- Automotive

- Europe Luxury Car Market

Europe Luxury Car Market Size, Share, Growth, Trends, Regional Forecasts 2026 - 2033

Europe Luxury Car Market by Vehicle Type (Executive Hatchbacks & Sedans, SUVs & Crossovers, Coupes, Convertibles, Sports & Performance Cars), Powertrain (ICE – Petrol & Diesel, HEV & PHEV, BEV), Price Range (Upto 70k USD, 71k to 150k USD, Above 150k USD), and Country Analysis for 2026 - 2033

Europe Luxury Car Market Share and Trends Analysis

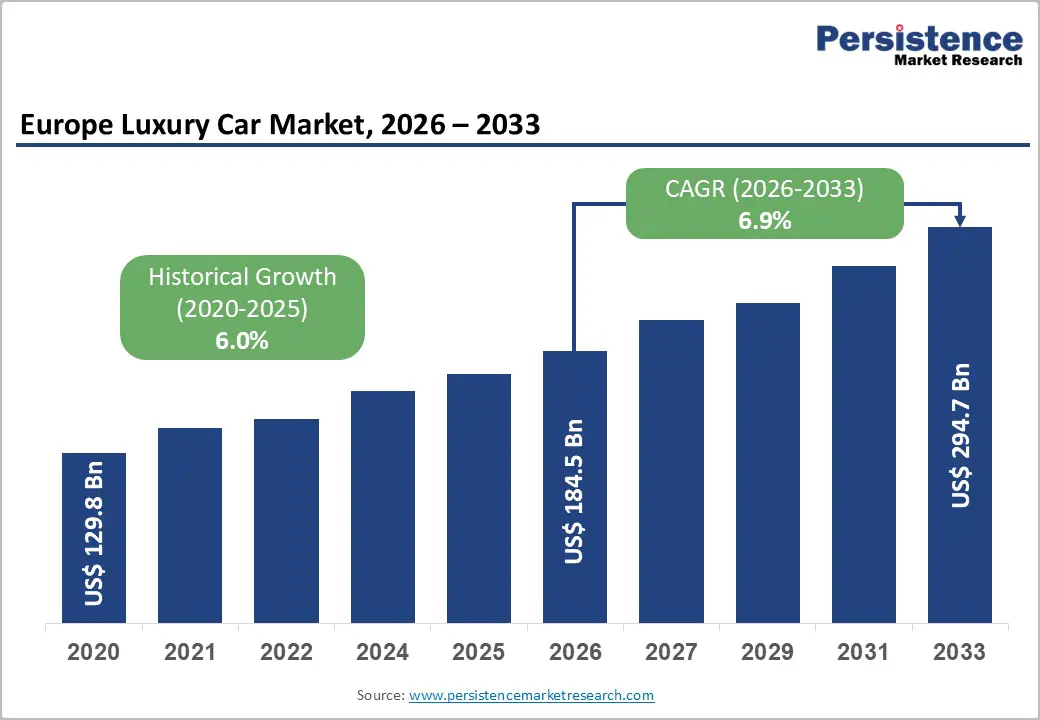

Europe Luxury Car Market size is projected at US$184.5 Bn in 2026 and is projected to reach US$294.7 Bn by 2033, growing at a CAGR of about 6.9% between 2026 and 2033.

Demand is underpinned by rising premium vehicle registrations, with Europe’s wider luxury segment expected to grow around 6–7% annually through the decade. Tightening CO2 norms and Euro 7 preparations accelerate electrified luxury offerings, particularly HEV, PHEV, and BEV models. Higher household wealth, fleet/company-car schemes, and strong OEM financing support replacement and upgrade cycles despite macroeconomic volatility.

Key Highlights Summary

- The Europe luxury car market is projected to grow from US$184.52 Bn in 2026 to about US$294.69 Bn by 2033, reflecting a steady ~6.9% CAGR, supported by rising premium vehicle demand and accelerating electrification trends.

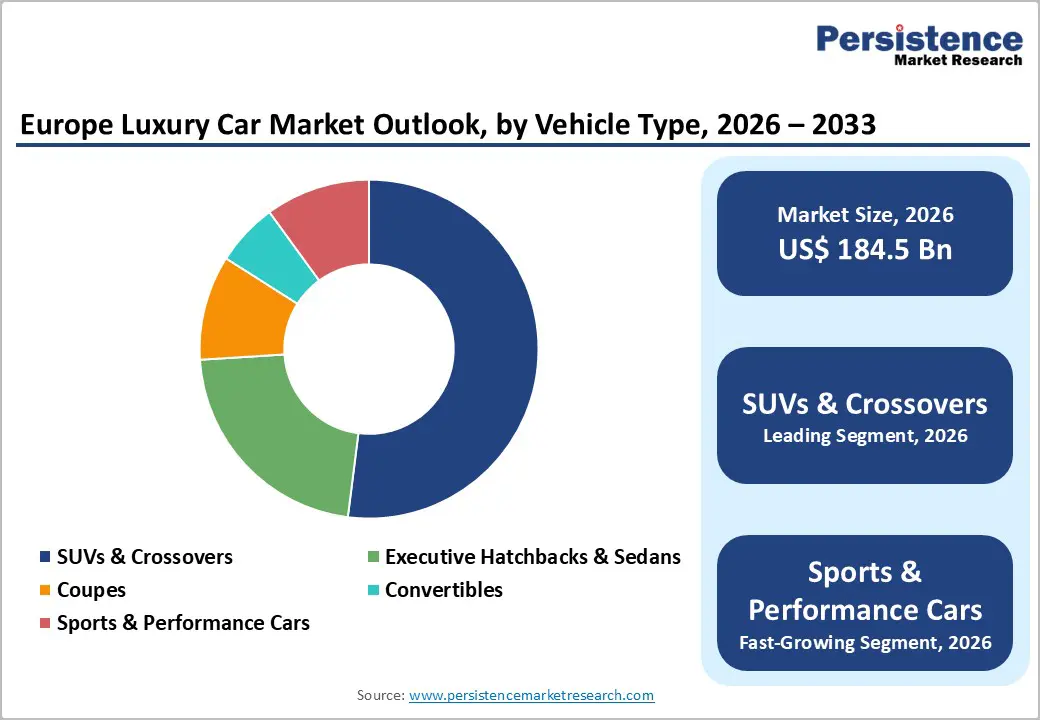

- SUVs and crossovers dominate the market with nearly 52% share, driven by strong consumer preference for spacious, versatile, and high-comfort luxury vehicles.

- Sports and performance cars are the fastest-growing segment, expected to expand at around 8.5% CAGR as demand increases for high-power and track-oriented luxury models.

- ICE vehicles still hold around 68% market share, while battery electric luxury cars are growing rapidly at ~11.5% CAGR due to stricter emission norms and expanding EV infrastructure.

- The US$71k–150k price range leads with about 46% share, whereas the above US$150k segment is growing at nearly 7.7% CAGR, supported by rising ultra-luxury demand.

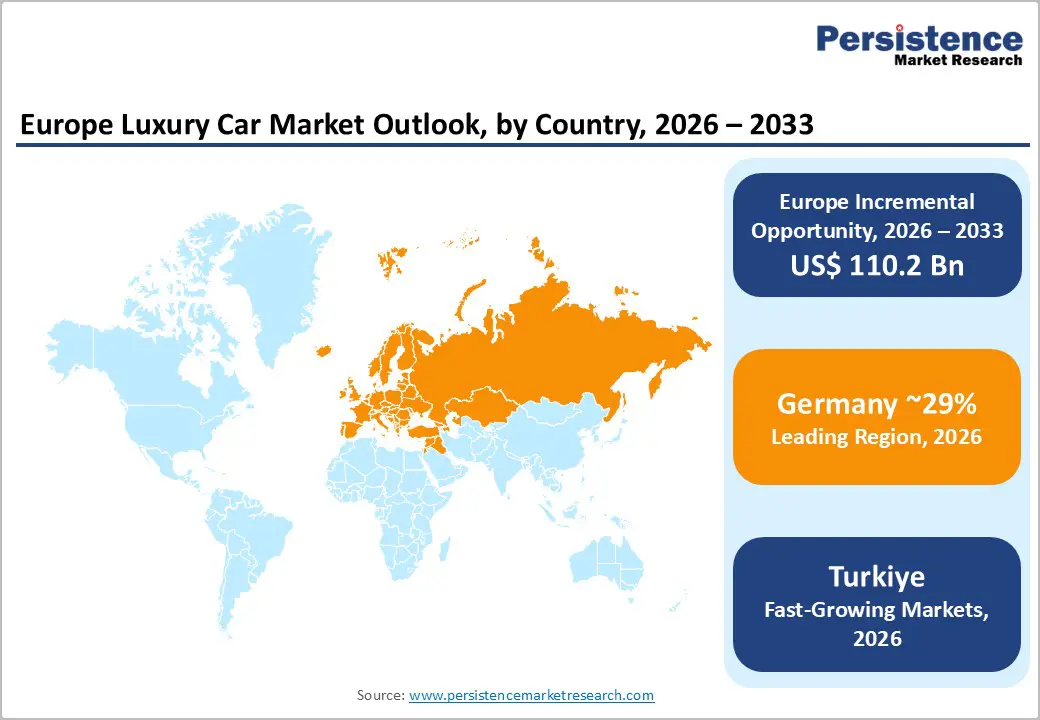

- Germany accounts for nearly 29% of the regional market, followed by the United Kingdom with ~17% share, while Türkiye is emerging as one of the faster-growing luxury car markets in Europe.

- Leading brands including Mercedes-Benz, BMW, Audi, Porsche, and Tesla collectively held around 55% of the Europe luxury car market in 2024, reflecting strong brand presence and innovation in premium mobility.

| Key Insights | Details |

|---|---|

|

Europe Luxury Car Market Size (2026E) |

US$ 184.5 billion |

|

Market Value Forecast (2033F) |

US$ 294.7 billion |

|

Projected Growth CAGR (2026-2033) |

6.9% |

|

Historical Market Growth (2020-2025) |

6.0% |

Market Dynamics Analysis

Drivers - Macroeconomic resilience and an affluent customer base

Europe hosts one of the largest high-net-worth and upper-middle-income populations globally, supporting resilient luxury auto demand even during modest GDP slowdowns. The European luxury car market is projected to approach US$287–295 Bn by early next decade, reflecting a sustained appetite for premium mobility solutions. Premium financing, company-car tax schemes, and leasing penetration increase affordability for executives and professionals. As a result, OEMs sustain high margins on SUVs & Crossovers, high-spec sedans, and performance lines, reinforcing continuous model refreshes and technology upgrades.

Technological innovation, connectivity, and ADAS

European luxury brands lead in integrating advanced driver-assistance systems (ADAS), over-the-air software updates, and immersive infotainment into premium vehicles. Features such as Level 2/2+ assisted driving, high-resolution displays, and connected services differentiate luxury offerings from mass-market segments. Increasing digital content per vehicle, combined with subscription-based services, creates recurring revenue streams beyond initial car sales. These innovations strengthen the value proposition of sports & performance cars and high-end SUVs, supporting higher option take-rates and enhancing customer retention.

Restraints - High acquisition and ownership costs

Luxury vehicles entail substantial upfront prices, insurance, and maintenance costs, limiting accessible demand during interest-rate spikes or economic downturns. Rising input costs—batteries, semiconductors, and advanced materials—add pressure on MSRP levels. While OEMs partly offset this through financing and leasing, elevated total cost of ownership can delay replacement cycles and constrain volume growth among aspirational buyers, especially in Southern and Eastern Europe.

Charging infrastructure gaps and BEV demand volatility

Despite rapid BEV rollout, charging networks remain uneven across Europe, with infrastructure concentration in Western and Northern countries. Recent ACEA data indicates that BEV registrations softened in some major markets in 2024 amid subsidy changes and infrastructure concerns. For luxury buyers contemplating high-value BEVs, range, charging convenience, and residual values remain key risks, slowing the pace at which BEVs can replace ICE (Petrol & Diesel) as the dominant powertrain.

Opportunities - Scaling BEV and electrified luxury portfolios

With BEV luxury lines expected to grow at around 11.5% CAGR, OEMs can capture substantial incremental revenue by introducing dedicated electric platforms and halo models. As charging infrastructure improves and battery costs decline, BEV penetration in the luxury segment could account for a significant share of new registrations by 2033. Targeting tech-savvy, sustainability-oriented customers with performance-focused BEVs and exclusive charging or software services can unlock multi-billion-dollar revenue pools.

Digital retail, subscription, and new ownership models

Online configuration, agency sales models, and direct-to-consumer pilots in select European markets open avenues for margin optimization and richer data capture. Combining digital sales journeys with flexible subscription and short-term leasing formats can attract younger affluent customers and corporate fleets. As digital channels expand, cross-selling of services (connectivity, software features, maintenance packages) could add measurable recurring revenues and smooth cyclical swings in new-car demand.

Category-wise Analysis

Vehicle Type Insights

SUVs & Crossovers constitute the leading vehicle type, with an estimated 52% share of the Europe luxury car market in 2026. Consumer preference for higher seating position, versatility, and perceived safety, combined with OEM focus on high-margin SUV platforms, sustains this dominance. Germany, the U.K., and other Western European markets report that sports utility formats generate the largest share of luxury registrations and revenue, reflecting strong adoption in both private and company-car channels.

The fastest-growing segment is Sports & Performance Cars, expected to post around 8.5% CAGR during 2026–2033 as demand for high-output ICE, hybrid, and BEV performance models expands. Track-capable yet road-legal coupes, GTs, and performance sedans attract enthusiasts and affluent buyers seeking differentiated driving experiences, particularly in Germany and the U.K.

Powertrain Insights

ICE (Petrol & Diesel) remains the leading powertrain, accounting for about 68% share of Europe luxury car revenues in 2026, supported by extensive refuelling infrastructure, mature technology, and established consumer familiarity. High-output petrol engines and refined diesel units still dominate in executive sedans and large SUVs, especially for long-distance and fleet users. While their share will gradually decline, ICE vehicles will continue to anchor profitability and residual values over the medium term.

BEVs represent the fastest-growing powertrain, forecast to expand at roughly 11.5% CAGR between 2026 and 2033 as OEMs roll out dedicated electric luxury platforms. Growth is driven by tightening emissions rules, corporate sustainability policies, and the appeal of instant torque and quiet operation in luxury applications.

Price Range Insights

The 71k to 150k USD band leads the Europe luxury car market with around 46% share, reflecting the core pricing sweet spot for high-spec executive sedans and premium SUVs. This range captures a broad swath of affluent private buyers and corporate fleets, where financing structures, leasing, and attractive residual values make ownership economically viable. As OEMs pack more technology and electrification into mid-to-upper trims, this band remains central to volume and revenue generation.

The Above 150k USD segment is the fastest-growing price tier, projected to log about 7.7% CAGR as ultra-luxury limousines, super-SUVs, and performance sports cars gain traction. Limited-run models, bespoke specifications, and high-performance variants from leading brands target a niche but rapidly expanding ultra-wealthy clientele across Europe.

Country Insights

Germany Luxury Car Market Trends

Germany holds a dominating ~29% share of the Europe luxury car market, backed by its position as a leading manufacturing hub and home base for global premium brands. The German luxury segment generated over US$55 Bn in 2024 and is projected to approach US$77 Bn by 2030, at about 5.8% CAGR. Strong export orientation, high domestic incomes, and a robust company-car culture underpin demand for executive sedans and SUVs. A dense innovation ecosystem, including R&D centers and test facilities in Bavaria and Baden-Württemberg, accelerates deployment of advanced powertrains and ADAS technologies.

From 2026 to 2033, Germany is expected to expand broadly in line with regional averages, driven by electrified SUVs and performance vehicles. Regulatory pressure on CO2 emissions and city-level low-emission zones will gradually tilt new registrations toward HEV, PHEV, and BEV, while ICE continues to play a significant role in export-oriented production.

U.K. Luxury Car Market Trends

The U.K. accounts for around 17% of Europe luxury car demand and is projected to grow at roughly 7% CAGR, supported by a strong high-income consumer base and deep financing penetration. The country features robust demand for premium SUVs, executive saloons, and performance models, underpinned by brand loyalty and a vibrant used-luxury market. U.K. industrial capabilities include heritage performance and ultra-luxury marques, while regulatory frameworks closely track EU emissions and safety standards, even after Brexit, supporting harmonized product offerings.

Over 2026–2033, the U.K. is poised to remain one of Europe’s fastest-growing luxury markets as electrification accelerates, especially in metropolitan areas with strong charging networks. Investment in BEV and hybrid portfolios, along with attractive benefit-in-kind tax treatment for low-emission company cars, will reinforce premium and upper-premium segment growth.

Türkiye Luxury Car Market Trends

Türkiye, while smaller in absolute size, is growing at a prominent ~7.8% CAGR, benefitting from rising household incomes, an expanding upper-middle class, and its strategic manufacturing position between Europe and Asia. Local assembly and supplier bases support competitive production of components and select vehicle lines, while affluent consumers increasingly opt for premium German and European brands. Ongoing investments in automotive clusters and free-trade arrangements facilitate imports and exports of luxury vehicles into the wider region.

From 2026 to 2033, Türkiye is expected to outpace the regional average in volume growth, albeit from a lower share base. As macroeconomic stability improves and financing options widen, luxury car penetration will climb, especially in large metropolitan centers. Regulatory convergence with EU standards will further encourage OEMs to position higher-spec models in the market.

Competitive Landscape

Leading luxury OEMs in Europe pursue technology-focused differentiation, combining electrification, ADAS, and connected services with strong brand heritage. They optimize costs via modular platforms and flexible production while capturing value through higher-margin SUVs and ultra-luxury trims. Emerging business models include agency sales, digital-first journeys, subscription and shorter leases, as well as software-driven features and services that extend monetization beyond initial vehicle delivery.

Key Developments

- In May 2024, Mercedes-Benz launched new all-electric EQS and EQE SUV variants in Europe, enhancing its BEV luxury portfolio and targeting higher BEV mix in premium SUV sales.

- In June 2024, BMW Group expanded its Neue Klasse investment program for European production sites, focusing on next-generation electric luxury sedans and SUVs to be launched from 2025 onwards.

- In October 2024, Audi introduced updated plug-in hybrid versions of its Q7 and Q8 luxury lines for Europe, aimed at meeting fleet CO2 targets while preserving long-range usability.

Companies Covered in Europe Luxury Car Market

- Mercedes-Benz Group AG

- BMW Group

- Volkswagen Group

- Stellantis N.V.

- Jaguar Land Rover Automotive

- Ferrari N.V.

- Aston Martin Lagonda Global Holdings

- Volvo Car Corporation

- Polestar

- Tesla, Inc.

- Lexus

- Genesis Motor Europe

- Bentley Motors

- Lamborghini

- Rolls-Royce Motor Cars

Frequently Asked Questions

The Europe Luxury Car Market is projected at about US$184.5 Bn in 2026, advancing toward nearly US$295 Bn by 2033.

Growth is driven by affluent household expansion, strong demand for SUVs and executive cars, and regulatory‑driven electrification and technology upgrades in premium segments.

Major opportunities lie in BEV and hybrid luxury portfolios, ultra‑luxury models above US$150k, and digital‑first sales, subscription, and service‑based revenue models.

Key players include Mercedes‑Benz, BMW Group, Audi, Porsche, Jaguar Land Rover, Ferrari, Aston Martin, Volvo, Polestar, Tesla, Lexus, and Genesis.