- Aerospace & Defense

- Military Land Vehicles Market

Military Land Vehicles Market Size, Share, and Growth Forecast, 2025 - 2032

Military Land Vehicles Market by Vehicle Type (Armored Vehicles, Tactical Vehicles, Logistics Vehicles, Combat Vehicles), Technology (Internal Combustion Engine, Hybrid, Electric, Autonomous Systems), End-use (Defense Forces, Private Contractors, Government Agencies), and Regional Analysis for 2025 - 2032

Military Land Vehicles Market Size and Trends Analysis

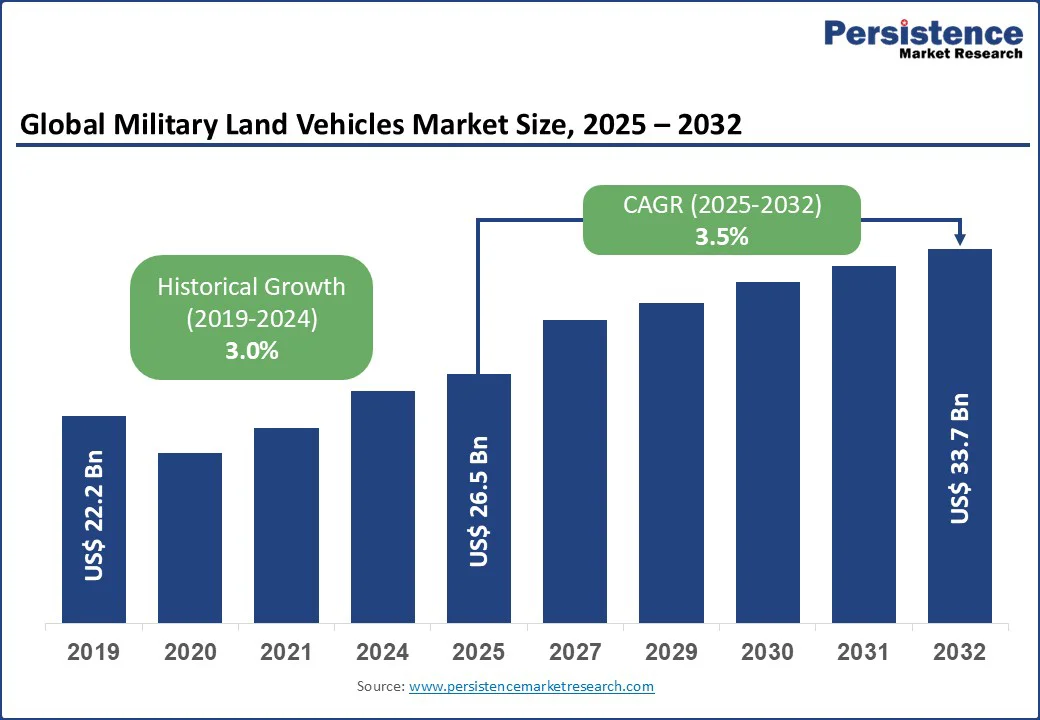

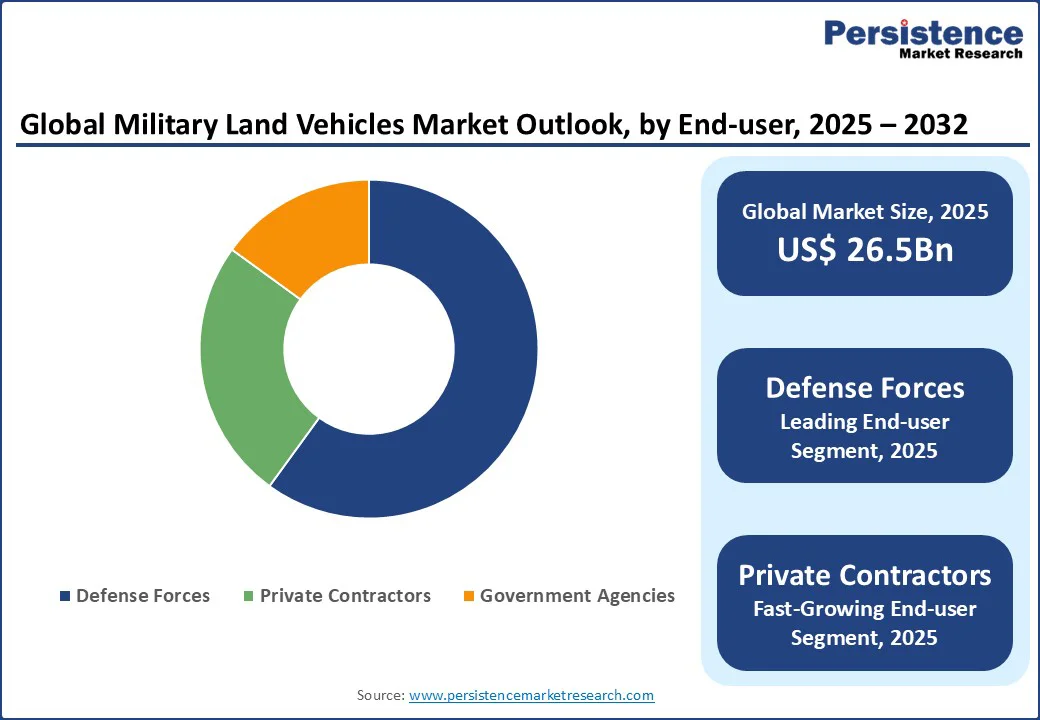

The global military land vehicles market size is likely to be valued at US$26.5 Bn in 2025 and is expected to reach US$33.7 Bn by 2032, growing at a CAGR of 3.5% during the forecast period from 2025 to 2032.

Key Industry Highlights:

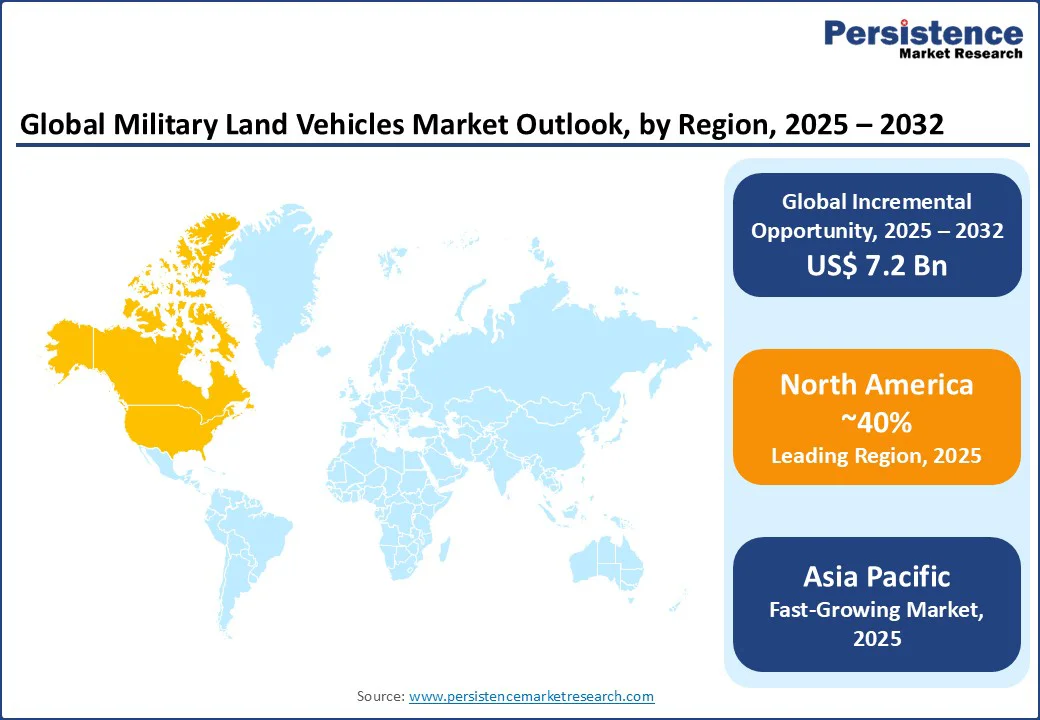

- Leading Region: North America, holding a 40% market share in 2025, driven by the presence of major defense hubs in the U.S., high adoption of advanced military technologies, and strong demand for combat and surveillance applications.

- Fastest-growing Region: Asia Pacific is emerging as the fastest-growing market, fueled by rapid defense program developments, increasing government investments in military infrastructure, and growing demand for tactical and armored vehicles in countries such as China and India.

- Dominant Vehicle Type: Armored Vehicles, commanding nearly 53% market share, due to their robustness, rapid deployment, and widespread adoption in operations for various applications.

- Leading Technology: Internal combustion engine, accounting for over 60% of market revenue, driven by the need for reliable power and endurance in expanding defense networks.

| Global Market Attribute | Key Insights |

|---|---|

| Military Land Vehicles Market Size (2025E) | US$26.5 Bn |

| Market Value Forecast (2032F) | US$33.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.0% |

The military land vehicles industry has experienced significant growth, driven by the increasing need for advanced defense capabilities, rising adoption of autonomous and electrified systems across militaries, and advancements in modular and hybrid technologies. The demand for reliable vehicles in complex military operations, particularly in combat, logistics, and defense sectors, has significantly boosted market expansion.

Rise in Global Defense Spending

The growing global defense spending in industries such as combat, logistics, tactical operations, and surveillance has significantly driven the adoption of military land vehicles. Over the past decade, the demand for robust, cost-effective, and easily deployable vehicles has surged across both government and private sectors.

Military land vehicles are widely used for applications such as combat support, logistics transport, tactical maneuvers, and defense, making them a versatile solution for organizations seeking rapid access to ground-based capabilities. Their relatively lower cost of development and shorter production cycles compared to aerial systems have made them particularly attractive to militaries, contractors, and emerging defense companies.

The rising trend of military modernization, especially for integrated ground forces projects led by countries such as the U.S. (Future Combat Systems) and NATO allies, has further accelerated the deployment of land vehicles. This growth creates significant demand for reliable and efficient vehicle systems, including propulsion, armor, autonomy, and data handling. For instance, main battle tanks and armored personnel carriers rely heavily on advanced integrated systems to achieve mission objectives despite challenging terrains. As the defense industry shifts toward high-volume vehicle upgrades, the demand for advanced military land vehicles is expected to remain a critical driver of market expansion.

High Procurement and Maintenance Costs

The high costs associated with procuring and maintaining military land vehicles hamper market growth. The procurement and long-term maintenance of military land vehicles represent one of the most significant restraints for market growth. Armored cars, tactical trucks, and combat platforms require highly specialized technologies, advanced materials, and integrated systems such as active protection, digital communication, and surveillance equipment. These features substantially raise the initial purchase cost.

Beyond acquisition, maintenance costs remain a persistent challenge. Military land vehicles operate in extreme terrains and combat environments, requiring frequent overhauls, spare parts, and technical expertise. The complexity of modern vehicles equipped with hybrid propulsion, electronic warfare systems, and AI-enabled features adds to servicing costs and requires continuous investments in training and infrastructure. While developed countries can allocate higher budgets for lifecycle support, developing nations often face financial strain, restricting large-scale procurement.

For instance, the M1 Abrams tank is notably more expensive to operate and support than its predecessor, the M60 tank. Despite expectations for reduced operational costs, the Abrams tank's operating and support (O&S) costs are currently three to four times higher than those of the M60. These high costs not only slow adoption but also intensify reliance on upgrade and retrofit programs rather than new vehicle acquisitions, ultimately restraining overall market expansion.

Advancements in Electric and Autonomous Vehicle Technologies

Advancements in electric and autonomous military land vehicle technologies present a significant growth opportunity for the domain. Electric designs allow vehicle manufacturers to build flexible and scalable systems that can be customized for diverse missions, ranging from combat and logistics to tactical operations and surveillance. This reduces both development time and overall costs, making vehicles more accessible for defense forces, contractors, and emerging military programs.

Additionally, electrification supports easier upgrades and component replacements, extending vehicle lifespans and improving return on investment. For instance, the U.S. Army is developing the robotic combat vehicle-light (RCV-L. This small, lightweight hybrid-electric unmanned ground combat vehicle can be transported easily by military aircraft. This vehicle is part of the Army's effort to field robotic combat vehicles in future operations.

The integration of autonomous systems into vehicles further enhances performance by enabling unmanned operations, predictive maintenance, and efficient resource management. Autonomous-driven systems can optimize navigation, threat detection, and fuel management in real time, reducing dependency on human operators and ensuring higher mission reliability.

For instance, Oshkosh Defense developed the TerraMax autonomous driving technology, which was integrated into the M-ATV armored vehicle. This system utilizes radar, LIDAR, and a drive-by-wire system to navigate challenging terrains autonomously.

The TerraMax-equipped vehicles can detect and neutralize roadside bombs, IEDs, and mines, enhancing mission safety and efficiency. Additionally, the system allows a single operator to manage multiple vehicles, optimizing convoy operations.

Category-wise Analysis

Vehicle Type Insights

Armored vehicles dominate, expected to account for approximately 53% share in 2025. Its dominance stems from its robustness, rapid development cycles, and ease of integration with forces for applications such as combat and surveillance.

Armored vehicle systems, such as those offered by BAE Systems and Rheinmetall, enable real-time protection, force scalability, and seamless collaboration across missions, making them a preferred choice for industries such as defense and logistics. Their modular designs also reduce upfront costs, driving adoption among contractors and agencies.

The combat vehicles segment is the fastest-growing, driven by industries with high-performance requirements, such as military operations and tactical support. Combat vehicle systems offer greater payload capacity and customization, appealing to large enterprises with complex missions.

The growing focus on ground warfare and high-mobility platforms, such as U.S. DoD initiatives, is accelerating the adoption of combat systems in regions such as North America and Europe, with significant growth potential in high-stakes applications.

Technology Insights

Internal combustion engine leads the military land vehicles market, holding a 60% share in 2025. The segment’s dominance is driven by the need for reliable power and endurance in expanding defense networks, particularly in rugged and long-range operations. Engine subsystems streamline the integration of propulsion payloads, reduce failures, and improve operational efficiency, making them critical for providers such as General Dynamics and Oshkosh Corporation.

The electric segment is the fastest-growing, fueled by the rapid growth of sustainable defense and the need for low-emission mobility. The rise in green military platforms and the increasing demand for silent operations have spurred the adoption of electric systems in this sector. The Asia Pacific region, with its booming defense needs, is driving rapid adoption in this segment.

End-use Insights

Defense forces hold the largest market share, accounting for approximately 60% of revenue in 2025. Defense forces' end-use allows vendors such as Lockheed Martin and Elbit Systems to maintain close relationships with customers, offer tailored vehicles, and provide dedicated support. This end-use is particularly dominant in applications with complex requirements, such as combat and logistics, where customized solutions are critical.

The private contractors' end-use is the fastest-growing, driven by the increasing adoption of outsourced defense technologies and the rise of support constellations for surveillance and transport. These platforms offer seamless access to vehicle systems, enabling faster development and integration with other defense services. The growing popularity of contractor-focused vehicles among governments and agencies is accelerating the adoption of solutions through this end-use, particularly in North America and the Asia Pacific.

Regional Insights

North America Military Land Vehicles Market Trends

North America is projected to account for nearly 40% of the global military land vehicles market, reflecting its leadership in defense innovation and technology adoption. The region’s dominance is primarily driven by the presence of major defense hubs in the United States, which host leading companies such as Lockheed Martin, General Dynamics, and Northrop Grumman. These firms play a pivotal role in developing advanced vehicle systems that support critical missions in combat, logistics, tactical operations, and surveillance.

The region’s strong adoption of cutting-edge military technologies is further fueled by robust government investments, particularly through the U.S. Department of Defense, the Army, and the Marine Corps, which continue to prioritize ground mobility, security, and intelligence gathering.

Additionally, the rising demand for autonomous and hybrid vehicles, particularly for expeditionary forces, has accelerated the development of cost-effective and modular systems. With a combination of defense-driven demand, commercial initiatives, and private investments in vehicle upgrades, North America continues to set global standards in reliability, performance, and innovation, making it a frontrunner in shaping the future trajectory of the military land vehicles market.

Europe Military Land Vehicles Market Trends

Europe is emerging as a significant player in the military land vehicles market, supported by strong institutional frameworks and collaborative defense programs. The European Defence Agency (EDA), along with national agencies such as the UK Ministry of Defence, Germany's Bundeswehr, and France's DGA, is driving extensive investments in vehicle missions for combat, logistics, tactical support, and surveillance. These initiatives are fueling demand for advanced and modular vehicle systems capable of supporting multi-mission requirements.

The region is also home to leading defense companies, including BAE Systems, Rheinmetall, and Leonardo S.p.A., which are at the forefront of developing cutting-edge technologies. With a focus on hybrid architectures, autonomous navigation, and AI-enabled operations, European manufacturers are increasingly catering to both government and contractor end-users.

Europe’s growing emphasis on sovereign defense capabilities and reducing reliance on external suppliers is encouraging greater R&D for systems that enhance autonomy and resilience. The rising demand for vehicle-based logistics, border security systems, and joint operations such as NATO further strengthens Europe’s market position, ensuring steady growth in the coming years.

Asia Pacific Military Land Vehicles Market Trends

Asia Pacific is positioned as the fastest-growing market for military land vehicles, supported by rapid advancements in defense programs and the rise of government investments in military infrastructure. Countries such as China, India, and Japan are leading the region’s expansion, with China accelerating its vehicle modernization programs for combat, logistics, and tactical operations. At the same time, India’s DRDO continues to launch cost-effective vehicles with global recognition. Japan, through its Self-Defense Forces, is focusing on surveillance missions and next-generation technologies.

The increasing need for high-mobility armored vehicles to support border security, disaster response, urban operations, and threat monitoring is driving demand for compact, efficient, and modular systems. Similarly, the surge in tactical vehicles to expand ground forces and networks across underserved regions is boosting adoption.

Private players and emerging defense startups are also contributing by leveraging hybrid vehicle technologies to deliver affordable solutions. With supportive government policies, advancements in electric-enabled systems, and expanding applications, the Asia Pacific is expected to dominate future vehicle deployment, creating substantial opportunities for vendors.

Competitive Landscape

The global military land vehicles market is characterized by intense competition, regional strengths, and a mix of global and niche players. In developed regions such as North America and Europe, large firms such as Lockheed Martin Corporation, General Dynamics, and BAE Systems dominate through scale, advanced R&D capabilities, and established partnerships with defense agencies.

In the Asia Pacific, rapid defense developments and increasing demand for tactical vehicles are attracting significant investments from both international players, such as Oshkosh Corporation and Rheinmetall, and regional vendors.

Companies are focusing on product innovation, modular designs, and strategic alliances to gain a competitive edge. The development of autonomous-powered and electrified vehicle systems has emerged as a key differentiator, enabling faster adoption in combat, logistics, and surveillance sectors.

Strategic collaborations, acquisitions, and digital-first approaches for supply chain and marketing are further intensifying the competitive landscape. The industry exhibits a dual nature, consolidated at the top by global giants while remaining fragmented across numerous regional and niche players catering to local preferences and cost-sensitive segments.

Key Developments

- In February 2024, the U.S. Marine Corps selected Navistar Defense (formerly ND Defense) to participate in Phase I of the Medium Tactical Truck (MTT) program. This initiative aims to replace the existing Medium Tactical Vehicle Replacement (MTVR) fleet, including cargo, dump, wrecker, tractor, and resupply vehicles.

- In May 2024, Textron Systems announced a collaboration with Kodiak Robotics to develop an autonomous military ground vehicle specifically designed for driverless operations. This partnership integrates Kodiak's autonomous system into a Textron Systems prototype, a purpose-built uncrewed military vehicle.

Companies Covered in Military Land Vehicles Market

- Navistar Defense

- Textron

- KMW

- Rheinmetall

- BAE Systems

- Elbit Systems

- Oshkosh Corporation

- Northrop Grumman

- Leonardo S.p.A.

- SAIC

- AM General

- Lockheed Martin

- Honeywell

- Thales Group

- General Dynamics

- Others

Frequently Asked Questions

The global Military Land Vehicles Market is projected to reach US$ 26.5 Bn in 2025.

The increasing global defense spending is a key driver.

The military land vehicles market is poised to witness a CAGR of 3.5% from 2025 to 2032.

Advancements in electric and autonomous vehicle technologies are a key opportunity.

Navistar Defense, Textron, KMW, Rheinmetall, BAE Systems, Elbit Systems, Oshkosh Corporation, Northrop Grumman, Leonardo S.p.A., SAIC, AM General, Lockheed Martin, Honeywell, Thales Group, and General Dynamics are key players.