- Technology

- Smart Logistics Market

Smart Logistics Market Size, Share, Trends, Growth, Forecasts, 2026 - 2033

Smart Logistics Market by Component (Hardware, Software, Services), Industry (Infrastructure, Services, Distribution Services, Public Sector, Finance), and Regional Analysis 2026 - 2033

Smart Logistics Market Share and Trends Analysis

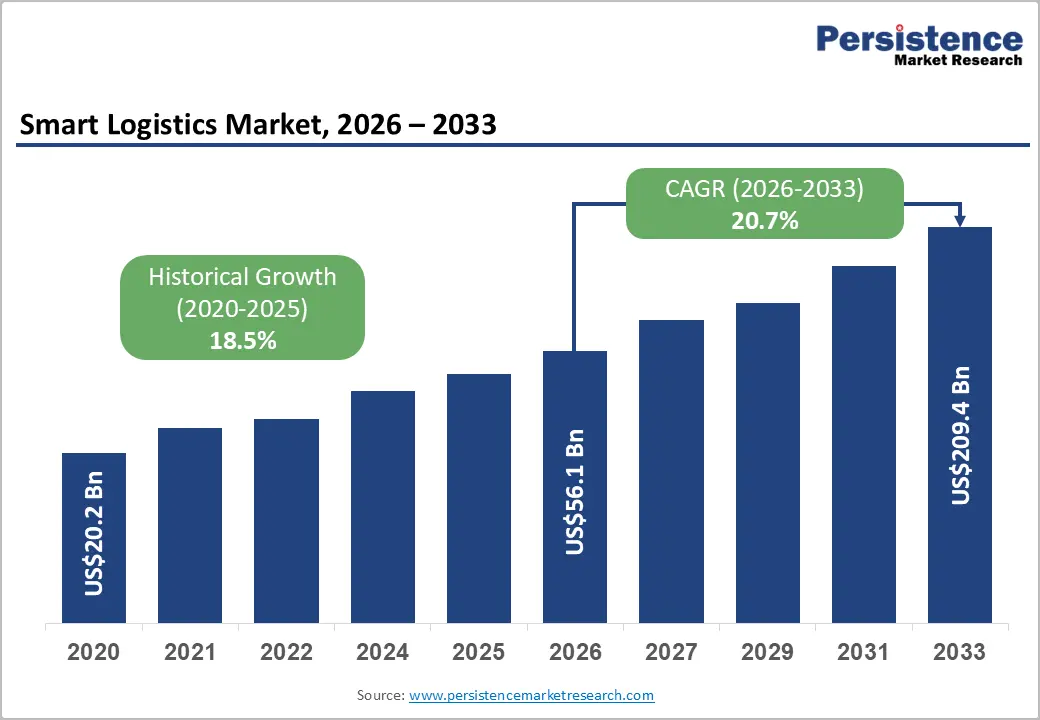

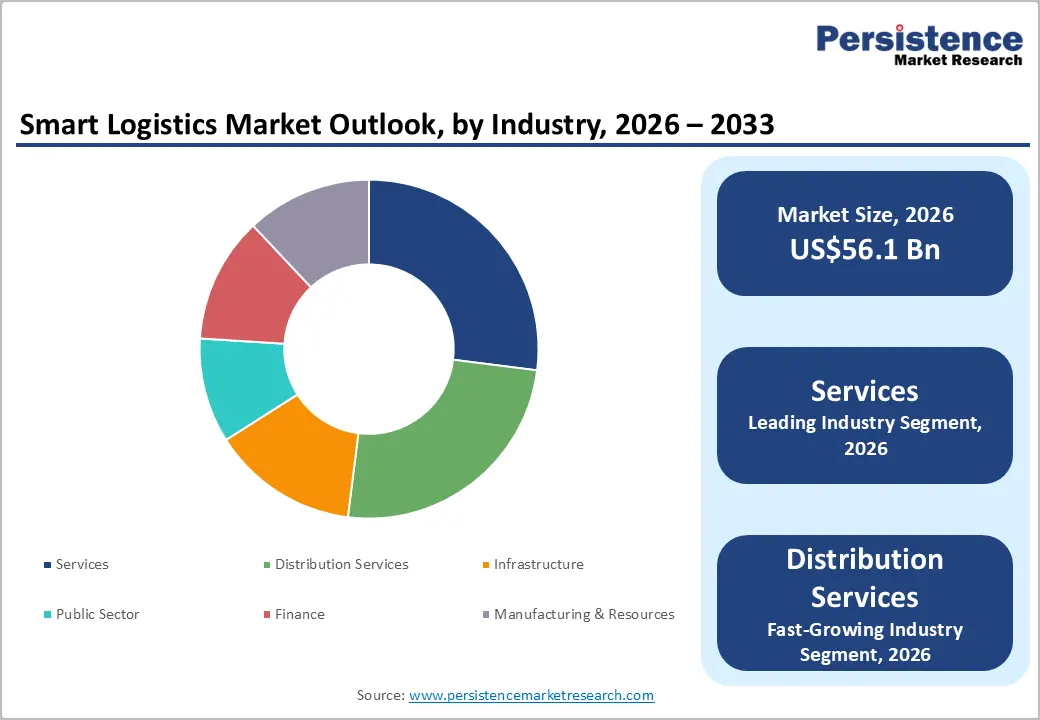

The global smart logistics market size is likely to be valued at US$ 56.1 billion in 2026 and is projected to reach US$ 209.4 billion by 2033, growing at a CAGR of 20.7% between 2026 and 2033. Market expansion is driven by e-commerce acceleration requiring same-day delivery capabilities and advanced supply chain visibility, accelerating artificial intelligence and machine learning deployment reducing logistics costs by 15% while improving inventory levels by 35% and service levels by 65%, and systematic workforce constraints requiring warehouse automation and robotics integration.

Key Industry Highlights:

- Software commands 38% market share as dominant component, while Services (Professional/Managed) represent a considerable growing segment at 20.8% CAGR driven by implementation complexity and recurring revenue models.

- Services sector leads with 27% industry share, while Distribution Services expand as prominent growing segment at 20.9% CAGR supporting e-commerce fulfillment and warehouse automation.

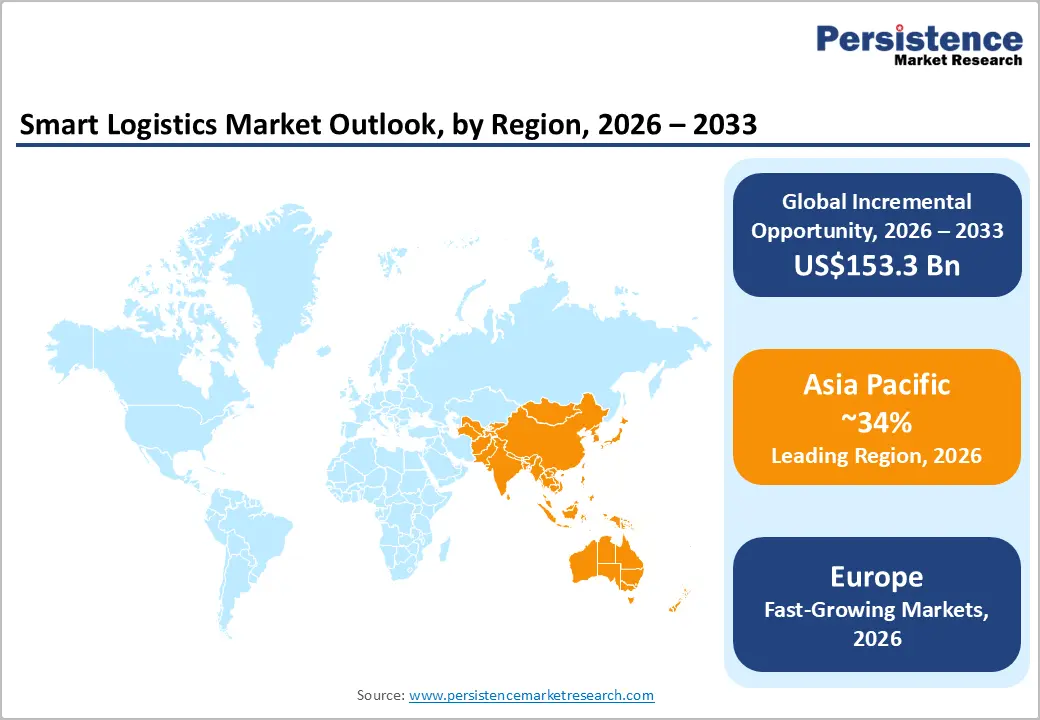

- North America accelerates at 20.3% CAGR with Amazon 520,000+ robots and advanced technology deployment, while Asia Pacific commands 34% market share with India warehouse automation growing prominently.

- Europe maintains 24% market share at 19.2% CAGR growth anchored by GDPR compliance, sustainability focus, and advanced manufacturing logistics.

- Flexport acquired Convoy Platform (2023), DAT acquired Convoy from Flexport (July 2025 for ~USD 250M), DHL deployed DHLBots AI sorting robots, and FedEx expanded Surround platform demonstrating ecosystem transformation and technology consolidation momentum.

| Key Insights | Details |

|---|---|

|

Smart Logistics Market Size (2026E) |

US$ 56.1 billion |

|

Market Value Forecast (2033F) |

US$ 209.4 billion |

|

Projected Growth CAGR (2026-2033) |

18.5% |

|

Historical Market Growth (2020-2025) |

20.7% |

Market Dynamics Analysis

Drivers - E-Commerce Proliferation and Last-Mile Delivery Complexity Supporting Supply Chain Technology Adoption

Rapid e-commerce expansion and rising consumer expectations for same-day and next-day delivery are systematically accelerating smart logistics adoption across global supply chains. Last-mile optimization and orchestration have become critical competitive differentiators, driving sustained technology investment throughout distribution centers and warehousing networks. Online retail sales continue expanding at high double-digit rates in key markets, intensifying pressure on fulfillment speed and accuracy. Omnichannel fulfillment complexity requires sophisticated coordination across inventory, transportation, and customer touchpoints. Accelerating delivery expectations are reinforcing investments in advanced route optimization, fleet management, and real-time tracking technologies. Growing reverse logistics volumes from returns and exchanges are pushing adoption of integrated visibility and analytics platforms. Competition among third-party logistics providers increasingly centers on delivery speed, reliability, and service flexibility. Dynamic pricing models and delivery options necessitate optimization and customer communication.

Artificial Intelligence and Machine Learning Deployment Enabling Cost Reduction and Operational Optimization

Artificial intelligence deployment in logistics operations is systematically reducing costs and improving performance metrics, driving accelerated adoption across global supply chains. Organizations implementing AI enabled supply chain management are achieving meaningful logistics cost efficiencies, stronger inventory optimization, and materially improved service levels, reinforcing continued investment momentum and competitive necessity. Demand forecasting accuracy is significantly enhanced through machine learning models that adapt to volatile consumption patterns. Advanced route optimization algorithms reduce delivery distances, fuel usage, and emissions while improving fleet utilization. Predictive maintenance systems identify potential equipment failures well in advance, minimizing downtime and unplanned repairs. Warehouse automation supported by AI powered robotics increases throughput, picking accuracy, and labor productivity. Intelligent inventory management enables dynamic allocation, safety stock reduction, and improved working capital efficiency. Supplier risk assessment benefits from continuous monitoring.

Restraints - High Initial Technology Investment and Organizational Change Management Requirements Limiting Adoption

Smart logistics market expansion is constrained by significant upfront capital requirements for software, hardware, and automation infrastructure, with mid-market and small logistics operators facing implementation costs exceeding around USD 5-10 million creating adoption barriers particularly in cost-sensitive and price-competitive segments limiting market penetration in lower-margin operator categories. Technology integration complexity across legacy systems and multiple platforms. Skilled workforce requirements for implementation and operation. Extended ROI timelines extending 3-5 years in many scenarios. Change management challenges across established organizations. Integration risks with existing business processes. Vendor lock-in concerns limiting flexibility and competitive alternatives.

Cybersecurity and Data Privacy Regulatory Complexity Creating Implementation and Compliance Barriers

Smart logistics market expansion is constrained by increasing cybersecurity and data privacy regulatory requirements including GDPR, CCPA, and emerging regional frameworks, with supply chain technology providers facing escalating compliance costs and liability exposure limiting adoption particularly in privacy-sensitive jurisdictions and creating implementation complexity for cross-border operations. Data protection compliance costs increasing with regulatory enforcement. Supply chain partner compliance requirements extending to entire ecosystem. Cybersecurity incident liability risks creating insurance and reputational exposure. Cross-border data transfer restrictions limiting international operations. Third-party vendor assessment requirements for supply chain partners. Technology infrastructure security investment requirements. Regulatory audit and certification costs.

Opportunity - Emerging Market Smart Warehousing Infrastructure Development and Automation Investment

Emerging market warehouse automation and modernization represent a substantial growth opportunity driven by rapid industrialization and expanding consumption across developing economies. Accelerating e commerce logistics hub development is strengthening regional distribution networks and supporting faster delivery expectations. Government led infrastructure programs are actively encouraging supply chain modernization and technology adoption. Manufacturing cost advantages across Asia Pacific are enabling competitively priced automation equipment and localized solution development. Favorable labor economics further strengthen return on investment justification for automation projects. Rapid urbanization and rising disposable incomes are increasing shipment volumes and last mile delivery requirements. Technology localization is improving system affordability, scalability, and operational relevance for local operators. Structural supply chain inefficiencies in developing markets continue to create opportunities for productivity gains, cost optimization, service quality improvement, and long term logistics transformation.

Warehouse Automation Robotics and Autonomous Systems Enabling High-Density Operations

Warehouse automation robotics represent a high potential opportunity as enterprises accelerate adoption of autonomous transportation and material handling technologies to address persistent labor constraints and enable high density facility operations. Growing deployment of Autonomous Mobile Robots supports flexible material movement and scalable layouts. Automated Storage and Retrieval Systems enhance vertical space utilization and throughput efficiency. Computer vision systems enable intelligent picking, sorting, and quality verification with reduced error rates. Collaborative robotics allow safe human machine interaction, improving productivity without full workforce displacement. Robotic process automation extends benefits beyond the shop floor by streamlining warehouse administrative and planning tasks. Integrated fleet management platforms optimize robot scheduling, utilization, and energy consumption. Advanced safety and compliance systems ensure reliable operations, regulatory adherence, and workforce protection, reinforcing long term investment confidence across warehouse environments.

Category-wise Analysis

Component Insights

Software components command 38% of smart logistics market share, representing dominant segment reflecting fundamental role of logistics platforms, visibility solutions, and optimization algorithms supporting supply chain coordination and decision-making across organizations of all sizes. Transportation management systems optimizing routing and carrier selection. Warehouse management platforms supporting inventory and fulfillment operations. Demand forecasting and planning software leveraging AI and historical data. Visibility platforms providing real-time supply chain transparency. Fleet management solutions supporting vehicle and driver tracking. Integration platforms connecting disparate supply chain systems. Data analytics platforms enabling performance insights.

Services expands prominently with a CAGR of 20.8%, driven by implementation complexity, continuous optimization needs, and managed service models enabling recurring revenue and stronger customer outcomes. Growth is supported by implementation and integration, managed operations, consulting, training and certification, ongoing support and maintenance, advanced analytics, and continuous improvement services that maximize system performance and long term value realization globally effectively.

Industry Insights

Services sector commands 27% of smart logistics market share, representing established dominant segment reflecting high-value services delivery requiring sophisticated supply chain and delivery logistics supporting sustained demand across diverse services verticals including professional services, hospitality, and entertainment. IT and professional services requiring delivery of solutions and resources. Travel and hospitality supporting tourism logistics and reservations. Media and entertainment requiring content and merchandise distribution. Legal services supporting document delivery and case management. Consumer and personal services requiring last-mile delivery for personal services. Established service provider networks supporting logistics innovation. Customer experience criticality driving logistics technology investment.

Distribution services expands with a CAGR of 20.9%, driven by accelerating e commerce growth, rising last mile delivery complexity, and sustained warehouse automation investment supporting above average expansion. Growth is reinforced by e commerce retail fulfillment, wholesaler efficiency improvements, third party logistics modernization, automated warehousing, digital freight matching, courier innovation, and optimized returns and reverse logistics models across global networks.

Regional Market Insights

North America Smart Logistics Market Trends

North America expands at prominent 20.3% CAGR, driven by technology innovation leadership, mature digital infrastructure, sophisticated consumer expectations, and regulatory excellence supporting market growth acceleration and premium technology adoption across logistics sectors. U.S. market dominance with Amazon, FedEx, and UPS leading technology investment. Amazon 520,000+ AI-powered robots supporting warehouse operations with 99.8% picking accuracy. FedEx Surround platform deploying real-time tracking and predictive analytics. UPS Smart Package initiative rolling out RFID replacing manual scanning across 60,000 vehicles. Walmart AI logistics eliminating 30 million unnecessary delivery miles annually. Mature logistics infrastructure supporting technology integration. Capital availability supporting growth investment. Talent ecosystem supporting specialized talent availability.

North American market characterized by innovation leadership with logistics giants investing heavily in AI, IoT, and automation technologies supporting competitive advantages and operational cost reduction. Enterprise customers demanding advanced visibility and analytics capabilities. Logistics software providers concentrated in established markets. Strategic M&A activity enabling capability acquisition and market consolidation.

Europe Smart Logistics Market Trends

Europe maintains 24% market share with 19.2% CAGR growth, driven by stringent data privacy regulations (GDPR), sustainability consciousness, advanced manufacturing heritage, and established supply chain excellence supporting premium technology positioning and regulatory compliance emphasis. Germany manufacturing strength supporting industrial logistics sophistication. UK regulatory framework driving data protection and compliance excellence. France sustainability focus supporting green logistics investment. Spain distribution hub development supporting regional logistics. GDPR compliance requirements limiting data usage and analytics applications. Sustainability directives driving route optimization and electric vehicle adoption. Advanced manufacturing integration requiring sophisticated supply chain. Cross-border logistics complexity supporting visibility platform demand.

European market characterized by stringent regulatory compliance and sustainability emphasis with logistics providers focusing on data protection and environmental impact reduction. Advanced technology adoption in manufacturing and pharmaceutical logistics. Strong emphasis on supply chain transparency and ethical sourcing. Established customs and compliance expertise supporting international operations.

Asia Pacific Smart Logistics Market Trends

Asia Pacific commands significant 34% market share, driven by rapid e-commerce growth, emerging market infrastructure development, manufacturing excellence, and accelerating digital transformation supporting market leadership and sustained expansion exceeding global averages. China e-commerce dominance supporting warehouse automation and last-mile logistics. India warehouse automation is rapidly expanding with strong adoption momentum. Japan leads in robotics and automation technology innovation. ASEAN logistics growth is supporting regional distribution hub development and stronger supply chain connectivity. Mobile-first digital adoption enabling smart logistics platform adoption. Manufacturing concentration requiring supply chain coordination. Emerging market workforce supporting labor-cost-effective automation ROI. Government infrastructure programs supporting supply chain modernization.

Asia Pacific market characterized by rapid growth and emerging market opportunities with technology adoption accelerating faster than developed markets. Cost-conscious procurement supporting mid-range equipment adoption. Manufacturing presence attracting equipment supplier investment. Government initiatives supporting supply chain modernization and logistics infrastructure development.

Competitive Landscape

The global smart logistics market exhibits a consolidated structure, with multinational leaders including DHL, FedEx, UPS, and Amazon leveraging integrated logistics operations and advanced technology platforms, complemented by software and technology specialists such as Flexport, Descartes, JDA/Blue Yonder, and FourKites, while emerging logistics technology providers including Agistix, Convoy (now DAT), and specialized automation vendors capture niche opportunities and support technology driven competitive differentiation.

Strategic Developments

- In October 2023, Flexport acquired Convoy Platform assets and intellectual property following Convoy's shutdown, acquiring sophisticated freight-matching technology automating 98% of load procurement and retaining core product engineering team supporting expanded logistics service offerings and integrated platform capabilities.

- In April 2024, Flexport launched Convoy Platform as open digital marketplace for freight brokers enabling automated freight matching with thousands of carriers and supporting adoption across independent brokers while maintaining platform neutrality and expanding value proposition to broader market.

- In July 2025, DAT Freight & Analytics announced definitive agreement to acquire Convoy Platform from Flexport for approximately USD 250 million, integrating advanced freight-matching automation with DAT One load board supporting enhanced customer capabilities and seamless access to both automated and hands-on freight-matching options.

Companies Covered in Smart Logistics Market

- DHL

- FedEx

- UPS

- Amazon

- Walmart

- Flexport

- DAT Freight & Analytics

- JDA Software/Blue Yonder

- Descartes

- XPO

- Geodis

- Agistix

- FourKites

- Convoy

Frequently Asked Questions

The smart logistics market is expanding from US$ 56.1183 Billion in 2026 to US$ 209.4381 Billion by 2033 at a 20.7% CAGR.

Market growth is primarily driven by e-commerce driven last-mile complexity, AI and machine learning enabled cost and performance optimization, and widespread IoT adoption enabling real-time supply chain visibility.

The smart logistics market is projected to grow at a 20.7% CAGR during 2026-2033.

Key opportunities include emerging market warehouse automation, supply chain visibility platform monetization, and rapid adoption of autonomous robotics and digital twin technologies.

The smart logistics market is led by global logistics giants and technology providers such as DHL, FedEx, UPS, Amazon, Walmart, Blue Yonder, Descartes, XPO, and emerging visibility and automation specialists.