- Beauty & Personal Care

- Mineral Sunscreen Market

Mineral Sunscreen Market Size, Share, and Growth Forecast 2026 - 2033

Mineral Sunscreen by Form (Creams, Lotions, Sticks, Gels, Others), by SPF Range (SPF 15-30, SPF 30-50, SPF 50+), by Skin Type (Dry, Oily, Sensitive), End-user (Male, Female, Unisex), by Distribution Channel (Pharmacies & Drugstores, Supermarkets / Hypermarkets, Specialty Beauty Stores, Online), and Regional Analysis, 2026 - 2033

Mineral Sunscreen Market Size and Trend Analysis

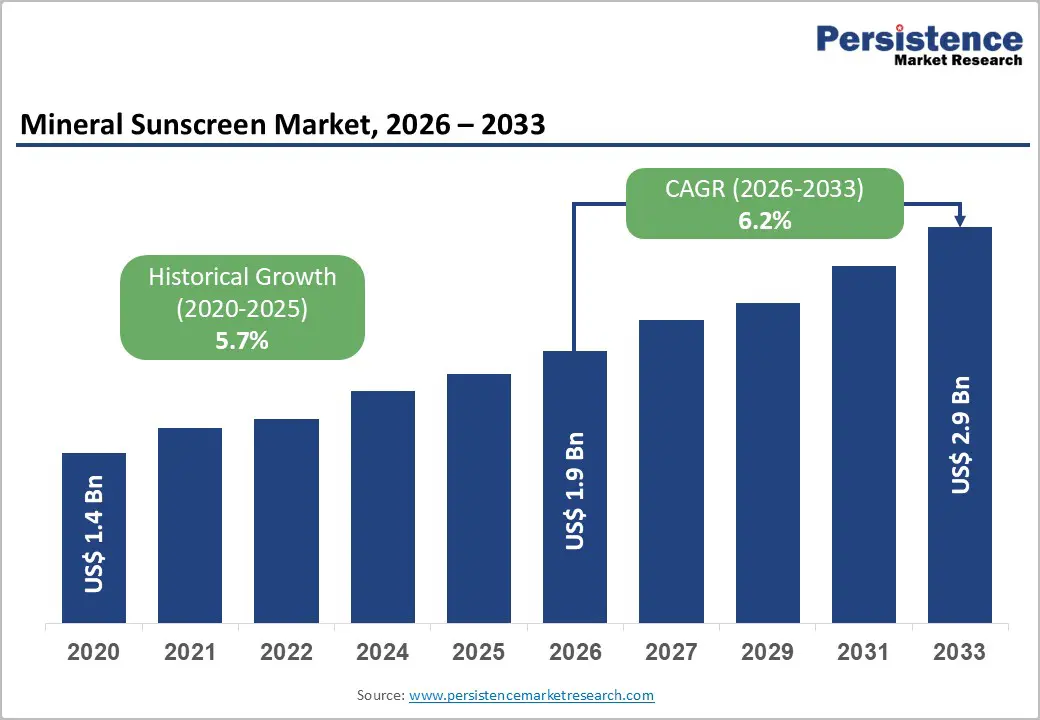

The global mineral sunscreen market size is expected to be valued at approximately US$ 1.9 billion in 2026 and is forecast to reach around US$ 2.9 billion by 2033, growing at a CAGR of 6.2% during the forecast period.

Market expansion is driven by rising awareness of UV radiation risks and increasing skin cancer incidence, prompting consumers to adopt preventive skincare practices, with dermatologists strongly recommending daily SPF 30+ use. In parallel, the clean beauty movement is accelerating demand for mineral-based sunscreens formulated with zinc oxide and titanium dioxide, perceived as safer alternatives to chemical filters. Additionally, stringent regulatory measures, including reef-safe mandates and EU cosmetic regulations, are redirecting demand toward compliant mineral sunscreen solutions.

Key Industry Highlights:

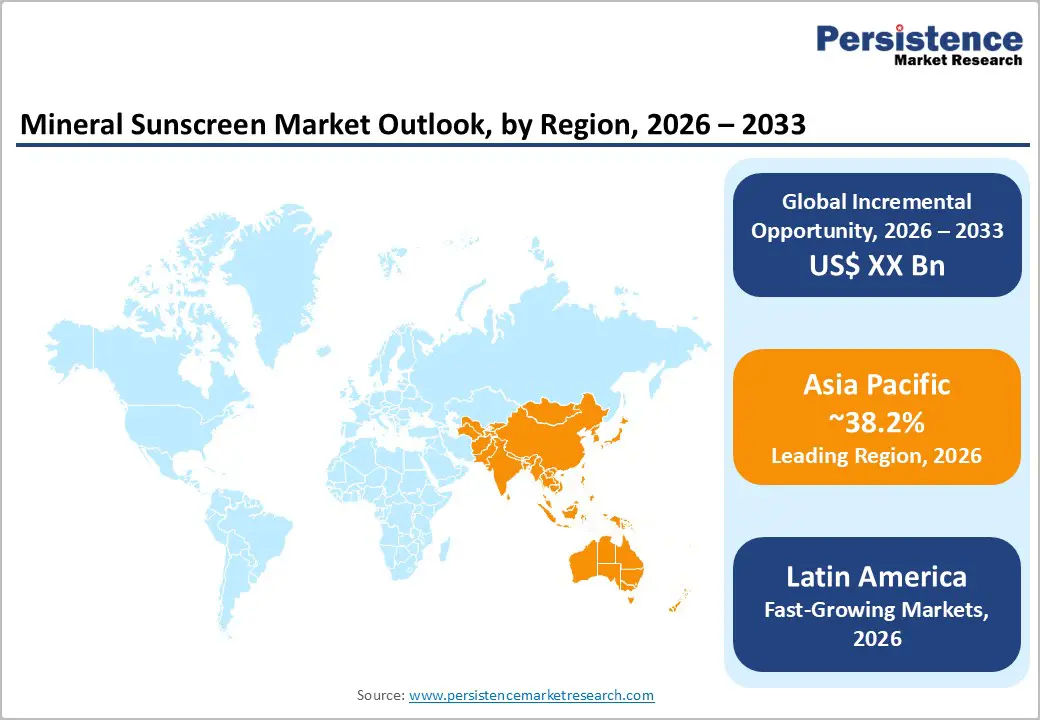

- Leading Region: Asia Pacific leads the global mineral sunscreen market with approximately 38.2% share in 2024, supported by urbanization, rising incomes, diverse skin tone considerations, and growing environmental awareness across China, Japan, and India.

- Fastest Growing Region: Latin America shows the highest growth, expanding at 13.9% CAGR from 2025 - 2030, driven by rising middle-class wealth, increased outdoor activity, and Brazil emerging as the regional market leader.

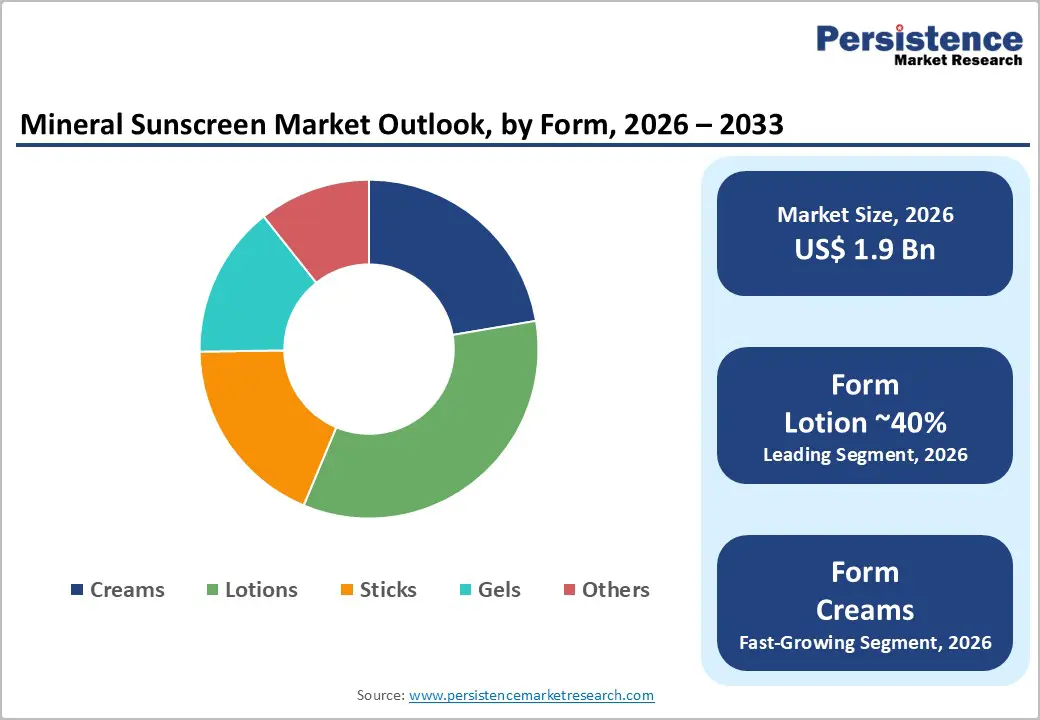

- Dominant Segment from Any Category: Lotion formulations hold around 40% market share, favored for cosmetic elegance, ease of use, and premium dermatologist-backed positioning.

- Fastest Growing Segment from Any Category: SPF 50+ products capture roughly 35% share, driven by sensitive skin needs, outdoor enthusiasts, and high-UV-exposure regions.

- Key Market Opportunity: E-commerce and digital channels grow fastest (25-30% CAGR), enabling direct engagement, transparency, and brand loyalty among younger, sustainability-conscious consumers.

| Key Insights | Details |

|---|---|

| Mineral Sunscreen Market Size (2026E) | US$ 1.9 Billion |

| Market Value Forecast (2033F) | US$ 2.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 5.7% |

Market Dynamics

Drivers - Rising Consumer Awareness of Skin Health Risks and Environmental Protection Standards

Consumer education campaigns, dermatology-led awareness programs, and digital health platforms have significantly elevated understanding of photoaging, melanoma, and non-melanoma skin cancers associated with prolonged UV exposure. Public health messaging increasingly promotes daily sunscreen use as a preventive skincare essential rather than a seasonal product. Social media influencers and dermatology professionals have further normalized mineral sunscreen adoption across age groups by emphasizing safety, gentleness, and daily usability.

Parallel to health awareness, environmental protection concerns are reshaping purchasing behavior. Regulatory actions such as Hawaii’s reef-safe sunscreen legislation and local bans on coral-harming chemical filters have reinforced mineral sunscreens as environmentally responsible alternatives. A measurable share of U.S. consumers now actively prefer mineral formulations, associating them with sustainability, ingredient transparency, and reduced ecological impact. This shift is particularly strong among millennials and Gen Z consumers who prioritize ethical consumption and clean-label personal care products.

Technological Advancements Addressing Historical Mineral Sunscreen Formulation Limitations

Historically, mineral sunscreens faced adoption barriers due to cosmetic drawbacks, including white cast, thick textures, and uneven application. Recent formulation advancements leveraging micronized and optimized mineral particles have significantly improved spreadability, transparency, and skin feel. These innovations enable zinc oxide and titanium dioxide to disperse light effectively while maintaining broad-spectrum protection, allowing mineral sunscreens to achieve aesthetic parity with chemical alternatives.

Further innovation includes tinted mineral sunscreens designed to blend across diverse skin tones and lightweight formulations delivering near-invisible finishes. Clinical validation highlights an added functional advantage: mineral sunscreens provide immediate UVA and UVB protection upon application. Leading brands have combined these advances with skincare benefits such as hydration and barrier repair, expanding usage occasions and strengthening consumer acceptance across premium and mass-market segments.

Restraint - Price Premiums and Cost Sensitivity Across Diverse Consumer Segments

Mineral sunscreens continue to carry noticeable price premiums compared to chemical alternatives, largely due to complex formulation requirements, higher-grade mineral inputs, and relatively smaller production scales. These cost differentials create adoption challenges among price-sensitive consumers, particularly within emerging economies and middle-income demographics in developed markets. Regions such as Latin America and parts of the Asia Pacific, despite high UV exposure, show lower penetration of mineral sunscreens as affordability remains a key barrier.

While safety, regulatory alignment, and environmental benefits are widely recognized, elevated pricing limits accessibility and slows mass-market adoption. This cost sensitivity restricts demand expansion within price-elastic consumer segments, potentially moderating overall market growth even as awareness rises and regulatory frameworks increasingly favor mineral-based sun protection solutions.

Persistent Consumer Perception Challenges and Sensory Experience Concerns

Despite meaningful formulation advancements, mineral sunscreens continue to face lingering perception issues related to white cast, heavier textures, and reduced compatibility with makeup or daily skincare routines. These concerns, often rooted in older product generations, are reinforced by social media narratives and consumer reviews that overshadow recent technological improvements. Many consumers accustomed to the lightweight, invisible feel of chemical sunscreens remain hesitant to transition to mineral options.

This perceptual gap creates psychological resistance, particularly among convenience-driven and first-time buyers. As a result, trial rates remain constrained in mass-market channels where sensory experience and peer validation strongly influence purchase decisions, limiting faster penetration of mineral sunscreen products.

Market Opportunities

Accelerated Growth of E-Commerce, Digital Retail, and Direct-to-Consumer Sales Models

E-commerce has emerged as the fastest-expanding distribution channel for mineral sunscreens, enabling brands to bypass traditional retail limitations and engage consumers directly. Digital platforms allow manufacturers to communicate ingredient transparency, provide education on mineral sunscreen benefits, and address usage misconceptions through expert content and reviews. Social media and dermatologist-led advocacy further strengthen purchase intent, especially among digitally native consumers.

Leading brands have successfully leveraged direct-to-consumer strategies to build category leadership and brand loyalty. The continued expansion of e-commerce infrastructure across tier-2 and tier-3 markets in Asia Pacific, Latin America, and Africa is unlocking new demand pools. Digital-first launches, influencer collaborations, and subscription-based models present scalable opportunities for sustained market penetration.

Rising Adoption Among Male Consumers and Pediatric Sun Protection Segments

Historically underrepresented in sunscreen usage, male consumers are increasingly adopting mineral sunscreens as awareness of UV-related aging and skin cancer risks grows. Targeted marketing focused on sports, outdoor activity, and professional lifestyles has normalized daily sunscreen use within male demographics. This shift is translating into accelerated year-over-year growth in men’s sun care purchases.

Simultaneously, pediatric and baby-safe mineral sunscreens are gaining traction among health-conscious parents seeking gentle, chemical-free protection for sensitive skin. These high-margin formulations remain underpenetrated relative to adult female segments. Brands offering gender-neutral positioning, sports-specific durability, and clinically validated pediatric lines are well-positioned to capture long-term growth opportunities.

Category-wise Analysis

Form Insights

Lotion formulations dominate the mineral sunscreen market, holding approximately 40% market share, driven by superior cosmetic elegance, ease of application, and widespread consumer familiarity. Their balanced viscosity enables smooth spreadability across large body areas while maintaining hydration without excessive greasiness. Strong dermatological validation and endorsement by premium brands have reinforced lotions as the default choice for daily sun protection. Cream formulations represent the next leading category, favored by consumers with dry or sensitive skin requiring enhanced moisturization and barrier support.

Beyond lotions and creams, innovation is accelerating the adoption of alternative formats. Stick sunscreens are gaining popularity for targeted facial and lip application due to portability and mess-free usage, while gel formulations appeal to oily and acne-prone consumers seeking lightweight textures. Multifunctional and hybrid formats are also expanding usage occasions, reflecting increasingly personalized sunscreen preferences.

SPF Range Insights

SPF 30-50 products represent the leading category, accounting for approximately 43% market share, as they align closely with dermatological recommendations for daily protection while maintaining cosmetic acceptability. This range delivers effective broad-spectrum coverage without the formulation heaviness often associated with higher SPF concentrations. Consumers widely perceive SPF 30-50 as offering an optimal balance between protection, comfort, and usability for everyday exposure.

Growth momentum is shifting toward higher-protection products as sun awareness deepens. SPF 50+ formulations are increasingly favored by outdoor enthusiasts, travelers, and consumers in high-UV environments. Lifestyle changes emphasizing outdoor activity and heightened skin cancer awareness are encouraging adoption of stronger protection, reinforcing a dual-market structure centered on daily-use and high-exposure sunscreen needs.

Skin Type Insights

Sensitive skin remains the leading application segment, capturing approximately 38% market share, supported by strong dermatological recommendations and consumer trust in mineral formulations. Zinc oxide and titanium dioxide-based sunscreens are widely perceived as gentle, hypoallergenic, and suitable for compromised skin barriers, including rosacea-prone and post-procedure skin. This positioning enables premium pricing and sustained demand among health-conscious consumers.

Rapid growth is emerging from oily and acne-prone skin segments as formulation advancements address historical texture concerns. Lightweight gels, matte finishes, and non-comedogenic mineral sunscreens are reshaping perceptions and broadening appeal. At the same time, normal and dry skin users increasingly favor hybrid products that combine sun protection with moisturization, driving diversified portfolio development across skin profiles.

End-user Insights

Female consumers dominate mineral sunscreen usage with approximately 62% market share, reflecting established skincare routines, higher engagement with preventive beauty products, and greater awareness of photoaging risks. Women’s strong preference for ingredient transparency and dermatologist-endorsed products has consistently positioned them as the primary revenue-driving demographic within the market.

Adoption among male consumers is accelerating as sunscreen becomes normalized within sports, outdoor recreation, and professional lifestyles. Gender-neutral branding and performance-focused messaging are further broadening appeal across demographics. Occupational users such as athletes and outdoor workers increasingly prioritize durability and water resistance, signaling expanding demand beyond traditional beauty-focused consumer segments.

Distribution Channel Analysis

Pharmacies and drugstores lead distribution with approximately 28% market share, benefiting from professional credibility, pharmacist guidance, and dermatologist-backed product assortments. Supermarkets and hypermarkets follow closely, driven by convenience and established brand availability, while online platforms continue to strengthen their presence. Specialty beauty retailers maintain relevance through curated, premium mineral sunscreen offerings.

The fastest expansion is occurring across digital and omnichannel platforms as consumers seek ingredient transparency, expert reviews, and direct brand engagement. Online channels enable premium mineral sunscreen brands to penetrate emerging markets and underserved regions efficiently. This evolving channel mix reflects growing consumer sophistication and a shift toward informed, experience-driven purchasing behavior.

Regional Insights

North America Mineral Sunscreen Market Trends

North America represents a mature and high-penetration mineral sunscreen market, accounting for approximately 35.4% of global demand. Growth is supported by strong skin cancer awareness, clean beauty adoption, and regulatory actions favoring reef-safe formulations. The U.S. leads regional performance, supported by premium brand dominance, dermatologist endorsements, and sophisticated consumer segmentation. Environmental legislation in coastal and tourist regions has further strengthened mineral sunscreen adoption, reinforcing competitive advantages for compliant formulations.

Market momentum is increasingly shaped by channel diversification and premiumization. E-commerce and dermatology-backed retail models enable deeper consumer education and ingredient transparency. Aging demographics, rising melanoma incidence, and preventive dermatology advocacy sustain long-term demand. Despite maturity, innovation in texture, multifunctionality, and sustainable packaging continues to drive incremental growth across secondary and tertiary markets.

Europe Mineral Sunscreen Market Trends

Europe functions as a regulation-driven, premium-oriented mineral sunscreen market characterized by stringent safety oversight and highly informed consumers. The region benefits from strong regulatory alignment favoring mineral UV filters and maintains steady expansion at a projected 7.3% CAGR through 2033. Key markets including Germany, France, the U.K., and Spain exhibit strong adoption supported by healthcare system engagement, coastal tourism protection initiatives, and sustainability-driven purchasing behavior.

European consumers prioritize ingredient transparency, clinical validation, and environmental credentials, reinforcing premium positioning for mineral formulations. Pharmacy-led distribution and dermatological partnerships anchor brand credibility, while online channels expand accessibility. Market growth is driven less by penetration and more by innovation-led premiumization, enhanced performance claims, and gradual expansion into Eastern and Southern European markets.

Asia Pacific Mineral Sunscreen Market Trends

Asia Pacific represents the largest and most dynamic regional market, accounting for approximately 38.2% of global mineral sunscreen demand. Rising disposable incomes, urbanization, and heightened sun exposure awareness across diverse climates drive strong adoption. China leads regional consumption, supported by premium skincare expansion and dermatological engagement, while Japan maintains leadership in advanced formulations and multifunctional sunscreen innovation.

Growth across Asia Pacific is shaped by regional diversity and rapid digitalization. E-commerce platforms and social media enable market penetration beyond metropolitan centers, particularly in India and Southeast Asia. Consumers increasingly favor lightweight, water-resistant, and cosmetically elegant mineral sunscreens tailored to climate and skin tone diversity, positioning the region as the primary long-term growth engine for global manufacturers.

Competitive Landscape

The mineral sunscreen market exhibits a moderately consolidated structure, with major players controlling significant premium brand portfolios while emerging niche and direct-to-consumer brands leverage digital channels to bypass traditional retail dependencies. Leadership is established through strong brand equity, dermatological endorsements, and expansive distribution networks. Strategic differentiation focuses on formulation innovation, multifunctional product offerings, and sustainability credentials such as reef-safe positioning, which enhance consumer trust and premium perception.

Smaller and digitally native brands capitalize on influencer partnerships, clinical validation, and subscription-based models to rapidly scale market presence. Community engagement and e-commerce-first strategies enable these brands to capture younger, ingredient-conscious consumers, driving growth and creating competitive tension that encourages continuous innovation and market evolution.

Key Market Developments:

- In May 2025, EU regulatory amendment restricting 4-MBC chemical filter use effective May 1, 2025, and implementing Homosalate concentration limits, systematically constraining chemical sunscreen competitive positioning and reinforcing mineral formulation market advantages.

- In April 2024, EltaMD emerged as top-ranked "buzziest" mineral sunscreen brand globally, surpassing Supergoop! in consumer perception metrics and professional endorsements, reflecting accelerating market adoption of dermatologist-formulated premium brands.

- In December 2022, Supergoop! launched Daily Dose Bioretinol + Mineral SPF 40, pioneering multifunctional mineral sunscreen combining UV protection with bioretinol skincare benefits, establishing innovation leadership in advanced formulation categories.

Companies Covered in Mineral Sunscreen Market

- Neutrogena

- EltaMD

- Sun Bum

- La Roche-Posay

- Johnson & Johnson Consumer Inc.

- Australian Gold

- Avalon Natural Products

- Coppertone

- Edgewell Personal Care

- Goddess Garden

- Supergoop!

- Coola

- MDSolarSciences

- Raw Elements USA

- All Good

Frequently Asked Questions

The global mineral sunscreen market is projected to reach US$1.9 billion in 2026 and grow to US$2.9 billion by 2033 at a 6.2% CAGR, reflecting strong demand for natural UV protection and regulatory support.

Key demand drivers include rising awareness of UV hazards, preference for natural and clean beauty products, and regulatory mandates like Hawaii reef-safe laws and EU chemical UV filter restrictions.

Lotion formulations dominate, holding approximately 40% global market share, due to ease of application, cosmetic elegance, and consumer familiarity.

Asia Pacific leads with around 38.2% share, supported by urbanization, rising incomes, diverse skin tone considerations, and environmental consciousness, with regional growth of 10-14% CAGR.

E-commerce and digital channels are the largest growth opportunity, expanding at 25-30% CAGR, enabling direct consumer engagement, transparency, and brand loyalty, especially in emerging markets.

Key market leaders include Neutrogena, EltaMD, Sun Bum, La Roche-Posay, Johnson & Johnson Consumer Inc., and Australian Gold.