- Power Generation, Transmission, & Distribution

- Molded Case Circuit Breaker Market

Molded Case Circuit Breaker Market Size, Share, and Growth Forecast 2026 - 2033

Molded Case Circuit Breaker Market by Product Type (Miniature, Molded Case), by Power Case (0-100 A, 101-250 A, 251-800 A, Above 800 A), by Pole Type (Single Pole, Double Pole, Triple Pole, Four Pole), End-user (Residential, Commercial, Industrial, Power & Utilities, Data Centers), by Regional Analysis, 2026 - 2033

Molded Case Circuit Breaker Market Size and Trend Analysis

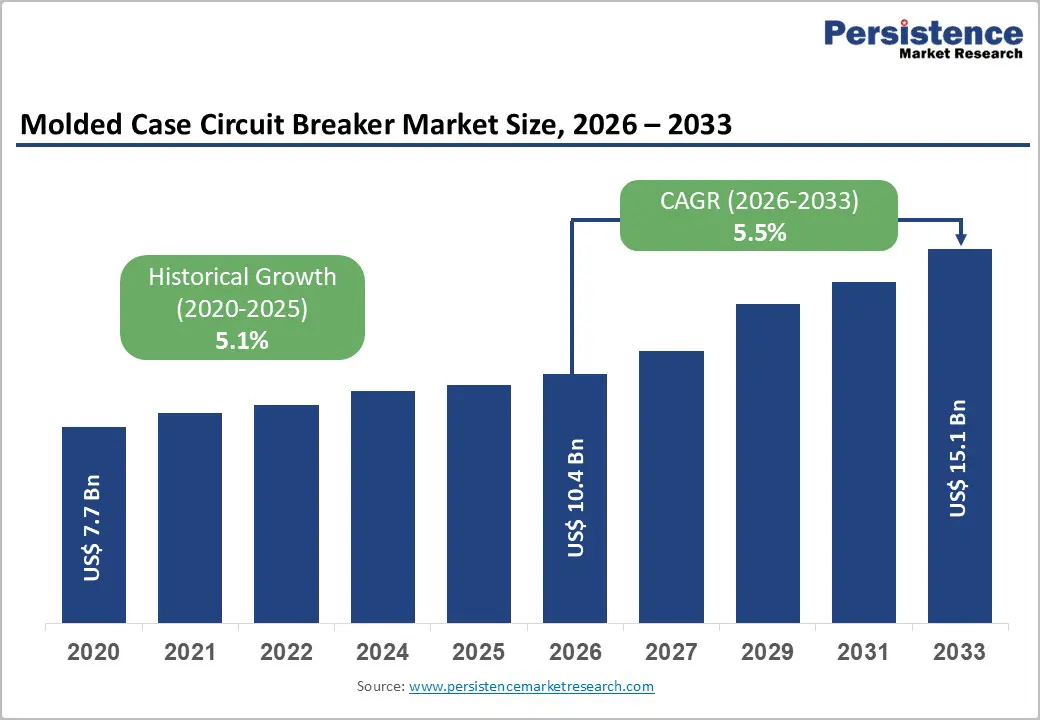

The global molded case circuit breaker market size is expected to be valued at US$ 10.4 billion in 2026 and projected to reach US$ 15.1 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Market expansion is fundamentally driven by the rise in demand for reliable electrical protection infrastructure across industrial, commercial, and utility power distribution systems, coupled with accelerating renewable energy integration and the adoption of smart grid technologies worldwide. The rise in data center infrastructure expansion and mission-critical facilities requiring advanced power protection systems has substantially increased demand for molded-case circuit breakers with enhanced reliability. Growing industrialization in emerging economies, increasing investments in electrical infrastructure modernization, and the proliferation of Internet of Things (IoT) enabled intelligent circuit breakers incorporating real-time monitoring capabilities are significantly propelling market growth across diverse end-use applications.

Key Industry Highlights:

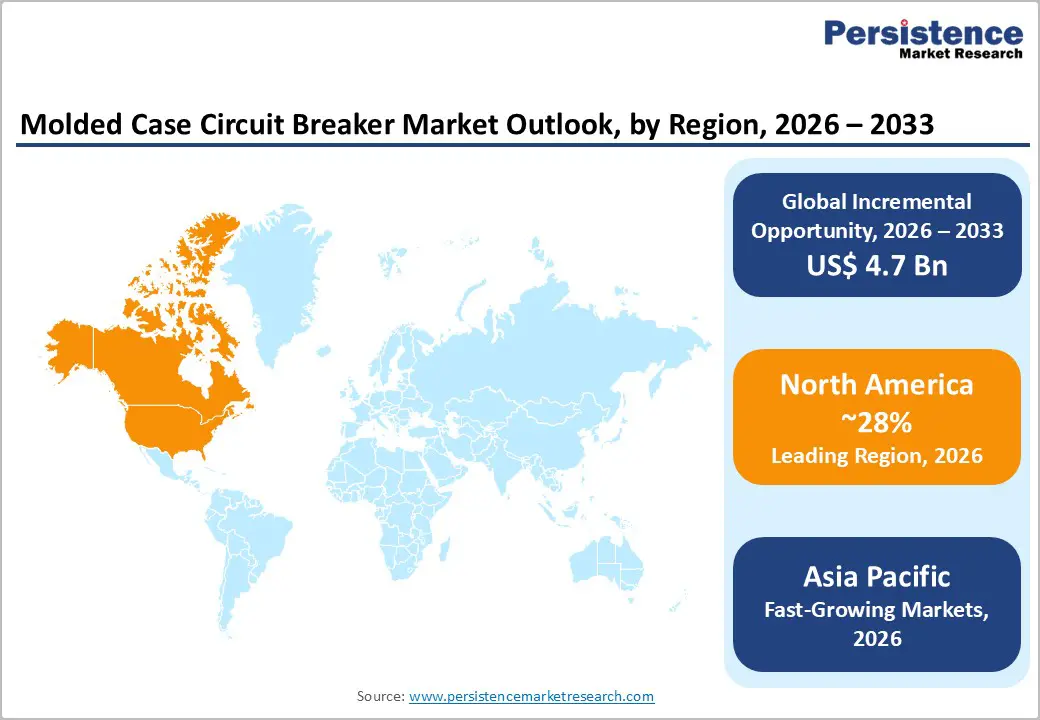

- Leading Region: North America leads the global molded case circuit breaker market with approximately 28% share in 2025, supported by mature industrial infrastructure, advanced power distribution systems, and substantial investments in electrical system modernization and smart grid technology adoption.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, expected to post a CAGR of approximately 6.7% through 2033, driven by rapid industrialization, expansion of electrical infrastructure

- across emerging economies, and government emphasis on power system modernization.

- Dominant Segment by Product Type: Molded Case holds roughly 78% share in 2025, reflecting superior protection capabilities, higher interrupting capacity, and versatility across diverse industrial and commercial applications.

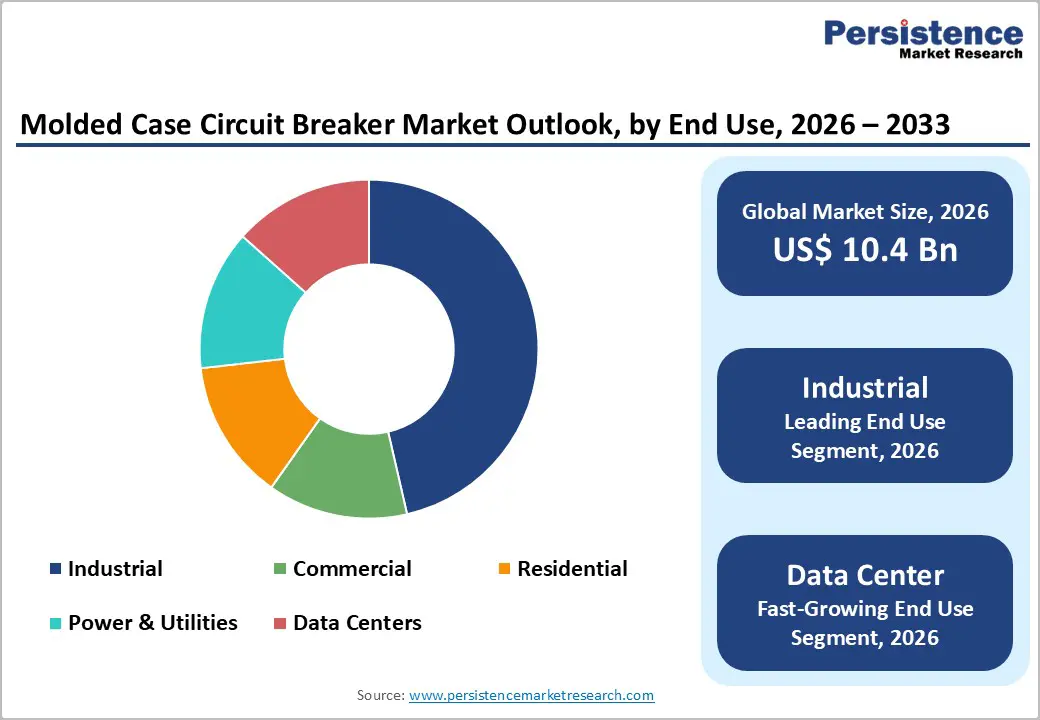

- Fastest Growing Segment from End Use: Data centers is the fastest-growing segment, with an estimated 8.3% CAGR through 2033, fueled by exponential cloud computing adoption and artificial intelligence infrastructure requiring mission-critical power protection.

- Key Opportunity: Renewable energy integration and smart grid modernization initiatives offer significant opportunity for developing advanced circuit breaker solutions optimized for distributed energy resources and autonomous grid management systems.

| Key Insights | Details |

|---|---|

|

Molded Case Circuit Breaker Market Size (2026E) |

US$ 10.4 billion |

|

Market Value Forecast (2033F) |

US$ 15.1 billion |

|

Projected Growth CAGR (2026-2033) |

5.5% |

|

Historical Market Growth (2020-2025) |

5.1% |

Market Dynamics

Market Growth Drivers

Escalating Global Demand for Reliable Electrical Infrastructure and Power Protection Solutions

The exponential growth in global electrical infrastructure requirements is driving sustained demand for molded case circuit breakers as essential components for power protection and distribution systems. As global electrical power consumption continues to rise, driven by industrialization, urbanization, and increasing electrification in emerging economies, demand for advanced circuit protection devices has become critical. Industrial segments increasingly recognize that sophisticated power protection requirements require advanced molded-case circuit breakers capable of handling complex electrical loads and fault conditions.

The International Energy Agency reports that electrical infrastructure investments are accelerating worldwide, with developing nations in Asia, Africa, and Latin America substantially expanding power distribution networks requiring substantial quantities of protective devices. Modern industrial operations, including manufacturing facilities, chemical plants, steel mills, and petrochemical refineries, require robust circuit protection systems that safeguard specialized equipment against overcurrent, short circuits, and complex fault conditions.

Integration of Smart Grid Technology and IoT-Enabled Circuit Breaker Solutions

The rapid advancement of smart grid infrastructure and the emergence of the Internet of Things, which enable circuit breakers, represent transformational growth drivers for the molded case circuit breaker market. Traditional circuit breaker technology is evolving toward intelligent solutions that incorporate real-time monitoring, remote control, and predictive maintenance, enhancing operational efficiency and reliability. According to research on smart grid technology, IoT-enabled circuit breakers fundamentally transform energy management by providing real-time data access, enabling facility operators to make informed decisions and optimize energy consumption and system performance.

Schneider Electric’s innovations in low-voltage circuit breakers include advanced MTZ Active technology, which incorporates smart connectivity, real-time analytics, and artificial intelligence-powered monitoring systems that support predictive maintenance and operational optimization. Integrating smart circuit breakers into automated power distribution systems enables rapid fault detection and automated responses, significantly reducing downtime and improving grid stability. Utilities and facility managers are increasingly recognizing that IoT-enabled circuit breakers provide data-driven insights that support renewable energy integration, energy efficiency optimization, and sustainability objectives, while maintaining enhanced safety standards for personnel and equipment.

Market Restraints

High Initial Capital Investment and Complex Integration Requirements

Molded-case circuit breaker deployment requires substantial capital investment in manufacturing infrastructure, quality assurance systems, and research and development, creating barriers to entry for smaller manufacturers and constraining market expansion. Advanced production facilities incorporating precision manufacturing equipment, automated assembly systems, and comprehensive testing infrastructure require significant upfront capital expenditures often exceeding millions of dollars.

The development of next-generation intelligent circuit breakers incorporating IoT capabilities, advanced materials, and sophisticated electronic components demands substantial research and development investments that smaller manufacturers struggle to justify. Integration of new circuit breaker technologies into existing electrical infrastructure often requires complex coordination with multiple stakeholders, including electrical utilities, equipment manufacturers, and regulatory bodies.

Raw Material Price Volatility and Supply Chain Complexities

Molded case circuit breaker manufacturing depends on specialized materials, including copper windings, insulation compounds, ferromagnetic cores, and electronic components, subject to significant price volatility and intermittent supply constraints. Copper prices have fluctuated substantially, affecting production costs and manufacturers' profitability across the industry. Specialized electronic components required for intelligent circuit breakers face supply constraints exacerbated by semiconductor supply chain disruptions and geopolitical trade tensions.

Manufacturers must maintain substantial raw material inventories and working capital reserves to manage supply chain uncertainties, elevating operational costs. Additionally, the transition to sustainable materials and eco-friendly manufacturing processes requires investment in alternative material sourcing and process development, thereby increasing supply chain complexity for smaller manufacturers that lack diversified supplier networks.

Opportunity

Expansion of Data Center Infrastructure and Mission-Critical Facilities Protection

Significant growth opportunities exist for molded case circuit breaker manufacturers serving the rapidly expanding data center sector, where mission-critical power protection and operational continuity are paramount business requirements. Global data center capacity is expanding substantially, driven by cloud computing adoption, artificial intelligence infrastructure requirements, and digital transformation initiatives across diverse industries. Data centers require advanced circuit protection systems that incorporate high short-circuit capacity, selective tripping, and real-time monitoring to ensure continuous operational stability.

Data centers require specialized molded-case circuit breakers with precise coordination settings to enable seamless fault isolation without affecting adjacent power distribution systems. Manufacturers developing customized circuit breaker solutions optimized for data center environments, incorporating zone-selective interlocking features and remote monitoring capabilities, can establish competitive advantages and capture premium pricing within this high-growth segment. The emphasis on energy efficiency, cooling system optimization, and uninterrupted power supply in data centers creates sustained opportunities for manufacturers offering advanced circuit protection solutions supporting operational reliability and sustainability objectives.

Renewable Energy Integration and Smart Grid Modernization Initiatives

The global transition to renewable energy sources and the modernization of smart grid infrastructure create substantial opportunities for molded case circuit breaker manufacturers to develop advanced solutions optimized for distributed energy resource management and renewable integration. Renewable energy expansion, including solar and wind power installations, requires sophisticated electrical protection systems managing variable power generation characteristics and complex grid integration requirements.

According to the International Renewable Energy Agency, renewable energy capacity is expanding rapidly, requiring parallel investment in supporting electrical infrastructure incorporating advanced circuit protection technologies. Molded case circuit breaker manufacturers investing in technology development optimized for direct current transmission systems, microgrids, and renewable energy applications can access emerging market segments with substantial growth potential. The emphasis on grid automation, distributed energy storage, and enhanced fault detection capabilities creates opportunities to develop next-generation circuit breakers with advanced sensing, communication, and automated control capabilities.

Category-wise Analysis

Product Type Insights

Within the product type category, molded case circuit breakers dominate the market, accounting for approximately 78% share in 2025. Their leadership is driven by superior interrupting capacity, robust construction, and suitability for high-power industrial and commercial applications. Molded case units provide reliable protection against overloads and short circuits while offering adjustable trip settings that enable precise coordination for specific operational requirements. These breakers are widely deployed in manufacturing plants, power distribution panels, utilities, and large commercial buildings where system reliability and safety are critical. Their ability to handle demanding fault conditions and support diverse voltage and current requirements reinforces strong adoption across core infrastructure applications, positioning molded case breakers as the standard solution for medium- to high-capacity electrical protection systems.

Power Case Insights

The 101–250 A power case rating is the leading segment, capturing approximately 42% of the market in 2025 due to its broad applicability and balanced performance profile. This amperage range effectively meets the protection needs of medium-scale industrial and commercial installations, including motors, transformers, and feeder circuits. End users favor this segment for its cost-effectiveness, operational reliability, and compatibility with diverse electrical loads. The 101–250 A rating is widely used in manufacturing facilities, commercial complexes, and distribution networks, where reliable overcurrent protection is essential. Its versatility and proven performance across varied applications continue to sustain strong demand within core industrial and infrastructure environments.

Pole Type Insights

Three-pole molded-case circuit breakers dominate the pole-type category, holding approximately 48% market share in 2025. This dominance reflects the widespread use of three-phase power systems in industrial and commercial electrical infrastructure. Three-pole configurations provide balanced and comprehensive protection across all phases, making them essential for machinery, motors, and large building systems. Their long-established reliability and compatibility with standard industrial power architectures support consistent demand. Three-pole breakers are integral to manufacturing plants, utility distribution systems, and commercial installations, where stable three-phase power delivery and protection are critical for safe and continuous operations.

End-use Insights

The industrial segment leads end-use demand, accounting for roughly 45% of the market in 2025, driven by the need for robust electrical protection in high-load and mission-critical environments. Industrial facilities require molded-case circuit breakers capable of handling high fault currents, complex load profiles, and continuous operation. Applications span heavy manufacturing, process industries, and equipment-intensive operations, where electrical failures can lead to costly downtime and safety risks. The increasing focus on operational reliability, equipment protection, and compliance with safety standards continues to drive strong adoption of molded case circuit breakers among industrial end users.

Regional Insights

North America Molded Case Circuit Breaker Market Trends and Insights

North America commands approximately 28% global market share in 2025, supported by mature industrial base, advanced power distribution infrastructure, and substantial investments in electrical system modernization and smart grid technology adoption. The United States represents the region’s primary market, with extensive industrial manufacturing capacity, established utility infrastructure, and continuous investment in power system upgrades supporting sustained demand for advanced circuit protection solutions. Major electrical equipment manufacturers including Eaton, Rockwell Automation, and Siemens maintain significant manufacturing and research capabilities in North America supporting product innovation and market leadership.

North American utilities are investing in smart grid infrastructure and renewable energy integration, driving demand for advanced molded-case circuit breakers with enhanced monitoring and control capabilities. The emphasis on operational reliability, system resilience, and regulatory compliance across North American electrical networks supports premium positioning for manufacturers offering advanced circuit protection solutions. Industrial automation initiatives and the expansion of data center infrastructure throughout North America create sustained opportunities for circuit breaker manufacturers offering specialized solutions optimized for mission-critical applications and complex electrical environments.

Europe Molded Case Circuit Breaker Market Trends and Insights

Europe is a significant market, accounting for approximately 26% of the global market in 2025, characterized by an emphasis on energy efficiency, sustainable infrastructure development, and stringent electrical safety regulations. Germany, the United Kingdom, France, and Spain maintain robust industrial bases, with substantial power-distribution requirements that support sustained demand for advanced circuit protection systems. European manufacturers, including Schneider Electric and Siemens AG, leverage advanced technology capabilities and established relationships with industrial customers, supporting market leadership across the region.

European regulatory frameworks emphasizing environmental sustainability and energy efficiency drive the adoption of advanced circuit breakers incorporating intelligent features supporting reduced energy consumption and operational optimization. The emphasis on renewable energy integration and grid modernization across the European Union creates sustained opportunities for manufacturers developing solutions optimized for distributed energy resources and smart grid applications. Europe’s industrial sector modernization initiatives and commercial infrastructure development support continued demand for reliable circuit protection systems across diverse applications.

Asia Pacific Molded Case Circuit Breaker Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, projected to expand at approximately 6.7% CAGR through 2033, driven by rapid industrialization, accelerating urbanization, and massive investments in electrical infrastructure development across emerging economies, including China, India, and Southeast Asia. China is the largest market, with extensive manufacturing capacity and growing domestic consumption, driven by industrial expansion and modernization of power distribution networks. India demonstrates substantial market potential, with a projected 4.2% CAGR through 2033, driven by expanding electrical infrastructure requirements, industrial development initiatives, and growing recognition of the importance of advanced protection systems for operational reliability.

Japan maintains technological leadership in advanced circuit breaker development, with manufacturers such as Mitsubishi Electric and Fuji Electric driving innovation and the export of specialized solutions. The region’s manufacturing advantages, including cost-effective production and established supply chains, position Asia Pacific as the center for global molded case circuit breaker manufacturing and distribution. Rapid urbanization across the region, rising electricity consumption in developing economies, and government emphasis on infrastructure modernization create substantial opportunities for manufacturers offering cost-effective solutions that meet regional requirements and performance specifications.

Competitive Landscape

The global molded case circuit breaker market is moderately consolidated, with large integrated manufacturers alongside regionally focused and application-specific players. Market leadership is driven by scale advantages, vertically integrated manufacturing, broad product portfolios, and well-established distribution networks serving industrial, commercial, and utility customers. Business strategies increasingly center on technology differentiation, with strong emphasis on intelligent protection systems, digital monitoring, and compatibility with smart grid and renewable energy applications.

Companies are prioritizing research and development to enhance reliability, safety standards, and breaking capacity performance while supporting compliance with evolving regulations. Customization and application-specific design have become important competitive levers, particularly in infrastructure, data centers, and energy projects. Additionally, service capabilities, lifecycle support, and robust after-sales networks reinforce long-term customer relationships. Emerging and regional players compete by targeting niche end-use sectors, offering tailored solutions, and leveraging local market knowledge to gain share within specific geographies.

Key Developments:

- April 2024: Schneider Electric launched the GoPact MCCB, a new range of molded-case circuit breakers rated up to 800A for simple applications. Compliant with IEC standards, it offers robust, reliable protection at an affordable price with a comprehensive accessory portfolio.

- October 2024: Schneider Electric introduced MasterPacT MTZ Active, an advanced circuit breaker featuring real-time energy monitoring, Native ERMs for arc flash protection, QR code diagnostics for rapid fault resolution, and a refurbishable design promoting circularity to boost safety, efficiency, and sustainable energy management.

- February 2025: Lauritz Knudsen launched innovative electrical solutions at ELECRAMA 2025, including Dsine DZ MCCB for renewables, enConnect home automation, numerical protection relays, EV charging ecosystem with apps, and smart irrigation systems for agriculture.

- February 2025: Eaton debuted the 9395 XR UPS system and LV to MV switchgear solutions, including ACBs and MCCBs, at ELECRAMA 2025, targeting data centers, renewable energy, and industrial applications with a focus on efficiency, sustainability, and Make in India.

Companies Covered in Molded Case Circuit Breaker Market

- Mitsubishi Electric Corporation

- Fuji Electric FA Components & Systems Co., Ltd.

- Schneider Electric

- Siemens AG

- Hitachi Industrial Equipment Systems Co., Ltd.

- Rockwell Automation Inc.

- Legrand

- Eaton

- Powell Industries Inc.

- Havells India Ltd.

- ABB Ltd.

- Hubbell Electrical Products

- Toshiba Corporation

- General Electric Company

Frequently Asked Questions

The market is projected to reach approximately US$ 10.4 billion in 2026.

Rising demand for reliable electrical protection, data center expansion, smart grid adoption, and renewable energy integration are the key drivers.

North America leads the market with around 28% share in 2025.

Renewable energy integration and smart grid modernization present the most attractive opportunities.

Key players include Schneider Electric, Siemens AG, Eaton, Mitsubishi Electric, Rockwell Automation, Legrand, Havells India, Fuji Electric, Hitachi, and Powell Industries, among others.