- Metals & Minerals

- Mineral Sand Market

Mineral Sand Market Size, Share, and Growth Forecast, 2025 - 2032

Mineral Sand Market by Mineral Type (Ilmenite, Rutile, Zircon, Titanium, Garnet, Others), End-use (Building and Construction, Aerospace, Automotive, Oil and Gas, Consumer Goods), and Regional Analysis for 2025 - 2032

Mineral Sand Market Size and Trend Analysis

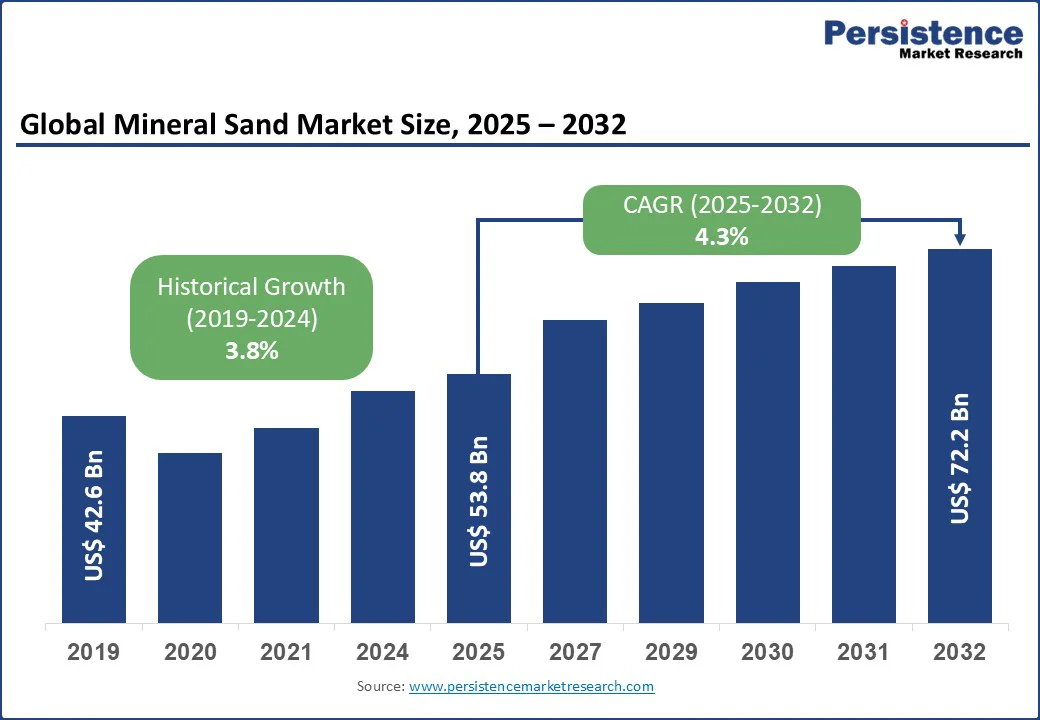

The global mineral sand market size is likely to value US$53.8 Bn in 2025 and reach US$72.2 Bn by 2032, growing at CAGR of 4.3% during the forecast period from 2025 to 2032.

Key Industry Highlights:

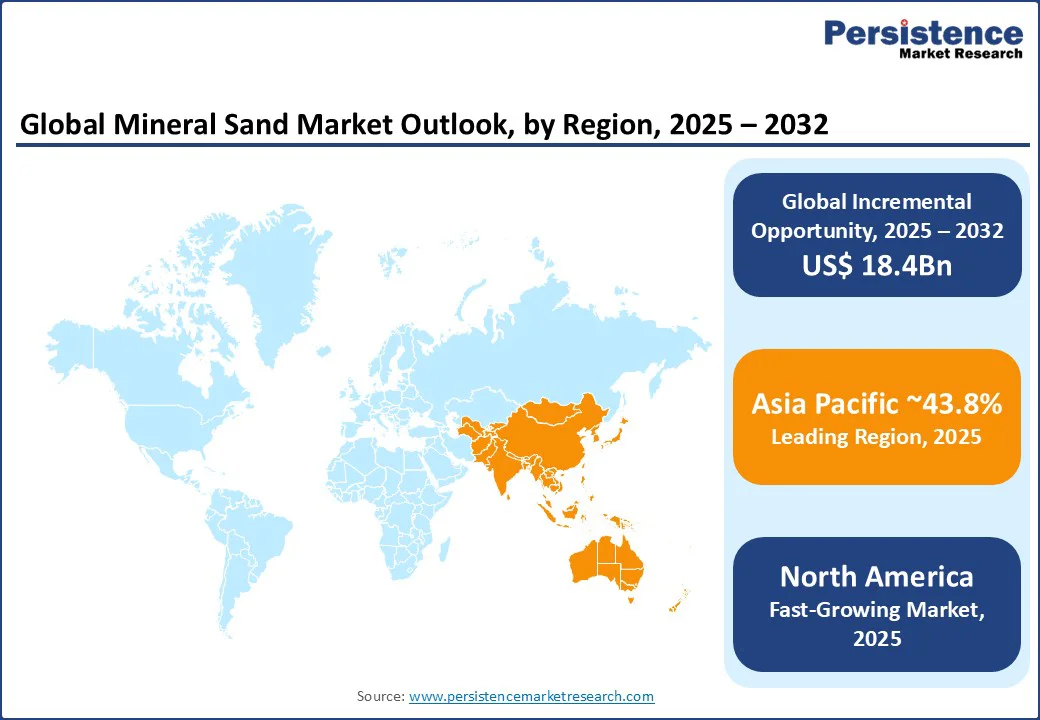

- Leading Region: Asia Pacific holds a commanding 43.8% market share in 2025, driven by rapid urbanization, infrastructure development, and significant mineral sand production in countries such as China and India.

- Fastest-growing Region: North America is the fastest-growing region, propelled by strong demand from the construction and aerospace sectors in the U.S. and Canada, supported by advanced industrial capabilities.

- Investment Plans: Iluka Resources is seeking additional government support to complete its Eneabba rare earths refinery in Western Australia, with updated cost estimates between $1.7 billion - $1.8 billion. The project is strategically significant for rare earth supply, critical for national security, and the energy transition.

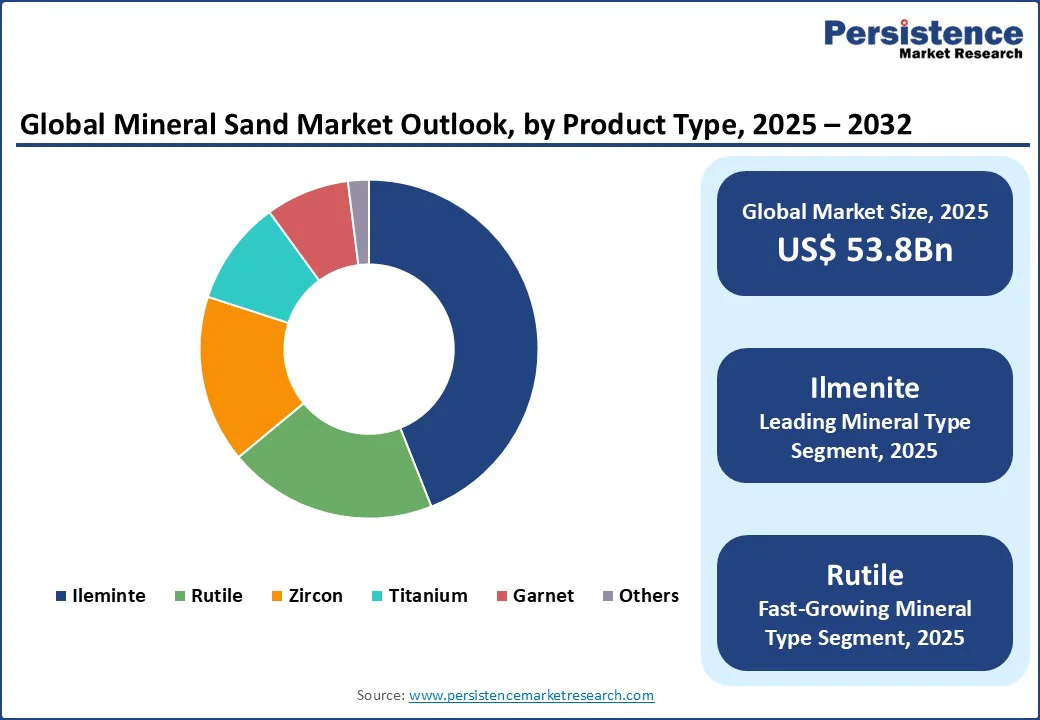

- Dominant Mineral Type: Ilmenite accounts for approximately 45.3% of the mineral sand market share in 2025, due to its abundance and versatility in titanium production for aerospace and automotive applications.

- Leading End-use: Building and construction contribute over 28.8% of market revenue, driven by global urbanization trends and infrastructure investments.

| Global Market Attribute | Key Insights |

|---|---|

| Mineral Sand Market Size (2025E) | US$ 53.8Bn |

| Market Value Forecast (2032F) | US$ 72.2Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.8% |

The mineral sand market is experiencing robust growth, fueled by increasing demand from industries such as building and construction, aerospace, and automotive, where minerals such as ilmenite, rutile, and zircon are critical for their unique properties, including high strength, corrosion resistance, and heat tolerance.

The surge in global infrastructure projects, coupled with advancements in mining and processing technologies, supports market expansion. Key players such as Iluka Resources, Rio Tinto, and Tronox Holdings are driving innovation, while rising demand for sustainable materials in renewable energy applications further bolsters market growth.

Market Dynamics

Driver - Growing Infrastructure and Construction Activities Fuel Market Expansion

The global mineral sand market is experiencing significant growth due to the surge in infrastructure and construction activities worldwide. Mineral sands, particularly ilmenite and zircon, are critical for producing titanium dioxide and ceramic materials used in paints, coatings, and tiles for construction.

According to the World Bank, global infrastructure investment needs are projected to reach $94 trillion by 2040, with a significant share directed toward emerging economies. In the Asia Pacific, China’s Belt and Road Initiative and India’s Smart Cities Mission are driving demand for mineral sands in construction applications.

The American Society of Civil Engineers notes that over 623, 000 U.S. bridges require repair or replacement, increasing the need for durable materials derived from mineral sands. Companies such as Iluka Resources reported a sales increase in construction-grade mineral sands in 2024. Government-led initiatives and rapid urbanization ensure sustained demand, positioning construction as a key driver for market growth through 2032.

Restraint - Volatility in Raw Material Prices and Environmental Concerns

The mineral sand market faces challenges due to fluctuating raw material prices and growing environmental concerns. Mining mineral sands relies on energy-intensive processes, and price volatility in energy markets impacts production costs. In 2023, energy price fluctuations affected operational costs for manufacturers, creating pricing pressures, especially for smaller players such as Base Resources.

Additionally, environmental regulations and concerns over coastal ecosystem degradation due to heavy mineral sand mining limit expansion in certain regions. Coastal mining, particularly in India and South Africa, has faced resistance due to biodiversity loss and saltwater intrusion, as noted in ecological studies. These factors, combined with competition from alternative materials such as synthetic substitutes, hinder market growth, particularly in environmentally sensitive or cost-conscious markets.

Opportunity - Rising Demand in Renewable Energy and Electric Vehicle Sectors

The increasing focus on renewable energy and electric vehicles (EVs) presents significant opportunities for the mineral sand market. Mineral sands, such as ilmenite and zircon, are essential for producing titanium and zirconium used in renewable energy projects such as offshore wind farms and EV battery manufacturing.

The International Energy Agency projects global renewable energy capacity is expected to grow by 2.7 times by 2030 under current policies and market conditions, with offshore wind investments driving demand for high-strength materials. Companies such as Tronox Holdings are innovating with high-purity titanium feedstocks for renewable energy applications, aligning with sustainability trends.

In the EV sector, mineral sands are used in battery component assembly, with players such as Kenmare Resources expanding offerings. Government incentives, such as the EU’s Green Deal, encourage investments in green technologies, creating opportunities for manufacturers to develop advanced, eco-friendly mineral sand products to meet evolving industry needs through 2032.

Category-wise Insights

By Mineral Type

- Ilmenite holds the largest market share of the mineral sand market, approximately 45.3% in 2025, due to its abundance and critical role in titanium dioxide production. Widely used in aerospace, automotive, and construction industries, ilmenite is favored for its cost-effectiveness and versatility in producing pigments and titanium metal. Companies such as Rio Tinto and Tronox Holdings lead with extensive ilmenite portfolios, catering to demand in North America and the Asia Pacific, where infrastructure and industrial applications drive growth.

- Rutile is experiencing rapid growth due to its high titanium dioxide content, making it essential for high-performance applications in paints, coatings, and aerospace. Its demand is rising in harsh environments, such as offshore energy projects, with companies such as Iluka Resources expanding rutile offerings in Europe and the Asia Pacific to meet growing needs in advanced engineering and renewable energy sectors.

By End-use

- The construction sector accounts for over 28.8% market share of mineral sand market in 2025, driven by global infrastructure projects and urbanization. Mineral sands, such as zircon and ilmenite, are critical for producing ceramic tiles, paints, and coatings used in buildings and bridges. Major players, such as Base Resources, supply high-quality sands for projects in China and the U.S., where government investments in highways and urban development fuel demand.

- The energy sector is witnessing rapid growth, propelled by rising investments in renewable energy and oil & gas exploration. Mineral sands are used in offshore wind farms and drilling rigs, with companies such as Kenmare Resources innovating for high-performance applications. Growth in the Asia Pacific and the Middle East, driven by energy infrastructure projects, supports this segment’s rapid expansion.

Regional Insights

Asia Pacific Mineral Sand Market Trends

The Asia Pacific region is poised to dominate the global mineral sand market with a commanding 43.8% share by 2025, a trend expected to continue through 2032. This dominance is driven by several interlinked factors spanning economic growth, infrastructure development, industrial demand, and rich natural resources.

Countries in the Asia Pacific, especially China and India, are experiencing unprecedented urban growth and infrastructural transformation. China, a global leader in construction, drives demand for ilmenite and zircon through initiatives such as the Belt and Road Initiative. India’s Smart Cities Mission boosts construction-grade mineral sand usage.

The region’s mining industry, led by companies such as Iluka Resources and South32, benefits from abundant deposits and low production costs. Australia, a key producer, contributes significantly with operations such as Iluka’s Jacinth-Ambrosia mine. Rising demand from the aerospace and automotive sectors further supports growth, ensuring Asia Pacific’s dominance through 2032.

North America Mineral Sand Market Trends

North America is the fastest-growing region in the mineral sands market, propelled primarily by strong demand from the construction and aerospace sectors in the U.S. and Canada.

The U.S. construction industry, with spending reaching $2.14 trillion in July 2025 per the U.S. Census Bureau, relies heavily on mineral sands-particularly titanium dioxide-for paints, coatings, and durable structural materials essential to infrastructure projects such as bridge repairs and high-rise developments. Meanwhile, Canada’s expanding aerospace sector fuels demand for titanium-based products used in lightweight, high-strength components.

Industry leaders such as Tronox Holdings play a critical role, leveraging extensive distribution networks to supply mineral sands across diverse applications. Additionally, growing consumer preference for high-purity, environmentally sustainable materials strengthens the market position of North America.

Supported by advanced industrial infrastructure and technological innovation, the region is poised for sustained growth, with the mineral sands market expected to expand steadily through 2032, driven by ongoing urbanization, infrastructure renewal, and aerospace manufacturing.

Europe Mineral Sand Market Trends

Europe is the second fastest-growing region in the mineral sands market, propelled by stringent environmental regulations, expanding aerospace and automotive industries, and significant infrastructure investments, particularly in Germany and France.

Valued at €1,683 billion in 2023 according to the European Construction Industry Federation, the European construction sector drives robust demand for mineral sands used in ceramic tiles, coatings, and specialty materials. Germany’s advanced aerospace sector relies heavily on titanium-based minerals, with companies such as TiZir Limited playing a vital role in supplying high-quality titanium products.

Additionally, the EU’s ambitious Green Deal is accelerating renewable energy development, especially offshore wind farms, boosting demand for rutile and zircon minerals crucial for durable and corrosion-resistant turbine components.

Europe’s strong emphasis on sustainability, regulatory compliance, and high-quality standards fosters innovation among market players, who continually develop eco-friendly, efficient mineral sand processing techniques. This commitment positions Europe for steady mineral sand market growth through 2032, aligned with evolving environmental and industrial priorities.

Competitive Landscape

The global mineral sand market is highly competitive and fragmented, with numerous domestic and international players, including large corporations such as Rio Tinto and Iluka Resources, alongside regional manufacturers such as Lanka Mineral Sands. Companies dominate through extensive product portfolios, advanced mining technologies, and global distribution networks.

Players such as Tronox Holdings and Kenmare Resources focus on high-purity titanium and zircon products, while Base Resources emphasizes sustainable mining practices. Investments in advanced processing and eco-friendly technologies are key strategies to enhance market share, driven by demand in construction, aerospace, and energy sectors.

Key Industry Developments

- February 2025: Iluka Resources reported strong progress on the Balranald mineral sands project, with development well advanced ahead of its planned commissioning in the second half of 2025. The mine is projected to produce 60,000 tonnes of natural rutile and 50,000 tonnes of high-quality zircon annually, along with feedstock for synthetic rutile and rare earth processing over its ten-year life.

- June 2025: Astron Corporation’s Donald Rare Earth and Mineral Sands Project in western Victoria received final state government approval, paving the way for development. The approved work plan allows mining of 7.5 million tonnes of mineral sands per year for 19 years, including targets such as ilmenite, monazite, rare earth elements, rutile, and zircon, positioning this as one of the state's most significant critical minerals initiatives.

Companies Covered in Mineral Sand Market

- Base Resources

- South32

- Iluka Resources

- Lanka Mineral Sands

- VHM Limited

- Dundas Titanium

- Sierra Rutile

- TiZir Limited

- Meridian Mining

- Macarthur Minerals

- Istanbul Minerals and Metals

- Namakwa Sands

- Rio Tinto

- Tronox Holdings

- Kenmare Resources

- Others

Frequently Asked Questions

The Mineral Sand market is projected to reach US$ 53.8 Bn in 2025.

Growing infrastructure and construction activities, and expanding applications in renewable energy are the key market drivers.

The Mineral Sand market is poised to witness a CAGR of 4.3% from 2025 to 2032.

The rising demand in the renewable energy and electric vehicle sectors is the key market opportunity.

Base Resources, South32, Iluka Resources, Rio Tinto, and Tronox Holdings are key market players.