- Hardware & Software IT Services

- Cloud Logistics Market

Cloud Logistics Market Size, Share, and Growth Forecast 2026 - 2033

Cloud Logistics Market by Service Type (Public, Private, Hybrid, Multi), by OS Type (Native, Web-based), by Enterprise Size (Small and Medium Enterprises, Large Enterprise), by End-use Industry (Consumer Electronics, Healthcare, Automotive, Food & Beverage, Other), by Regional Analysis, 2026 - 2033

Cloud Logistics Market Size and Trend Analysis

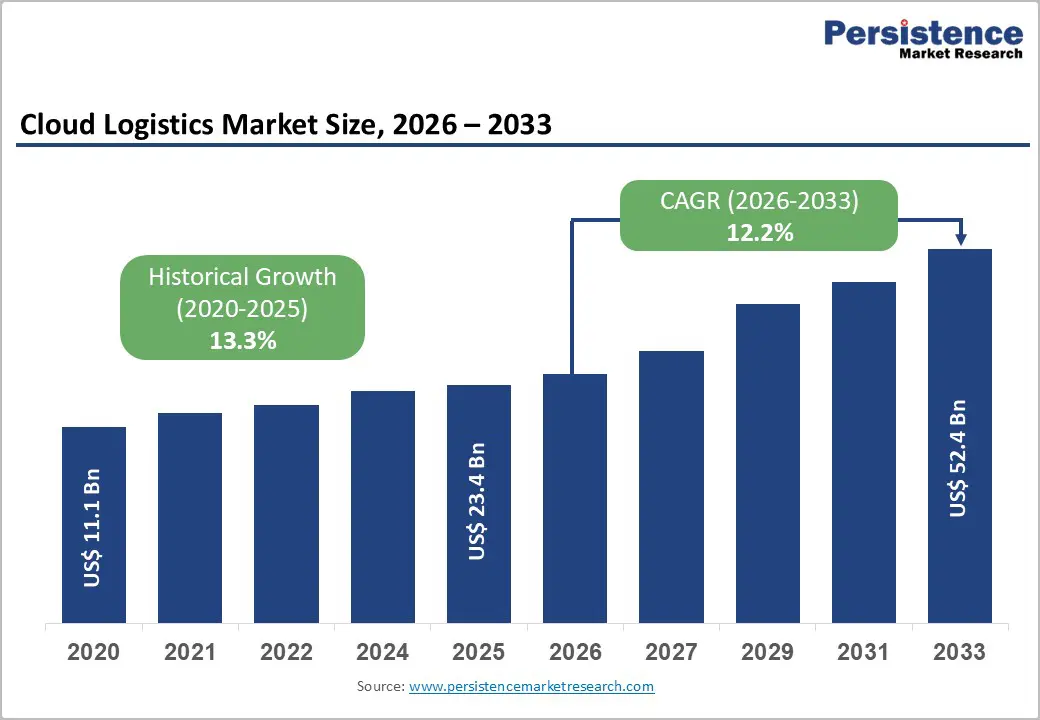

The global cloud logistics market size is expected to be valued at US$ 23.4 billion in 2026 and projected to reach US$ 52.4 billion by 2033, growing at a CAGR of 12.2% between 2026 and 2033.

The exponential acceleration of digital transformation across enterprises, combined with the escalating growth of e-commerce and the demand for real-time supply chain visibility, represents the primary market catalyst. Cloud logistics platforms enable the seamless integration of transportation management systems, warehouse automation, and demand forecasting capabilities across globally dispersed operations. Notably, 21% of supply chain executives have implemented cloud-based solutions across their entire processes. The convergence of increasing supply chain complexity, regulatory compliance requirements, and shorter delivery timelines is compelling organizations to transition from legacy on-premises infrastructure to scalable cloud-based platforms.

Key Industry Highlights:

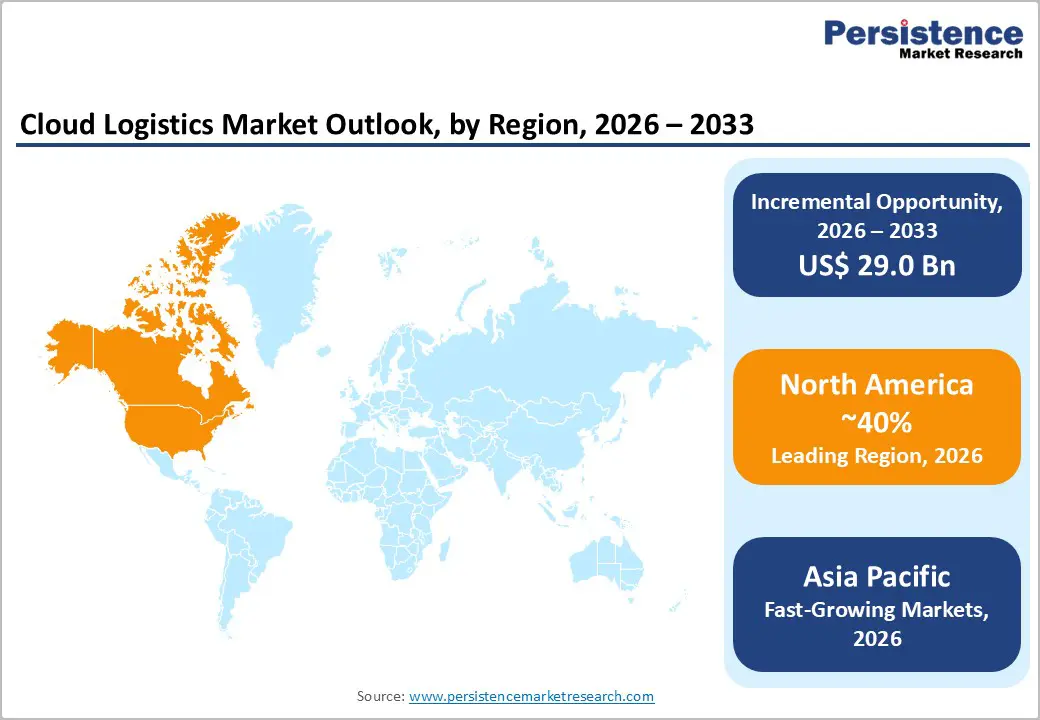

- Leading Region: North America commands the largest regional market share of approximately 40% in 2025, driven by mature cloud infrastructure, substantial enterprise technology investments, concentration of 3PL companies, and innovative cloud service providers.

- Emerging Region: Asia Pacific represents the fastest-growing regional market, expanding at approximately 17% CAGR through 2033, propelled by rapid industrialization in China and India, explosive e-commerce expansion, and accelerating digital transformation across manufacturing and logistics sectors.

- Dominant Segment: Public cloud services dominate the market segment, commanding approximately 54% market share in 2025, reflecting widespread adoption of cost-effective, scalable multi-tenant platforms including AWS, Microsoft Azure, and Google Cloud by diverse enterprise and SME users.

- Fastest Growing Segment: Native applications represent the fastest-growing category at approximately 15% CAGR, driven by containerization technologies including Docker and Kubernetes deployment demand.

- Key opportunity: Healthcare sector cloud logistics represents the fastest-growing end-use industry, expanding at approximately 17% CAGR through 2033, driven by stringent regulatory compliance requirements, temperature-controlled transportation needs, pharmaceutical supply chain integrity, and real-time traceability mandates.

| Key Insights | Details |

|---|---|

| Cloud Logistics Market Size (2026E) | US$ 23.4 billion |

| Market Value Forecast (2033F) | US$ 52.4 billion |

| Projected Growth CAGR (2026 - 2033) | 12.2% |

| Historical Market Growth (2020 - 2025) | 13.3% |

Market Dynamics

Drivers - Rise in E-Commerce Expansion and Demand for Supply Chain Visibility

The explosive growth of e-commerce activities worldwide is fundamentally reshaping logistics infrastructure requirements, with cloud-based solutions becoming essential for managing unprecedented order volumes and complexity. Global e-commerce sales exceeded US$ 5.8 trillion in 2024, requiring sophisticated logistics platforms capable of managing omnichannel fulfillment, real-time inventory visibility, and dynamic routing optimization across multiple distribution channels. Cloud logistics platforms enable retailers to integrate warehouse management systems, transportation management systems, and order management capabilities into unified operational ecosystems supporting seamless customer experiences.

Companies deploying cloud logistics solutions achieve 26% improvements in demand forecast accuracy, 16% reduction in operating costs, and 5% revenue growth increases, compelling additional enterprise adoption. Shopify’s ability to process 3.6 million transactions per minute during Black Friday 2024 demonstrates cloud infrastructure scalability essential for managing seasonal demand spikes. The integration of real-time tracking capabilities enables consumers to monitor delivery status and estimated arrival times in real-time, significantly enhancing customer satisfaction. This convergence of e-commerce growth, consumer expectations for transparency, and operational efficiency requirements is driving rapid cloud logistics adoption across retail, direct-to-consumer, and marketplace sectors.

Integration of Artificial Intelligence and Predictive Analytics Capabilities

Advanced artificial intelligence and machine learning algorithms integrated into cloud logistics platforms are revolutionizing supply chain planning, enabling predictive analytics for demand forecasting, route optimization, and risk management. IBM Consulting Supply Chain Ensemble on AWS exemplifies enterprise-grade AI integration, incorporating cognitive classifiers for intelligent data mapping, anomaly detection, and predictive modeling across 1,000+ data entities supporting 100+ supply chain use cases. Cloud platforms enable organizations to leverage IoT sensor data, RFID tracking information, and real-time traffic conditions to dynamically optimize transportation routes, reducing fuel consumption and delivery times.

Oracle Transportation Management has integrated machine learning models analyzing historical transportation data and current risk factors including port congestion and weather disruptions to provide alternative delivery route recommendations. The FDA’s OpenFDA platform demonstrates cloud-enabled analytics for food safety monitoring, enabling real-time compliance tracking and contamination detection across supply chains. Industry survey highlights 97% of companies deploying cloud logistics have at least 75% of supply chains operating in cloud environments, validating AI-powered analytics effectiveness in improving operational decision-making.

Restraints - Data Security, Privacy Concerns, and Compliance Complexity

Data security and privacy represent paramount concerns impeding cloud logistics adoption, particularly among enterprises managing sensitive supply chain information and operating in highly regulated industries. SMEs report substantial hesitation regarding cloud adoption due to perceived vulnerabilities including data breaches, account hijacking, inadequate encryption protocols, and exploited system vulnerabilities. Regulatory compliance requirements including GDPR, HIPAA for healthcare, and FDA regulations for food and beverage sectors require organizations to implement robust data governance frameworks, encryption protocols, and audit trails that increase implementation complexity and total cost of ownership.

The permanent data loss risk associated with cloud migrations, combined with multi-tenancy security concerns in shared cloud environments, creates organizational hesitation particularly among enterprises with mission-critical logistics operations. Vendor lock-in concerns regarding proprietary data formats and API restrictions further constrain cloud adoption among risk-averse organizations preferring infrastructure independence.

High Implementation Costs and Expertise Gaps

Substantial capital investments required for cloud migration, system integration, and personnel training create significant barriers particularly for small and medium-sized enterprises operating with constrained technology budgets. The integration complexity associated with connecting legacy on-premises logistics systems to cloud platforms requires specialized technical expertise increasingly scarce in regional markets. SMEs report difficulty acquiring cloud computing infrastructure, implementing communication networks, and developing strategic partnerships with cloud providers, creating financial and operational hurdles to adoption.

Training requirements for existing personnel necessitate substantial investment in skill development and change management initiatives, creating additional total cost of ownership barriers. Organizations frequently encounter difficulty recruiting and retaining personnel with cloud architecture, data integration, and cybersecurity expertise, particularly in developing regions.

Opportunity - Rapid Growth of Small and Medium-Sized Enterprise Cloud Adoption

Exceptional market opportunities exist in expanding cloud logistics adoption among SMEs, representing the fastest-growing enterprise segment at approximately 15% CAGR through 2033, compared to 13% growth for large enterprises. SMEs represent approximately 99% of businesses globally and employ approximately 70% of the global workforce, creating substantial addressable market opportunity. Cloud-based solutions eliminate prohibitive capital infrastructure investments required for traditional on-premises systems, enabling SMEs to access enterprise-grade logistics capabilities at substantially reduced costs through subscription-based pricing models.

The convergence of decreasing cloud service costs, simplified deployment architectures, and increased vendor attention to SME market segments is accelerating adoption. Descartes Systems Group acquisition of 3GTMS for US$ 115 million exemplifies industry consolidation focused on expanding SME customer reach through cloud-native platforms enabling easy integration with existing freight management systems.

Expansion of Industry-Specific Cloud Solutions and Vertical Integration

Substantial opportunities exist in developing and deploying industry-specific cloud logistics solutions tailored to unique requirements within healthcare, automotive, food and beverage, and consumer electronics sectors. Healthcare logistics presents compelling opportunities for specialized cloud platforms addressing HIPAA compliance, temperature-controlled transportation tracking, and pharmaceutical supply chain integrity monitoring. Nestlé’s 18% logistics cost reduction through cloud platform integration demonstrates food and beverage sector potential, with cloud-enabled demand forecasting, supplier collaboration, and route optimization creating significant value.

Automotive industry cloud logistics platforms can integrate supplier communication, just-in-time inventory management, and production scheduling across global supply networks. Vertical-specific regulatory expertise, domain-specific workflows, and industry best practices create differentiation opportunities for vendors developing tailored solutions addressing sector-unique requirements including traceability, compliance, and real-time monitoring capabilities.

Category-wise Analysis

Service Type Insights

Public cloud logistics services dominate the market, commanding approximately 54% market share in 2025, driven by cost-effective multi-tenant platforms from providers such as AWS, Microsoft Azure, and Google Cloud Platform. Public cloud solutions offer rapid deployment, scalability aligned with logistics demand fluctuations, and reduced operational burden through vendor-managed infrastructure, security, and maintenance. The 75% projected cloud adoption rate by 2026 reflects continued preference for public cloud services due to low upfront costs and operational flexibility.

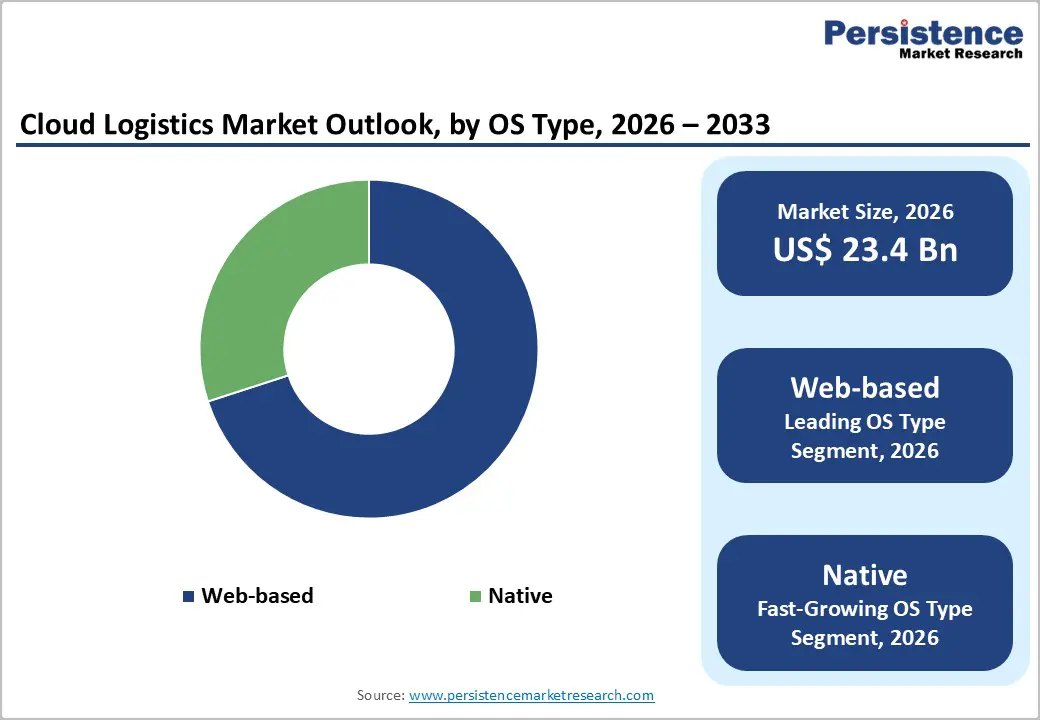

OS Type Insights

Web-based cloud logistics platforms dominate the market, commanding approximately 70% market share in 2025, enabling users to access systems through standard internet browsers without requiring local software installation or maintenance. Web-based architectures provide exceptional accessibility, enabling supply chain stakeholders including vendors, logistics providers, and customers to access real-time visibility information from any location with internet connectivity.

Native cloud-based applications represent the fastest-growing OS category, expanding at approximately 15% CAGR through 2033, as organizations increasingly prioritize performance optimization, offline capabilities, and seamless platform integration through native containerized architectures including Docker and Kubernetes. AKS users report 60% reduction in critical priority incidents and 50% cost reduction compared to virtual machine-based architectures, validating native cloud application benefits for mission-critical logistics operations.

Enterprise Size Insights

Large enterprises dominate the cloud logistics market, commanding approximately 67% market share in 2025, reflecting substantial capital availability, sophisticated technology infrastructure, and complex global supply chains justifying premium cloud logistics investments. Large organizations benefit from enterprise-grade platform capabilities including advanced analytics, artificial intelligence integration, and multi-entity consolidation features supporting complex supply chain requirements.

Industry Insights

Consumer Electronics represents the dominant end-use industry segment, commanding approximately 37% market share in 2025, driven by complex global supply chains, rapid product lifecycles, and demand for real-time component tracking and inventory visibility. Consumer electronics manufacturers including Apple, Samsung, and Sony maintain sophisticated global supply networks requiring cloud-enabled coordination across multiple suppliers, manufacturing facilities, and distribution channels.

Regional Insights

North America Cloud Logistics Market Trends and Insights

North America maintains dominant market position, commanding approximately 40% market share in 2025, driven by substantial enterprise technology investments, advanced digital infrastructure, and concentration of leading cloud service providers including AWS, Microsoft Azure, and IBM. The United States represents dominant 85% share of North American market value, supported by mature cloud computing adoption, extensive 3PL ecosystem, and regulatory frameworks supporting digital transformation including FDA compliance requirements and GDPR equivalents.

The region benefits from robust innovation hubs in Silicon Valley, Seattle, and Boston, attracting venture capital and fostering continuous product development. Leading enterprises such as Walmart, Amazon, FedEx, and UPS have implemented sophisticated cloud logistics solutions, setting industry benchmarks for adoption. Favorable policies promoting automation, digital documentation, and trade compliance under USMCA enhance market growth. The presence of prominent 3PL providers, freight forwarders, and technology-driven logistics firms further stimulates competitive innovation, encouraging adoption of advanced cloud-based supply chain visibility, predictive analytics, and operational efficiency solutions across the region.

Europe Cloud Logistics Market Trends and Insights

Europe represents significant share of global cloud logistics market in 2025, with market expansion driven by stringent EU Detergent Regulation, GDPR compliance requirements, and regulatory support for digital supply chain transformation. Germany, France, and the Netherlands lead European adoption, with major investments in integrated cloud-based transportation and warehouse management systems. UK market expansion continues despite Brexit, with regulatory harmonization initiatives supporting cloud logistics adoption across member states.

European enterprises prioritize sustainability, with cloud-enabled green logistics optimization, carbon-neutral freight networks, and eco-optimized route planning representing significant competitive differentiators. The UK market projects approximately 11.8% CAGR growth through 2032, driven by regulatory compliance requirements and competitive pressure. Major logistics providers including Maersk, DB Schenker, and DPD have substantially increased cloud infrastructure investments supporting seamless cross-border operations and real-time visibility across European supply networks. European emphasis on data privacy and local data residency creates opportunities for EU-compliant cloud providers offering regional data center infrastructure.

Asia Pacific Cloud Logistics Market Trends and Insights

Asia Pacific represents the fastest-growing regional market, projected to expand at approximately 17% CAGR through 2033, driven by rapid industrialization, explosive e-commerce expansion, and increasing adoption of digital technologies across China, India, Japan, and Southeast Asian nations. China dominates Asia Pacific market with government digital transformation initiatives, Alibaba ecosystem, and manufacturing sector sophistication driving adoption. India’s rapidly urbanizing economy, accelerating e-commerce penetration, and increasing logistics sector digitalization create substantial growth opportunities.

Japan and South Korea maintain mature, sophisticated cloud logistics markets with exceptional technology adoption rates and an emphasis on supply chain efficiency. The region’s manufacturing advantages, cost-effective cloud infrastructure, and emerging logistics technology startups position Asia Pacific as a growth engine for the global cloud logistics market. The ASEAN region’s expanding cross-border e-commerce ecosystem creates compelling demand for cloud-enabled supply chain visibility and multi-country compliance tracking.

Competitive Landscape

The cloud logistics market exhibits a moderately consolidated competitive structure, with established enterprise software vendors coexisting alongside specialized logistics technology providers and agile cloud-native startups. Leading platforms command significant market share through comprehensive software portfolios, long-standing client relationships, and substantial R&D investments, enabling end-to-end supply chain visibility, predictive analytics, and multimodal logistics management. Specialized providers differentiate themselves through focused product development, deep industry expertise, and strategic partnerships with carriers, 3PLs, and shippers to enhance transportation management and operational efficiency.

Industry consolidation, including acquisitions and strategic alliances, reflects efforts to expand geographic reach, integrate advanced capabilities, and strengthen service offerings. Cloud-native startups are disrupting traditional logistics with user-friendly interfaces, technology-first approaches, and venture-backed growth, targeting niche segments and SMEs. Across the market, competitive strategies increasingly emphasize AI and machine learning integration, IoT-enabled monitoring, real-time supply chain visibility, and tailored solutions for industry-specific logistics challenges, fostering differentiation and long-term customer retention.

Key Market Developments:

- October 2023: IBM Consulting launched Supply Chain Ensemble on AWS, a no-license, modular framework co-created with AWS. It integrates AI, generative AI, and real-time analytics for end-to-end supply chain visibility, agility, and collaborative risk management.

- March 2025: Descartes Systems Group completed the acquisition of 3GTMS, expanding the carrier network and offering enhanced tools for shippers and logistics providers managing truckload, LTL, and parcel shipments across North America through an integrated cloud platform.

- December 2025: Amazon announced an additional investment of over $35 billion in India by 2030, focusing on cloud infrastructure, e-commerce, logistics, AI, and SME technology. This brings the total commitment to $75 billion, aiming to empower 15 million small businesses and create one million jobs.

- December 2025: IFS announced a definitive agreement to acquire Softeon, a leading provider of cloud-native Warehouse Management, Execution, and Distributed Order Management solutions. The move extends IFS's Industrial AI into warehouse operations, integrating manufacturing with intelligent automation, robotics, and labor optimization

Companies Covered in Cloud Logistics Market

- BWISE

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Thomson Reuters

- Trimble

- Uber Freight

- The Descartes Systems Group Inc

- C.H. Robinson Worldwide Inc.

- MetricStream

- 3Gtms LLC

- CargoSmart Limited

- e2open LLC

- ShipBob Inc.

- Flexport

- Convoy

- Project44

- Magaya

- Cogoport

Frequently Asked Questions

The Cloud Logistics Market is projected to reach US$ 23.4 billion in 2026.

Demand is driven by rapid e-commerce growth, real-time supply chain visibility needs, and increasing adoption of AI-enabled cloud platforms.

North America is expected to retain the largest regional market share due to strong cloud infrastructure and enterprise adoption.

Major opportunities include rising adoption among SMEs and industry-specific cloud solutions for sectors such as healthcare and automotive.

Leading market participants include e2open, IBM Corporation, Oracle Corporation, Descartes Systems Group, SAP SE, etc.