- Telecommunications

- Mobile Handset Protection Market

Mobile Handset Protection Market Size, Share, and Growth Forecast 2026 - 2033

The global Mobile Handset Protection Market by Protection Provider (Mobile Operator/Carrier, Mobile Device OEM, Direct-to-Consumer Services, Other Channel (Retailers)), by Pricing Model (One Time Fee, Monthly Fee, Billed By Carrier/OEM), by Sales Channel (Retail Chains, Brand Stores, E-Commerce/Online), by Regional Analysis, 2026-2033

Mobile Handset Protection Market Size and Trend Analysis

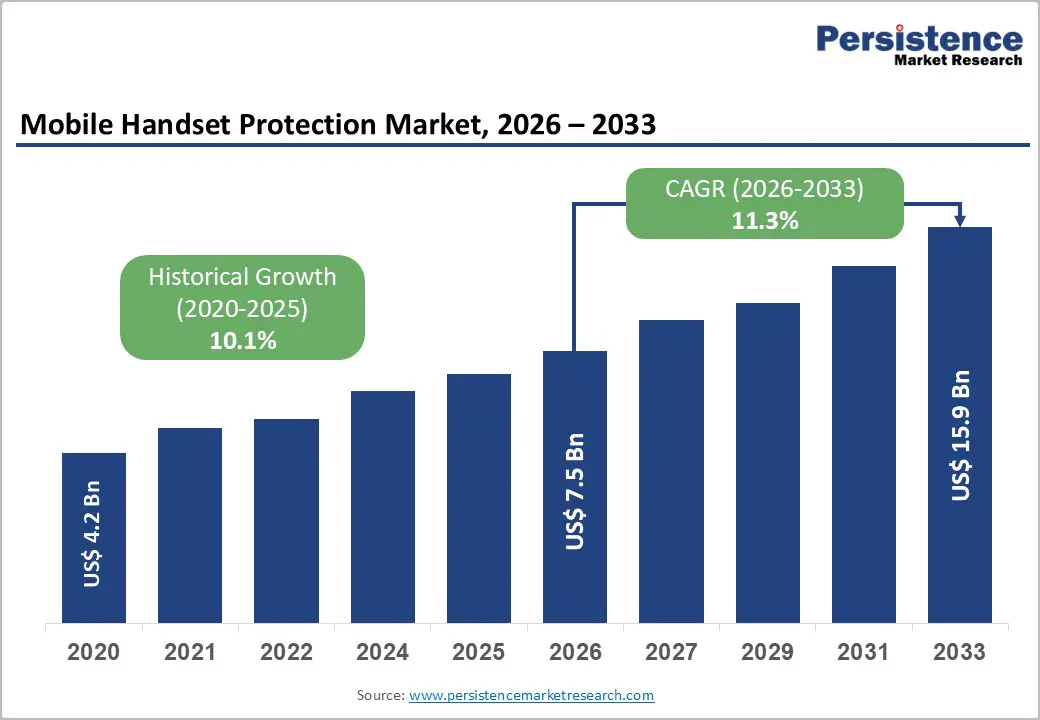

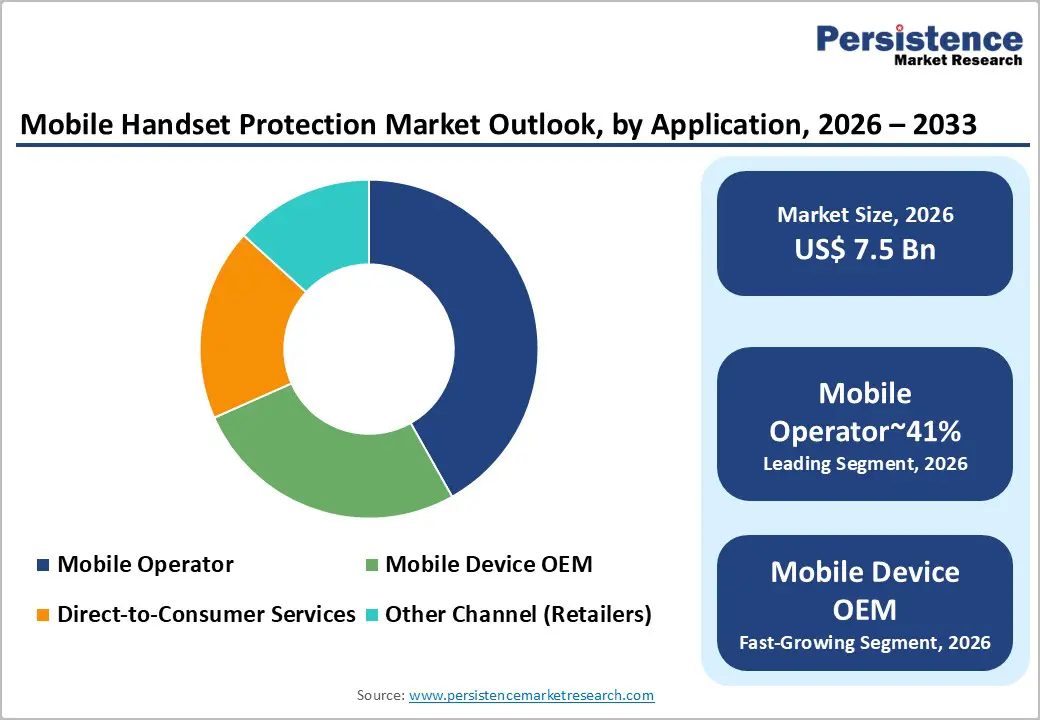

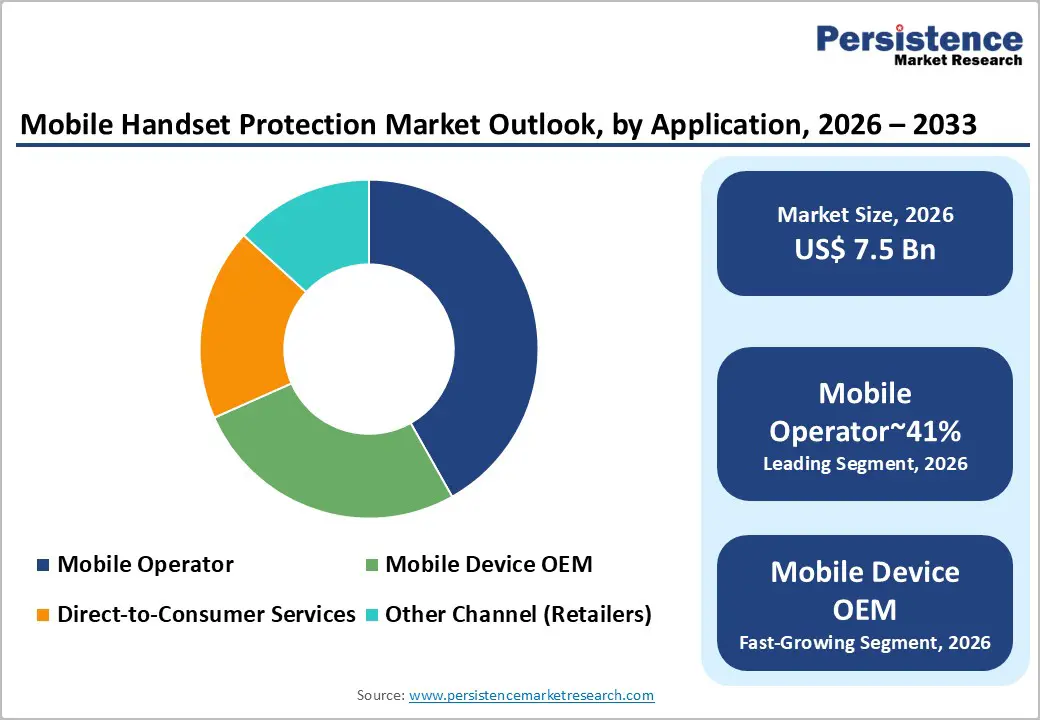

The global mobile handset protection market size is likely to be valued at US$ 7.5 Billion in 2026 and is expected to reach US$ 15.9 Billion by 2033, growing at a CAGR of 11.3% during the forecast period from 2026 and 2033. This robust expansion reflects accelerating smartphone adoption worldwide.

Key Market Highlights

- North America leads the Mobile Handset Protection Market with 38.8% share, driven by high smartphone penetration and carrier-led bundling innovations.

- Asia Pacific emerges as the fastest-growing region at 12.5% CAGR, propelled by China and India premium device adoption and digital infrastructure investments.

- Mobile Operator/Carrier dominates Protection Provider category with 41% share, benefiting from seamless billing integration and point-of-sale enrollment.

- E-Commerce/Online leads Sales Channel growth at 16.8% CAGR, capturing 38% share through AI recommendations and instant digital activation.

- Cybersecurity-integrated protection plans offer key opportunity, addressing 82% rise in mobile threats and creating $2.1 billion revenue potential by 2030.

| Key Insights | Details |

|---|---|

| Mobile Handset Protection Market Size (2026E) | US$ 7.5 Bn |

| Market Value Forecast (2033F) | US$ 15.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.1% |

Market Dynamics

Market Growth Drivers

Escalating Smartphone Penetration and Premium Device Adoption

The global smartphone user base surpassed 6.8 billion in 2024, representing 85% of the world's population, according to international telecommunications data. This unprecedented penetration has created a massive addressable market for protection services. The premium smartphone segment, defined as devices priced above $600, now accounts for 46.7% of global shipments, up from 35% in 2020. These high-value devices, featuring advanced ceramic shields, titanium frames, and sophisticated camera systems, carry repair costs that can exceed 40% of the original purchase price.

iPhone users are 3.5 times more likely to purchase protection plans compared to mid-range device owners, with AppleCare+ services generating over $9 billion in annual revenue. The increasing sophistication of smartphone technology, including 5G connectivity, foldable displays, and AI-powered features, has elevated replacement costs, making comprehensive protection economically rational for consumers. Mobile carriers have capitalized on this trend, with Verizon, AT&T, and T-Mobile reporting that 68% of premium device purchases include bundled protection plans at point-of-sale.

Rising Incidence of Device Damage and Theft

Statistical data from law enforcement agencies indicates that 1.2 million smartphones are stolen annually in the United States alone, while accidental damage affects 30% of smartphone users within the first year of ownership. The Bureau of Justice Assistance reports that smartphone theft accounts for 40% of all property crimes in major metropolitan areas. Physical damage, particularly screen cracks and water exposure, remains the most common issue, affecting 45 million devices globally each year. The average cost of screen repair for premium devices has increased by 85% since 2020, reaching $329 for flagship models.

This risk landscape has driven consumer awareness, with 78% of smartphone owners now recognizing the financial vulnerability of device loss. Insurance providers have responded by expanding coverage to include accidental damage, liquid spills, and mechanical breakdown, with Asurion processing over 50 million claims annually. The integration of Internet of Things (IoT) technology in modern devices has further complicated repair processes, increasing average claim values by 23% year-over-year.

Market Restraints

High Premium Costs and Consumer Price Sensitivity

Despite growing awareness, 42% of smartphone users cite high premium costs as the primary barrier to purchasing protection plans, according to consumer surveys. Monthly premiums for comprehensive coverage range from $8 to $19 per device, representing a significant recurring expense for budget-conscious consumers. In developing economies, where average monthly incomes remain below $500, protection plan adoption rates are merely 12%, compared to 58% in developed markets. The price sensitivity is particularly acute among Gen Z and millennial demographics, with 67% indicating willingness to accept device risk rather than pay insurance premiums.

This constraint is amplified by economic uncertainties, with inflation rates exceeding 5% in major economies during 2023-2024, forcing consumers to prioritize essential expenses over discretionary protection services. Insurance providers face margin pressures as claim frequencies rise, with loss ratios reaching 72% for some carriers, limiting their ability to reduce premiums. The challenge is exacerbated by the proliferation of unauthorized third-party repair services offering screen replacements at 60% lower costs than manufacturer-authorized repairs, undermining the value proposition of official protection plans.

Complex Claims Processes and Regulatory Hurdles

The mobile handset protection industry faces significant operational challenges, with average claim processing times extending to 7-10 business days due to verification requirements and repair logistics. Consumer Financial Protection Bureau data reveals that 23% of protection plan complaints involve claim denials based on ambiguous terms and conditions. Regulatory fragmentation across jurisdictions creates compliance complexities, with 47 different state-level insurance regulations in the U.S. alone requiring customized policy structures.

The European Insurance and Occupational Pensions Authority has implemented stringent consumer protection directives that increased administrative costs by 18% for providers operating in the region. Additionally, the lack of standardized damage assessment protocols leads to disputes, with 15% of claims requiring third-party arbitration. Fraudulent claims, estimated at 8% of total submissions, necessitate robust verification systems that inadvertently delay legitimate claims processing. These operational inefficiencies result in customer satisfaction scores averaging 3.2 out of 5 stars for traditional insurance providers, compared to 4.5 stars for digital-native platforms.

Market Opportunities

Expansion in Emerging Markets and 5G Ecosystem Integration

The Asia Pacific region presents a $4.3 billion opportunity by 2030, driven by India and China adding 78 million new smartphone users annually. India's smartphone insurance market is projected to grow from $140 million in 2020 to $500 million by 2025, representing a 29% CAGR. This growth is fueled by rising disposable incomes, with the middle class expanding by 15% annually, and increasing device costs as 5G adoption accelerates. The Chinese market, valued at $1.8 billion in 2024, is experiencing rapid digitalization of insurance distribution through platforms like Alipay and WeChat Pay, which have integrated micro-insurance products with premiums as low as $1.50 per month.

The rollout of 5G networks, covering 65% of the global population by 2027, is creating new protection needs as devices become more complex and expensive. Telecom operators are uniquely positioned to capture this opportunity, with Jio and Airtel in India already bundling protection plans with 5G service packages, achieving 35% attachment rates. The opportunity extends to Latin America, where smartphone penetration is forecast to reach 75% by 2028, creating a $1.2 billion addressable market.

Innovation in Cybersecurity and AI-Driven Protection Services

The convergence of mobile handset protection with cybersecurity presents a $2.1 billion incremental revenue opportunity by 2030. Modern smartphones store sensitive financial data, with 82% of users conducting mobile banking, making them prime targets for cyberattacks. Zimperium's 2024 Global Mobile Threat Report reveals that 82% of phishing attacks specifically target mobile devices, while malicious apps have increased by 156% year-over-year. This threat landscape is driving demand for integrated protection plans that combine physical damage coverage with AI-powered threat detection, identity theft monitoring, and remote data wipe capabilities.

Apple has pioneered this approach with AppleCare+ now including iCloud security features and Find My network protection. Asurion has invested $200 million in AI-driven diagnostics that can predict device failures 72 hours before occurrence, enabling proactive customer outreach. The emergence of foldable devices, projected to capture 15% of the premium market by 2027, requires specialized coverage for unique failure modes, creating premium-tier products with 30% higher margins. Blockchain technology is being piloted for transparent claims processing, reducing fraud by 40% and processing times by 60%.

Category-wise Insights

Protection Provider Analysis

Mobile Operator/Carrier dominates the distribution landscape, commanding 41.2% market share in 2024 due to strategic advantages in customer acquisition and billing integration. Verizon, AT&T, and T-Mobile have embedded protection plans into their device financing programs, achieving 68% attachment rates for premium smartphones. These carriers leverage their 300 million combined subscriber base and point-of-sale presence to offer seamless enrollment, with premiums bundled into monthly service bills. The carrier model benefits from proprietary device usage data, enabling personalized pricing and risk assessment.

AT&T reported that Mobile Protection Pack subscribers have 23% higher lifetime value than non-subscribers, justifying the $13 average monthly premium. The segment's growth is propelled by 5G device launches, with carriers offering promotional free protection periods for 90 days to drive adoption. However, regulatory scrutiny is increasing, with the Federal Communications Commission examining automatic enrollment practices. Despite this, the carrier channel is projected to maintain 38% market share through 2033, supported by IoT device expansion and enterprise fleet management services.

Pricing Model Analysis

Monthly Fee structures represent the dominant pricing model, capturing 67% of the market in 2024, driven by consumer preference for predictable, low-cost payments. This model aligns with subscription economy trends, with 78% of consumers preferring monthly premiums averaging $11 over one-time fees exceeding $150. Verizon Mobile Protect charges $17 monthly, while AppleCare+ monthly plans start at $9.99, making premium protection accessible. The monthly model reduces purchase friction, with e-commerce platforms reporting 45% higher conversion rates compared to one-time fee presentations.

Carriers benefit from reduced churn, as insured customers show 18% lower attrition rates. The model's success is evidenced by SquareTrade's data showing 72% renewal rates for monthly subscribers versus 45% for annual purchasers. However, regulatory changes in California and New York now require clear disclosure of total annual costs, impacting marketing strategies. The Billed By Carrier/OEM sub-segment is growing at 14.2% CAGR, as Samsung Care+ and Google Preferred Care integrate directly into device purchase flows, eliminating separate payment friction.

Sales Channel Analysis

E-Commerce/Online channels are the fastest-growing distribution method, expanding at 16.8% CAGR and capturing 38% of the market in 2024. Amazon, Best Buy, and manufacturer direct-to-consumer sites have revolutionized protection plan distribution through AI-driven recommendations and instant digital enrollment. Amazon's partnership with Asurion enables one-click protection addition during device checkout, achieving 52% attachment rates. The online channel benefits from detailed product comparisons, customer reviews averaging 4.3 stars, and instant policy activation.

Best Buy's Totaltech program bundles protection with other services, driving $2.1 billion in protection revenue. The shift to online is accelerated by Gen Z and millennial consumers, with 83% preferring digital purchase journeys. Social media advertising generates $340 million in annual protection plan sales, with Instagram and TikTok campaigns achieving 6.8% conversion rates. Despite growth, online channels face challenges from fraudulent sellers, prompting Federal Trade Commission interventions. The channel is projected to reach 45% market share by 2033, supported by augmented reality tools that simulate damage scenarios to educate consumers.

Regional Insights

North America Mobile Handset Protection Trends

North America maintains market leadership, accounting for 38.8% of global revenue in 2024, driven by 90% smartphone penetration and high premium device adoption. The U.S. market alone generated $2.9 billion in protection revenue, with Verizon, AT&T, and T-Mobile controlling 65% of distribution. Regulatory frameworks, including state insurance commissioners and the National Association of Insurance Commissioners, provide consumer protection while enabling market innovation. The Bureau of Justice Assistance reports 1.2 million annual smartphone thefts, driving demand for comprehensive coverage.

Apple dominates the premium segment, with AppleCare+ covering 42% of iPhone users, while Asurion processes 25 million claims annually for carrier partners. The region's mature ecosystem supports advanced offerings, including cybersecurity bundles and AI-powered diagnostics. Canada shows 12% annual growth, with Rogers and Bell expanding protection portfolios. Enterprise adoption is rising, with 70% of Fortune 500 companies implementing device protection programs. The market is characterized by high consumer awareness, with 78% of smartphone owners considering protection essential for devices costing over $800.

Europe Mobile Handset Protection Trends

Europe represents 24% of the global market, valued at $1.8 billion in 2024, with Germany, the U.K., and France driving 68% of regional revenue. The European Insurance and Occupational Pensions Authority has harmonized regulations across 27 member states, reducing compliance costs by 15% for pan-European providers. Germany leads with $620 million in protection sales. Allianz and other insurers offer AI-based fraud protection, enhancing consumer trust amid rising theft rates. The U.K. demonstrates strong performance, with Vodafone and EE expanding coverage to include cybersecurity features, driven by GDPR compliance.

France emphasizes sustainability, promoting refurbished phone protection amid 5G and foldable device launches. Spain and Italy show steady growth through operators like Telefónica and TIM, focusing on theft protection and cyber coverage. The ENISA reports 45% increase in mobile malware attacks, spurring integrated protection demand. Regional harmonization under EIOPA directives has reduced compliance costs by 15%, enabling pan-European offerings. The refurbished smartphone market, supported by circular economy programs, has boosted extended warranty sales by 22%. Southern Europe benefits from rising e-commerce, with 30% of consumers experiencing virus issues per Eurostat. Overall, Europe exhibits 6.7% CAGR, balancing regulatory rigor with innovation.

Asia Pacific Mobile Handset Protection Trends

Asia Pacific commands 29% global market share, fueled by explosive smartphone growth in China, India, Japan, and ASEAN nations. China leads with 30.3% regional share, where 90% urban households own smartphones, per Ministry of Industry and Information Technology. Premium device adoption exceeds 65% in urban areas, driving demand for comprehensive coverage via platforms like Alipay. India follows at 18.6% share, with 60% first-time users purchasing insurance amid 25% penetration growth projected by 2030, according to Ministry of Electronics and Information Technology. Japan focuses on data privacy, with Financial Services Agency promoting new device plans that reduce repair costs by 60%.

ASEAN leverages manufacturing advantages, with Indonesia and Vietnam expanding micro-insurance for middle-class consumers. The Asian Development Bank notes $1 trillion annual digital infrastructure investment, creating scalable solutions. 5G rollout covers 70% of urban areas, necessitating protection for high-end devices. E-commerce bundling achieves 45% attachment rates, while refurbished markets grow 20% annually.

Competitive Landscape

Market Structure Analysis

The Mobile Handset Protection Market exhibits a moderately consolidated structure, with the top 10 players controlling 62% share through carrier partnerships and OEM integrations. Asurion and SquareTrade dominate claims processing, leveraging AI for fraud detection and diagnostics. Companies pursue expansion via M&A, such as Asurion's acquisition of D&G for European scale, and R&D in cybersecurity bundles. Key differentiators include 24/7 support, instant claims via apps, and sustainability-focused refurbished coverage.

Emerging models emphasize embedded insurance at purchase, subscription flexibility, and IoT integration for predictive repairs, shifting from reactive to proactive protection. Carriers like AT&T and Verizon drive 58% volume through bundled offerings, while OEMs innovate with tiered pricing. The landscape favors incumbents with scale, though digital disruptors gain via e-commerce penetration.

Key Market Developments

- July 2025: Asurion launched anytime trade-in program with Cricket Wireless, enhancing device lifecycle management and customer retention through seamless protection and upgrade services.

- October 2025: AT&T updated Protect Advantage plan, expanding coverage for new enrollments with improved benefits for accidental damage and theft protection.

- December 2025: Asurion acquired D&G for £2.1 billion, bolstering European warranty capabilities and integrating advanced tech care solutions across markets.

Companies Covered in Mobile Handset Protection Market

- American International Group, Inc.

- Apple Inc.

- Asurion LLC

- AT&T Mobility

- Best Buy Inc.

- Verizon Wireless

- Liberty Mutual Holding Company Inc

- Sprint Corp.

- Squaretrade,Inc.

- T-Mobile, Inc.

- Others.

Frequently Asked Questions

The market is expected to grow from US$ 7.5 Billion in 2026 to US$ 15.9 Billion by 2033, at a CAGR of 11.3%, driven by premium smartphone adoption and rising repair costs.

Key drivers include 6.8 billion global smartphone users and 30% annual damage incidence, with premium devices exceeding $1,000 and screen repairs at $329, compelling bundled protection purchases.

Mobile Operator/Carrier holds 41% share, leveraging 300 million subscribers and 68% attachment rates through integrated billing and point-of-sale offerings.

North America dominates with 38.8% share, supported by 90% smartphone penetration, 1.2 million annual thefts, and innovations from Verizon and Asurion.

Cybersecurity integration offers $2.1 billion potential, addressing 156% rise in malicious apps and 82% phishing attacks via AI-driven threat detection.

Leading companies include Asurion LLC, SquareTrade, Inc., Apple Inc., AT&T Mobility, Verizon Wireless, and T-Mobile, Inc., controlling 62% share through partnerships and innovations.