- Hardware & Software IT Services

- Logistics Order Management Solutions Market

Logistics Order Management Solutions Market Size, Share, and Growth Forecast 2026 – 2033

Logistics Order Management Solutions Market by Deployment Mode (Cloud-based, On-premise), Component (Software, Managed Services), Organization (Size Large Enterprises, SMEs), Application Type, and Regional Analysis 2026 – 2033

Logistics Order Management Solutions Market Size and Trend Analysis

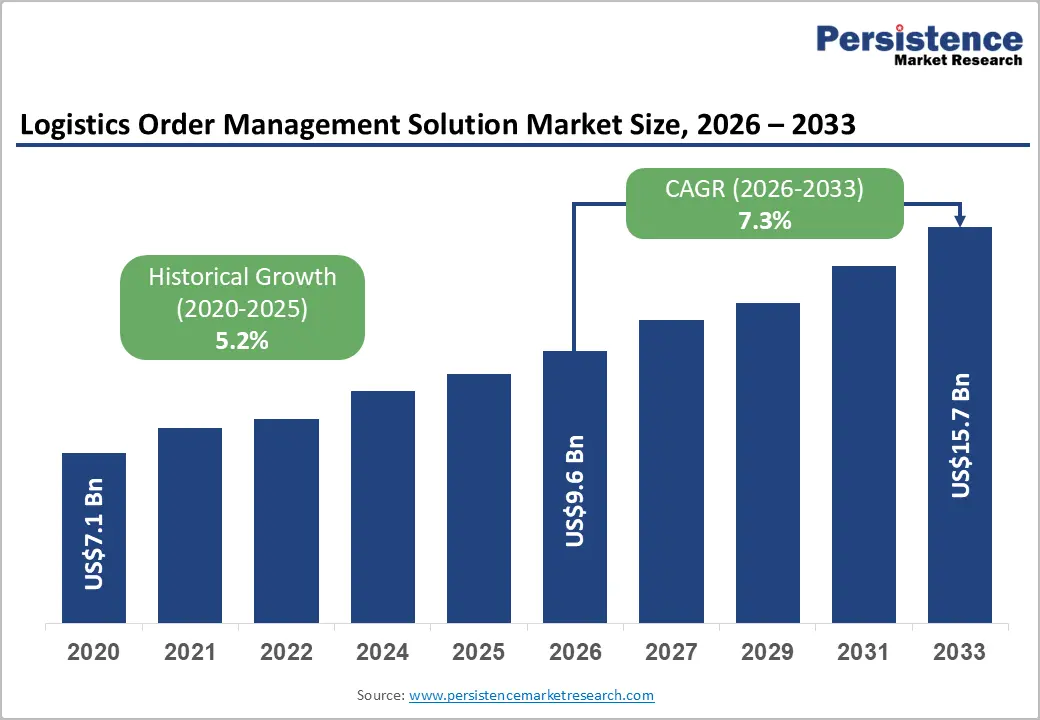

The global logistics order management solutions market size was likely to be valued at US$9.6 billion in 2026, and is expected to reach US$15.7 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by the integration of Artificial Intelligence (AI) and Machine Learning (ML) into order fulfillment processes, enabling predictive analytics and real-time inventory visibility.

As organizations transition from legacy systems to cloud-native microservices architectures, the demand for scalable, agile order management solutions (OMS) is projected to surge, particularly within the retail and manufacturing sectors.

Key Industry Highlights:

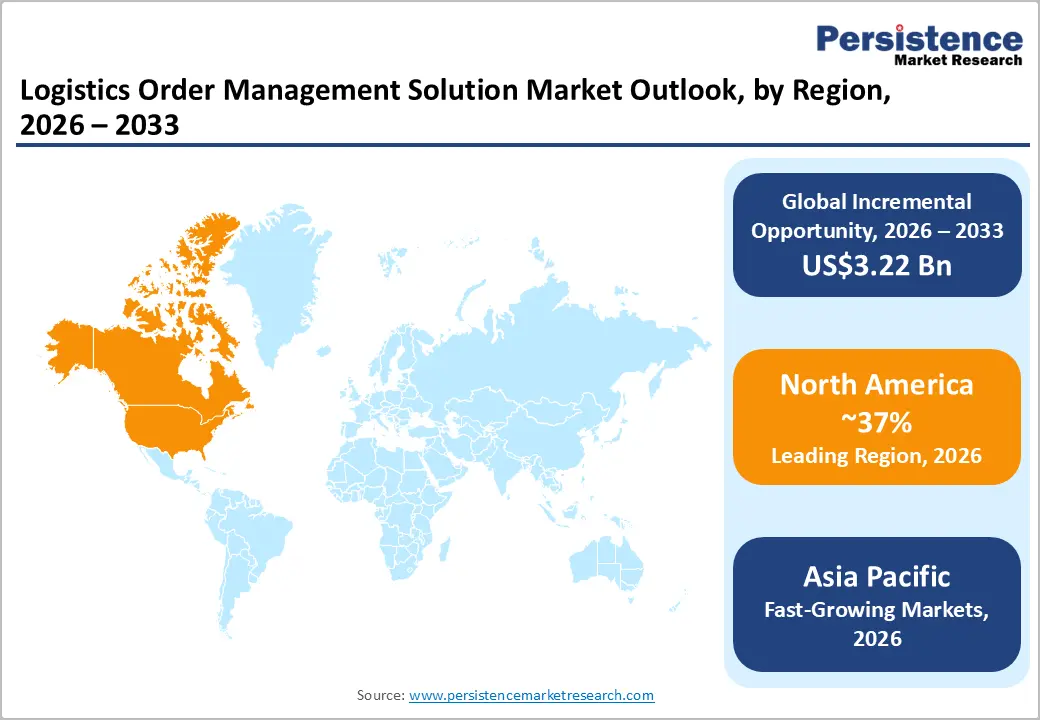

- Leading Region: North America is expected to lead the logistics order management solutions market with a 37% share in 2026, driven by a mature digital commerce ecosystem, extensive omnichannel retail, strong third-party logistics, and investment in AI-powered fulfillment and last-mile optimization.

- Fastest-growing Region: Asia Pacific is set to be the fastest-growing market, fueled by rapid e-commerce growth, expanding social commerce, and the increasing digitalization of logistics across China, India, and Southeast Asia.

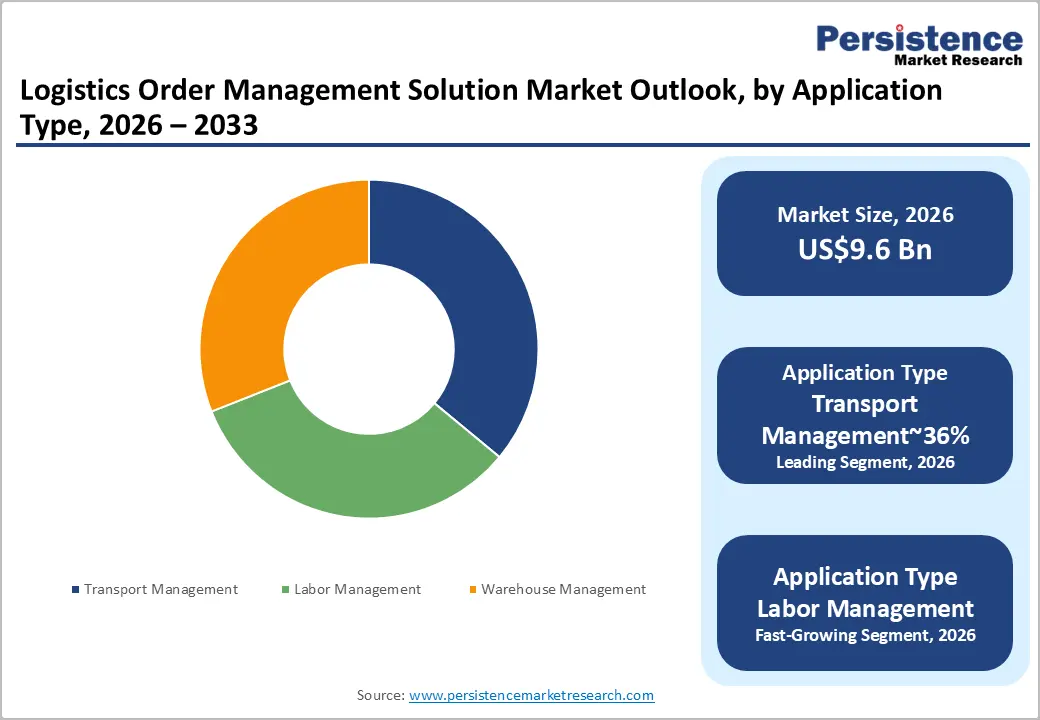

- Leading Component: Software is expected to dominate the market with approximately 62% share in 2026, as OMS platforms increasingly function as the central orchestration layer for order routing, inventory visibility, exception management, and omnichannel execution.

- Leading Application: Warehouse management system–linked OMS is expected to lead with approximately 38% share, reflecting its role in controlling physical fulfillment execution, automation-heavy warehouses, and high-throughput e-commerce operations.

- Industry Developments: In January 2026, Oracle launched its “Self-Healing Supply Chain” module to autonomously reroute global shipments during climate-induced port closures. This development drastically reduces "Cost-to-Serve" by eliminating manual intervention during disruptions and ensures 99.9% fulfillment reliability for omnichannel retailers.

| Key Insights | Details |

|---|---|

|

Logistics Order Management Solutions Market Size (2026E) |

US$9.6 Bn |

|

Market Value Forecast (2033F) |

US$15.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Omnichannel Commerce as the Growth Engine for Logistics Order Management Solutions

The Logistics Order Management Solutions (OMS) market is being propelled by the rapid expansion of omnichannel commerce, which is transforming traditional retail into a fully integrated, multi-touchpoint ecosystem. Consumers now expect a seamless experience across online, mobile, and in-store channels, forcing retailers to adopt OMS platforms as central operational hubs rather than mere back-office tools. This convergence ensures that orders can flow effortlessly between sales channels, allowing retailers to fulfill consumer demands for flexible purchase and delivery options while maintaining inventory accuracy and operational efficiency.

Advanced OMS platforms now enable intelligent order routing, real-time inventory visibility, and dynamic fulfillment strategies, reducing the risk of overselling and enhancing customer satisfaction.

The rise of complex fulfillment models further amplifies OMS adoption. Solutions that support buy-online-pickup-in-store (BOPIS), curbside collection, ship-from-store, and online returns-to-store (BORIS) are increasingly essential for retailers seeking to optimize speed, reduce last-mile costs, and convert returns into additional sales opportunities. Retailers leveraging these capabilities can pool inventory across locations, automatically assign the most efficient fulfillment node, and monitor order progress in real time.

As consumer expectations for convenience intensify, OMS platforms have become a strategic necessity, enabling retailers to orchestrate distributed fulfillment networks and capture revenue from evolving e-commerce and mobile-first purchasing behaviors.

Data Security Risks and Legacy System Barriers in Logistics OMS Adoption

The logistics sector faces significant adoption challenges for modern Order Management Solutions due to the dual pressures of data security concerns and legacy system constraints. Migrating sensitive customer, supplier, and inventory data from on-premise or outdated ERP and warehouse platforms to cloud-based OMS creates exposure to cyberattacks, operational downtime, and compliance risks. High-profile ransomware incidents have demonstrated the severity of these vulnerabilities: global logistics companies have been forced to halt operations for weeks, incurring operational losses, reputational damage, and legal consequences.

For example, targeted ransomware attacks have caused complete system shutdowns and operational collapse for some long-established firms, highlighting the sector’s low tolerance for disruptions.

Many firms still operate ERP or warehouse management systems that lack modern APIs or secure communication protocols. Attempting to patch these systems for OMS integration can create unintended security gaps, expanding the attack surface and making firms vulnerable to supply chain intrusions. This complexity also increases migration costs, discouraging mid-sized and conservative operators from upgrading. Combined, cybersecurity threats and legacy incompatibilities act as structural barriers, slowing OMS adoption and limiting the potential for logistics companies to fully exploit real-time visibility, automation, and distributed fulfillment efficiencies.

AI and Generative AI-Driven Transformation in Logistics OMS

The convergence of Artificial Intelligence (AI) and Generative AI (GenAI) presents a transformative opportunity for the Logistics Order Management Solutions (OMS) market. By embedding GenAI capabilities, OMS platforms can evolve into “conversational” supply chains, allowing users to query order status, explore alternatives, or simulate complex scenarios using natural language. This innovation lowers the barrier to sophisticated analytics, empowering non-technical staff to optimize inventory allocation, order routing, and fulfillment decisions.

GenAI also supports predictive decision-making, automatically adjusting to disruptions such as port delays, weather events, or supplier constraints. The adoption of AI-enhanced OMS enables organizations to improve operational efficiency, reduce customer service overhead, and enhance sustainability through real-time carbon-aware routing decisions.

Autonomous natural language procurement platforms, such as Pactum AI, conduct large-scale supplier negotiations for optimal pricing. Predictive disruption management by companies such as Project44 dynamically reroutes shipments around bottlenecks. Hyper-personalized customer portals leverage conversational AI to handle service requests seamlessly. Demand forecasting now integrates unstructured data sources, while automated warehouse logic synthesis and code-free LLM-driven API integration streamline OMS deployment. Innovations also extend to green order routing, automated returns management, compliance automation, and digital twin simulations, enabling pre-emptive risk planning.

Together, these applications demonstrate that AI and GenAI integration can unlock significant operational, financial, and environmental value across the global logistics ecosystem. In October 2025, C.H. Robinson unveiled the Agentic Supply Chain powered by Lean AI. This ecosystem of AI agents enables real-time optimization, proactive disruption handling, and faster shipment planning, freeing resources for strategic focus.

Category–wise Analysis

Component Insights

The software component is expected to retain the dominant revenue position in the logistics OMS market, accounting for close to 62% share in 2026, as it remains the core layer enabling order orchestration, inventory visibility, and omnichannel execution. Enterprise platforms from SAP, Oracle, Blue Yonder, and Manhattan Associates are widely adopted for their advanced modules such as AI-driven order promising, real-time inventory pooling, and API-led integration with WMS, TMS, and last-mile partners.

Software value is increasingly concentrated in intelligence rather than transaction handling, with features like digital twins, predictive order routing, and exception management becoming standard requirements for large retailers and logistics providers. This structural reliance on OMS software as the system of record is likely to sustain its leadership, particularly in high-volume, multi-node fulfillment environments.

Managed services are anticipated to be the fastest-growing component, driven by rising operational complexity and a widening gap between OMS sophistication and in-house IT capabilities. Logistics operators are increasingly outsourcing platform monitoring, optimization, cybersecurity, and integration management to specialist providers such as IBM, Accenture, and dedicated logistics MSPs. This shift is expected to accelerate as OMS deployments incorporate AI models, IoT data streams, and real-time decision engines that require continuous tuning and uptime assurance.

Managed services are also likely to gain traction as compliance requirements, resilience expectations, and always-on fulfillment models push companies toward guaranteed service levels and outcome-based contracts. As a result, managed services are emerging as a critical execution layer that complements core software, rather than a discretionary add-on.

Application Insights

Warehouse management systems are expected to remain the leading application within the Logistics OMS market, accounting for an estimated 38% share in 2026, as they anchor the physical execution of order fulfillment. WMS-linked OMS platforms are likely to dominate because they directly control picking, packing, slotting, and dispatch across high-throughput facilities. Large e-commerce and retail operators such as Amazon, Walmart, and JD Logistics increasingly rely on WMS modules from Manhattan Associates, Blue Yonder, and Körber to orchestrate automation-heavy environments. Solutions integrating AutoStore and shuttle-based robotics are anticipated to strengthen this position, as they enable dense storage and faster order cycles in large fulfillment centers.

The rapid expansion of urban micro-fulfillment hubs and dark stores further reinforces WMS relevance, with vision-picking and goods-to-person workflows improving accuracy and labor productivity. As same-day and sub-hour delivery expectations rise, WMS is likely to remain the core execution layer, translating OMS decisions into physical outcomes.

Transportation management systems are anticipated to be the fastest-growing application, driven by cost pressure, sustainability mandates, and network volatility. TMS adoption is likely to accelerate as fuel price fluctuations and capacity constraints force shippers to optimize routing and carrier selection dynamically. Platforms from SAP, Oracle, Descartes, and MercuryGate increasingly embed AI-driven load optimization, real-time visibility, and carbon-aware routing to support cost-to-serve reduction.

Retailers and manufacturers are expected to use TMS to balance road, rail, and intermodal options while tracking emissions across outbound legs. Integration with real-time traffic, weather intelligence, and autonomous freight pilots further positions TMS as a strategic control layer. As transport shifts from a fixed expense to a variable risk factor, TMS is likely to gain priority within OMS-driven decision frameworks.

Regional Insights

North America Logistics Order Management Solutions Market

North America is expected to lead, accounting for approximately 37% of the total market share in 2026, reinforced by a highly mature digital economy, strong domestic consumption, and persistent pressure to optimize last-mile delivery performance. Intense competition among large retailers and marketplaces is likely to keep OMS adoption at the center of supply chain strategy, particularly as same-day and next-day delivery become baseline expectations rather than differentiators.

Labor constraints across trucking, warehousing, and fulfillment operations will continue to push enterprises toward automation-ready OMS platforms that support AI-driven decision making and managed service models. Ongoing investments in ports, highways, and intermodal infrastructure are expected to further increase demand for OMS solutions capable of coordinating complex, real-time transportation flows.

Enterprises are anticipated to accelerate the adoption of orchestration-layer OMS platforms that unify order capture, routing, inventory visibility, and exception management across channels. Generative AI will increasingly automate order workflows, compliance documentation, and carrier selection logic. Regulatory requirements around food traceability, cross-border trade under USMCA, and heightened cybersecurity disclosure will favor cloud-native, interoperable OMS platforms with enterprise-grade security.

As large retailers mandate standardized API integration from logistics partners, North America is likely to deepen its position as the most standardized, interconnected, and commercially advanced OMS market globally.

Asia Pacific Logistics Order Management Solutions Market

Asia Pacific is expected to remain the fastest-growing market, benefiting from rapid e-commerce penetration, rising social commerce adoption, and increasing digitalization of logistics operations across China, India, and Southeast Asia. Growth is likely to be supported by mobile-first consumer behavior, expanding D2C ecosystems, and the accelerated adoption of cloud-based order management and logistics platforms. Unlike mature Western markets, Asia Pacific enterprises are expected to scale without heavy legacy constraints, enabling faster deployment of AI-driven fulfillment, inventory orchestration, and last-mile optimization tools.

Supply chain diversification strategies such as China Plus One are likely to increase cross-border trade complexity, strengthening demand for OMS solutions capable of handling multi-country compliance and fragmented logistics networks. Government-led digital infrastructure initiatives and regional trade frameworks are anticipated to streamline data exchange and customs processes, further supporting market expansion. Despite regulatory fragmentation across countries, Asia Pacific is expected to remain the fastest-growing logistics technology market, driven by structural consumption growth, digital-native businesses, and ongoing investment in scalable fulfillment infrastructure.

Europe Logistics Order Management Solutions Market

Europe is expected to retain a mature yet strategically important position, benefiting from deeply entrenched logistics infrastructure and high digital readiness across Germany, the U.K., and France. E-commerce intensity and complex cross-border trade flows are likely to sustain demand for advanced OMS platforms capable of managing last-mile delivery, reverse logistics, and multi-carrier orchestration. Ongoing nearshoring from Asia into Eastern and Southern Europe is anticipated to increase intra-regional freight movements, raising operational complexity and reinforcing the need for OMS solutions tightly integrated with transportation and warehouse systems. Europe’s dense road, rail, and port networks will further support the adoption of multimodal, asset-optimizing order management platforms.

Regulation will remain the defining force shaping market evolution. The Digital Product Passport is expected to accelerate demand for OMS with deep traceability and lifecycle data integration, while CBAM requirements will push carbon-aware order routing and emissions reporting into core OMS functionality. Cyber resilience mandates under DORA and NIS2 are likely to favor enterprise-grade, cloud-native platforms with strong uptime guarantees and security governance. Adoption is expected to concentrate around large retailers, third-party logistics providers, and industrial exporters, with SAP, Oracle, Siemens Digital Logistics, and Generix Group positioned to benefit as customers prioritize compliance, interoperability, and long-term operational resilience over rapid expansion.

Competitive Landscape

The global logistics order management solutions market is moderately fragmented but steadily trending toward consolidation, led by a cluster of Tier-1 enterprise vendors including SAP, Oracle, and Blue Yonder that collectively control roughly 40–50% of global market share. These players benefit from deep ERP penetration, long-standing enterprise relationships, and the ability to bundle OMS within broader supply chain and planning suites. The remaining market is distributed among best-of-breed specialists such as Manhattan Associates and Descartes, alongside a growing set of cloud-native SaaS providers targeting specific use cases or mid-market customers. Competitive intensity is shifting away from isolated functional differentiation toward platform-level competition, where vendors position OMS as an orchestration layer connecting planning, execution, warehouse, and transportation systems into a unified ecosystem.

Key Industry Developments:

- In January 2026, Blue Yonder launched AI-driven innovations for unified planning and execution, with enhanced Order Management. Native AI agents provide real-time inventory visibility, automated issue resolution, and proactive fulfillment recommendations, improving agility and customer experiences.

- In July 2025, Oracle introduced advanced inventory management capabilities in Cloud SCM. These streamline warehouse operations, simplify transactions, and accelerate processes, supporting efficient order fulfillment in dynamic supply chains.

- In May 2025, Manhattan Associates released Enterprise Promise & Fulfill to improve ERP-integrated order management. The cloud-based tool delivers real-time visibility, automated routing, and exception handling, enabling faster, more transparent B2B fulfillment without full system overhauls.

Companies Covered in Logistics Order Management Solutions Market

- SAP SE

- Oracle Corporation

- Manhattan Associates

- Blue Yonder

- IBM Corporation

- The Descartes Systems Group

- Infor

- Kinaxis Inc.

- Körber AG

- Microsoft Dynamics 365

- Zoho Corporation

- Epicor Software Corp.

- Basware

- Softeon

Frequently Asked Questions

The global logistics order management solutions market is projected to be valued at US$9.6 billion in 2026 and is expected to reach US$15.7 billion by 2033, driven by the integration of AI and the shift to cloud-native, omnichannel fulfillment.

The rapid expansion of omnichannel commerce is a primary growth engine, as it requires OMS platforms to act as a central hub for seamless order orchestration, real-time inventory visibility across all channels, and the execution of complex fulfillment models such as BOPIS and ship-from-store to meet modern consumer expectations.

The logistics order management solutions market is forecast to grow at a CAGR of 7.3% from 2026 to 2033, reflecting sustained demand for intelligent, scalable fulfillment orchestration.

North America is expected to be the leading region, accounting for approximately 37% share in 2026, supported by a mature digital commerce ecosystem, large-scale omnichannel retail operations, and significant investment in AI-enabled fulfillment and last-mile optimization.

The logistics order management solutions market is dominated by SAP SE, Oracle Corporation, Manhattan Associates, and Blue Yonder, with the top vendors holding 40–50% of global market share, focusing on AI-driven platforms that integrate planning, execution, and transportation systems.