- Industrial Machinery

- Glass Reactor Market

Glass Reactor Market Size, Share, and Growth Forecast, 2026-2033

Glass Reactor Market by Product Type (Single-Layer, Double-Layer, Triple-Layer, Photochemical, High-Pressure), Material (Borosilicate, Quartz, Fluoropolymer-Lined, Specialty Glass), End-Use (Pharma & Biotech, Chemicals, Petrochemicals, Food & Beverage, Research Labs), and Regional Analysis for 2026-2033

Glass Reactor Market Share and Trends Analysis

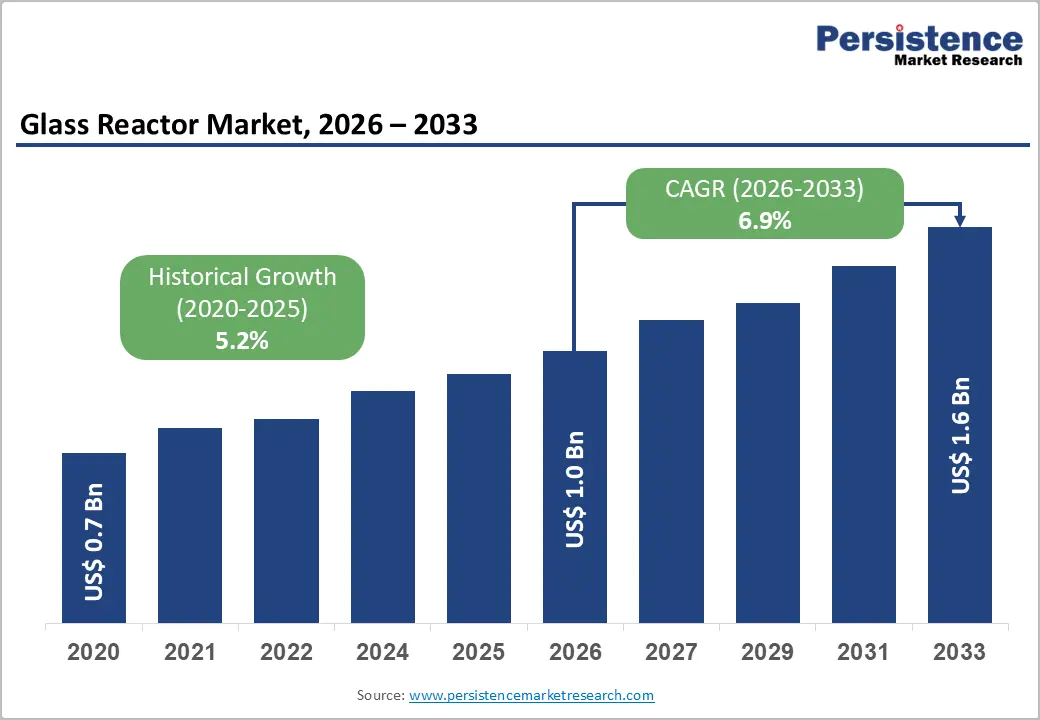

The global glass reactor market size is likely to be valued at US$ 1.0 billion in 2026, and is projected to reach US$ 1.6 billion by 2033, growing at a CAGR of 6.9% during the forecast period 2026–2033. The demand for glass reactors is primarily driven by the expanding activities in pharmaceutical and chemical synthesis, where high-purity, corrosion-resistant vessels are essential for safe and efficient production. Researchers and manufacturers increasingly require real-time reaction visibility to monitor complex processes and ensure consistent product quality. Technological upgrades, including the integration of automation, modular flow systems, and digital control interfaces, are enabling broader adoption across laboratories, pilot plants, and small-scale production facilities. Despite these advantages, high upfront costs, maintenance requirements, and the inherent fragility of glass constrain adoption in certain industrial segments. Emerging markets in the Asia Pacific and advancements in smart, connected reactor technologies offer significant growth potential.

Key Industry Highlights

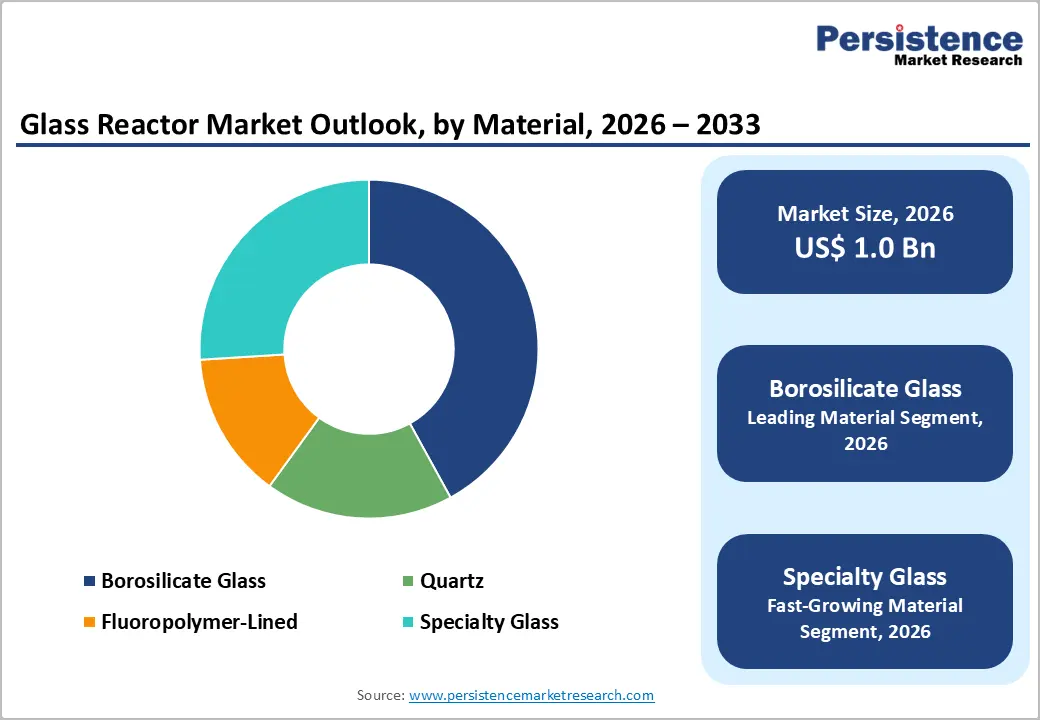

- Top Segments: Pharma & biotech is set to lead with an estimated 35% revenue share in 2026, while borosilicate materials are expected to capture 42% share, reflecting broad usage and thermal reliability.

- Fastest Growth: Photochemical reactors, specialty glass materials, and research lab end-use categories are forecasted as the fastest-growing segments through 2033, driven by specialized chemistries and modular flexibility.

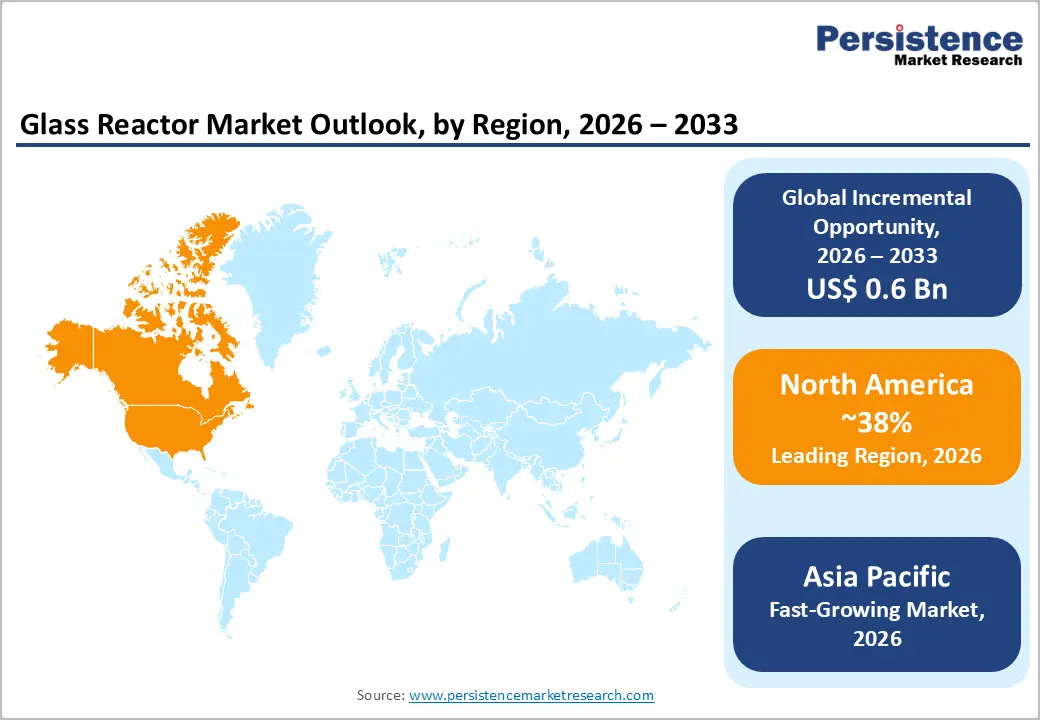

- Regional Leadership: North America is poised to lead with 38% market share in 2026, while the Asia Pacific market is projected to register the fastest CAGR at about 7.8%, driven by pharmaceutical and chemical manufacturing expansion.

- Competitive Environment: Strategic moves include Asia Pacific facility expansions, modular reactor launches, and deployment of data-integrated systems to strengthen regional presence and technological differentiation.

| Key Insights | Details |

|---|---|

| Glass Reactor Market Size (2026E) | US$ 1.0 Bn |

| Market Value Forecast (2033F) | US$ 1.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Pharmaceutical & Biotech Reactions Demand

The pharmaceutical and biotech industry is a key demand driver for glass reactors due to the need for strict purity, contamination control, and visual inspection during active pharmaceutical ingredient (API) synthesis and biologics process development. Around 45% of global installations are linked to pharmaceutical production and R&D, reflecting the importance of controlled laboratory and pilot environments. Sustained clinical trials and growing pipeline molecules have further expanded pilot plant and lab requirements. Companies increasingly prioritize scalable reactor solutions to reduce cycle times and maintain quality across multiple product lines.

In 2025–2026, AbbVie, a leading U.S. pharmaceutical company, announced a US$ 380 million investment to build two new API manufacturing facilities at its North Chicago campus to bolster domestic production capacity using advanced manufacturing technologies and AI enabled systems. This expansion supports the broader industry shift toward high-precision synthesis and localized production. The move directly reinforces demand for glass reactors capable of precise temperature and pressure control, supporting pilot-scale experimentation and multi-step synthesis processes under stringent GMP compliance.

Process Visibility & Chemical Resistance Requirements

Glass reactors provide unmatched visual monitoring and chemical inertness compared with metal alternatives, allowing operators to observe reaction phases in real time and minimize contamination risks. Sectors such as specialty chemicals and fine chemicals increasingly rely on these reactors for rapid process changeovers and efficient handling of multiple reaction types with minimal residue carryover. Their transparency also facilitates operator training and ensures better reproducibility across scale-up processes, which is critical in both research labs and pilot manufacturing.

The chemical and pharmaceutical producers have accelerated adoption of continuous processing and process intensification technologies that depend on real time monitoring and tight thermal control. Industry analyses highlight that continuous flow systems and advanced automation are becoming standard drivers for safer, more efficient syntheses. The superior corrosion resistance and thermal stability of glass reactors further enhance reaction reliability, reduce product rejection rates, and support faster experimental throughput in R&D and specialty chemical operations.

High Initial & Lifecycle Costs

Glass reactors generally require significant capital investment, particularly for sophisticated multi acketed units with integrated automation and digital control systems. Advanced systems can cost 40–60% more than comparable metal reactors, creating budgetary barriers for small and medium enterprises (SMEs), academic institutions, and small scale pilot plants. High upfront costs often limit rapid adoption despite clear operational benefits. Specialized installation, calibration, and operator training add to upfront expenditures and extend implementation timelines. This cost sensitivity often forces facilities to prioritize core production investments over advanced equipment procurement.

Budget constraints have been amplified by broader research funding challenges that emerged in past years. U.S. universities such as Stanford and the University of North Carolina paused major research construction projects and reduced discretionary spending in response to federal funding uncertainties and cuts, illustrating how tight budgets can delay or cancel capital equipment investments. These developments have made research institutions more cautious about committing to high cost reactors, reinforcing cost sensitivity as a key restraint on glass reactor adoption and innovation deployment.

Material Fragility and Operational Limitations

The inherent fragility of glass limits its mechanical strength under rapid thermal cycling, extreme temperature changes, or high pressure conditions, making it less suitable for aggressive industrial processes. Even minor thermal shocks or physical impacts can cause fractures, posing significant safety risks, downtime, and equipment replacement costs. These limitations require additional protective infrastructure, such as secondary containment and reinforced supports, increasing overall complexity for high intensity applications. Highly skilled operators and strict maintenance protocols are necessary to mitigate fracture risk, elevating operational demands.

Operational fragility has drawn regulatory and safety focus. For example, several universities and research settings in the U.S. reported tightened safety reviews and budget freezes tied to pressure system risks and federal funding uncertainties, leading to caution around high pressure glass equipment purchases and installation. These safety and operational concerns were highlighted when institutions slowed lab expansions and updated risk assessments for high pressure equipment, underlining that material limitations and safety vulnerabilities remain a constraint on glass reactor adoption in industrial and academic contexts.

Modular & Continuous Flow Reactor Expansion

Demand continues to rise for modular, customizable glass reactor systems that support both batch and continuous operations, particularly among contract development and manufacturing organizations (CDMOs) and specialty chemical producers seeking improved flexibility. Modular designs allow rapid reconfiguration for diverse reaction sequences and pilot workflows, supporting evolving production needs in R&D and smaller manufacturing units. These systems reduce setup and changeover times while improving reproducibility, which accelerates process development and scale up timelines. As manufacturers focus on agility, reactors with plug and play features become more attractive. Adoption also benefits labs aiming to optimize throughput without massive capital investments.

The industry operations have placed heightened emphasis on continuous flow manufacturing to enhance efficiency and quality in chemical and pharmaceutical production, as noted in analyses of flow chemistry applications that highlight its role in safer, more sustainable processes. This trend, supported by regulatory encouragement for process intensification and operational efficiency, underscores how continuous flow and modular reactor solutions can deliver tangible benefits in precision, energy usage, and waste reduction, making them increasingly strategic for modern chemical workflows.

Emerging Market Penetration & Localized Manufacturing

Emerging economies in Asia Pacific, particularly India and China, are driving strong expansion in chemical manufacturing and pharmaceutical production, creating robust demand for glass reactors across R&D and pilot production. Government incentives, infrastructure initiatives, and export oriented strategies are boosting domestic production capacity, improving access to advanced processing equipment. In India, expanding specialty chemical and pharma output is supported by policy frameworks aimed at attracting investment and improving local manufacturing capabilities. These structural shifts encourage technology adoption and local ecosystem development for high quality reactor systems.

India’s chemical and pharmaceutical sectors have shown notable growth momentum, with government plans to broaden production-linked incentive (PLI) applications for bulk drug and specialty chemical manufacturing and support export competitiveness. Initiatives to strengthen domestic manufacturing contours and streamline technology uptake in these regions are shortening delivery lead times and improving service support. Combined with global trade realignments favoring diversification, these developments are unlocking glass reactor adoption among mid tier producers and startup labs seeking localized, efficient solutions.

Category-wise Analysis

Material Insights

Borosilicate glass are likely to lead material adoption with an estimated 42% of the glass reactor market revenue share in 2026, due to its excellent chemical resistance, thermal stability, and compatibility across pharmaceutical, fine chemical, and biotech applications where contamination control and visual monitoring are critical. Its robustness ensures enhanced batch reproducibility, operational reliability, and seamless integration with automated control systems, reducing process variability and downtime. The regional access improved through supply chain expansions, exemplified by a new high tech borosilicate tubing facility near Hyderabad, India, inaugurated by Corning and SGD Pharma, producing 13,000 tons of Type 1 borosilicate annually to support pharmaceutical and biotech manufacturing. This development highlights both material demand growth and strategic regional sourcing advantages.

Specialty glass reactors are projected to the fastest-growing material segment, projected to expand at 8.3% CAGR through 2033, driven by the need to handle highly corrosive media and extreme pH chemistries in fine chemicals and research-intensive applications. Their superior inertness and reduced contamination risk make them ideal for modular, continuous-flow, and automated setups, enabling safer, high-purity reactions. The adoption increased with the opening of Jubilant Biosys’ discovery and preclinical facility in Noida, featuring pilot plants and reactors from 20 L to 250 L for early-phase chemistry and specialty synthesis. This real-world deployment underscores operational demand and growing recognition of advanced materials in research and specialty chemical production.

End-Use Insights

Pharmaceutical and biotech applications are likely to capture an estimated 35% of the glass reactor market share in 2026, driven by API production, biologics pipelines, drug discovery, and process scale-up needs. Glass reactors provide high-purity synthesis, visual monitoring, reproducible batch control, and support for complex multi-step reactions, essential in regulated production and pilot-scale operations. The expansions such as Novartis’ radioligand therapy manufacturing site in Texas highlight continued investments in high-precision reactors for both pilot and commercial production. These developments reinforce the segment’s dominance, growth trajectory, and critical role in supporting advanced pharmaceutical workflows.

Research laboratories are anticipated as the fastest-growing end-use segment, projected to grow at 9.1% CAGR through 2033, driven by flexible, analytical, and modular reactor requirements for experimental workflows and fine chemical development. Glass reactors enable rapid configuration changes, safe handling of aggressive chemistries, and high reproducibility in multi-project research pipelines.The adoption surged with investments like Jubilant Biosys’ new discovery and preclinical facility in Noida, providing modular reactors for pilot-scale chemistry and specialty synthesis. These implementations highlight the increasing importance of adaptable reactors in R&D and specialty chemical operations globally.

Regional Insights

North America Glass Reactor Market Trends

North America is predicted to command an estimated 38% of the glass reactor market value in 2026, anchored by the U.S. pharmaceutical and biotech industries, advanced R&D infrastructure, and stringent regulatory standards emphasizing quality, safety, and process compliance. Federal and state incentives supporting manufacturing modernization and pilot plant expansions encourage adoption of automated, data-integrated reactors. Aging pilot plant facilities and scale-up labs drive replacement cycles, with modern glass reactors offering improved process reproducibility, real-time monitoring, and corrosion-resistant vessels that extend operational lifespans while minimizing contamination risks.

Canada’s research and specialty chemical sectors are also advancing reactor adoption, with provincial initiatives in Ontario, British Columbia, and Quebec supporting modern laboratory upgrades for high-purity and continuous-flow processes. Industry investments in modular, plug-and-play reactor systems and digital process analytics enhance compliance and reduce operator dependency. Leading companies such as AbbVie and Novartis expanded U.S. pilot and production sites in 2025–2026, reinforcing demand for precision reactor platforms. The North America market exhibits strong competitive intensity, with both global original equipment manufacturers (OEMs) and specialized modular system providers capturing share, while modular and continuous-flow reactors emerge as the fastest-growing submarket at 6.8% CAGR through 2033.

Europe Glass Reactor Market Trends

Europe is projected to hold approximately a 30% share of the global market for glass reactors in 2026, supported by harmonized EU regulations, advanced chemical and life science sectors, and demand for corrosion-resistant, contamination-free reactors that comply with strict environmental and safety standards. Countries such as Germany, France, and the U.K. anchor regional adoption through investments in pilot plants, energy-efficient thermal control systems, and automated reactor technologies for R&D and specialty chemical production. The European manufacturers emphasized digital integration and sustainability, reinforcing premium reactor uptake across laboratories and small-scale production units.

Notable developments include Merck’s € 150 million climate-neutral pharmaceutical facility in Cork, Ireland, with advanced sterile processing capabilities, illustrating the trend toward high-quality, compliant reactor systems. European OEMs are increasingly partnering with system integrators to embed digital monitoring, process analytics, and traceability into reactor deployments, enabling regulatory adherence. Germany and France are the fastest-growing submarkets, projected at 6.2% CAGR through 2033, driven by R&D incentives, stringent process standards, and expanding pilot-scale chemical production capabilities.

Asia Pacific Glass Reactor Market Trends

Asia Pacific is projected to be the fastest-growing regional market for glass reactors, estimated to grow at 7.8% CAGR through 2033, fueled by rapid expansion of pharmaceutical and chemical manufacturing in China, India, Japan, and ASEAN nations. Rising domestic production capacities, cost competitiveness, and government support for advanced laboratory infrastructure drive glass reactor adoption for R&D, pilot plants, and small-scale production. In 2025–2026, OEMs expanded facilities, service networks, and technical support hubs to shorten lead times and facilitate rapid deployment across emerging chemical and pharmaceutical firms.

For instance, Corning and SGD Pharma inaugurated a high-tech borosilicate tubing facility near Hyderabad, India, producing 13,000 tons annually for pharmaceutical and biotech applications, demonstrating local material sourcing improvements. Strategic partnerships, localized manufacturing, and modular system offerings reduce cost and logistical barriers, boosting adoption among mid-tier chemical firms and research institutes. China and India lead regional volume growth, with continuous-flow and modular reactors driving innovation, positioning Asia Pacific as a key global growth engine for glass reactors in the coming decade.

Competitive Landscape

The global glass reactor market structure is moderately consolidated, with leading players such as Büchi Labortechnik, Parr Instrument Company, IKA Works, and HEL Group collectively controlling over half of the market revenue. These established manufacturers leverage deep relationships with pharmaceutical, biotech, and specialty chemical clients, strong regulatory knowledge, and integrated hardware-software solutions for automated, modular, and continuous-flow reactors. They continue to invest in R&D to maintain leadership in reactor automation, process monitoring, thermal management, and corrosion-resistant materials.

Regional and niche competitors, including Radleys, Syrris, and LabTech, focus on specialized applications, pilot-scale systems, and emerging markets. High technical complexity, stringent safety regulations, and the need for process validation act as barriers to new entrants. However, growing demand for digital monitoring, modular reactor platforms, and plug-and-play systems allows smaller, software-integrated providers to gain traction. Market consolidation is expected to increase gradually, as global leaders expand geographically, enhance service networks, and integrate digital solutions while partnering with specialized automation and analytics companies.

Key Industry Developments

- In February 2026, Glass Technology Services (GTS) secured funding from the United Kingdom Atomic Energy Authority (UKAEA) Fusion Industry Programme to study glass and glass-ceramic materials as radiation shielding for future fusion reactors. The project, conducted with Sheffield Hallam University, will evaluate these materials as cost-effective and sustainable alternatives.

- In February 2026, AbbVie announced a major investment to expand its North Chicago campus with two state-of-the-art API production facilities. The sites will integrate AI and advanced manufacturing technologies to enhance complex drug synthesis, supporting next-generation neuroscience and obesity medications while creating 300 new jobs.

- In August 2025, SCHOTT expanded its Jambusar plant to produce high-precision syringe and cartridge glass tubing locally, leveraging FIOLAX® borosilicate glass and advanced inspection processes. The move strengthens India’s pharmaceutical packaging capabilities and aligns with the ‘Make in India’ initiative to reduce import dependence.

Companies Covered in Glass Reactor Market

- Pfaudler

- De Dietrich Process Systems

- Büchi Labortechnik

- Chemglass Life Sciences

- Ace Glass

- Radleys

- Syrris

- GMM Pfaudler

- IKA

- Heidolph Instruments

- Buchiglas

- Sachin Industries

- Tef Engineering

- Corning

Frequently Asked Questions

The global glass reactor market is projected to reach approximately US$ 1.0 billion in 2026.

Growing pharmaceutical and chemical R&D, high-purity reaction needs, and demand for corrosion-resistant, visually monitored reactors are driving the market.

The market is poised to witness a CAGR of 6.9% from 2026 to 2033

Adoption of modular and continuous-flow reactors, and expansion in emerging Asia Pacific manufacturing hubs are opening new opportunities.

Büchi Labortechnik, Parr Instrument Company, IKA Works, HEL Group, Radleys, and Syrris, are a few among the leading companies in the market.