- Specialty & Fine Chemicals

- Graphene Oxide Market

Graphene Oxide Market Size, Share, and Growth Forecast, 2026 – 2033

Graphene Oxide Market by Product Form (Powder, Solution/Dispersion), Manufacturing Method (Hummers’ Method, Others), Functionalization Type (Non-functionalized, Amine-functionalized, Others), Application (Electronics, Others), and Regional Analysis 2026 – 2033

Graphene Oxide Market Size and Trends Analysis

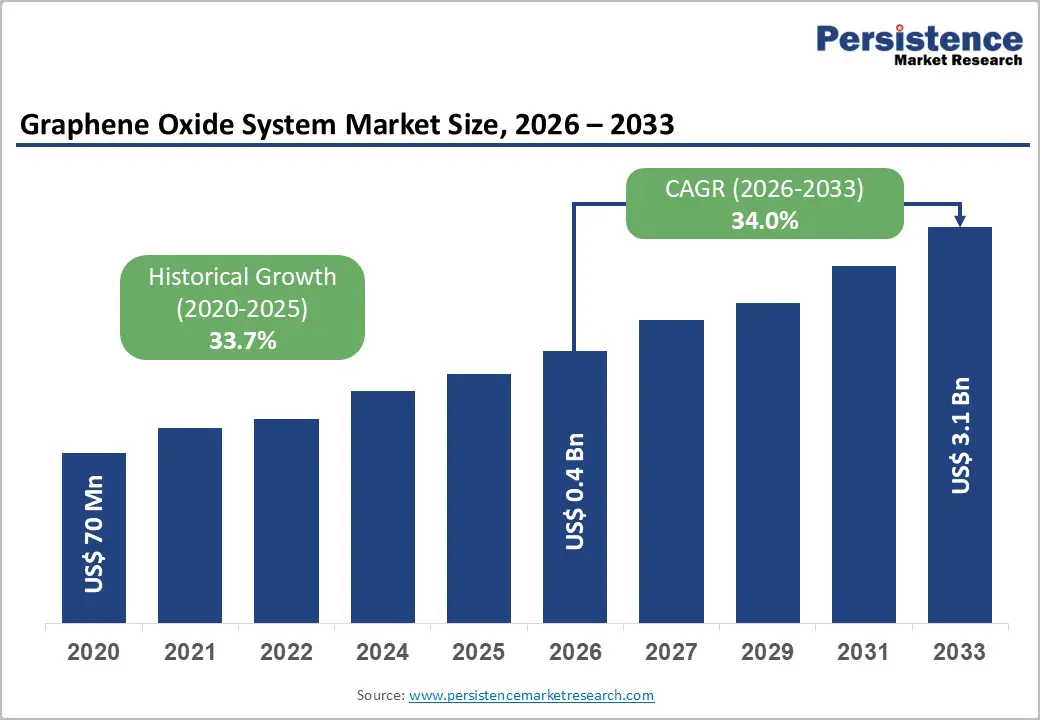

The global graphene oxide market size is likely to be valued at US$0.4 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 34.0% during the forecast period from 2026 to 2033, driven by rapid adoption in electronics, energy storage, and advanced composites, supported by the improving scalability of production and falling unit costs. Government-funded nanotechnology programs and corporate R&D are accelerating commercialization, particularly in Asia Pacific and North America. The increasing adoption of graphene oxide (GO) in composite materials for the aerospace and automotive sectors, owing to its exceptional strength-to-weight ratio, serves as a critical catalyst. Industrial deployment remains concentrated in high-value applications where graphene oxide’s performance advantages offset its premium pricing.

Key Industry Highlights:

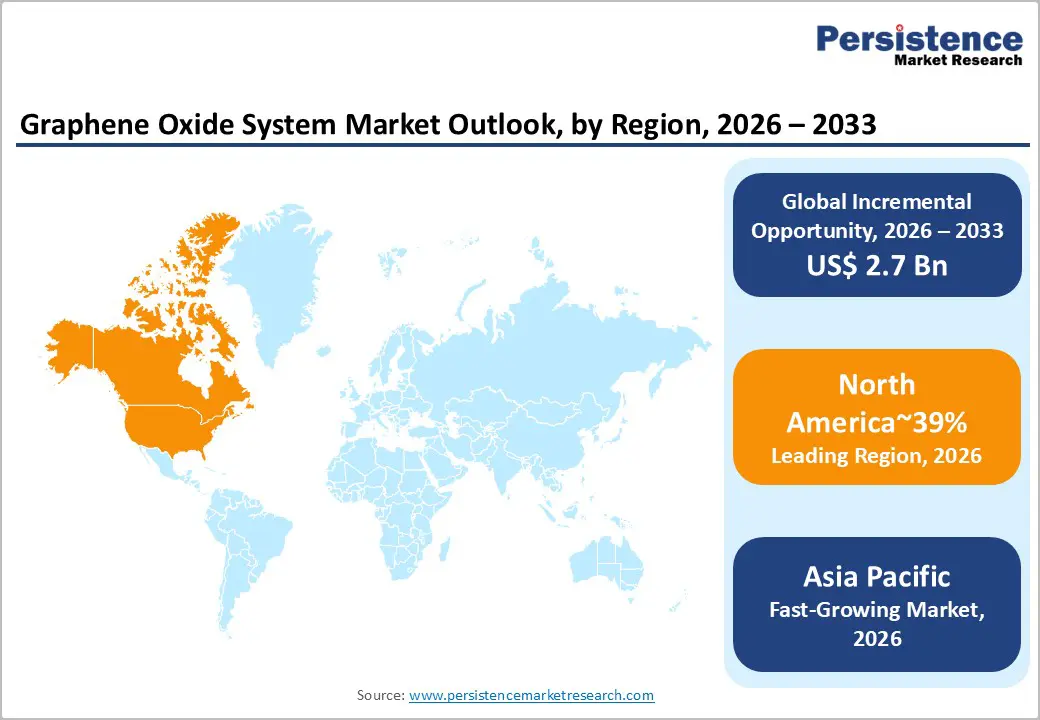

- Leading Region: North America, with around 39% share, supported by strong research commercialization pipelines, a high concentration of advanced materials companies, and early adoption across electronics, aerospace, and defense R&D ecosystems.

- Fastest-growing Region: Asia Pacific, fueled by China's battery manufacturing boom, expanding electronics production in South Korea and Japan, and rising government investments in nanomaterials research and local supply chain development.

- Leading Manufacturing Method: Hummers’ method is expected to hold around 62% market share, reflecting its established industrial scalability, relatively high yield, and widespread standardization across commercial suppliers serving electronics, composites, and research-grade material demand.

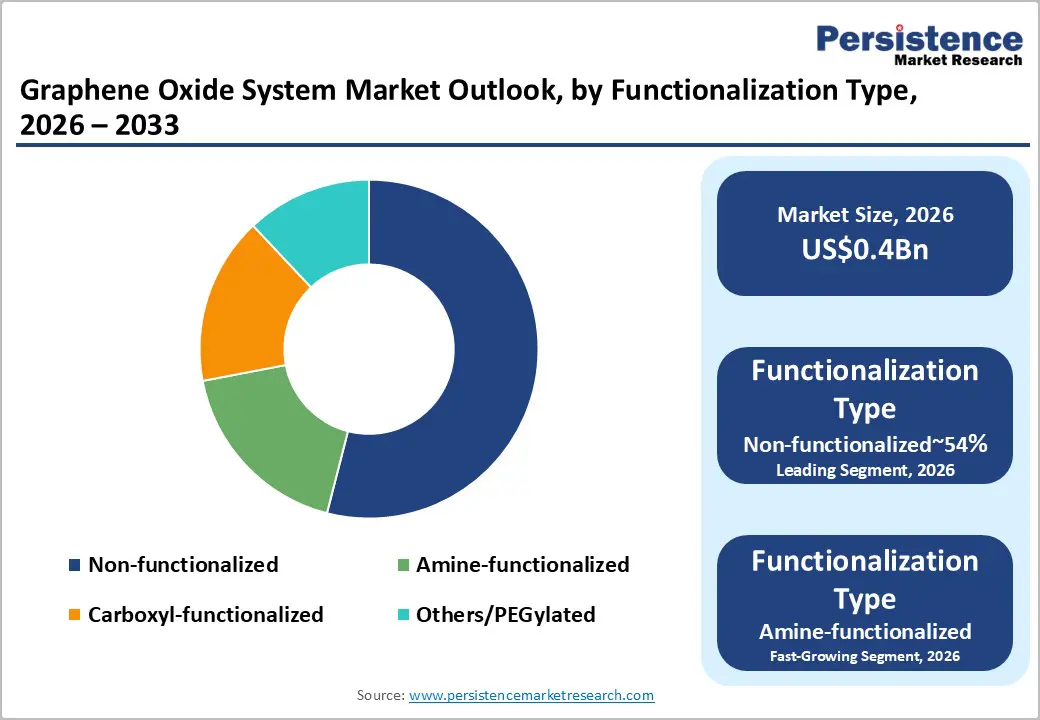

- Leading Functionalization Type: Non functionalized graphene oxide is estimated to account for approximately 54% market share, driven by its broad applicability as a baseline additive in polymer composites, coatings, membranes, and conductive formulations, where end-users prefer post-processing flexibility to tailor surface chemistry based on specific performance requirements.

| Report Attribute | Details |

|---|---|

|

Graphene Oxide Market Size (2026E) |

US$0.4 Bn |

|

Market Value Forecast (2033F) |

US$3.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

34.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

33.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Exponential Demand in Energy Storage Solutions

The accelerating electrification of transportation and grid infrastructure is driving higher demand for advanced electrode materials, with graphene oxide playing a key role in energy storage systems. As electric mobility and renewable energy integration grow, batteries and supercapacitors face increasing demands for higher energy density, faster charging, and longer lifecycles. Graphene oxide's unique surface chemistry and conductive network enhance performance while enabling thinner electrodes and better ion transport. This shift away from conventional graphite to engineered carbon derivatives increases demand for specialty precursors and precision coating technologies.

Market dynamics are also evolving as the push for higher-performance storage systems changes cost structures and procurement priorities. Stricter regulatory scrutiny on safety, durability, and lifecycle efficiency highlights the value of materials that reduce thermal stress, even though they may raise input costs and processing complexity. This shifts margin distribution toward materials that support compliance and performance, encouraging investment in scalable production and quality control. The demand for graphene oxide is growing across automotive, stationary storage, and power electronics sectors. In May 2025, Graphene Manufacturing Group (GMG) approved an AU$900k (approx. US$570,000) investment for its Gen 2.0 graphene production plant, aiming for 10-tonne annual output by mid-2026 and cutting costs by up to 20 times, advancing ultra-fast charging technology.

Electrification and Energy Storage Value Chains

The global push for electrification and renewable energy integration is driving heightened demand for high-performance energy storage materials in both automotive and stationary systems. As battery and supercapacitor platforms evolve, electrodes must deliver a balance of conductivity, durability, and mechanical stability under high cycling stress. Graphene oxide addresses these challenges by improving charge transport, enhancing structural integrity, and stabilizing electrochemical interfaces, all of which contribute to extended range and faster charging capabilities. As electric mobility and grid storage enter mainstream use, tightening material qualification standards favor additives and coatings that ensure consistent performance across various chemistries and form factors.

From a market perspective, the expansion of battery value chains is creating sustained demand for advanced electrode components. Graphene oxide is becoming integral across cathodes, anodes, and conductive networks, shifting value capture toward suppliers who can deliver scalable, high-quality powders and dispersions. As performance demands rise, the intensity of graphene oxide content per cell strengthens margin resilience and drives long-term demand visibility. Electrification and technology advancements are embedding graphene oxide into core energy storage systems, supporting faster growth than the broader materials market. In July 2025, Argo Graphene Solutions signed a purchase agreement for one metric ton of graphene oxide paste with Ceylon Graphene Technologies, accelerating supply chain development for graphene oxide-based composites and batteries.

Barrier Analysis – High Production Costs and Scale-Up Complexity

Graphene oxide manufacturing remains structurally constrained by capital-intensive chemistries and process complexity, limiting cost competitiveness across high-volume, price-sensitive end markets. Oxidative synthesis routes rely on hazardous reagents, multi-stage purification, and stringent effluent treatment, elevating both fixed investment requirements and ongoing operating expenditure. These process characteristics increase unit cost volatility and expose producers to regulatory scrutiny around chemical handling, waste management, and environmental compliance. In parallel, downstream customers in energy storage, composites, and coatings require narrow specification windows for surface functionality and dispersion behavior, raising qualification thresholds and increasing the economic penalty of off-spec production.

At the value-chain level, scale-up challenges impede consistent supply of uniform flake morphology and reproducible surface chemistry, constraining integration into automated manufacturing lines that depend on tight materials tolerances. Variability across batches disrupts yield optimization in electrode fabrication and composite compounding, translating into higher scrap rates and process inefficiencies for integrators. These reliability and cost uncertainties reinforce segmentation of demand toward premium, low-volume applications where performance premiums absorb higher material input costs, structurally limiting near-term volume expansion relative to broader graphene derivatives with more mature industrial production economics.

Opportunity Analysis – Energy Storage and Electric Vehicle Battery Platforms

Energy storage systems, spanning electric vehicle batteries and stationary grid applications, represent a structurally expanding addressable pool for advanced conductive additives and high-surface-area carbon materials. As lithium-ion and emerging battery chemistries scale to meet electrification and renewable integration requirements, electrode architectures are becoming more performance-intensive, increasing reliance on materials that enhance conductivity, mechanical stability, and interfacial durability. Graphene oxide aligns with these requirements by improving charge transport efficiency and structural reinforcement within anode and cathode matrices, supporting higher energy density and durability under aggressive cycling conditions. This positions energy storage as the most commercially proximate demand engine for graphene oxide deployment across the battery value chain.

From a market-structure perspective, the expansion of cell manufacturing capacity and the industrialization of next-generation chemistries are raising content intensity per unit, favoring additive suppliers capable of delivering consistent, battery-grade materials at scale. Powder-form graphene oxide optimized for electrode integration is emerging as a high-velocity subsegment as manufacturers seek process-compatible inputs that integrate into existing slurry and coating workflows. Value capture is increasingly shaped by qualification depth, supply reliability, and co-development linkages across materials producers, cell manufacturers, and automotive platforms, reinforcing structurally superior growth dynamics relative to broader specialty materials markets.

Biomedical and Healthcare Applications

Biomedical adoption of graphene oxide presents a significant underexplored opportunity as healthcare systems prioritize targeted therapeutics, early diagnostics, and precision monitoring. Functionalized graphene oxide's surface properties enable effective molecular binding and controlled release, making it ideal for drug delivery platforms that require payload stability and site-specific interaction. Its use in biosensing architectures enhances signal sensitivity and response times, meeting the clinical need for rapid pathogen detection and continuous metabolic monitoring. These applications place graphene oxide within regulated medical device and pharmaceutical value chains, where material performance consistency and bio-interface reliability are critical.

From a commercialization perspective, expanding into medical-grade applications shifts upstream production requirements, emphasizing higher purity, traceability, and compliance with biomedical standards, which increases the strategic value of validated supply chains. Regulatory approval processes extend development timelines and raise certification costs, but also create entry barriers that support premium pricing and stronger margins once qualified. As diagnostics and therapeutic delivery increasingly rely on personalized, data-driven care, graphene oxide's versatility embeds it into emerging healthcare technologies, expanding its role across diagnostics, therapeutic carriers, and clinical sensing platforms.

Category-wise Analysis

Manufacturing Method Insights

Hummers’ method is expected to dominate, accounting for approximately 62% share in 2026, underpinned by its entrenched role as the only proven, mass-scale oxidation route across battery materials, coatings, construction additives, and polymer composites. Adoption remains anchored by yield efficiency, tunable oxygen functionality, and cost-effective use of lower-grade graphite, with producers prioritizing standardized chemistries and predictable batch outputs in high-volume manufacturing environments. Ongoing platform evolution, including nitrate-free oxidation, automated reactor control, advanced purification, and closed-loop acid recovery, continues to reinforce capacity expansion and utilization intensity. Vendors such as Graphenea, Sixth Element, and Abalonyx are expanding portfolios with application-tuned dispersions and qualification-ready grades to secure long-term supply agreements.

Green synthesis is expected to be the fastest-growing segment, driven by unmet sustainability requirements and purity constraints across biomedical, food-contact packaging, and electronics use cases. Growth is being catalyzed by technology inflection points such as biomass-derived carbon sources, water-only exfoliation, flash heating, and peroxide-based mild oxidation, which materially improve contaminant control, environmental performance, and processing speed. Accelerating adoption is supported by circular-economy enablers, modular pilot plants, and sustainability reporting frameworks, lowering operational friction for first-time industrial adopters. Companies including Universal Matter, HydroGraph, and Ceylon Graphene Technologies are scaling eco-oriented production platforms and waste-to-carbon supply models to capture early-cycle demand and embed switching costs.

Functionalization Insights

Non-functionalized graphene oxide is expected to dominate, accounting for approximately 54% share, underpinned by its entrenched role as the universal precursor across construction additives, bulk coatings, membranes, and energy materials workflows. Adoption remains anchored by cost efficiency, aqueous dispersibility, and qualification readiness, with producers prioritizing standardized grades and scale economics in high-volume environments. Ongoing platform evolution, including ISO-aligned specifications, high-solids dispersions, and automated purification, continues to reinforce replacement cycles and utilization intensity across industrial supply chains. Vendors such as Sixth Element, Graphenea, and Abalonyx are expanding portfolios with application-tuned dispersions and paste formats to lock in enterprise workflows and long-term offtake contracts.

Amine-functionalized graphene oxide is expected to be the fastest-growing segment, driven by interfacial bonding gaps and performance ceilings of legacy fillers across polymer composites, lightweighting, and sensing applications. Growth is being catalyzed by covalent grafting chemistries, composite process integration, and multifunctional property enablement, which materially improve load transfer, toughness, conductivity, and barrier performance at low filler loadings. Companies including Haydale Graphene, Graphenea, and Sigma-Aldrich are scaling functionalized platforms and composite-ready product lines to capture early-cycle demand and embed switching costs. As qualification pathways mature and composite supply chains standardize, this segment is positioned to outpace overall market growth over the forecast period.

Regional Insights

North America Graphene Oxide Market Trends

North America is expected to retain a structurally high-value position, with the region accounting for roughly 39% of global demand in 2026, driven more by functional performance than by volume throughput. The U.S. is anticipated to remain the core consumption base, supported by advanced electronics, defense, and automotive applications where material qualification thresholds are high. Companies such as Global Graphene Group and NanoXplore illustrate the region’s focus on battery materials and polymer reinforcement, while end users, including Intel, Ford, and Tesla, continue to prioritize high-purity and functionalized grades over commodity output. This positioning is likely to sustain a premium-oriented demand structure rather than a scale-driven one.

Regulatory and institutional frameworks are expected to reinforce this trajectory. DoD procurement programs and grid modernization initiatives are anticipated to support domestic supply chains, while EPA TSCA oversight and evolving FDA pathways for nanomaterials are likely to shape commercialization timelines. The shift toward flash-based production methods and infrastructure materials is expected to proceed cautiously, with quality control norms and standards bodies continuing to anchor adoption in high-specification segments.

Europe Graphene Oxide Market Trends

Europe is expected to remain a mature graphene oxide market, focused on research-to-industry translation rather than large-scale volume production. The region benefits from coordinated industrial policies, particularly the Graphene Flagship, which has advanced the transition from lab development to pilot-line integration in sectors, including semiconductors, advanced materials, and industrial coatings. Germany will continue to drive demand, particularly in automotive and industrial applications, while Spain is set to remain a key supplier of high-purity graphene oxide through producers such as Graphenea. The U.K., led by the University of Manchester and its spin-offs, is likely to remain a critical source of advanced materials IP and downstream commercialization.

Regional demand will continue to prioritize sustainability-focused applications, such as lightweight electric vehicle components for OEMs such as BMW and Mercedes-Benz, and functional materials for aerospace programs led by Airbus. Regulatory oversight and sustainability policies are expected to influence market access more than price competition. REACH registration and ECHA nano-form disclosures will continue to limit low-compliance imports, reinforcing the market position of established suppliers, including Graphenea, Haydale, and Talga Group. The EU Green Deal and circular economy mandates will support ongoing demand for graphene oxide in water treatment, low-carbon construction, and energy-efficient composites, solidifying Europe’s role in high-specification applications without shifting to mass-market production.

Asia Pacific Graphene Oxide Market Trends

Asia Pacific is set to remain the fastest-growing region for graphene oxide, driven by its shift from upstream raw-material supply to integrated manufacturing and application development, particularly in China, South Korea, Japan, and India. China is poised to continue leading the region through its dominance in graphite feedstock and downstream processing. South Korea is likely to strengthen its role in semiconductor and display-related thermal management materials, while India is expected to expand its presence in application-driven sectors such as water treatment and infrastructure coatings, supported by initiatives, including the Graphene Aurora program, which links research funding to commercialization.

Regional demand is bolstered by the concentration of EV battery manufacturing and consumer electronics supply chains, with key players such as CATL, LG Energy Solution, and BYD driving ongoing demand for graphene oxide and reduced graphene oxide (rGO) derivatives. Policy support and industrial organization are expected to influence market structure more than short-term pricing dynamics. China’s export controls on graphite derivatives may shift capacity toward high-value domestic processing, while South Korea’s K-REACH regulations will likely formalize compliance thresholds for nanomaterials. Technological advancements, such as electrochemical exfoliation in Taiwan and wafer-level integration in Japan, will enable firms, including The Sixth Element, LG Chem, and Mojiang Graphene, to benefit from vertical integration and ISO standardization.

Competitive Landscape

The global graphene oxide market is moderately fragmented, led by specialized nanomaterial producers such as Global Graphene Group, Graphenea, and The Sixth Element, which set quality benchmarks and ensure supply reliability through scalable production and expertise. These leaders dominate due to their high-purity output and established relationships with research institutions and industrial adopters.

While key manufacturing hubs remain concentrated, the broader market is competitive, with smaller firms and startups focusing on application-specific niches. Competitive positioning revolves around production capacity, consistency, and purity, with smaller players differentiating through tailored functionalization. The industry is shifting toward consolidation, with increasing partnerships, expansions, and selective acquisitions, though innovation remains decentralized as developers pursue specialized variants.

Key Industry Highlights:

- In December 2025, GMG received US EPA approval for its graphene coating product, derived from GO processes. This enables US market entry, promoting energy-saving coatings that cut HVAC costs by up to 36%.

- In October 2025, NanoXplore unveiled its next-gen GrapheneBlack xGnP product line, incorporating graphene oxide enhancements. The new dry-process product, set for production in early 2026, offers improved dispersion in plastics, boosting conductivity and strength for automotive uses.

- In March 2025, CamGraPhIC secured €25 million (US$26.5 million) funding for graphene-based integrated circuits, leveraging graphene oxide in photonics. This supports commercial scaling of GO-integrated circuits, potentially reducing energy use in AI data transmission by 50%.

Companies Covered in Graphene Oxide Market

- Global Graphene Group

- Graphenea

- The Sixth Element Materials Technology Co., Ltd.

- NanoXplore Inc.

- Haydale Graphene Industries plc

- First Graphene Ltd.

- Abalonyx AS

- ACS Material, LLC

- Versarien plc

- Zen Graphene Solutions (ZEN)

- Garmor Inc.

- Directa Plus plc

- XG Sciences

- CVD Equipment Corporation

- Thomas Swan & Co. Ltd.

- Applied Graphene Materials plc

- Universal Matter Inc.

Frequently Asked Questions

The global graphene oxide market is projected to be valued at US$0.4 billion in 2026 and is expected to reach US$3.1 billion by 2033, driven by its rapid adoption in energy storage, electronics, and advanced composites as production scalability improves.

The shift toward electrification in transport and grid infrastructure creates a structural demand for advanced electrode materials. Graphene oxide enhances battery and supercapacitor performance by improving conductivity, energy density, and charge cycles, making it a critical material for next-generation energy storage systems.

The graphene oxide market is forecast to grow at a CAGR of 34.0% from 2026 to 2033, reflecting its rapid commercialization and expanding high-value applications in electronics and energy storage.

North America is the leading regional market, accounting for approximately 39% share, supported by strong R&D commercialization, a high concentration of advanced materials companies, and early adoption in electronics, aerospace, and defense sectors.

The graphene oxide market is moderately fragmented, with leadership from specialized nanomaterial producers such as Global Graphene Group, Graphenea, and The Sixth Element. These players compete on high-purity, scalable production and established customer relationships, while diversified firms and startups focus on application-specific functionalization and niche markets.