- Non-food Packaging

- Luxury Rigid Box Market

Luxury Rigid Box Market Size, Share, and Growth Forecast, 2026-2033

Luxury Rigid Box Market by Box Type (Two-Piece Boxes, Magnetic Closure Boxes, Flip-Top Boxes, Slide-Out Boxes, Collapsible Rigid Boxes), Material (Solid Bleached Sulfate (SBS) Board, Chipboard, Recycled Paperboard, Fabric-Wrapped Boxes, Wooden Boxes), End-Use Industry (Cosmetics & Personal Care, Jewelry & Watches, Fashion & Accessories, Consumer Electronics, Premium Food & Confectionery), and Regional Analysis for 2026-2033

Luxury Rigid Box Market Share and Trends Analysis

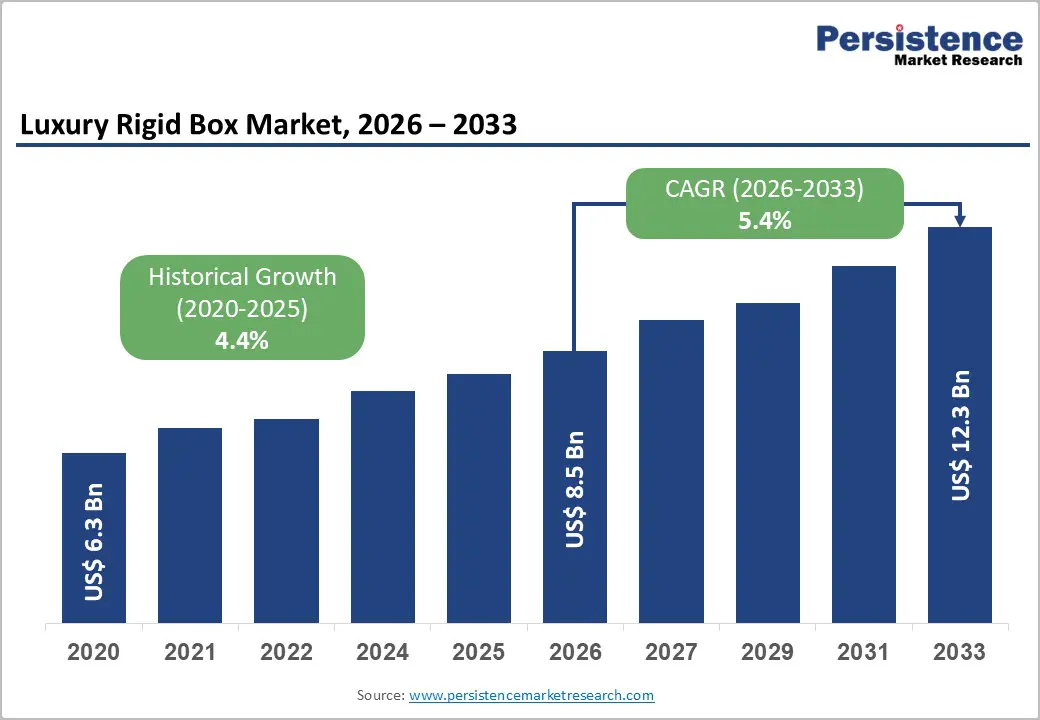

The global luxury rigid box market size is likely to be valued at US$ 8.5 billion in 2026, and is projected to reach US$ 12.3 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026–2033.

Increasing premiumization across cosmetics, fashion, and consumer electronics, along with the continued expansion of global luxury retail channels, is primarily driving market growth. According to the Organization for Economic Co-operation and Development (OECD) and the World Bank, rising disposable incomes in emerging economies are strengthening consumer spending on premium and aspirational products. Luxury brands actively adopt premium rigid packaging solutions to reinforce brand identity and enhance perceived product value. The rapid growth of e-commerce and direct-to-consumer luxury retail also increases the need for durable and visually appealing packaging. As a result, companies increasingly use high-end rigid boxes to differentiate products, support sustainability goals, and deliver enhanced unboxing experiences that strengthen customer engagement.

Key Industry Highlights

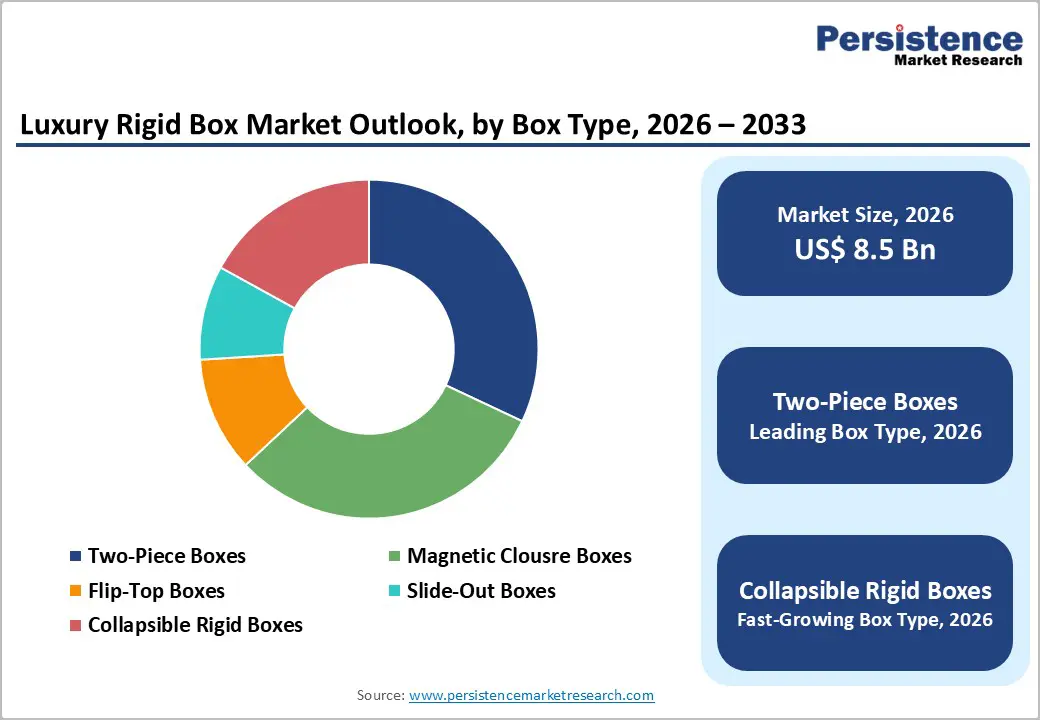

- Dominant Box Type: Two-piece rigid boxes are set to hold around 32% revenue share in 2026, while collapsible rigid boxes are likely to grow the fastest at over 6% CAGR through 2033, driven by e-commerce growth and seasonal product launches.

- Leading Material: Solid bleached sulfate (SBS) board is expected to lead with approximately 34% share in 2026, while recycled paperboard is anticipated to be the fastest-growing segment during 2026–2033, reflecting a preference for sustainable materials.

- Dominant End-Use Industry: Cosmetics & personal care are projected to account for roughly 36% of global demand in 2026, while premium food and confectionery are poised to be the fastest-growing segment, fueled by gifting culture and festive packaging.

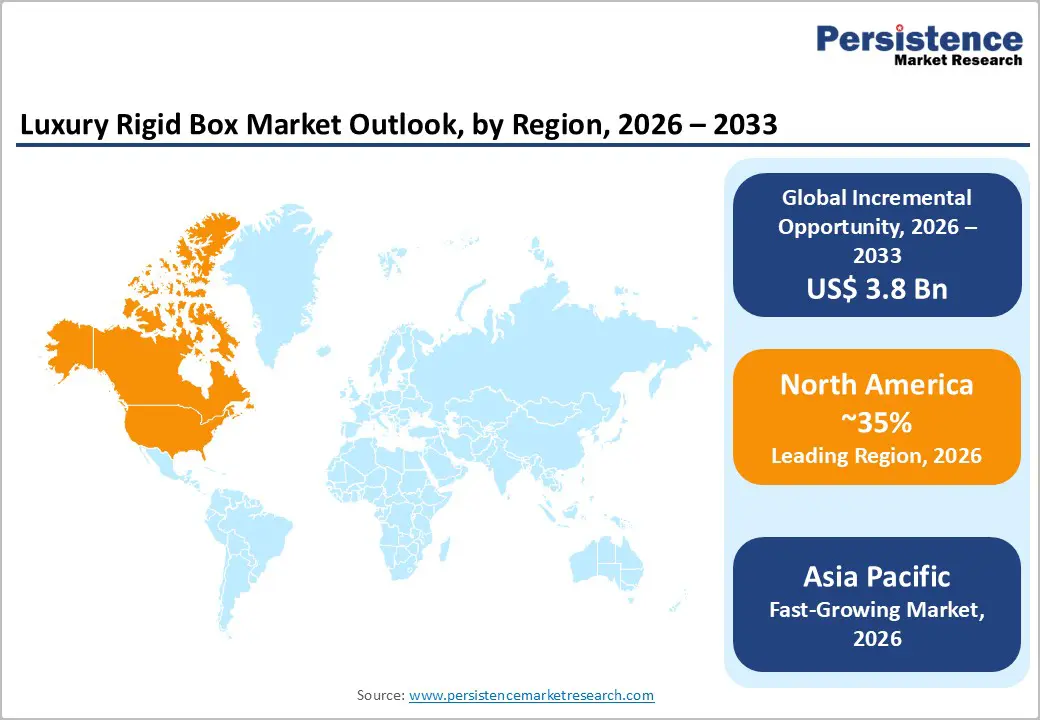

- Regional Leadership: North America is poised to dominate with an estimated 35% share in 2026, led by strong luxury retail demand, while Asia Pacific is expected to register the fastest regional growth through 2033.

- Market Trends: Increasing adoption of sustainable rigid packaging materials and customized luxury packaging designs are expected to remain key industry trends through 2033, enabling brands to strengthen consumer engagement, brand storytelling, and premium product differentiation.

| Key Insights | Details |

|---|---|

|

Luxury Rigid Box Market Size (2026E) |

US$ 8.5 Bn |

|

Market Value Forecast (2033F) |

US$ 12.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of the Global Luxury Goods Industry

One of the primary drivers of the luxury rigid box market is the sustained expansion of the global luxury goods sector. According to industry data published by Bain & Company and the Italian luxury goods association Altagamma, the global personal luxury goods market reached approximately € 358 billion in 2025, while overall luxury industry spending across goods and experiences totaled nearly € 1.44 trillion, with long-term growth supported by high-income consumers and younger luxury buyers. Luxury brands invest heavily in premium packaging solutions, including magnetic rigid boxes and custom rigid boxes, to strengthen brand perception and customer engagement. Recent industry coverage from Reuters indicates that the luxury sector is expected to return to 3–5% growth in 2026, supported by resilient demand across the United States, Europe, Japan, and improving consumption trends in China.

Rigid boxes are particularly preferred for products such as watches, cosmetics, perfumes, and high-end fashion accessories due to their durability, aesthetics, and protection. Luxury brands increasingly focus on premium unboxing experiences as a strategic tool to build emotional connections with customers. High-quality packaging also supports storytelling, limited-edition releases, and premium gifting experiences. Industry observations from luxury retail coverage highlight that brands are intensifying investments in product presentation and packaging to maintain desirability and reinforce brand value in a competitive global market. As luxury consumption expands across developed and emerging markets, demand for custom luxury rigid packaging continues to grow steadily.

E-Commerce Expansion and Sustainability-Driven Packaging Adoption

The shift toward digital retail channels is another significant factor driving demand for rigid packaging solutions. According to the International Trade Administration of the U.S. Department of Commerce, global cross-border e-commerce is projected to exceed US$ 7 trillion by 2030, creating strong demand for protective yet visually appealing packaging formats. Luxury brands selling online require packaging that can withstand long shipping distances while preserving product presentation and brand identity. Rigid boxes, especially magnetic closure boxes and collapsible rigid boxes, provide structural strength and premium aesthetics, making them highly suitable for direct-to-consumer shipments.

The sustainability regulations and consumer expectations are reshaping the global luxury packaging market. The European Commission (EC)’s Circular Economy Action Plan and similar regulatory initiatives across major economies encourage companies to reduce plastic packaging and adopt recyclable materials. In parallel, several packaging innovation initiatives and investments in biodegradable materials were announced in 2025, reflecting the industry’s shift toward environmentally responsible solutions. For instance, sustainable materials startups secured funding to scale plant-based alternatives to single-use plastics, signaling growing industry momentum toward eco-friendly packaging technologies. As a result, luxury brands are increasingly adopting recycled paperboard, chipboard, and fiber-based rigid boxes to align with sustainability commitments and evolving regulatory standards.

High Production and Material Costs

The production of luxury rigid boxes relies on high-quality materials, intricate finishing techniques, and complex manufacturing processes such as embossing, foil stamping, and fabric wrapping, leading to significantly higher costs compared to conventional cartons. Decorative finishes and premium substrates can increase production costs by 30–50%, limiting adoption by mid-tier brands and smaller luxury players. Manufacturers must carefully balance design innovation and cost efficiency to maintain profitability without compromising packaging quality.

Recent industry movements further underscore this restraint. In March 2026, major packaging supplier Greif announced significant price increases for uncoated recycled paperboard products, citing rising labor, utility, and transportation costs, reflecting broader cost pressures for primary packaging inputs that directly feed rigid box production. Likewise, reports of global paper price hikes indicate that board producers are implementing new pricing for paper and board grades in 2026, which is expected to ripple through packaging costs across Europe and other markets. These inflationary pressures in raw materials and processing inputs create ongoing challenges for rigid packaging manufacturers and brand owners alike, particularly for seasonal or limited-edition luxury products.

Supply Chain Volatility in Paperboard and Specialty Materials

The availability and stability of SBS board, specialty papers, and other key substrates remain critical for luxury rigid box manufacturing. Throughout 2025 and into 2026, containerboard production in North America saw meaningful declines due to mill closures and capacity reductions, tightening supplies and increasing operating rates, a dynamic that puts upward pressure on pricing and complicates procurement planning for packaging manufacturers. These supply issues have also forced some brands to adjust production schedules, further complicating logistics and inventory management.

In addition, regulatory and trade developments have contributed to material volatility. For example, China’s 2025 restrictions on certain recycled pulp imports have been described within industry publications as a potential “black swan event” for recovered fiber markets, creating uncertainty in global supply flows and price structures for recycled board materials. Such trade policy shifts, coupled with periodic global logistics disruptions such as seasonal slowdowns around major holidays such as Chinese New Year, have materially affected supply chain responsiveness and lead times. These developments highlight continued structural supply risks for luxury rigid packaging producers who depend on stable access to specialty inputs, and underline the importance of robust sourcing and inventory strategies.

Rising Demand from Emerging Luxury Markets

Emerging economies in Asia Pacific, the Middle East, and Latin America present significant growth opportunities for luxury rigid box manufacturers as rising affluence fuels demand for premium goods. According to recent luxury market analyses, the Middle East has distinguished itself as a stand-out growth hub within the global luxury sector, with robust luxury retail activity and strong domestic purchases reported even amid broader industry challenges in 2025. Notably, cities such as Dubai continue to outperform traditional luxury centers, driven by a high proportion of affluent households and sustained consumer appetite for premium products. This growth is also supported by increasing tourism and inflow of international luxury shoppers, further reinforcing demand for high-end packaging solutions.

India’s luxury fashion landscape is also showing rapid evolution, with local designers closing the gap on global players and expanding market relevance beyond traditional bridal segments into ready-to-wear and accessories, reflecting structural growth in domestic premium consumption. This momentum is driving demand for premium packaging formats, particularly as domestic and international brands expand their presence to reach regional affluent and aspirational buyers. Rising interest in gifting culture and seasonal luxury promotions is further driving the need for sophisticated packaging. These regional dynamics support expanding opportunities for customized rigid boxes tailored to trending consumer tastes, cultural preferences, and localized brand positioning strategies.

Technological Advancements in Packaging Design and Printing

Advances in digital printing, automation, and structural packaging design continue to open new avenues for luxury rigid box producers to innovate and capture market share. Industry coverage from 2026 highlights a wave of technological modernization in packaging, where enhanced smart packaging, digital enhancements, and customization capabilities are gaining traction among premium brands seeking deeper consumer engagement. These innovations enable more complex graphics, structural designs, and limited-edition executions that elevate the unboxing experience, a key differentiator in luxury retail environments.

Regional flagship events and trade showcases have also underscored this trend, bringing together luxury brand leaders and packaging innovators to explore automated production systems and next-generation finishing techniques. Growth in e-commerce and omnichannel luxury retail is concurrently elevating demand for packaging that performs both functionally and aesthetically across digital and physical channels. As manufacturers adopt advanced printing and production technologies, they can better meet these evolving demands while expanding into value-added services such as personalization, shorter lead times, and high-precision finishes that align with premium brand strategies.

Category-wise Analysis

Box Type Insights

Two-piece rigid boxes are set to capture about 32% of the global demand in 2026. Featuring a separate lid and base, they offer premium presentation, durability, and structural integrity, making them widely used for luxury jewelry, cosmetics, and high-end gift packaging. Brands favor them for the enhanced unboxing experience and the ability to incorporate embossing, foil stamping, and fabric wrapping.

In 2025, Louis Vuitton launched its La Beauté luxury beauty line with two-piece monogram-stamped boxes, combining refillable functionality with collectible value to enhance consumer engagement and reinforce brand prestige. This example highlights how leading brands leverage two-piece rigid boxes to blend aesthetic appeal, product protection, and brand storytelling, sustaining global demand.

Collapsible rigid boxes are projected to grow at a CAGR exceeding 6% through 2033, making them the fastest-growing box type. They combine the premium look and structural quality of traditional rigid boxes with foldable designs that reduce shipping and storage costs. Increasingly adopted by luxury brands, these boxes support seasonal product releases, limited editions, and e-commerce fulfillment, where efficiency and presentation are critical.

In 2025, Luxe Pack Monaco highlighted FSC-certified collapsible designs that allowed luxury brands to reduce their carbon footprint while maintaining premium aesthetics, illustrating the adoption of functional sustainability. The versatility, cost-effectiveness, and aesthetic appeal of these boxes make them a strategic choice for brands looking to optimize logistics without compromising the premium unboxing experience.

End-Use Industry Insights

The cosmetics and personal care industry is expected to account for approximately 36% of the rigid box market revenue share in 2026. Premium skincare, fragrances, and beauty products rely heavily on luxury rigid packaging to convey product quality, brand prestige, and exclusivity. Brands frequently release limited-edition collections and seasonal gift boxes, requiring innovative designs and decorative finishes.

In 2025, Hunter Luxury collaborated with Espa for its Limited-Edition Christmas collection, featuring embossed rigid boxes with pull-out trays that elevated unboxing appeal while emphasizing exclusivity. High-end packaging strengthens consumer perception, differentiates products in competitive markets, and supports brand storytelling in both mature and emerging regions.

The premium food and confectionery segment is anticipated to be the fastest-growing end-user, with a CAGR of over 6% through 2033. Growth is driven by gourmet chocolates, luxury desserts, and festive gift packaging, where aesthetics and durability are essential. The rising gifting culture and seasonal promotions are accelerating the adoption of decorative rigid boxes that enhance product appeal.

In 2025, Chaumet introduced bio-based rigid packaging for its luxury confectionery gift sets, showcased at the Paris Packaging Week Premium & Luxury Innovation Awards, combining environmental sustainability with high-end presentation. Luxury brands increasingly prioritize packaging as a marketing tool and a means to enrich consumer engagement, reflecting the intersection of visual presentation, product protection, and premium positioning.

Regional Analysis

North America Luxury Rigid Box Market Trends

North America is forecast to hold approximately 35% of the luxury rigid box market share in 2026, driven by strong consumption across the United States luxury retail and e-commerce sectors. Premium cosmetic, fragrance, fashion, and consumer electronics brands drive consistent demand for high-quality rigid packaging that reinforces brand equity and premium positioning. The region’s affluent consumer base and well-established retail networks support frequent limited-edition and seasonal packaging releases, expanding premium packaging adoption.

Rigid box formats with customized finishes, tactile surfaces, and embedded brand elements are particularly valued for brand storytelling and customer experience.

In 2025, major regional players such as WestRock and DS Smith expanded their luxury packaging capacity to meet accelerating demand from high-end beauty and lifestyle brands, directly supporting market growth and strengthening local supply. These expansions underline North America’s role as a hub for premium rigid packaging and reflect broader investment trends in sustainable, high-performance materials and automated production systems. Regulatory pressure and shifting consumer preferences toward environmentally responsible packaging further reinforce the adoption of recyclable rigid formats.

Combined, these factors ensure North America’s continued leadership as a dominant and strategically influential region in the global luxury rigid box market.

Europe Luxury Rigid Box Market Trends

Europe is a major market for luxury rigid boxes, anchored by key luxury goods manufacturers in France, Italy, Germany, and the United Kingdom. These countries serve as core hubs for premium fashion houses, high-end fragrance producers, and jewelry brands that rely on visually striking and structurally sophisticated packaging to communicate heritage, craftsmanship, and brand exclusivity. European luxury brands emphasize design excellence, often incorporating bespoke textures, specialty inks, and advanced finishing techniques that elevate premium perception at the point of sale and in direct-to-consumer channels.

Strong collaborations between luxury houses and packaging suppliers further enhance the quality, innovation, and customization of rigid box offerings, ensuring that products meet evolving consumer expectations across Europe.

The region’s packaging ecosystem showcased smart packaging innovations such as NFC-enabled rigid boxes at major industry exhibitions, enabling luxury brands to authenticate products and deepen consumer engagement across retail and digital touchpoints. These advancements reflect Europe’s blending of premium aesthetics with technology to enhance value and user experience. Sustainability regulations, including the Circular Economy Action Plan, continue to drive the shift toward eco-friendly materials and recyclable designs, prompting collaborations between luxury houses and packaging partners to develop innovative, environmentally responsible rigid solutions.

European manufacturers also invest in material-efficient processes that balance aesthetics with regulatory compliance, strengthening the region’s competitive position.

Asia Pacific Luxury Rigid Box Market Trends

Asia Pacific is poised to be the fastest-growing regional market for luxury rigid boxes, driven by rapid expansion in luxury consumption across China, Japan, and Southeast Asia, fueled by rising disposable incomes, a growing affluent class, and strong cultural emphasis on premium gifting and personal luxury products. China represents the largest market in the region, supported by its sophisticated manufacturing ecosystem and increasing demand from domestic and international luxury brands.

Japan continues to show strong adoption of premium packaging due to its highly discerning retail culture and focus on presentation, while Southeast Asian markets are experiencing rapid growth in cosmetics, jewelry, and premium confectionery sectors.

Regional growth is further supported by cost-efficient manufacturing capabilities, expanding e-commerce platforms, and increasing brand investments, allowing companies to meet rising domestic consumption and global export demand. Trade events such as the Hong Kong International Printing and Packaging Fair 2025 highlighted innovations in premium rigid packaging and customized rigid box solutions, emphasizing design excellence, functionality, and brand differentiation. These factors collectively position Asia Pacific as a high-potential market for luxury rigid packaging, combining manufacturing efficiency with evolving consumer preferences to accelerate growth in both production and demand.

Competitive Landscape

The global luxury rigid box market structure is moderately consolidated, with leading players such as WestRock, DS Smith, International Paper, Smurfit Kappa, and Rengo controlling a significant portion of the revenue share. These established companies leverage extensive relationships with luxury brands, advanced production capabilities, and integrated design-finishing services. They also invest heavily in R&D, automation, and premium printing technologies, enabling them to deliver high-quality, customizable rigid boxes with sophisticated embossing, foil stamping, and sustainable material options.

Regional and niche competitors, including Sakshi Packagers, Quadpack, and Packaging Corporation of Asia, focus on specialized sectors and local markets, offering bespoke solutions for cosmetics, jewelry, and premium confectionery. Barriers such as high production costs, material sourcing, and design complexity limit new entrants, yet digital printing, e-commerce packaging demand, and on-demand customization are enabling innovative smaller players to participate. Market consolidation is expected to grow gradually as global leaders expand geographically, integrate advanced finishing technologies, and collaborate with smaller design-centric or sustainable packaging firms to strengthen their premium packaging offerings.

Key Industry Developments

- In February 2026, Zeus Packaging Group expanded its luxury packaging capabilities in Europe by acquiring KOEX, a premium packaging specialist in Spain. The acquisition strengthens Zeus’s offerings in cosmetics, fashion, and high-end gift sectors, while adding integrated manufacturing and logistics capabilities in China for end-to-end premium rigid box solutions.

- In December 2025, Paris Packaging Week introduced a new award category to honor sustainable and creative innovations in luxury packaging. This initiative highlights high-end rigid packaging design, encouraging brands to adopt eco-friendly, premium solutions and set new standards in the luxury sector.

- In September 2025, U.S. investment firm KKR completed the US$528 million acquisition of South Korea’s Samhwa Co., a leading cosmetic packaging supplier. Samhwa serves luxury clients including L’Oréal, Chanel, Estée Lauder, and LVMH, strengthening KKR’s position in premium packaging solutions for global luxury beauty brands.

Companies Covered in Luxury Rigid Box Market

- DS Smith plc

- WestRock Company

- Smurfit Kappa Group

- International Paper Company

- PakFactory

- Robinson plc

- Holmen Group

- Burt Rigid Box

- Design Packaging Inc.

- Elite Marking Systems

- Marigold & Grey

- Taylor Box Company

- Bigso Box of Sweden

- Sunrise Packaging

Frequently Asked Questions

The global luxury rigid box market is projected to reach US$ 8.5 billion in 2026.

Rising premiumization, expanding luxury retail, and growing e-commerce demand are driving the market.

The market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Emerging luxury markets and sustainable, customized packaging solutions offer significant growth potential.

Key players in this market include WestRock, DS Smith, International Paper, Smurfit Kappa, and Rengo.