- Automation & Robotics

- Military Drone Market

Military Drone Market Size, Share, and Growth Forecast 2026 - 2033

Military Drone Market by Vehicle Type (Armored Vehicles, Tactical Vehicles, Logistics Vehicles, Combat Vehicles), Product Type (Fixed-Wing, Rotary Blade, Hybrid), Technology (Remotely Piloted, Partially Autonomous, Fully Autonomous), End-Use (Defense Forces, Private Contractors, Government Agencies), Maximum Take-off Weight (<150 Kg, 150 – 1000 Kg, >1000 Kg), and Regional Analysis for 2026 - 2033

Military Drone Market Size and Trend Analysis

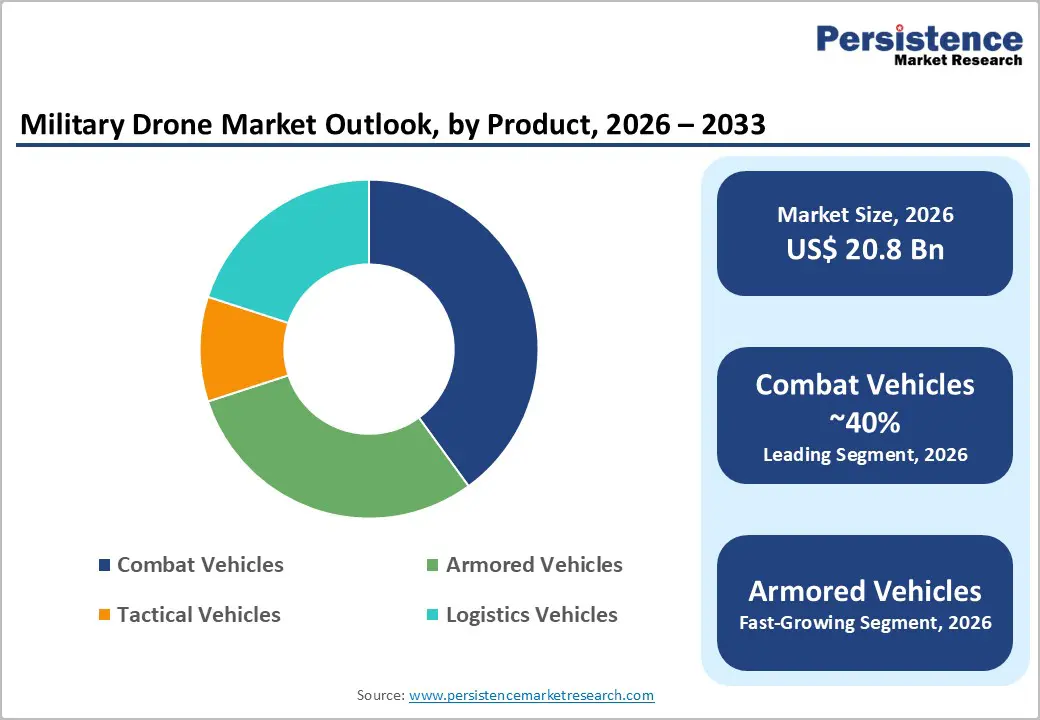

The global Military Drone Market size is valued at US$ 20.8 billion in 2026 and is projected to reach US$ 34.1 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The military drone market is on a robust growth trajectory, driven by escalating global defense budgets, rapidly advancing autonomous and AI-guided flight technologies, and expanding battlefield applications across intelligence, surveillance, reconnaissance (ISR), and precision-strike missions. NATO member nations collectively exceeded US$ 1.3 trillion in defense spending in 2023, with unmanned aerial systems (UAS) procurement among the fastest-growing expenditure lines.

Key Industry Highlights:

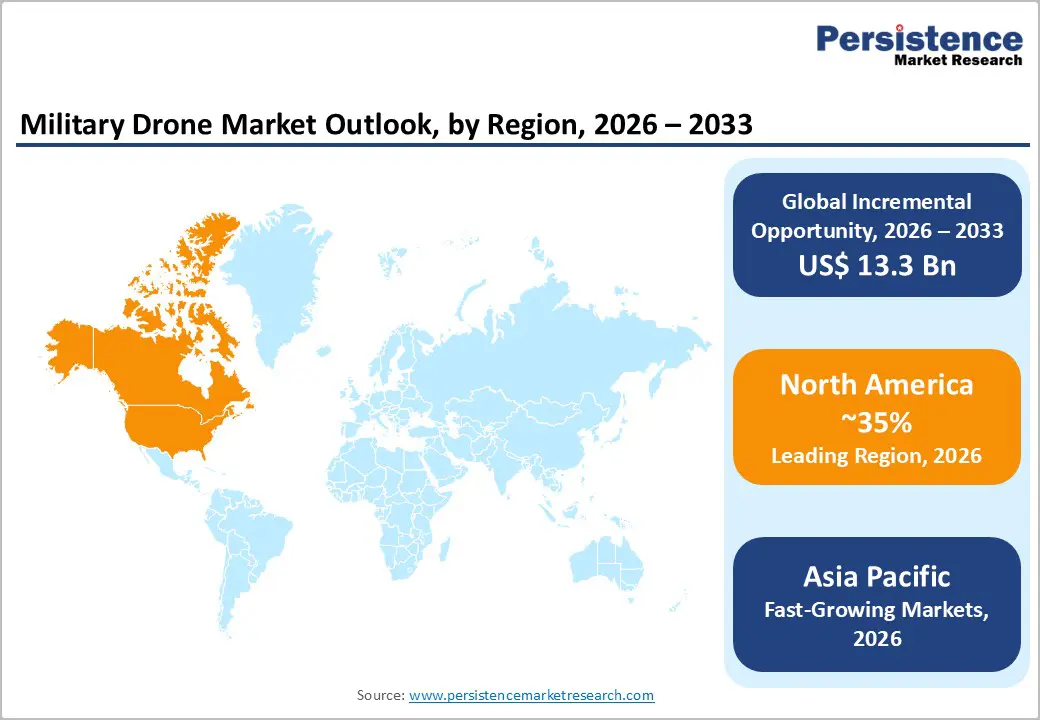

- Leading Region – North America leads the Military Drone Market, anchored by U.S. DoD procurement exceeding US$ 1.8 billion in drone-related spending in FY2024 and the Replicator Initiative targeting autonomous drone fleet deployment by mid-2025.

- Fastest Growing Region – Asia Pacific is the fastest-growing region, driven by China's indigenous UAS expansion, India's US$ 3.99 billion MQ-9B procurement, and Japan's record five-year US$ 56 billion defense build-up, accelerating multi-domain drone modernization.

- Dominant Segment – Fixed-wing drones command approximately 55% of the product type segment, preferred for superior endurance, altitude, and payload capacity in long-range ISR and precision-strike missions across major armed forces globally.

- Fastest Growing Segment – The Fully Autonomous segment is the fastest-growing technology tier, driven by U.S. DoD's Replicator Initiative, DARPA's swarm programs, and analogous PLA investments enabling AI-guided mass drone deployment through 2033.

- Key Opportunity – Expanding drone roles in military logistics, cargo resupply, and AI-enabled swarm operations represent high-growth revenue streams, underpinned by U.S. Army ExLF and NATO multi-domain operations doctrine investments through 2033.

| Key Insights | Details |

|---|---|

|

Military Drone Market Size (2026E) |

US$ 20.8 Bn |

|

Market Value Forecast (2033F) |

US$ 34.1 Bn |

|

Projected Growth CAGR (2026–2033) |

7.3% |

|

Historical Market Growth (2020–2025) |

4.8% |

Market Dynamics

Drivers

Surging Global Defense Budgets and Geopolitical Tensions Accelerating UAS Procurement

Rising geopolitical instability across multiple theatres including the Russia-Ukraine conflict, tensions in the South China Sea, and ongoing security challenges in the Middle East has prompted governments worldwide to substantially increase defense expenditures, with unmanned aerial systems emerging as a strategic procurement priority. According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure reached a record US$ 2,443 billion in 2023, reflecting the highest level since the end of the Cold War. The conflict in Ukraine has demonstrated the transformative tactical utility of military drones from ISR and artillery spotting to direct strike missions, convincing defense establishments globally to accelerate modernization programs.

Advancements in AI, Autonomy, and Swarm Technologies Expanding Operational Capabilities

Rapid technological advancement in artificial intelligence, machine learning-enabled target recognition, and swarm coordination algorithms is fundamentally expanding the operational capabilities of military drones, making them indispensable across a growing range of mission profiles. The U.S. Department of Defense (DoD) has been investing heavily in autonomous systems under initiatives including the Replicator Initiative, which announced plans to field thousands of autonomous drones within 18 to 24 months by mid-2025. This initiative alone signals a paradigm shift toward mass-deployment of AI-enabled military drones as a force multiplier. Fully autonomous engagement and navigation technologies are reducing operator dependency and enabling complex multi-domain operations. These advancements are directly driving demand across the Military Drone Market, particularly for higher-capability platforms in the partially and fully autonomous technology segments.

Restraints

Stringent Export Controls and International Regulatory Barriers

Military drone exports are tightly governed by international arms control frameworks, including the Missile Technology Control Regime (MTCR), the Wassenaar Arrangement, and bilateral export licensing regimes administered by governments such as the U.S. State Department under ITAR (International Traffic in Arms Regulations). These regulatory frameworks significantly restrict the transferability of advanced UAS technologies across borders, limiting market access for leading manufacturers and constraining revenue opportunities in high-demand markets. MTCR guidelines cap the export of drone systems capable of carrying payloads exceeding 500 kg beyond 300 km, directly affecting high-value MALE and HALE-class UAV transaction volumes.

High Development and Lifecycle Costs Straining Smaller Defense Budgets

Advanced military drones particularly medium-altitude long-endurance (MALE) and high-altitude long-endurance (HALE) platforms carry substantial development, procurement, and lifecycle maintenance costs that place them beyond reach for nations with constrained defense budgets. The U.S. Air Force's MQ-9 Reaper carries a unit cost exceeding US$ 32 million, with annual operating and sustainment costs adding further expenditure. For developing nations in Africa, Southeast Asia, and Latin America, this cost barrier limits adoption to lower-tier tactical systems, restricting addressable market expansion for premium-segment drone manufacturers and slowing full-spectrum UAS modernization across global defense establishments.

Opportunities

Fully Autonomous Drone Technology and AI-Enabled Swarm Platforms

The transition toward fully autonomous military drones represents the most transformative growth opportunity in the Military Drone Market over the forecast period through 2033. The U.S. DoD's Replicator Initiative and analogous programs being developed by China's People's Liberation Army (PLA) and European NATO members signal massive procurement pipelines for AI-driven drone swarms capable of collaborative autonomous operations. DARPA's ongoing investments in programs such as Offensive Swarm-Enabled Tactics (OFFSET) and Gremlins are accelerating the maturation of technologies required for scalable autonomous drone deployment. Industry analysts at Persistence Market Research project that the autonomous drone segment will outpace the broader market growth rate, driven by multi-billion-dollar defense R&D investment commitments and a structural shift toward attritable, mass-deployable drone platforms across all major military powers.

Expanding Role of Drones in Multi-Domain Operations and Logistics Support

Beyond traditional ISR and strike roles, military drones are rapidly gaining traction in logistics, medical resupply, electronic warfare, and communications relay missions significantly expanding the addressable end-use scope. The U.S. Army has been piloting autonomous cargo drone programs under the Expedient Leader Follower (ExLF) initiative, while the U.S. Marine Corps has deployed cargo drone resupply systems in operational exercises. The growth of the Military Land Vehicles Market and its integration with drone-based logistics platforms is further driving demand for unmanned ground-air coordination systems. As multi-domain operations doctrine becomes institutionalized across major military forces, demand for logistics-oriented rotary-blade and hybrid drone platforms is expected to create significant new revenue streams for manufacturers with diversified UAV portfolios through the 2033 forecast horizon.

Category-wise Analysis

Vehicle Type Insights

The Combat Vehicles segment holds the leading share in the Military Drone Market by vehicle type, accounting for approximately 40% of total revenues. Combat-configured drones encompassing armed UAVs, loitering munitions, and precision-strike platforms represent the highest-value procurement category across global defense forces. Their deployment in recent conflicts, including in Ukraine and the Middle East, has validated their battlefield effectiveness and accelerated procurement urgency among NATO and non-NATO armed forces alike. Platforms such as the General Atomics MQ-9 Reaper, Bayraktar TB2, and Israel Aerospace Industries' Harop loitering munition represent the commercial backbone of this segment.

Product Type Analysis

The Fixed-Wing segment is the dominant product type in the Military Drone Market, commanding approximately 55% of segment revenues. Fixed-wing military drones offer superior endurance, higher operational altitudes, and greater payload capacity compared to rotary-blade counterparts, making them the preferred platform for long-range ISR, border surveillance, and precision-strike missions. Platforms such as Northrop Grumman's RQ-4 Global Hawk, with endurance exceeding 30 hours and operational altitudes above 60,000 feet, exemplify the strategic value of fixed-wing designs. The U.S. Air Force and allied MALE/HALE UAV programs across NATO nations continue to drive procurement volumes for advanced fixed-wing platforms, cementing the segment's market leadership through the forecast period.

Technology Insights

The remotely piloted segment holds the largest technology share in the Military Drone Market, accounting for approximately 58% of revenues. Despite the rapid emergence of autonomous capabilities, remotely piloted systems remain the operationally dominant technology due to established doctrine, pilot training infrastructure, and legal and ethical frameworks governing the use of lethal force that currently require human control in most military operations. The DoD Directive 3000.09 on autonomous weapons systems mandates human oversight of lethal engagements, reinforcing the continued primacy of remotely piloted configurations across most armed forces. However, the partially autonomous segment is the fastest-growing technology tier, driven by increasing integration of AI co-pilot systems, automated takeoff/landing, and AI-assisted targeting functionalities across next-generation platforms.

End-user Insights

The Defense Forces segment accounts for the dominant end-use share in the Military Drone Market, representing approximately 72% of global revenues. National armed forces air forces, armies, and navies are the primary institutional purchasers of military drones, driven by formal defense procurement cycles and government-to-government acquisition programs. According to SIPRI, the world's largest military spenders the United States (US$ 916 billion in 2023), China, Russia, India, and Saudi Arabia collectively represent the core institutional demand base for military drones. Expanding UAS fleets across emerging defense markets in Southeast Asia, the Middle East, and Africa are additionally broadening the global defense forces end-use segment.

Maximum Take-off Weight Insights

The 150 – 1000 Kg maximum take-off weight (MTOW) segment leads the Military Drone Market, holding approximately 45% of the segment revenues. This weight class encompasses medium-altitude long-endurance (MALE) platforms the most commercially active drone category globally including iconic systems such as the General Atomics MQ-9B Sky Guardian and Turkish Aerospace Industries Aksungur. MALE-class UAVs deliver the optimal operational balance: sufficient payload capacity for ISR sensors and precision munitions, combined with multi-day endurance and satellite link capability, at unit costs accessible to a broad range of defense customers. Their versatility across ISR, strike, and maritime patrol roles makes them the most widely procured drone platform category across both established and emerging defense markets globally.

Regional Insights

North America Military Drone Market Trends

North America is the largest and most technologically advanced regional market in the global Military Drone Market, led overwhelmingly by the United States. The U.S. Department of Defense allocated approximately US$ 1.8 billion specifically for drone-related procurement and R&D in its FY2024 budget, with the Replicator Initiative targeting deployment of thousands of autonomous drones by mid-2025.

Regulatory leadership through the Federal Aviation Administration (FAA) and defense-specific waivers enables expansive domestic test and training operations, accelerating technology maturation. Canada is investing in Arctic surveillance UAVs under its NORAD modernization program, adding a secondary demand node. North America also benefits from deep integration between defense prime contractors and government-funded research agencies including DARPA and AFRL, which underwrite the next generation of autonomous and hypersonic drone technologies shaping global military UAS development through the 2033 horizon.

Europe Military Drone Market Trends

Europe is the second-largest regional market for military drones, driven by heightened security concerns following Russia's invasion of Ukraine in 2022 and the subsequent acceleration of NATO member defense spending commitments. Collectively, European NATO members increased aggregate defense expenditure by over 11% in 2023 per NATO data, with drone procurement among the fastest-growing line items. Germany approved the acquisition of armed Euro drone MALE UAVs under a multi-billion-euro program, while the U.K. Royal Air Force continues to operate the Protector RG Mk1 (MQ-9B) under a major procurement program.

France is advancing indigenous drone capabilities through the MALE 2025 European consortium program alongside Airbus, Dassault Aviation, and Leonardo S.p.A., aimed at reducing dependence on U.S. and Israeli platforms. Spain has deployed Bayraktar TB2 drones for border and maritime surveillance, reflecting growing European adoption of cost-effective non-domestic UAS.

Asia Pacific Military Drone Market Trends

Asia Pacific is the fastest-growing regional market in the Military Drone Market, propelled by massive indigenous drone development programs in China, accelerating procurement in India, and expanding UAS modernization across Japan, South Korea, and Australia. China's People's Liberation Army (PLA) operates one of the world's largest military drone fleets, with the China Aerospace Science and Technology Corporation (CASC) and AVIC producing platforms including the Wing Loong II and CH-5 MALE UAVs for both domestic and export markets.

India is a rapidly growing UAS market, having approved the procurement of 31 MQ-9B Predator drones from General Atomics in a US$ 3.99 billion deal approved in 2023 and progressing in 2024, alongside advancing its indigenous TAPAS-BH-201 MALE drone under DRDO. Japan's Ministry of Defense is accelerating drone procurement under its record US$ 56 billion five-year defense build-up plan. ASEAN nations, including Indonesia, the Philippines, and Vietnam, are acquiring tactical UAS systems for maritime domain awareness, expanding the regional demand base significantly.

Competitive Landscape

The global Military Drone Market is moderately consolidated, with a small number of defense primes including Northrop Grumman, General Atomics Aeronautical Systems, Lockheed Martin, and Israel Aerospace Industries commanding significant revenue shares, particularly in high-value MALE/HALE and strike UAV categories. Competition intensifies in the tactical and micro-drone segments, where companies including AeroVironment and Elbit Systems compete with a growing number of regional challengers. Strategic differentiators include government relationships, security clearances, multi-role platform versatility, AI integration depth, and sustainment ecosystems.

Key Developments:

- In November 2025, BAE Systems PLC signed a Memorandum of Understanding (MoU) with Turkish Aerospace Industries (TAI) to explore the joint development of advanced uncrewed air systems (UAS). The goal is to merge UK combat air integration expertise with Turkish drone manufacturing for next-generation joint drones for NATO and other allied fleets.

- In July 2025, Northrop Grumman Corporation partnered with Red 6 to integrate its Advanced Tactical Augmented Reality System (ATARS) into Northrop’s Beacon autonomous mission testbed. This collaboration enables realistic virtual training environments that replicate complex, near-peer threat scenarios while reducing safety risks and airspace limitations.

Companies Covered in Military Drone Market

- Northrop Grumman Corporation

- General Atomics Aeronautical Systems Inc.

- Lockheed Martin Corporation

- Israel Aerospace Industries (IAI)

- AeroVironment Inc.

- Elbit Systems Ltd.

- BAE Systems

- Turkish Aerospace Industries (TAI)

- China Aerospace Science and Technology Corporation (CASC)

- Leonardo S.p.A.

- Textron Systems

- Saab AB

- Thales Group

Frequently Asked Questions

The global Military Drone Market is valued at US$ 20.8 Bn in 2026 and is projected to reach US$ 34.1 Bn by 2033, growing at a CAGR of 7.3% over the forecast period. Growth is driven by record global defense budgets, expanding UAS procurement across NATO and Indo-Pacific nations, and the rapid integration of AI and autonomous technologies into next-generation military drone platforms.

The primary demand drivers are escalating global defense expenditure with SIPRI recording a record US$ 2,443 billion in global military spending in 2023 geopolitical tensions validating drone battlefield utility, and the U.S. DoD Replicator Initiative targeting mass autonomous drone deployment. Advances in AI, swarm technology, and satellite-linked communications are continuously broadening the operational scope of military drones globally.

The Fixed-Wing segment dominates the Military Drone Market with approximately 55% of product type revenues. Fixed-wing platforms offer superior endurance, higher operational altitudes, and greater payload capacity, making them the preferred choice for long-range ISR, border surveillance, and precision-strike missions across major armed forces including the U.S. Air Force and NATO allied nations.

North America is the leading region, dominated by the United States, which allocated approximately US$ 1.8 billion for drone-related procurement and R&D in its FY2024 DoD budget. The U.S. hosts the world's most advanced military UAS innovation ecosystem, anchored by primes including Northrop Grumman, General Atomics, and Lockheed Martin, and maintains the most extensive operational drone fleet globally.

The leading companies in the global Military Drone Market include Northrop Grumman Corporation, General Atomics Aeronautical Systems Inc., Lockheed Martin Corporation, and Thales Group. These companies compete on platform performance, AI integration, government relationships, export credentials, and sustainment ecosystem depth.