia Pacific.

| Key Insights | Details |

|---|---|

|

Graphene Market Size (2026E) |

US$ 315.9 Million |

|

Market Value Forecast (2033F) |

US$ 3,346.7 Million |

|

Projected Growth CAGR (2026–2033) |

40.1% |

|

Historical Market Growth (2020–2025) |

36.8% CAGR |

Market Dynamics

Drivers - Growing Use of Graphene in Advanced Electronics and Energy Storage Is Driving Strong Global Market Expansion

The graphene market is gaining strong momentum due to rising demand for advanced materials in electronics and energy applications, where graphene’s exceptional electrical conductivity and heat-transfer properties provide clear performance benefits. In electronics, graphene is increasingly used in flexible displays, high-speed transistors, and precision sensors. Research leadership from institutions such as the University of Manchester and collaborative programs such as Graphene Flagship demonstrated prototype devices that operate faster and more efficiently than traditional silicon-based technologies. In energy storage, graphene-enhanced electrodes are improving lithium-ion battery charging speed, durability, and thermal stability. Studies indicate performance improvements of 10–20% in charge rate and cycle life. These measurable benefits are encouraging electronics manufacturers, battery producers, and material suppliers to expand graphene integration, driving consistent long-term market growth across multiple industries.

Massive Government Funding and Research Programs Are Accelerating Commercial Adoption of Graphene Technologies Worldwide

Strong public-sector funding and institutional backing are playing a major role in accelerating graphene commercialization by reducing development risks and improving technology transfer from research labs to industry. The European Union has invested heavily through the Graphene Flagship initiative, coordinating more than 150 academic and industrial partners to advance applications in electronics, energy storage, and healthcare technologies.

In China, national innovation programs and regional development hubs in cities such as Shenzhen and Beijing are providing large-scale funding for graphene manufacturing and product development, helping position the country as a global production leader. In the United States, agencies including the National Science Foundation and the Department of Energy continue to support graphene research across advanced manufacturing and clean-energy systems. This coordinated global funding environment is strengthening the innovation pipeline and accelerating market adoption.

Restraints - High Manufacturing Costs and Difficulties in Scaling Quality Production Continue to Limit Wider Graphene Adoption

Despite its strong performance advantages, graphene adoption is limited by high production costs and difficulties in scaling consistent, high-quality output. Manufacturing techniques such as chemical vapor deposition and exfoliation processes often produce materials with uneven layer thickness, structural defects, and variable purity. These inconsistencies require additional processing, testing, and quality control, significantly raising production expenses.

In electronics and precision engineering, even minor defects can negatively affect performance, making high-grade graphene costly to deploy at commercial scale. For large industrial sectors such as automotive, construction, and packaging, graphene remains more expensive than conventional fillers like carbon black or carbon fiber. This cost gap discourages widespread adoption in price-sensitive applications, slowing penetration across high-volume industries and limiting short-term market expansion despite strong technical advantages.

Lack of Global Material Standards Creates Buyer Uncertainty and Slows Large-Scale Commercialization of Graphene Products

Another key restraint is the absence of universally accepted material standards, which creates uncertainty for buyers and slows large-scale procurement. Graphene products sold under similar labels can differ significantly in purity, layer count, defect levels, surface area, and dispersion performance due to varied manufacturing methods. This inconsistency makes it difficult for end-user to predict performance outcomes, particularly in regulated sectors such as aerospace, energy storage, and medical devices.

Organizations, including the International Organization for Standardization and the ASTM International are working toward formal quality frameworks, but full standard harmonization is still in progress. Until these benchmarks are widely adopted, buyers are likely to maintain cautious qualification timelines, which continues to slow mass commercialization and large-volume contract adoption.

Opportunities - Graphene-Enhanced Batteries and Supercapacitors Are Emerging as a Major Growth Engine for Clean Energy Markets

Energy storage represents one of the most attractive growth opportunities for graphene suppliers, particularly as electric vehicles and renewable power systems expand globally. Research from institutions such as the Massachusetts Institute of Technology and Stanford University has shown that graphene-based battery anodes can increase capacity by 10–30%, extend battery lifespan, and improve thermal management.

These improvements directly address key performance challenges in EVs and grid storage. Commercial players, including NanoXplore and Directa Plus, have already launched graphene-enhanced conductive additives and electrode solutions are now adopted by battery manufacturers. As clean-energy adoption accelerates worldwide, graphene-based energy storage components are expected to become a major long-term demand driver.

Rising Demand for Lightweight High-Strength Materials Is Expanding Graphene Use in Automotive and Aerospace Sectors

Graphene-reinforced composites are gaining attention in aerospace and automotive industries, where reducing weight while improving strength is a strategic priority. In aerospace structures, graphene-enhanced polymers can lower component weight by up to 10% while improving fatigue resistance and durability, helping aircraft manufacturers reduce fuel consumption and maintenance costs. In automotive manufacturing, graphene is being explored in tires, thermal-management components, structural panels, and electromagnetic shielding materials to improve performance and longevity.

These innovations align closely with stricter global emissions regulations and energy-efficiency targets. As manufacturers shift toward lightweight materials to improve vehicle range and fuel economy, demand for advanced composites is expected to rise steadily. This trend creates strong commercial opportunities for graphene producers focused on construction-grade, automotive-grade, and aerospace-grade material formulations.

Category-wise Analysis

Material Insights

Graphene nanoplatelets represent the largest material segment in the Graphene Market, accounting for approximately 40% of the total market value. Their dominance is driven by relatively scalable production methods such as mechanical exfoliation, which enable cost-effective manufacturing compared with single-layer graphene. These multilayer flakes offer excellent conductivity, mechanical reinforcement, and thermal performance, making them highly suitable for polymer composites, coatings, inks, and battery additives.

In automotive and energy applications, nanoplatelets are widely used to enhance heat dissipation, electrical flow, and structural strength without adding significant weight. Their versatility across electronics, construction, packaging, and industrial manufacturing allows suppliers to serve multiple high-volume markets simultaneously. This broad application base continues to support strong commercial demand, positioning graphene nanoplatelets as the backbone material segment of the global graphene industry.

End-user Insights

Electronics remains the largest end-user segment of the graphene market, accounting for approximately 35% of total revenue. This leadership is driven by graphene’s unique combination of electrical conductivity, flexibility, and transparency, which enables next-generation display technologies and high-speed electronic components. Applications include flexible touchscreens, transparent electrodes, radio-frequency transistors, and high-sensitivity sensors used in wearable devices and smart systems.

Research programs have already demonstrated graphene-based alternatives to conventional materials such as indium tin oxide and silicon, offering improved durability and faster signal performance. With continued growth in 5G infrastructure, Internet of Things devices, and flexible electronics, manufacturers are increasingly adopting graphene components to gain performance advantages. This sustained innovation pipeline ensures electronics will remain the primary revenue contributor to the graphene industry.

Regional Insights

North America Graphene Market Trends

North America remains a global innovation leader in graphene development, driven by strong research infrastructure, venture capital investment, and early-stage commercialization. The United States dominates regional activity through extensive university research, government funding programs, and private-sector product development. Companies are actively deploying graphene in high-value applications such as advanced electronics, thermal-management systems, aerospace materials, and battery components.

A vibrant startup ecosystem supports rapid experimentation and pilot-scale commercialization, accelerating time-to-market for new technologies. As regulatory frameworks mature and material standards improve, buyer confidence is expected to increase, further supporting market growth. North America is likely to remain focused on premium performance applications rather than high-volume commodity uses, positioning the region as a hub for innovation-driven and technology-intensive graphene solutions.

Europe Graphene Market Trends

Europe benefits from a coordinated regulatory environment and strong cross-border research collaboration, supporting steady adoption of graphene technologies. Major economies, including Germany, the United Kingdom, France, Spain, and Italy, are actively integrating graphene into automotive components, construction materials, sensors, and energy-storage systems. EU-wide sustainability policies encourage eco-friendly production methods and long-lasting material solutions, supporting demand for graphene-based composites and coatings.

Strong industrial engineering capabilities in Germany are driving composite adoption, while biomedical and electronics research remains prominent in the UK and France. Infrastructure modernization projects across Southern Europe are also utilizing graphene-enhanced materials for durability and energy efficiency. Together, these trends position Europe as a stable, regulation-supported growth market with a strong emphasis on advanced manufacturing and sustainable material technologies.

Asia Pacific Graphene Market Trends

Asia Pacific is both the fastest-growing and largest graphene market globally, combining massive industrial demand with large-scale production capabilities. China continues to dominate through heavy government investment in graphene manufacturing plants, battery technology, and composite materials. Graphene-based energy storage is increasingly used in electric vehicles and grid-scale power systems to meet national emissions and efficiency targets.

Japan’s high-precision electronics sector is adopting graphene components to improve device miniaturization and durability. Meanwhile, India and Southeast Asia are building competitive production ecosystems supported by lower manufacturing costs and expanding domestic markets. These countries are rapidly becoming export suppliers for graphene-enhanced products. This balanced combination of innovation, scale, and cost efficiency ensures that Asia Pacific will remain the primary driver of global graphene market expansion.

Competitive Landscape

The global graphene Market remains highly fragmented, with numerous specialized material suppliers operating alongside a small group of established technology players. Leading companies such as Angstron Materials, XG Sciences, Graphenea, and Haydale Graphene Industries focus on proprietary production techniques, application-specific formulations, and strong intellectual property portfolios.

Many firms are shifting toward vertical integration by offering finished composite solutions rather than raw graphene powders. Partnerships with electronics manufacturers, battery producers, and automotive suppliers are becoming common to accelerate commercialization. Sustainability-focused production methods and customized technical services are emerging as key competitive differentiators. Overall, success in the graphene market increasingly depends on innovation capability, quality consistency, and close collaboration with end-users across high-performance industries.

Key Market Developments

- In February 2025, NanoXplore introduced a next-generation graphene-enhanced battery anode for electric vehicles, delivering 20% higher energy density and 30% faster charging performance. The innovation improves battery efficiency, extends driving range, and strengthens NanoXplore’s leadership in graphene-based energy storage solutions.

- In June 2024, Directa Plus formed a strategic partnership with an electric vehicle manufacturer to develop graphene-infused tires designed to improve durability, thermal control, and energy efficiency. The tires are expected to lower rolling resistance by 10–15%, enhancing vehicle range and safety performance.

- In October 2023, Graphenea announced a €20 million investment to expand graphene nanoplatelets manufacturing through new exfoliation lines and advanced quality-control systems. The expansion aims to meet rising demand from electronics and composite sectors while strengthening supply reliability across European markets.

Companies Covered in Graphene Market

- Angstron Materials, Inc.

- ACS Material, LLC

- BGT Materials Ltd.

- CVD Equipment Corp.

- Directa Plus SpA

- Grafoid Inc.

- Graphenea

- Graphene NanoChem

- NanoXplore, Inc.

- G6 Materials Corp.

- XG Sciences

- Thomas Swan & Co. Ltd.

- 2D Carbon Graphene Material Co., Ltd.

- Haydale Graphene Industries Plc

- Applied Graphene Materials

- Graphene Manufacturing Group (GMG)

- Graphene Square Inc.

- Graphene Frontiers LLC

- Skeleton Technologies

- Cambridge Nanomaterials Technology Ltd.

Frequently Asked Questions

The global Graphene Market is valued at US$ 315.9 Million in 2026 and is projected to reach US$ 3,346.7 Million by 2033, growing at a CAGR of 40.1% from 2026 to 2033, with a historical CAGR of 36.8% between 2020 and 2025.

Key demand drivers include rising demand for high‑performance materials in electronics and energy, strong government and institutional support for nanomaterials innovation, and increasing commercialization of graphene‑enhanced products such as batteries, sensors, and composites.

The graphene nanoplatelets segment is the leading material segment, capturing an estimated 40% share due to their versatility in polymer composites, coatings, and conductive inks across multiple industries.

Asia Pacific is the largest regional market for graphene, accounting for roughly 40% of global value, driven by large electronics and automotive manufacturing bases, rising R&D investment, and strong government support in China, Japan, India, and ASEAN countries.

A key opportunity lies in the integration of graphene into next‑generation batteries and supercapacitors for electric vehicles (EVs) and renewable‑energy storage, which is expected to drive long‑term demand in North America, Europe, and Asia Pacific.