- Pharmaceuticals

- U.S. Pharmaceutical Logistics Market

U.S. Pharmaceutical Logistics Market Size, Share, and Growth Forecast for 2025 - 2032

U.S. Pharmaceutical Logistics Market by Type (Cold Chain, Non-cold Chain), by Component (Storage, Transportation, Monitoring Components), Services (Transport, Warehousing Services, Value-added Services), and Analysis for 2025 - 2032

U.S. Pharmaceutical Logistics Market Size and Trends

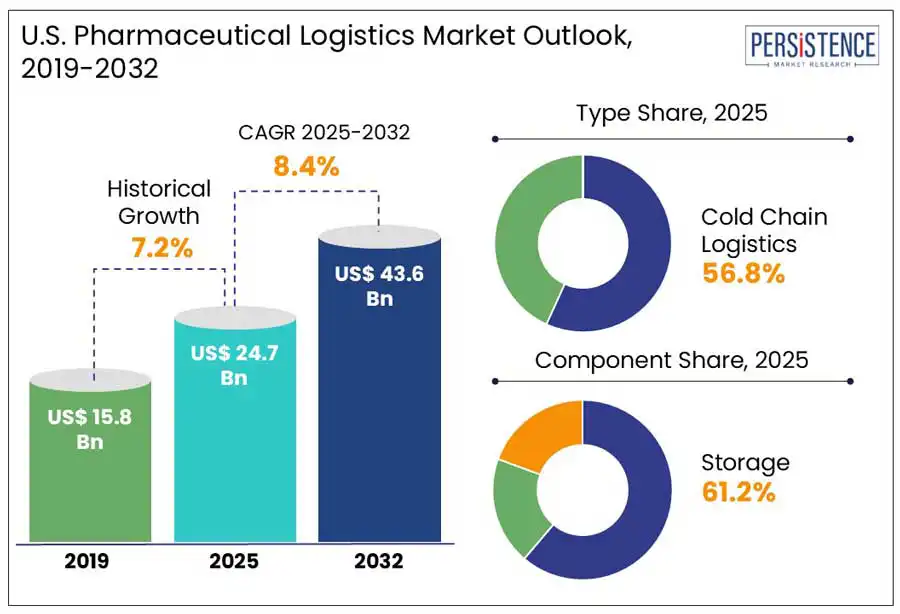

The U.S. pharmaceutical logistics market size is predicted to reach US$ 43.6 Bn in 2032 from US$ 24.7 Bn in 2025. It will likely witness a CAGR of around 8.4% in the forecast period between 2025 and 2032.

The U.S. has been witnessing a surge in the manufacturing of generic drugs as these are more cost-effective than brand-name drugs and do not require extensive testing and research. This surge has supported the U.S. healthcare sector by making the treatment easily accessible and affordable. Increasing generic drug manufacturing in the U.S. has resulted in the influx of several pharmaceutical distributors.

According to a new study, distributors in the country manage around 92% of pharmaceutical sales, bringing order and efficiency to the supply chain that connects two fragmented markets, namely, over 180,000 points of sale and 1,300 manufacturers. With the rising shipment of medical devices and drugs from the U.S. to other parts of the globe, pharmaceutical companies are inclining toward third-party logistics firms.

Key Industry Highlights

- Cold chain logistics are projected to generate around 56.8% share in 2025 as regulatory bodies mandate cold chain compliance for several high-value pharmaceutical products.

- Storage is estimated to hold about 61.2% share in 2025 due to growth in biologics and specialty drugs requiring specialized storage environments.

- Midwest U.S. is expected to account for approximately 31.6% share in 2025 amid increasing public-private partnerships promoting infrastructure for life sciences and supply chain resilience.

- Expansion of micro-fulfillment centers near urban hubs for same-day drug delivery will likely open the door to new avenues.

- Key companies are focusing on investing in customized logistics services for clinical trials and personalized medicine therapies.

|

Market Attribute |

Key Insights |

|

U.S. Pharmaceutical Logistics Market Size (2025E) |

US$ 24.7 Bn |

|

Market Value Forecast (2032F) |

US$ 43.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.2% |

Market Dynamics

Driver - Surge in HPAPI production to boost strategic shifts in pharmaceutical logistics

The active pharmaceutical ingredient market is expected to significantly transform the field of pharmaceutical logistics in the U.S. Various Active Pharmaceutical Ingredients (APIs) utilized in drug manufacturing are imported from countries such as China and India. It makes the supply chain vulnerable to export restrictions, trade disruptions, and geopolitical tensions. In 2023, for example, India restricted the export of 26 APIs temporarily due to high domestic demand. It resulted in supply chain disruptions, compelling U.S.-based logistics companies to develop strategic stockpiles of required APIs closer to manufacturing facilities as well as diversify sourcing routes.

The rapid inclination toward high-potency APIs (HPAPIs), specifically used in hormonal treatments and targeted cancer therapies, is further augmenting the U.S. pharmaceutical logistics market growth. HPAPIs are toxic and sensitive, requiring skilled handling, secure transport, and specialized containment. Companies, including DHL Supply Chain and FedEx have hence developed training programs and segregated transportation units to handle these materials. DHL, for example, recently introduced a specialized service for HPAPIs with improved compliance tools and isolation packaging. Similar developments point to the niche adaptations logistics companies are anticipated to make.

Restraint - Operational hurdles with increasing regulatory compliance demands

Increasing complexity of regulatory compliance is envisioned to be a key challenge in the field of pharmaceutical logistics in the U.S. The Food and Drug Administration (FDA) has implemented the Supply Chain Security Act (DSCSA), which requires the traceability of pharmaceutical products from manufacturers to patients. All pharmaceutical shipments must be tracked and serialized with innovative technologies, including Radio-Frequency Identification (RFID) and blockchain, as of 2024.

The aforementioned technologies are highly efficient in enhancing transparency and security. However, these require significant investments in software and infrastructure, creating both operational and financial hurdles for logistics companies. Companies such as Cencora, Inc., for example, have been updating their systems to comply with such norms, investing more than US$ 100 Mn in traceability technologies. For small-scale firms, such investments are not always feasible, thereby limiting growth.

Opportunity - Demand for specialized packaging spurs developments in medical logistics

The pharmaceutical packaging market is projected to create new growth avenues for logistics companies in the U.S. It is attributed to the rising demand for improved sustainability, compliance, and protection across the supply chain. The emergence of temperature-sensitive drugs and biologics have resulted in an increasing demand for specialized packaging materials, including real-time condition-monitoring sensors, Phase Change Materials (PCMs), and vacuum-insulated panels. Cryoport, for example, reported a 23% surge in demand for its ultra-cold packaging systems in 2024. These are used to transport mRNA-based treatments and gene therapies, highlighting a direct connection between logistics requirements and novel packaging.

Tamper-evident and child-resistant packaging norms are further predicted to influence pharmaceutical logistics. Such types of packaging solutions often add volume and weight to shipments, thereby increasing space requirements and transportation costs. Logistics companies in the U.S. are hence focusing on deploying AI-based load optimization tools to evaluate container and pallet layouts for such packaging solutions. Irving-based McKesson, for instance, recently rolled out its AI logistics software solution to reduce dead space in shipments of bulky opioid packaging. It led to an 18% improvement in cost savings and load efficiency.

Category-wise Analysis

Type Insights

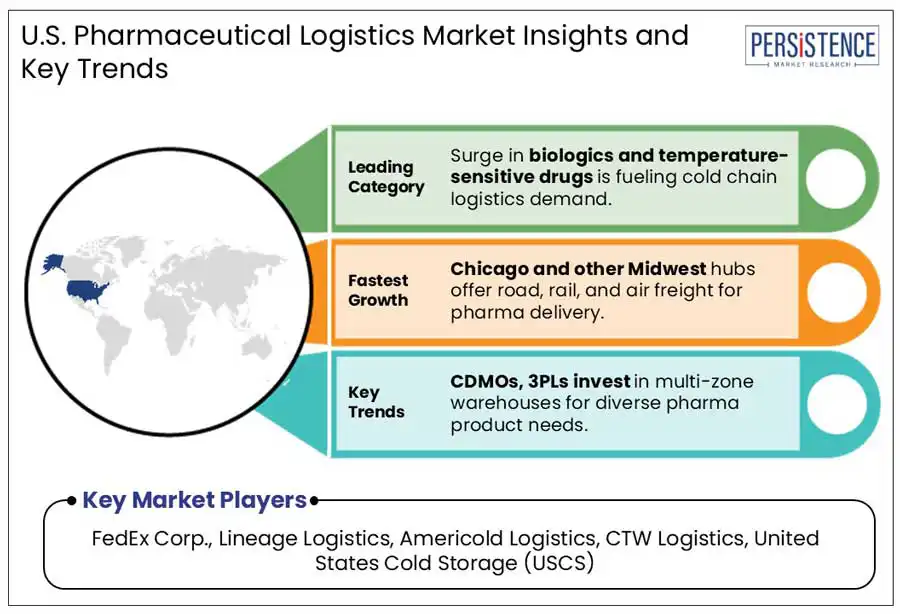

Based on type, the market is bifurcated into cold chain and non-cold chain logistics. Out of these, the cold chain logistics segment is predicted to generate approximately 56.8% of the U.S. pharmaceutical logistics market share in 2025. The government’s preparedness for public health crises will likely bolster investments in cold chain capacity expansions. The Strategic National Stockpile, for example, extended its cold chain storage provisions following the rollout of the COVID-19 vaccine. The increasing popularity of gene therapies and personalized medicine, which are usually produced in small batches, is also poised to spur the requirement for ultra-cold storage. Commercially available gene therapies, including Luxturna and Zolgensma, require storage temperatures as low as -60°C to -80°C. Hence, demand for innovative cold chain capabilities such as active temperature-controlled packaging systems and liquid nitrogen-cooled containers is anticipated to rise.

Non-cold chain logistics are expected to exhibit decent growth in the U.S., backed by the rising volume of oral solid dosage forms, over-the-counter (OTC) medications, and conventional drugs. These do not require temperature-controlled handling, thereby supporting the growth of non-cold chain logistics. As per IQVIA U.S.-based, oral solids such as capsules and tablets, accounted for nearly 60% of all prescriptions filled in 2023 in the U.S. This proves that even though the focus on biologics is rising in the country, a significant portion of the pharmaceutical industry still comprises small-molecule drugs. These drugs are capable of remaining stable at ambient temperatures, further spurring demand for affordable distribution using standard non-cold chain networks.

Component Insights

In terms of component, the market is trifurcated into storage, transportation, and monitoring components. Among these, storage will likely account for a share of nearly 61.2% in 2025, found Persistence Market Research. Increasing demand for both branded and generic drugs has led to the expansion of storage facilities in the U.S. These help procure and preserve the efficacy of drugs after production, further distributing them through various channels to retailers and distributors. The development of temperature-sensitive storage facilities is increasing across the country as these are gaining traction in the pharmaceutical biologics market. As biologics often face quality issues due to frequent temperature fluctuations, these are kept in time-sensitive storage solutions.

Monitoring components, on the other hand, are predicted to showcase a considerable CAGR from 2025 to 2032. This is mainly due to the increasing demand for safety, integrity, and efficiency of cold chain products. Ongoing developments in cloud-connected and Internet of Things (IoT)-based tracking solutions are projected to boost this trend. In 2024, UPS Healthcare, for example, launched SmartLabel technology to provide end-to-end visibility with humidity, temperature, and GPS tracking. It is embedded directly in shipping labels. Such new product developments in the logistics industry are speculated to propel the segment’s growth.

Zone Insights

West U.S. Pharmaceutical Logistics Market Trends

The West is expected to be outpaced by California, which houses more than 3,700 life sciences companies. The Bay Area and San Diego are considered the key biotech and pharmaceutical powerhouses. The Port of Long Beach and the Port of Los Angeles often handle a significant share of pharmaceutical imports from Asia Pacific, mainly raw materials and APIs. Both ports had collectively processed over 400,000 TEUs of refrigerated containers in 2023. The majority of these were temperature-controlled pharmaceutical shipments, showcasing the role of maritime cold chain in pharmaceutical logistics in the West.

The pharmaceutical outsourcing market is also predicted to positively impact the West as small-scale biotech companies are outsourcing logistics services without investing in their own infrastructure. Catalent, a renowned Contract Development and Manufacturing Organization (CDMO) with a significant presence in California, for instance, provides end-to-end services such as shipping, storage, labeling, and fill-finish for highly sensitive biologics. The launch of similar services in the West is envisioned to create new opportunities.

Southeast U.S. Pharmaceutical Logistics Market Trends

States in the Southeast, such as Florida, Georgia, and North Carolina, have become significant for life sciences investment, thereby propelling the development of novel logistics infrastructure. Research Triangle Park in North Carolina, for example, has attracted international pharmaceutical manufacturers, including Novo Nordisk and Eli Lilly. This has accelerated cold chain logistics services to boost the movement and storage of temperature-sensitive drugs. The state recorded more than US$ 3.2 Bn in life science investments in 2023, most of which was associated with advanced therapies and biologics requiring special logistics. These numbers are expected to skyrocket in the forthcoming years, further spurring the market.

The well-established pharmaceutical excipients market in the Southeast is further speculated to create new growth opportunities. Excipients are usually sourced separately from APIs and mixed at different stages of production. Hence, these require additional coordination in just-in-time delivery and warehousing. Hydroxypropyl methylcellulose (HPMC), a commonly utilized excipient in extended-release tablets, for instance, should be stored in humidity-controlled environments. This helps prevent degradation or clumping. Local logistics companies are hence anticipated to integrate excipient-specific handling protocols in distribution centers to prevent the loss of functionality before formulation.

Midwest U.S. Pharmaceutical Logistics Market Trends

The Midwest will likely hold a share of about 31.6% in 2025 due to its proximity to key transportation hubs and robust manufacturing presence. It has become a significant zone for pharmaceuticals, specifically for its central location. This enables more efficient reach to both West and East Coast markets. Prominent states, including Michigan, Ohio, and Illinois, have witnessed high investments in pharmaceutical distribution infrastructure. Illinois, with its close proximity to O'Hare International Airport and important rail networks, has become a logistical hub for various pharmaceutical companies.

FedEx, for instance, recently extended its Cold Chain Solutions facility in Indianapolis, investing about US$ 50 Mn to broaden gene therapies and vaccines handling capacity. This strategy came into action with the rising demand for innovative transportation and cold storage solutions for medicines in the area. Also, companies such as Cardinal Health in Ohio have started using automated systems to enhance order fulfillment accuracy and inventory management.

Competitive Landscape

The U.S. pharmaceutical logistics market is highly dynamic and specialized, with the presence of large-scale players, niche service providers, and mid-sized pharmaceutical distributors. The market is shaped by the requirement for real-time visibility, regulatory compliance, and temperature-controlled transport. With the boom of personalized medicine, specialty drugs, and biologics, key players are focusing on offering end-to-end cold-chain logistics.

Several pharmaceutical companies are also outsourcing logistics to focus on core competencies, creating space for partnerships and niche providers. The rising emphasis on real-time tracking and blockchain for chain-of-custody is leading to rapid digital transformation. Various companies are striving to invest in direct-to-patient services and clinical trial logistics to cater to personalized therapies and high-value biologics. Key companies are further acquiring specialized firms to extend their capabilities.

Key Industry Developments

- In May 2025, GXO Logistics, Inc. bagged a 10-year, US$ 2.5 Bn contract with the U.K.’s National Health Service (NHS) Supply Chain. It marked an important extension in healthcare logistics. Under this contract, GXO will oversee a dedicated fleet of more than 300 vehicles and manage eight NHS Supply Chain distribution centers.

- In April 2025, UPS declared its acquisition of Canada-based Andlauer Healthcare Group Inc. (AHG), a renowned provider of specialized cold chain transportation solutions for the healthcare sector for nearly US$ 1.6 Bn. This acquisition would help extend the portfolio of end-to-end cold chain capabilities of UPS.

- In February 2025, GXO Logistics, Inc., headquartered in Connecticut, signed a multi-year agreement with Siemens Healthineers to extend its Forward Stocking Network at two strategic locations in the U.S. This partnership will help extend inventory capacity by more than 30% as it includes two new distribution centers in California and New Jersey.

Companies Covered in U.S. Pharmaceutical Logistics Market

- FedEx Corp.

- Lineage Logistics

- Americold Logistics

- CTW Logistics

- United States Cold Storage (USCS)

- SEKO Logistics

- United Parcel Service Inc.

- Nichirei Logistics Group, Inc.

- C H Robinson Worldwide Inc.

- Owens and Minor Inc.

- Others

Frequently Asked Questions

The U.S. pharmaceutical logistics market is projected to reach US$ 24.7 Bn in 2025.

Increasing manufacturing of generic drugs and rising imports of APIs are the key market drivers.

The market is poised to witness a CAGR of 8.4% from 2025 to 2032.

Integration of RFID for real-time tracking and development of temperature-sensitive storage facilities are the key market opportunities.

FedEx Corp., Lineage Logistics, and Americold Logistics are a few key market players.