- Transportation & Logistics

- Disaster Relief Logistics Market

Disaster Relief Logistics Market Size, Share, and Growth Forecast, 2026-2033

Disaster Relief Logistics Market by Service (Transportation, Warehousing & Distribution, Inventory & Supply Chain Management, Procurement & Coordination, Reverse Logistics), End-User (Government Agencies, International Organizations, NGOs, Military & Defense, Private Sector), Disaster Type (Natural Disasters, Man-Made Disasters, Public Health Emergencies), and Regional Analysis for 2026-2033

Disaster Relief Logistics Market Share and Trends Analysis

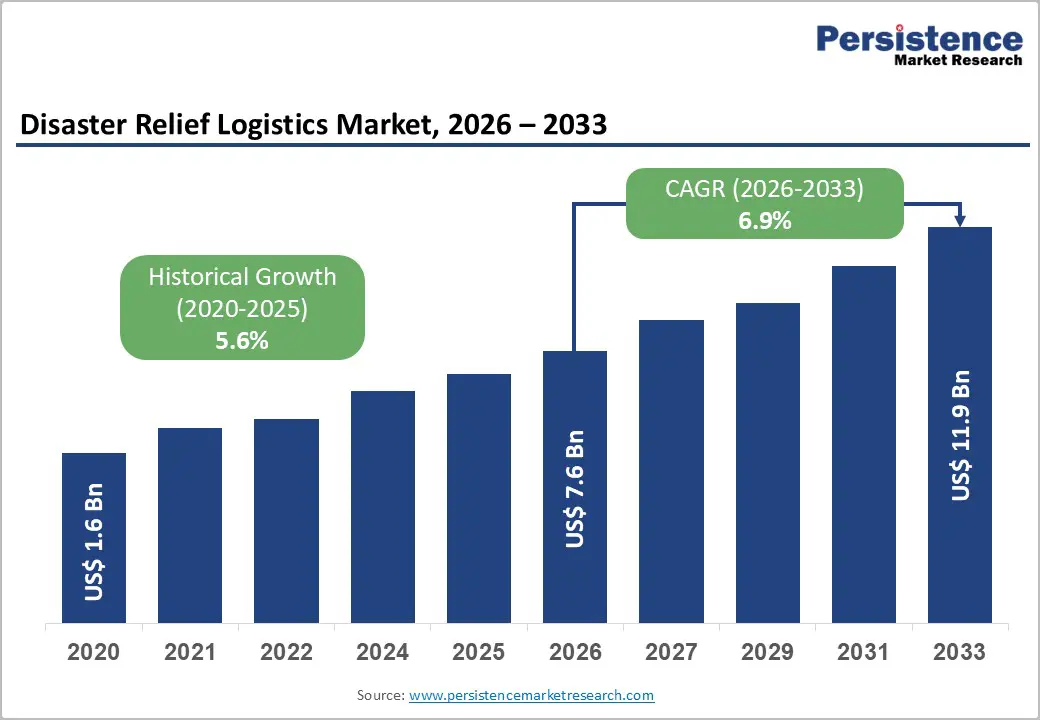

The global disaster relief logistics market size is likely to be valued at US$ 7.6 billion in 2026, and is projected to reach US$ 11.9 billion by 2033, growing at a CAGR of 6.9% during the forecast period 2026–2033.

The market is expanding due to the rising frequency and severity of climate-related disasters, increased humanitarian funding commitments, and the growing integration of digital supply chain technologies into emergency response operations. According to global disaster monitoring agencies, weather-related events now account for the majority of recorded large-scale emergencies, compelling governments to institutionalize structured logistics preparedness frameworks.

Budget allocations for disaster risk reduction and emergency response continue to rise across major economies, strengthening procurement pipelines for transportation, warehousing, and coordination services. The adoption of real-time tracking, predictive analytics, satellite mapping, and automated inventory systems is improving response speed, accountability, and operational efficiency, supporting sustained market expansion.

Key Industry Highlights

- Dominant Service: Transportation is expected to lead with approximately 40% share in 2026, while digital inventory solutions are projected to be the fastest-growing during 2026–2033, reflecting tightening need for coordinated emergency response systems.

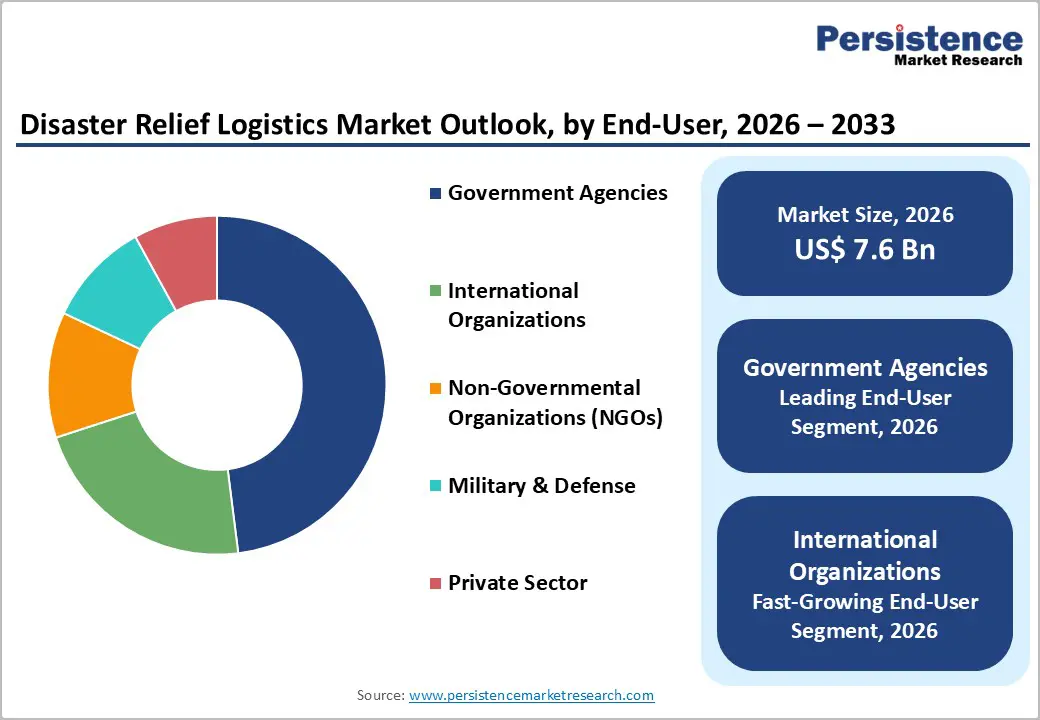

- Leading End-Users: Government agencies are anticipated to dominate with nearly 48% share in 2026, while international organizations are likely to register the fastest growth at around 7.9% CAGR through 2033, supported by expanding cross-border humanitarian operations.

- Dominant Disaster Type: Natural disasters are projected to account for about 68% revenue share in 2026, whereas public health emergencies are expected to grow the fastest through 2033, driven by epidemic preparedness and medical supply chain investments.

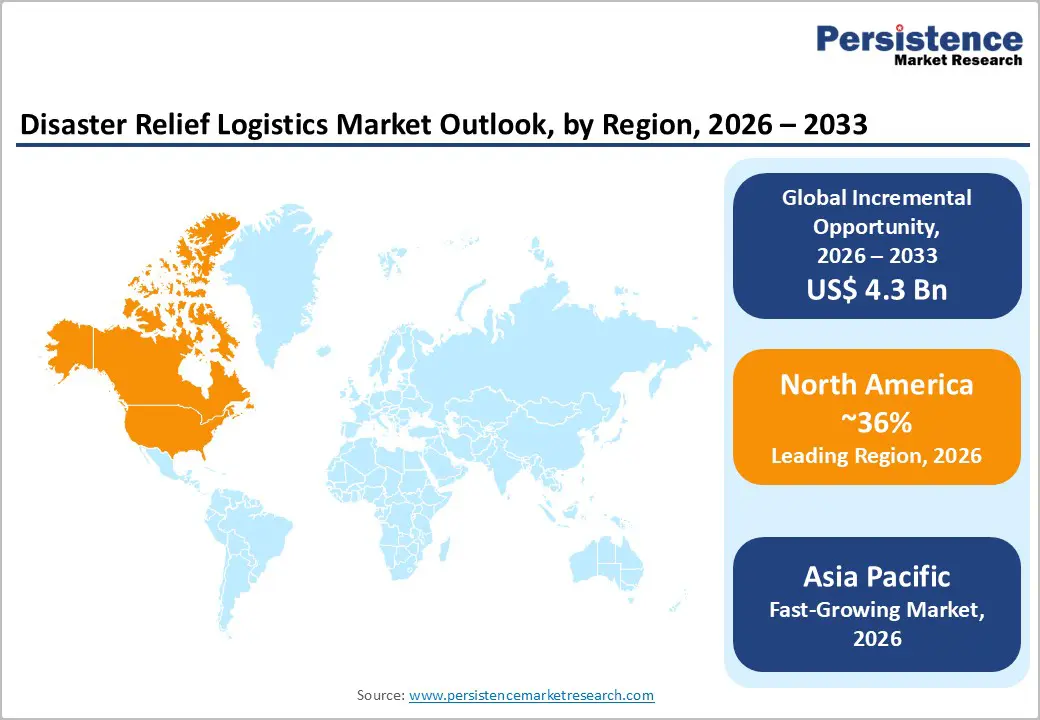

- Regional Leadership: North America is set to lead with an estimated 36% share in 2026, while the Asia Pacific market is forecast to expand at the fastest pace of roughly 8% CAGR through 2033, backed by climate resilience funding.

- November 2025: The International Organization for Migration (IOM) and DHL Group formed a global partnership to strengthen humanitarian logistics capacity through improved supply chain coordination, emergency response support, and disaster preparedness initiatives worldwide.

|

Key Insights |

Details |

|---|---|

|

Substation Automation Market Size (2026E) |

US$ 7.6 Bn |

|

Market Value Forecast (2033F) |

US$ 11.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Climate-Related Disasters and Institutional Funding Commitments

According to the United Nations Office for Disaster Risk Reduction (UNDRR), the number of climate-related disasters has nearly doubled over the past two decades, intensifying pressure on national response systems. In 2025, severe flooding across the U.S. and Canada prompted emergency declarations and large-scale logistics mobilization coordinated by the Federal Emergency Management Agency and Public Safety Canada. Similarly, governments in India and Indonesia activated national disaster response forces to manage flood and cyclone-related supply distribution. These operations required rapid airlift deployment, temporary warehousing, and coordinated last-mile delivery in damaged infrastructure zones. Authorities are increasingly expanding pre-positioned inventory hubs and formalizing emergency transport agreements. The growing scale of climate exposure is structurally strengthening demand for organized disaster logistics networks.

Humanitarian funding is expanding in parallel with rising disaster risk. The UN Office for the Coordination of Humanitarian Affairs reported global humanitarian funding requirements exceeding US$ 50 billion in 2024, reinforcing preparedness commitments worldwide. In the U.S., the Federal Emergency Management Agency (FEMA) allocates substantial disaster relief funding under federal emergency frameworks to support logistics readiness and recovery operations. In 2025, India’s National Disaster Management Authority (NDMA) and Japan’s Cabinet Office increased allocations for emergency warehousing and rapid-response fleet contracts. These structured budgetary commitments translate into predictable procurement agreements for transportation, coordination, and stockpiling services. Institutional funding mechanisms reduce revenue volatility and enhance long-term planning visibility for logistics providers.

Digital Transformation and Operational Modernization of Emergency Supply Chains

Disaster logistics is undergoing rapid digital modernization through AI-based forecasting, satellite mapping, blockchain traceability, and IoT-enabled inventory tracking. The World Economic Forum (WEF) has emphasized digital supply chains as critical to resilient humanitarian systems. In 2025, India’s NDMA expanded real-time flood monitoring and control room digitization initiatives to improve response coordination. Japan’s Fire and Disaster Management Agency also enhanced digital disaster information-sharing platforms to streamline supply allocation. These tools improve inter-agency coordination, reduce duplication of relief materials, and optimize deployment routes. As disasters grow more complex, data-driven logistics systems are becoming essential to operational effectiveness.

In 2025, the Government of Rwanda expanded its national drone delivery program in partnership with Zipline to strengthen medical supply distribution during emergencies. The U.S. Department of Transportation (DOT) supported pilot programs integrating unmanned aerial systems into disaster response corridors. Japan deployed digital twin simulations for earthquake preparedness under Cabinet Office disaster resilience initiatives. Technology integration reduces spoilage, misallocation, and theft, historically estimated to account for 5–10% of emergency supply losses. Digital cold-chain monitoring has strengthened vaccine and medical logistics resilience in multiple regions. These measurable efficiency gains are accelerating response timelines while improving accountability and cost control.

Infrastructure Damage and Last-Mile Delivery Constraints

Disasters frequently damage roads, ports, and airports, the very infrastructure required for logistics deployment. In late 2025, Cyclone Zelia caused major flooding and port closures in Australia, forcing closures at Port Hedland, Cape Lambert and Dampier for three days, disrupting shipping and offshore logistics operations. In the same period, Typhoon Matmo’s landfall in southern China led to airport closures, halted rail services, and suspended ferry operations, directly affecting freight movement. Cyclone “Ditaw” in Sri Lanka caused prolonged congestion at the Port of Colombo, with vessels delayed as recovery continued weeks after initial impact. Damaged roads and weakened bridges in the 2025 Cebu earthquake in the Philippines further illustrate how infrastructure degradation hinders emergency logistics access. These disruptions often require costly rerouting and emergency transport solutions. When access is compromised, timely delivery of relief supplies becomes significantly more challenging.

Such disruptions increase logistics costs by 15–25% due to rerouting, airlift dependence, and extended waiting times at backlog points. In infrastructure-limited regions, temporary warehousing capacity remains strained, reducing distribution throughput during high-demand periods. Telecommunications and power outages in disaster zones further slow coordination between agencies, lengthening response cycles. Last-mile access to remote communities is frequently delayed by damaged bridges and blocked roadways. These structural bottlenecks raise execution risks for logistics providers, especially in countries with limited resilience planning. The cumulative impact is slower aid delivery, higher operational costs, and reduced capacity to meet urgent humanitarian needs.

Funding Volatility and Bureaucratic Delays

Although aggregate humanitarian funding needs are growing, disbursement timing and consistency remain highly volatile. According to the UN High Commissioner for Refugees (UNHCR), major cuts to humanitarian funding have left millions at risk of losing essential support, with only a fraction of required resources met by mid-2025. Several UN agencies and non-governmental organizations (NGOs) have had to scale back programs or lay off staff due to shrinking budgets, affecting operational readiness and forward planning. In early 2026, ongoing funding shortfalls forced the UN Relief and Works Agency (UNRWA) to reduce core health and education services for refugees across multiple countries. This unpredictability complicates logistics resource allocation for ongoing and future emergencies.

Public-sector procurement rules and cross-border regulatory approvals can also extend onboarding timelines by 6–12 months, reducing operational agility in crisis scenarios. NGOs often report significant delays in grant releases after initial pledges are made, slowing program roll-outs. Even when funding is pledged, conditional rules or shifting geopolitical priorities can delay actual distribution of resources, weakening response capabilities. These financial uncertainties constrain long-term capacity planning and asset utilization, particularly for smaller logistics operators without diversified revenue streams. Revenue concentration among government contracts increases exposure to policy risk, tempering new entrants and investment in scalable logistics infrastructure.

Infrastructure Modernization and Public-Private Collaboration in Developing Economies

A growing of number of countries across Asia Pacific and Sub-Saharan Africa are investing heavily in disaster-resilient infrastructure to strengthen climate adaptation capacity. In early 2026, for instance, the Government of India announced a national disaster-resilient infrastructure initiative linking resilient transport corridors, elevated storage sites, and flood-proof warehousing to improve logistics continuity during extreme events. Similar investments are underway in Vietnam and Bangladesh, driven by flood risk reduction mandates. Multilateral development banks (MDBs) are financing climate adaptation projects exceeding US$ 100 billion globally, supporting resilient ports and inland freight facilities. These investments are creating long-term structural demand for integrated disaster logistics networks. Governments are transitioning from reactive response models toward proactive preparedness through strategic infrastructure planning.

Pre-positioned regional logistics hubs represent a high-growth sub-segment within these modernization efforts. Providers establishing early partnerships with national disaster management authorities gain first-mover advantage in long-term procurement cycles. In 2025, Nigeria’s National Emergency Management Agency (NEMA) inaugurated emergency logistics warehouses in Kano and Lagos to improve distribution speed during humanitarian responses. Public-private partnerships (PPPs) between municipal authorities and commercial logistics firms are expanding, reducing capital burden while scaling capacity. For example, the City of Toronto expanded agreements with private warehousing and transport providers to streamline urban emergency response logistics. These multi-year agreements generate recurring revenue streams and support long-term infrastructure expansion across emerging and developed markets alike.

Technology-Enabled Last-Mile and Digital Supply Chain Solutions

Drone delivery, autonomous vehicles, and satellite-enabled tracking systems are expanding the operational scope of disaster logistics. In 2025, the Rwandan government expanded its national drone delivery program in partnership with Zipline to strengthen medical supply distribution during emergencies. This program delivered essential medicines and vaccines to remote clinics faster than conventional transport systems. In early 2026, the U.S. Department of Transportation announced new funding for integrating unmanned aerial systems (UAS) into official emergency corridors to expedite last-mile delivery during natural disasters. These technological deployments reduce dependency on damaged ground infrastructure and improve service reliability.

Digital platforms offering predictive analytics for inventory allocation represent scalable SaaS-based revenue streams within the ecosystem. In 2025, Japan’s Cabinet Office expanded a cloud-based disaster logistics coordination platform integrating real-time inventory tracking and field reporting across prefectures, improving responsiveness during typhoon seasons. Automated cold-chain monitoring systems have also been adopted by multiple public health agencies to ensure integrity of vaccine distribution during emergencies. These systems enhance transparency, reduce wastage, and improve compliance reporting for funding agencies. As digital adoption accelerates among government and humanitarian partners, technology-driven logistics services are positioned to capture a growing share of overall market expansion.

Category-wise Analysis

Service & Function Insights

Transportation services are estimated to command an estimated 40% of the disaster relief logistics market revenue share in 2026, primarily driven by urgent mobility requirements during crisis events. For instance, in 2025, the Government of India’s large-scale deployment during the Kishtwar flash floods demonstrated extensive air and ground mobilization for relief distribution. Similarly, central authorities in China coordinated rapid airlift and land transport support following the 2025 Tibet earthquake. These government-led operations reinforce the structural dependence on transport capacity in emergency response systems. Multimodal integration across air, land, and marine networks continues to strengthen deployment efficiency. As public disaster preparedness budgets expand, transportation is projected to retain its dominant share through 2033.

Digital inventory solutions are projected to be the fastest-growing services, expanding at an estimated 7.8% CAGR between 2026 and 2033, supported by increasing government investments in stock pre-positioning and digital tracking. In 2025, the operationalization of the Caribbean Regional Logistics Centre in Barbados enhanced regional warehouse capacity and cold storage preparedness for hurricane response. Such infrastructure expansion reflects a broader shift toward centralized inventory visibility and coordinated supply networks. Governments are increasingly prioritizing real-time monitoring systems to minimize shortages and overstocking risks. Enhanced traceability and procurement transparency are further strengthening supply chain modernization efforts. This structural shift toward logistics optimization is expected to accelerate segment growth over the forecast period.

End-User Insights

Government agencies are anticipated to hold nearly 48% of the disaster relief logistics market share in 2026, maintaining leadership due to statutory responsibility and dedicated disaster management budgets. In 2025, national authorities across multiple regions conducted coordinated airlift and ground relief operations during large-scale flood and earthquake events, reinforcing the central logistical role of state institutions. Government agencies continue to invest in fleet modernization, emergency warehousing, and rapid deployment infrastructure. Structured funding cycles and legislative mandates ensure consistent procurement activity. Public sector dominance is therefore expected to remain stable throughout the forecast horizon. Continued climate-related disaster frequency is likely to further sustain this segment’s share.

International organizations are projected to record the fastest 2026-2033 growth at about 7.9% CAGR, supported by expanding cross-border humanitarian coordination. In 2025-2026, international humanitarian agencies scaled logistics operations in regions such as Myanmar, Bangladesh, and South Sudan following natural disasters and overlapping crises. These deployments highlight growing reliance on pooled procurement platforms and regional distribution hubs. International actors are increasingly complementing national response mechanisms, particularly in vulnerable and conflict-affected regions.

Regional Insights

North America Disaster Relief Logistics Market Trends

North America is poised to dominate in 2026, likely to capture approximately 36% of the disaster relief logistics market value in 2026. The U.S. anchors this leadership through structured federal disaster funding and well-defined emergency response frameworks. For example, during the 2025 Pacific Northwest floods, authorities in Washington State declared emergencies and mobilized the National Guard to support logistics and supply distribution across affected communities. Federal and state coordination in large-scale weather events enhances the demand for organized logistics services. Canada’s provincial disaster response units have also been strengthening inter-agency transport and warehouse deployment plans following atmospheric river events in late 2025. Digital adoption, integrated command centers, and coordinated multimodal transport systems support rapid mobilization across borders.

Market growth in North America is expected to remain stable as preparedness systems mature and digital platforms become embedded in government logistics planning. Public-private collaboration is strengthening, such as binational supply chain development discussions highlighted at the 2026 Logistics Summit Los Laredos, aimed at expanding regional logistics infrastructure and cooperation between U.S. and Mexican authorities. Investments are increasingly directed toward advanced robotics, autonomous vehicles, and resilient facilities that can support rapid distribution post-disaster. Workforce and policy support for last-mile logistics expansion further enhances readiness. Although disaster frequency varies year to year, the institutionalized readiness framework sustains recurring demand.

Europe Disaster Relief Logistics Market Trends

Europe is estimated to contribute approximately 27% of global market revenue in 2026, owing to harmonized civil protection mechanisms and strengthened regional preparedness. The Disaster Resilience Days 2025 conference in Brussels brought together policymakers and technical experts to advance coordinated disaster response and logistics readiness across European Union (EU) member-states. Such forums reinforce knowledge sharing and operational standardization among member states. Germany, France, the U.K., and Spain are together bolstering disaster logistics planning by reinforcing transport corridors and emergency supply networks. Cross-border civil protection mechanisms allow rapid mobilization of resources in response to extreme events. Reflecting wider climate risk patterns, Southern European states have been incrementally expanding wildfire and heatwave logistics support capacities in 2025.

Policy and investment trends in Europe increasingly emphasize sustainability and interoperability. Low-emission emergency fleets and eco-friendly warehouse infrastructure are aligning with broader climate and energy goals set by regional authorities. The EU’s coordinated humanitarian airlift operations following the 2025 Myanmar earthquake involved EU partners providing emergency supplies and logistical support, exemplifying how European capacities are deployed beyond regional boundaries. Digitized response platforms and shared resource allocation frameworks are improving operational efficiency. Policy stability under EU-backed initiatives provides predictable planning timelines. While growth is moderate relative to Asia Pacific, structured regional coordination ensures Europe remains a significant and dependable segment.

Asia Pacific Disaster Relief Logistics Market Trends

Asia Pacific is likely to stand out as the fastest-growing regional market for disaster relief logistics, exhibiting an approximate 2026-2033 CAGR of 7.2%. Frequent and complex climate events, including widespread 2025 Southeast Asia floods and landslides that impacted Indonesia, Malaysia, Thailand, and Vietnam, have highlighted the urgent need for strengthened logistical preparedness systems in the region. National governments, including China, Japan, India, and ASEAN members, are expanding emergency transport capacity and regional distribution hubs to improve reach into vulnerable and remote areas. Digital systems for situational awareness and rapid field coordination are increasingly integrated into national disaster management frameworks.

The region’s rapid infrastructure modernization is facilitating improved resilience planning and disaster logistics execution. For instance, sovereign disaster risk insurance and innovative financial preparedness tools in Southeast Asia are enabling faster payouts and funding availability following impact triggers, reducing response lag and strengthening logistics deployment capacity. Investments in regional multimodal transport corridors are also enhancing cross-border logistics linkages. Governments are prioritizing AI-enhanced weather monitoring systems and real-time field coordination platforms, improving early warning and response mobilization. These developments position Asia Pacific as the primary engine of incremental market growth through 2033, underpinned by expanding infrastructure, digital modernization, and cross-national disaster risk cooperation.

Competitive Landscape

The global disaster relief logistics market structure is moderately consolidated, with leading providers such as DHL Group, Kuehne+Nagel, DB Schenker, and FedEx accounting for a substantial share of structured emergency logistics contracts. These firms leverage global freight networks, chartered air capacity, and established government partnerships. Their strength lies in integrated multimodal transport, pre-positioned warehousing, and digital tracking platforms. Continued investment in AI-enabled route optimization and cold-chain systems enhances rapid response capability. Regulatory expertise and cross-border compliance further reinforce their competitive positioning.

At the same time, humanitarian-focused operators such as World Food Programme and corporate partners such as UPS Foundation support specialized and last-mile deployments. These players concentrate on fragile regions and coordinated public-private response models. High capital requirements, emergency readiness standards, and contractual complexity limit new entrants. However, digital-native platforms are entering through cloud-based coordination and inventory visibility tools. Strategic alliances, technology partnerships, and selective acquisitions are expected to gradually increase consolidation across the sector.

Key Industry Developments

- In January 2026, the Food and Agriculture Organization (FAO) launched a US$ 2.5 billion Global Emergency and Resilience Appeal covering 54 countries. The initiative strengthens coordinated humanitarian logistics, rapid deployment systems, and supply chain preparedness across climate-vulnerable regions.

- In October 2025, the Chinese central government allocated approximately CNY 484 million (around US$ 68 million) for disaster relief across seven provinces. The funding supports agrarian risk mitigation and enhances regional logistics and emergency distribution networks.

- In June 2025, the World Bank approved a US$ 250 million financing package for Lebanon under the Lebanon Emergency Assistance Project (LEAP) to repair critical infrastructure, restore lifeline services, and manage rubble in conflict-affected areas, forming part of a scalable US$ 1 billion recovery framework to support long-term reconstruction.

Companies Covered in Disaster Relief Logistics Market

- DHL Group

- Kuehne+Nagel

- FedEx Corporation

- United Parcel Service

- Maersk

- DB Schenker

- Agility Logistics

- CEVA Logistics

- XPO Logistics

- Rhenus Group

- Crowley Maritime

- AmerisourceBergen

Frequently Asked Questions

The global disaster relief logistics market is projected to reach US$ 7.6 billion in 2026.

Rising climate-related disasters, expanding humanitarian budgets, and digital transformation of emergency supply chains drive market growth.

The market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Technology-enabled last-mile delivery, emerging market infrastructure modernization, and public-private partnerships can create significant growth opportunities.

DHL Group, Kuehne+Nagel, DB Schenker, FedEx, and UPS are among the key players operating in this market.