- Sensors & Controls

- Radar Sensor Market

Radar Sensor Market Size, Share, and Growth Forecast for 2025 - 2032

Radar Sensor Market by Type (Imaging Radar, CW Radar, Pulse Radar, Non-imaging Radar, Speed Gauge, Altimeter), by Technology (Time Domain Reflectometry - TDR, Ultra-Wideband - UWB, RF MEMS-based Radar Sensors, Millimeter Wave), by Component (Antenna, Duplexer, Transmitter, Receiver, Video Amplifier), and Regional Analysis

Radar Sensor Market Size and Share Analysis

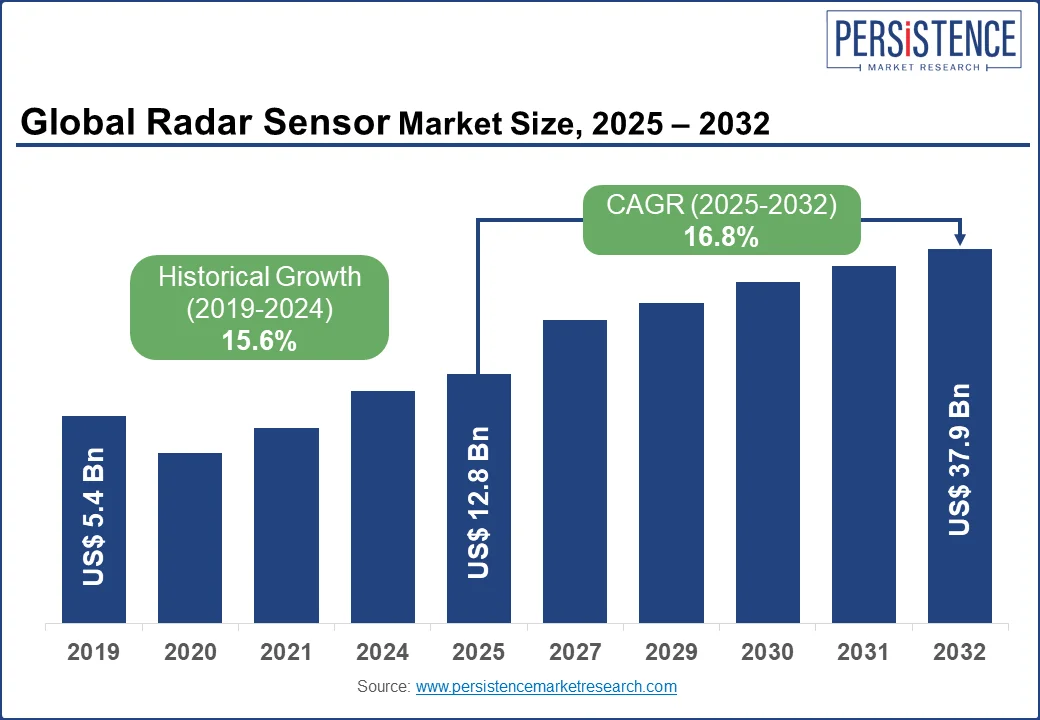

The global radar sensor market is predicted to reach US$ 12.8 billion by 2025, with a CAGR of 16.8%. As a result, revenues are expected to reach US$ 37.9 billion by 2032. With the development of semiconductor technology in recent years, radar has significantly reduced its power consumption and size. The capabilities of the system have also been enhanced, which have been improved through multiple transmissions and receptions, ultra-wideband technology, millimeter-wave technology, signal processing technology, and ICs with increasingly sophisticated processing capabilities.

With the aging of the population, there are more fall accidents and cognitive illnesses like Alzheimer's. In addition to reducing suffering, preventative measures can also reduce costs. About 100,000 people older than 65 in Sweden require medical care after sustaining a bad fall, including 70,000 in hospitals. The number of elderly people who die from fall accidents each year is approximately 1,000. Fall accidents lead to three million visits to emergency departments each year among elderly Americans.

An innovative radar sensor developed by Swedish researchers can predict falls and cognitive diseases such as Alzheimer's. A radar sensor developed by Chalmers University of Technology is able to detect a person's walking pattern in homes and healthcare facilities, which can be mounted to walls, furniture, or ceilings.

| Report Attributes | Details |

|---|---|

|

Radar Sensor Market Size (2025) |

US$ 12.8 billion |

|

Radar Sensor Projected Market Value (2032) |

US$ 37.9 billion |

|

Radar Sensor Market CAGR (2025 to 2032) |

16.8% |

|

United States Market Size (2032) |

US$ 14.6 billion |

|

China Market Size (2032) |

US$ 3.7 billion |

Sales of Radar Sensors are Predicted to Rise From 2025 to 2032 from 2019 to 2024

According to Persistence Market Research (PMR), radar sensor revenues grew by 19% CAGR between 2019 and 2024. Analysts predict that sales across the globe will grow by 16.8% between 2025 and 2032.

Radar sensors offer several benefits, which have led many businesses and government agencies to increase their research and development efforts, which are likely to have a positive impact on the market.

Surveillance systems are becoming increasingly common in military forces, and security concerns are increasing across the globe. New security and monitoring systems are being integrated by governments from several nations to increase their military power.

As the military and defense markets continue to grow, the increasing demand for intelligent targeting, countermeasures, navigation, and missile guidance for military and defense applications is contributing to this growth.

In 2019, there were an estimated 6.4 billion devices that were connected, according to the National Cybersecurity Center of Excellence. Approximately 20 billion devices were expected to be in use by 2020. As a result of the high level of demand for radar sensing technologies, market players continually innovate, reducing the competitiveness of their competitors.

What are the Key Factors Driving the Radar Sensor Market?

“Automation and Industry 4.0 to Drive Demand for Radar Sensor Market.”

Growing demand for the Internet of Things (IoT) and smart devices among developing nations is expected to drive market growth for radar sensors. With improved performance in different temperature and lighting conditions, these sensors are accelerating the demand for smart home devices for automation and security.

Over the next few years, improvements in automotive safety systems and autonomous driving are expected to drive demand. In the next few years, radar sensors are expected to become more prevalent as the development of medical devices grows. Moreover, sensor fusion and railway integration are driving the market's growth, as is the popularity of sensor fusion technology.

Systems such as adaptive cruise control and collision avoidance utilize these sensors to sense the environment. As security systems grow in sophistication, and advances and applications of high-tech technologies are being made in the market, the demand for radar sensors is expected to increase.

Due to the growth of the industrial sector, it has become increasingly necessary to integrate radar sensors into their designs, thus driving the global radar sensor market to grow. The use of radar sensors is common in industrial applications for detecting and tracking moving objects. All these factors are expected to drive demand for radar sensors in the market.

Country-wise Insights

How Fast is the Growth of the Radar Sensor Market in North America?

“New Technologies and the Increasing Demand for Autonomous Vehicles is Likely to Drive Demand in the Radar Sensor Market.”

The radar sensor market is expected to be dominated by North America. According to PMR, the North American radar sensor market will reach US$ 18.72 billion by 2032.

Technology advancements are being supported by increasing investments in the region. With increased security and surveillance focuses in the region, along with projected growth in radar sensor markets, radar sensor production is likely to increase.

As smartphones and wearable devices become more prevalent, there will be an increase in the demand for radar sensors in the market. As smartphone manufacturers integrate more sensors and features into their smartphones, the demand for radar sensors is also expected to increase. North America will have nearly 270 million mobile connections by the end of 2025, according to the GSMA.

The United States is expected to account for 78% of all market share during the forecast period. In 2032, revenues for the radar sensor market are projected to reach US$ 14.6 billion, growing at a CAGR of 15.5%.

Vehicle advancements and growing automobile purchases are likely to drive demand for the product. Recently, with the release of Automated Vehicles 3.0 by the NHTSA, new federal guidelines for automated vehicles have been released that have expanded the market for ADAS in mid-range vehicles, increasing production. Radar sensors are becoming increasingly popular among various brands. As a result of these factors is experiencing significant growth in the market.

What Role do Radars Hold in the Asia-Pacific Region?

“Expanding Government Initiatives and Military Investments are Likely to Increase Demand for Radar Sensor Market.”

The radar sensor market is expected to be dominated by Asian markets in the near future. According to estimates, the radar sensor market is estimated to be worth US$ 10.62 billion by the year 2032. According to PMR, the Chinese market will account for 35% of the market in 2032.

With the rise of the manufacturing industry, robots, and industrial automation are becoming more popular. The rise of disposable incomes, rising living standards, and technological advancements in automotive also contribute to the growth of the industry.

As the government takes initiatives to implement radar sensors in a variety of aerospace applications, which has resulted in a rapid growth of the market in Asia Pacific. Growing advances in the naval industry, as well as the growth of the internet in these regions, have increased the demand for radar sensors.

China, Japan, India, and South Korea are expected to show rapid growth for radar sensors in the coming years. It is estimated that China will generate US$ 3.7 billion by 2032. Between 2025 and 2032, the radar sensor market in China is projected to grow at a CAGR of 17.9%.

With increasing initiatives by government agencies to introduce safety systems into vehicles to mitigate the risk of accidents, the radar sensor market is expected to grow. These systems are also being incorporated into high-end commercial vehicles and motor vehicles around the world, enhancing road safety. All these factors are expected to grow demand for radar systems in the Asia Pacific region.

Category-wise Insight

Which Type of Radar Sensors are Driving Market Growth?

“Growing Innovations in Imaging Technologies are Expected to Grow Market.”

Based on type, the market is segmented into imaging radar, CW radar, pulse radar, non-imaging radar, speed gauge, and altimeter.

Radar-based sensors are intended to bridge the gap between current-generation lidars and radars, while RF sensors maintain their advantages over current-generation radars.

Imaging radar sensors are becoming increasingly popular among security, surveillance, and weather forecasting applications, resulting in the growth of the market for industrial and commercial applications.

Various businesses committed to innovation, companies continue to develop 4-D imaging radars to promote the acceptance of advanced automotive safety systems. As a result of 4D imaging radars, the capabilities of autonomous driving will be increased to 300 meters, allowing the market to expand.

As infrastructure projects become more demanding, radar technology is adopted more frequently in defense and security applications, and autonomous vehicles are increasingly being developed. Using artificial intelligence and machine learning to improve the quality of radar images, developing lightweight, compact radar systems, and the growing use of multi-sensor systems for enhancing situational awareness all represent advanced radar technologies.

What will be the Dominant Radar Sensor Application on the Market?

“The Automotive Segment is Likely to Lead the Radar Sensor Market.”

Demand for radar sensors is expected to rise in the automation segment. By 2032, the radar sensor market for automotive is expected to grow at a CAGR of 16.5%. The demand for automation and the development of advanced technologies will contribute to the growth of the radar sensor market in the automotive industry.

Growing sensors and technologies demand building autonomous vehicles to monitor their environment including cameras, LIDAR (Light Detection and Ranging), radar, and ultrasonics.

Using machine learning algorithms and other technologies, an autonomous vehicle makes decisions about navigating its surroundings based on data from these sensors.

Through the use of these various sensors, autonomous vehicles can compute their surroundings comprehensively and make real-time decisions to avoid obstacles, stay in their lane, and follow traffic laws.

Compared to radar positioning, laser location becomes increasingly precise with this new method. In low visibility environments, radar sensors can replace laser sensors in vehicles by seeing through dust, smoke, and fog.

With each new development, it appears that autonomous vehicles become more reliable, and they are becoming more widespread in the public eye with every passing day.

Competitive Landscape

Radar sensors are booming in the industry as companies develop devices to detect these signals. The key to gaining market share is providing a variety of products, creating outstanding marketing campaigns, and thoroughly understanding the industry's technical aspects. Different companies can combine their strengths to develop innovative products.

Research and development often result in the development of new products and technologies. Product improvements or the development of new ones can be used to gain a competitive advantage.

- In May 2023, Porsche and Mobileye announced a strategic collaboration for the production of premium ADAS solutions. A new sensor suite from Mobileye called SuperVision will be used in future Porsche models.

- In April 2023, Gapwaves AB (publ) announced that it would acquire 30 percent of Sensrad AB ("Sensrad"), which was previously a wholly owned subsidiary of Qamcom Group AB ("Qamcom"). Sensrad shares are subscribed for a total of SEK 40 million through cash on hand, and the total amount invested is SEK 40 million. A further 30% share of Sensrad can also be acquired by Gapwaves on certain conditions up until June 30, 2024.

Companies Covered in Radar Sensor Market

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Airbus Group

- Delphi Automotive LLP

- Hella KGaA Hueck & Co

- Infineon Technologies AG

- Autoliv Inc.

- Hitachi, Ltd.

- Lockheed Martin Corporation

- NXP Semiconductors N.V.

- Smart Microwave Sensors GmbH

- Start-Up Ecosystem

- Echodyne, Inc.

- Oculii Corporation

- Northrop Grumman Corporation

- ManTech International Corporation

- Saab AB

- Arbe Robotics

Frequently Asked Questions

Globally, the radar sensor market was worth US$ 8 billion by 2022.

By 2023, the radar sensor is expected to generate US$ 9.5 billion in revenue.

Radar sensor market growth is expected to reach US$ 45 billion by 2033.

The radar sensor market is expected to grow at a CAGR of 16.8% during the forecast period.

According to PMR, radar sensor sales increased by 19.6% between 2018 and 2022.

Automotive application is expected to increase by 16.5% by 2033.

The radar sensor market in Japan is expected to grow by 16.2% CAGR over the next few years.