- Aerospace & Defense

- Military Floating Bridge Market

Military Floating Bridge Market Size, Share, and Growth Forecast, 2025 - 2032

Military Floating Bridge Market by Product Type (Modular Floating Bridges, Panel Bridges, Beam Bridges, Special Purpose Floating Bridges), Application (Military Operations, Humanitarian Assistance, Disaster Relief, Training Exercises), End-use (Army, Navy, Air Force, Defense Contractors), and Regional Analysis for 2025 - 2032

Military Floating Bridge Market Size and Trends Analysis

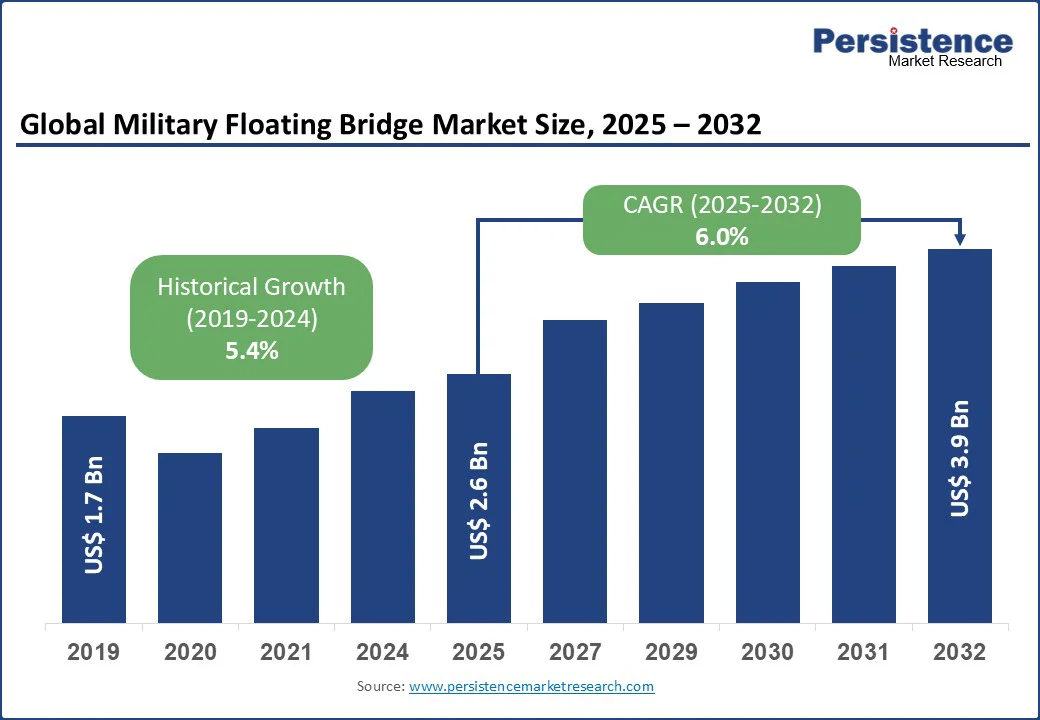

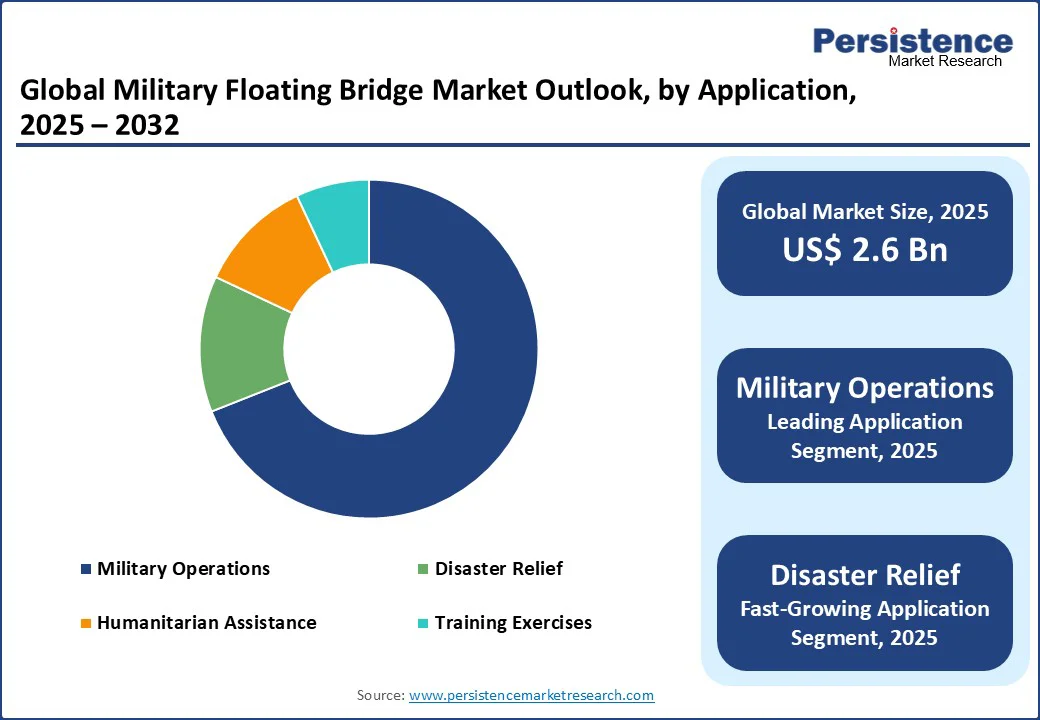

The global military floating bridge market size is likely to be valued at US$ 2.6 Bn in 2025 and is expected to reach US$ 3.9 Bn by 2032, registering a CAGR of 6.0% during the forecast period from 2025 to 2032.

The military floating bridge market has experienced steady growth, driven by increasing geopolitical tensions, rising defense budgets, and advancements in bridge construction technologies.

Military floating bridges, also known as pontoon bridges, enable armed forces to transport troops, vehicles, and supplies across waterways where permanent bridges are absent or damaged. The growing need for rapid deployment in military operations and disaster relief scenarios, coupled with innovations in lightweight and modular bridge designs, is fueling market expansion.

Key Industry Highlights:

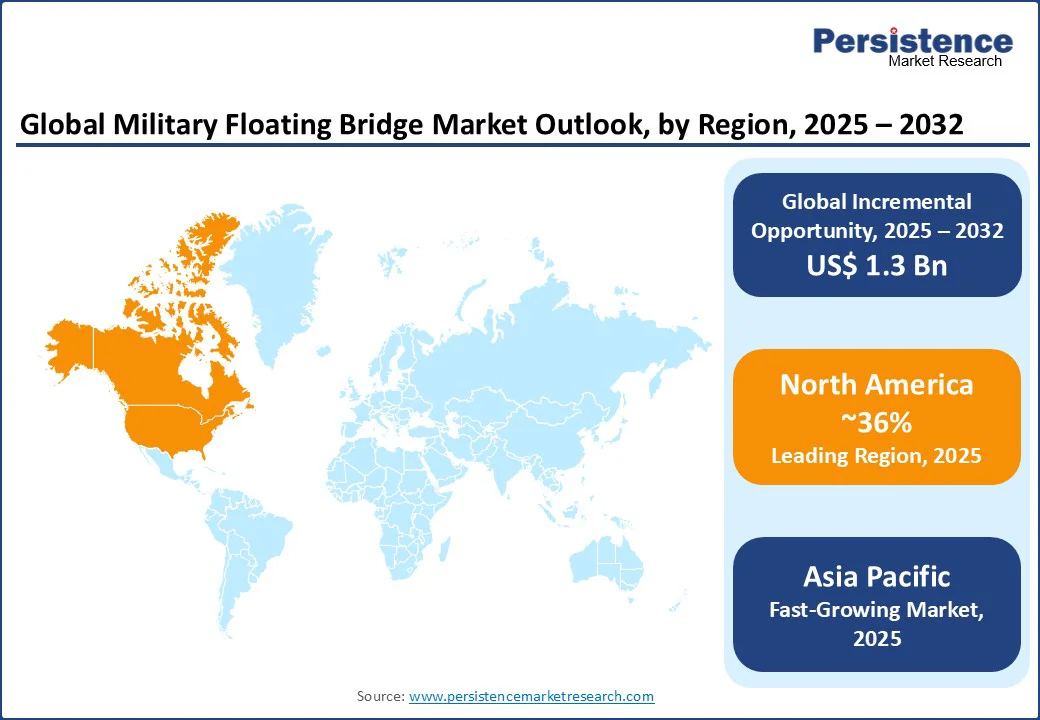

- Leading Region: North America, holding a 36% market share in 2025, driven by robust defense budgets and advanced military infrastructure in the U.S.

- Fastest-growing Region: Asia Pacific, propelled by increasing military expenditures and regional conflicts in countries such as India and China.

- Dominant Type: Modular Floating Bridges, commanding nearly 42% market share, due to their versatility and rapid deployment capabilities.

- Leading Application: Military Operations, accounting for over 69% of market revenue, driven by the critical need for mobility in combat scenarios.

|

Global Market Attribute |

Key Insights |

|

Military Floating Bridge Market Size (2025E) |

US$ 2.6 Bn |

|

Market Value Forecast (2032F) |

US$ 3.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.4% |

Market Dynamics

Driver - Increasing Geopolitical Tensions and Defense Budgets

The military floating bridge market is driven by the rise in geopolitical tensions across various regions, coupled with increasing defense budgets. As nations face evolving security threats, including territorial disputes, regional conflicts, and the need to secure critical infrastructure, the demand for rapid deployment and versatile military bridging solutions has intensified. Floating bridges allow armed forces to swiftly transport heavy vehicles, equipment, and personnel across rivers, lakes, or other water obstacles, enhancing operational flexibility and strategic mobility in contested areas. For instance, during DEFENDER-Europe 22, the U.S. Army employed a float ribbon bridge system to move tanks and armored vehicles across the Vistula River in Poland, demonstrating rapid deployment in a real-world exercise.

Rising defense expenditures are further amplifying this trend. Countries are investing heavily in modernizing military engineering capabilities, focusing on technologies that enable rapid, efficient, and reliable logistics support. Governments in North America, Europe, and Asia are allocating substantial budgets to procure advanced floating bridges, upgrade existing infrastructure, and integrate these systems with other tactical platforms. For example, Poland signed agreements with CNIM to acquire motorized floating bridges to enhance mobility for its armed forces.

Additionally, modernization programs emphasize lightweight, modular, and easily deployable bridge systems, reducing setup times and operational costs. The combination of heightened geopolitical risks and robust defense spending ensures sustained demand for military floating bridges, making them a critical component of contemporary defense strategy and force projection worldwide.

Restraint - High Initial Costs and Logistical Challenges

High initial costs and logistical challenges associated with military floating bridges pose significant restraints to market growth. Advanced floating bridges, especially modular and motorized variants, require substantial investment in design, manufacturing, and specialized materials, making upfront procurement expensive for defense budgets. In addition to purchase costs, operational deployment demands trained personnel, specialized transport vehicles, and supporting equipment to assemble, launch, and maintain the bridges in various terrains.

Logistical challenges further compound the issue. Transporting heavy bridge components to remote or conflict-prone areas can be difficult, particularly in regions with poor infrastructure or limited access to waterways. Environmental factors such as strong currents, flooding, or icy conditions can delay deployment or reduce operational efficiency. Moreover, maintenance and storage of large-scale bridge modules require dedicated facilities and ongoing upkeep, adding to lifecycle costs. These financial and operational burdens can limit adoption, particularly for smaller defense forces or nations with constrained defense budgets. For instance, during exercises in Eastern Europe, several Eastern European armies reported delays in deploying modular floating bridges due to a combination of heavy components, limited transport vehicles, and river conditions, highlighting the operational challenges faced in real-world scenarios.

Opportunity - Advancements in Lightweight and Modular Bridge Technologies

Technological advancements in lightweight and modular bridge technologies are expected to present significant growth opportunities for the military floating bridge market. Innovations in materials, such as high-strength composites and aluminum alloys, have enabled the development of lighter, more durable, and easier-to-deploy floating bridges. These advancements reduce transportation costs and enhance rapid deployment capabilities, making them ideal for modern warfare and disaster relief operations. For instance, WFEL’s Dry Support Bridge, which utilizes lightweight, modular components, can be deployed in under 90 minutes, significantly enhancing operational efficiency.

The integration of automation and smart engineering, such as self-propelled modular bridges, is transforming the industry. Companies such as CNIM are developing automated deployment systems that reduce the need for manual labor, enhancing safety and speed. The growing focus on sustainable materials and designs that minimize environmental impact also opens new avenues for innovation. These technological advancements are attracting investments from defense agencies and creating opportunities for market players to develop next-generation floating bridge solutions tailored to diverse operational needs.

Category-wise Analysis

Product Type Insights

Modular floating bridges dominate and is expected to account for approximately 42% of the share in 2025. Their dominance stems from their versatility, rapid assembly, and ability to support heavy military vehicles, such as tanks and armored personnel carriers. Modular designs allow for quick reconfiguration and scalability, making them suitable for a wide range of terrains and mission requirements. Their compatibility with existing military logistics and proven performance in combat scenarios make them a preferred choice for armies worldwide.

The special purpose floating bridges segment is the fastest-growing, driven by its tailored applications in niche scenarios, such as rapid river crossings in extreme conditions or support for humanitarian missions. These bridges incorporate advanced materials and designs to meet specific operational needs, such as enhanced buoyancy or resistance to environmental stressors. The Asia Pacific region, particularly India and China, is a key contributor to this growth due to increasing investments in specialized military infrastructure.

Application Insights

Military operations lead the military floating bridge market, holding a 69% share in 2025. The critical need for mobility in combat scenarios, including troop deployment and equipment transport across waterways, drives this segment’s dominance. Floating bridges are essential for maintaining operational flexibility in conflict zones, where permanent infrastructure may be damaged or absent. Government investments in military modernization and rapid deployment capabilities further support this segment’s growth.

The disaster relief segment is the fastest-growing, fueled by the increasing frequency of natural disasters and the need for rapid infrastructure solutions. Floating bridges are vital for delivering aid, evacuating civilians, and restoring connectivity in flood-affected or earthquake-damaged regions. The Asia Pacific region, prone to seasonal floods and typhoons, is a significant driver of this segment’s growth, with countries such as India and Japan prioritizing floating bridge deployments for disaster response.

End-Use Insights

Army dominates and accounts for approximately 55% of revenue in 2025. Armies worldwide rely on floating bridges to support ground operations, including the transport of heavy vehicles and troops across rivers and lakes. The adoption of modular and special-purpose bridges by armies, driven by the need for rapid deployment and operational flexibility, fuels this segment’s dominance.

The defense contractors segment is the fastest-growing, driven by increasing outsourcing of military infrastructure projects to private firms. Defense contractors, such as General Dynamics and WFEL, are investing in R&D to develop innovative bridge systems tailored to specific military needs. The growing trend of public-private partnerships in defense procurement, particularly in North America and Europe, is accelerating this segment’s growth.

Regional Insights

North America Military Floating Bridge Market Trends

North America is poised to hold a dominant position in the global military floating bridge market, capturing an estimated 36% share in 2025. This leadership is primarily driven by the region’s robust defense budgets, particularly in the United States, which consistently allocates substantial resources toward modernizing its military engineering capabilities. The U.S. Army, for instance, invests heavily in advanced bridging solutions to ensure rapid deployment and strategic mobility for heavy vehicles and equipment across rivers, lakes, and other water obstacles during both peacetime exercises and combat scenarios.

In addition to strong financial backing, North America benefits from a highly developed military infrastructure and technological expertise. The presence of leading manufacturers, such as General Dynamics and Oshkosh Defense, facilitates the development and procurement of modular, motorized, and lightweight floating bridge systems. These systems are designed for rapid assembly, reduced manpower requirements, and high load-bearing capacity, making them ideal for a variety of operational scenarios, including disaster relief, multinational exercises, and tactical military operations.

Ongoing modernization programs emphasize integrating floating bridge systems with digital command and control platforms, improving coordination and operational efficiency. The combination of substantial defense spending, technological innovation, and strategic focus on mobility ensures North America’s continued dominance through 2025 and beyond.

Europe Military Floating Bridge Market Trends

Europe holds a significant share of the military floating bridge market in 2025. This dominance is driven by stringent NATO defense requirements, increasing regional security concerns, and widespread adoption in countries such as Germany, France, and the U.K. Policies such as NATO’s Defense Planning Process and the European Defence Fund encourage investments in advanced military infrastructure, including floating bridges, to ensure operational readiness.

Technological advancements are supporting market growth, with companies such as CNIM and WFEL developing modular and self-propelled bridge systems tailored to NATO standards. For instance, in 2021, General Dynamics European Land Systems delivered floating bridges to the German Bundeswehr to support amphibious operations. The growing focus on joint military exercises and disaster response capabilities is further accelerating adoption. Countries such as Germany and France are integrating floating bridges into urban and rural defense strategies, combining mobility with operational flexibility. This trend highlights Europe’s leadership in military engineering and positions the region as a key driver of market innovation.

Asia Pacific Military Floating Bridge Market Trends

Asia Pacific is emerging as the fastest-growing region globally, driven by rapid military modernization, geopolitical tensions, and disaster-prone environments. Countries such as China, India, and Japan are at the forefront, promoting investments in floating bridge technologies through increased defense budgets and infrastructure development programs. India’s border conflicts with China and Pakistan have led to significant procurement of modular floating bridges, with companies such as China Harzone Industry supplying advanced systems.

Technological advancements, such as lightweight composites and automated deployment systems, enable integration into diverse terrains, including mountainous and riverine regions. Companies such as Jiangsu Bailey Steel Bridge are developing cost-effective solutions tailored to local operational needs. The growing emphasis on disaster relief, particularly in flood-prone countries such as India and Japan, is fueling demand. Initiatives such as China’s Belt and Road Initiative and India’s Atmanirbhar Bharat program are positioning the Asia Pacific as a hub for military floating bridge innovation and large-scale market expansion.

Competitive Landscape

The global military floating bridge market is characterized by intense competition, regional strengths, and a mix of established global players and innovative local manufacturers. In developed regions such as North America and Europe, major firms such as General Dynamics, CNIM, and WFEL dominate through scale, advanced R&D capabilities, and strategic contracts with defense agencies. These companies focus on high-performance, modular solutions, including self-propelled and lightweight bridges, to differentiate themselves in military and disaster relief applications.

In Asia Pacific, rapid military modernization and large-scale infrastructure projects are attracting investments from international players, such as China Harzone Industry, and regional manufacturers such as Jiangsu Bailey Steel Bridge, offering cost-effective and customized solutions. Companies are prioritizing product innovation, sustainable materials, and geographic expansion. Strategic partnerships, defense contracts, and eco-friendly designs, such as Mabey’s compliance with international military standards, are enhancing market penetration. The sector exhibits a dual structure: consolidated at the top by global leaders while remaining fragmented among regional and niche players serving application-specific and price-sensitive segments.

Industry Developments:

- In October 2024, China Harzone successfully delivered a floating trestle bridge for Yichun Luming Mining Co., Ltd., which passed the product acceptance review and was opened to traffic.

- In April 2025, CNIM introduced the PFM Motorized Floating Bridge, a versatile system enabling continuous or discontinuous crossing of wet gaps for MLC 70 vehicles, available in fixed bridge or ferry configurations.

Companies Covered in Military Floating Bridge Market

- AM General

- China Harzone Industry

- CNIM

- Jiangsu Bailey Steel Bridge

- General Dynamics

- RPC Technologies

- FBM Babcock Marine

- Mabey

- Oshkosh Defense

- WFEL

- Others

Frequently Asked Questions

The global Military Floating Bridge Market is projected to reach US$ 2.6 Bn in 2025.

Increasing geopolitical tensions and defense budgets are key drivers.

The military floating bridge market is poised to witness a CAGR of 6.0% from 2025 to 2032.

Advancements in lightweight and modular bridge technologies are a key opportunity.

AM General, China Harzone Industry, CNIM, Jiangsu Bailey Steel Bridge, and General Dynamics are key players.