- Advanced Materials

- LCD Glass Substrate Market

LCD Glass Substrate Market Size, Share, and Growth Forecast, 2026 – 2033

LCD Glass Substrate Market by Product Type (Gen 5 LCD glass, Gen 6 LCD glass, Gen 7 LCD glass, Gen 8 LCD glass), Application Type (Television, Smartphone & Tablet, Laptop & Desktop, Automotive Display), and Regional Analysis for 2026 – 2033

LCD Glass Substrate Market Size and Trends Analysis

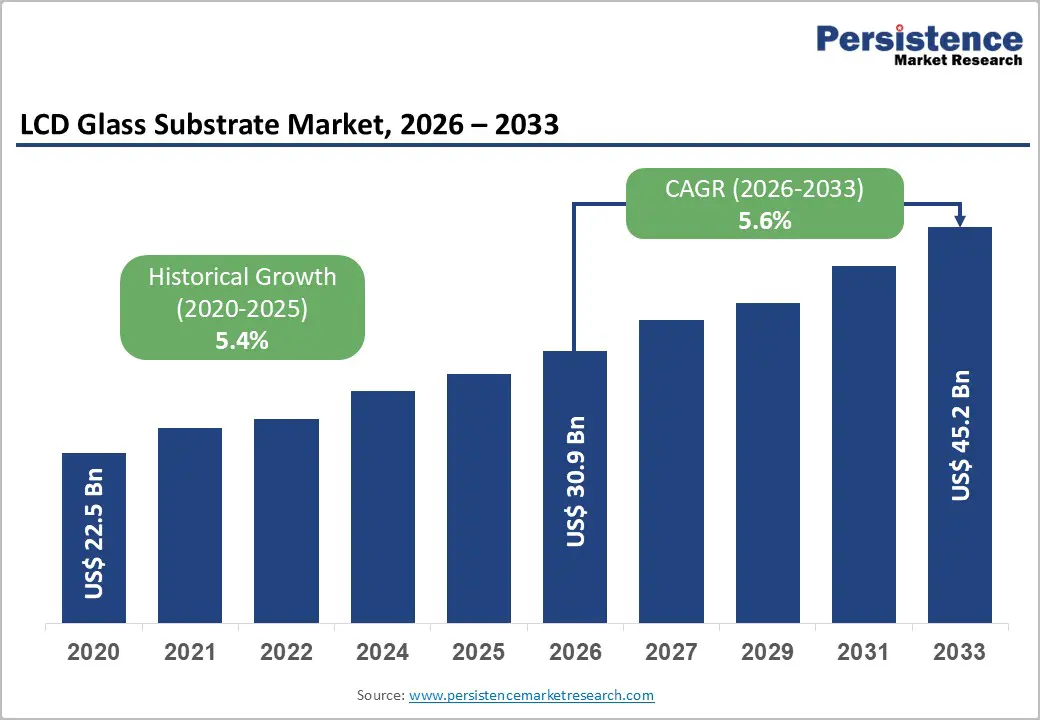

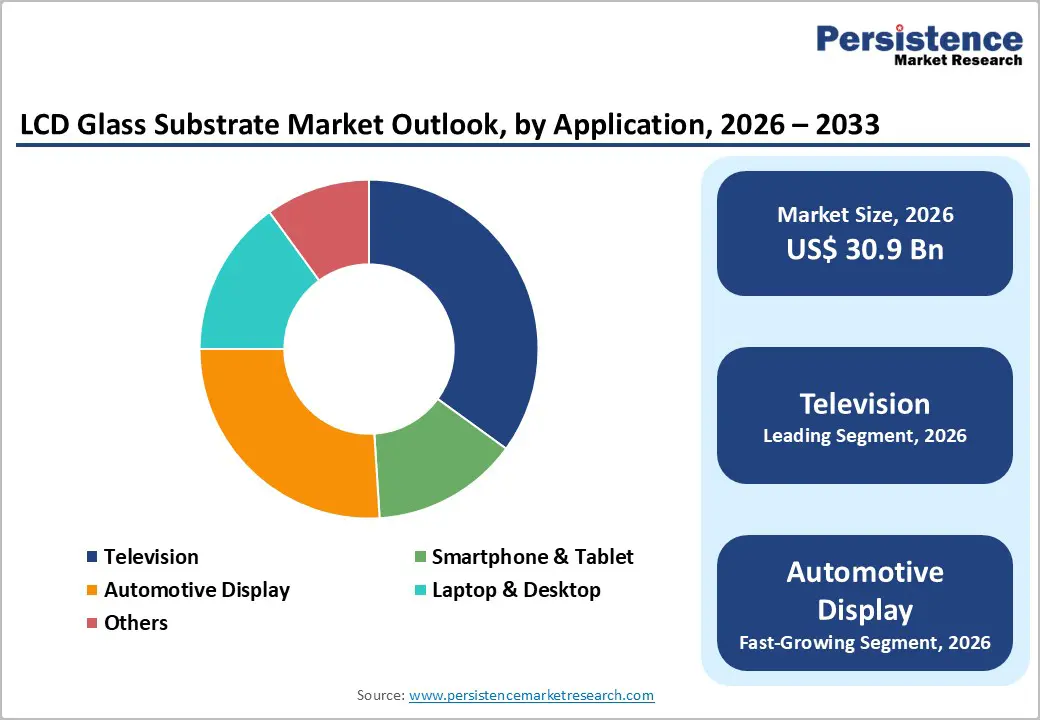

The global LCD glass substrate market size is likely to be valued at US$30.9 billion in 2026 and is expected to reach US$45.2 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by sustained demand for large-screen LCD televisions, laptops, and automotive displays, where high-quality glass substrates are critical for panel performance.

Technological advancements such as ultra-thin substrates, larger generation glass (Gen 7/8), and improved resolution compatibility are boosting manufacturing efficiency, minimizing material waste, and enhancing display quality. In emerging economies across Asia Pacific, Latin America, and the Middle East, the rapid adoption of LCD-based devices is driving an increase in shipment volumes.

Key Industry Highlights:

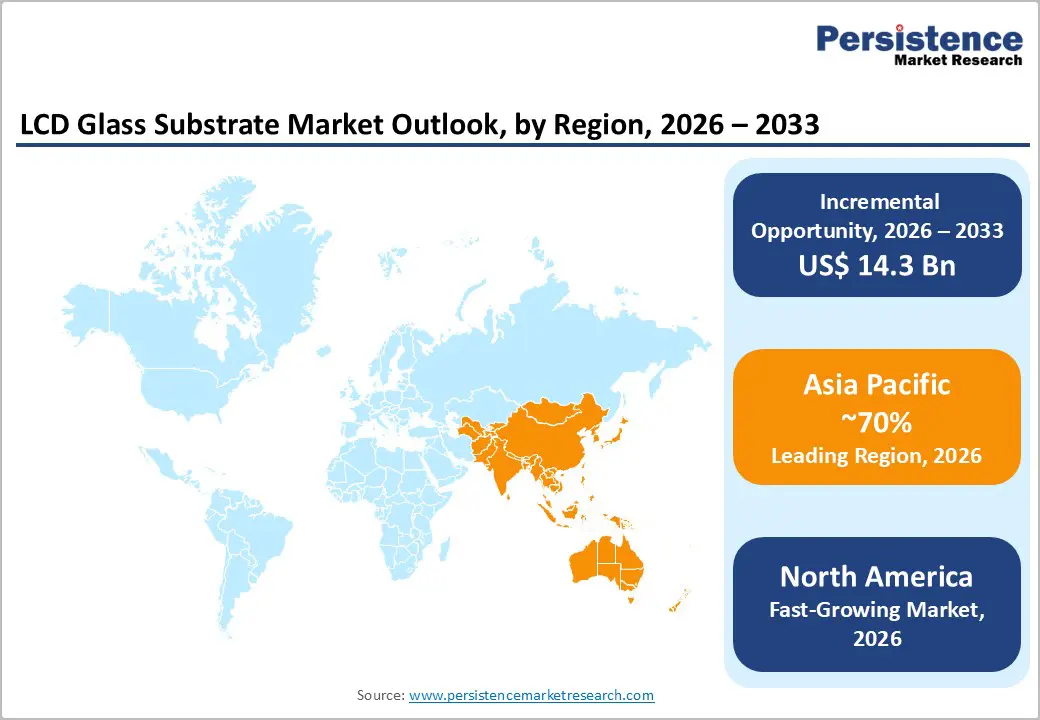

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 70% in 2026, driven by strong manufacturing capacity and high consumer demand.

- Fastest-growing Region: North America is likely to be the fastest-growing region in the LCD glass substrate in 2026, driven by strong demand in automotive and premium IT displays.

- Leading Product Type: The Gen 8 LCD glass segment is projected to represent the leading product type in 2026, accounting for 50% of the revenue share, driven by demand for ultra-large TVs and commercial displays.

- Leading Application: Television applications are anticipated to be the leading application type, accounting for over 40% of the revenue share in 2026, supported by strong demand in budget and mid-range LCD TVs.

| Report Attribute | Details |

|---|---|

|

LCD Glass Substrate Market Size (2026E) |

US$30.9 Bn |

|

Market Value Forecast (2033F) |

US$45.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Demand from Large-Format Televisions and Monitors

Consumers increasingly prefer larger screen sizes, particularly 55 inches and above, for enhanced viewing experiences in homes, offices, and commercial environments. This trend is complemented by the rising adoption of 4K and 8K resolution displays, which require high-quality, ultra-thin, and precise glass substrates to ensure panel performance and durability. Manufacturers are leveraging Gen 8 and higher LCD glass substrates to produce larger panels more efficiently, optimizing material usage and reducing production costs per unit. Asia Pacific, home to leading display manufacturers such as BOE Technology, Corning, and AGC, dominates this segment due to its high-volume production capabilities.

The commercial display sector, including digital signage, conference room monitors, and public information boards, contributes to substrate demand. Businesses prefer large-format panels for clarity and visibility, driving orders for premium glass substrates. Combined with urbanization and growing middle-class purchasing power in emerging markets, these factors collectively sustain robust demand for LCD glass substrates in large-screen TVs and monitors. Advancements in Gen 8 and higher glass substrates enable manufacturers to produce larger panels with higher yield and lower costs, meeting rising consumer and commercial expectations.

Shift toward OLED and Micro-LED Technologies

OLED and Micro-LED panels offer superior contrast ratios, richer colors, higher brightness, and the potential for flexible or foldable designs, making them increasingly attractive in premium smartphones, high-end televisions, laptops, and wearable devices. Consumers prioritize thinner, lighter, and more energy-efficient displays, and demand for traditional LCD panels and consequently LCD glass substrates faces pressure. Regions with high penetration of advanced consumer electronics, such as North America, Japan, and Western Europe, are witnessing faster adoption of OLED technology, which diverts growth away from LCD glass substrates. Micro-LED is emerging in niche applications such as large-format commercial displays and digital signage, further challenging LCD dominance in certain segments.

LCD glass manufacturers are focusing on innovation in high-generation substrates, ultra-thin glass, and large-panel production to maintain competitiveness. Advances in Gen 8 and Gen 10 substrates allow LCD producers to achieve higher yields, reduce production costs per panel, and deliver large-format TVs and monitors at affordable prices. Emerging applications such as automotive digital cockpits, industrial displays, and educational digital boards continue to rely on LCD technology due to its durability, reliability, and cost efficiency. Regional production hubs in China, South Korea, and Taiwan leverage economies of scale to sustain supply for both consumer and commercial LCD panels, offsetting some pressure from OLED and Micro-LED adoption.

Advancements in Thinner and Flexible Substrates

Manufacturers are increasingly focusing on ultra-thin substrates that reduce panel weight, improve energy efficiency, and support higher resolution displays. These substrates enable larger screen sizes, slimmer designs, and improved portability for televisions, monitors, laptops, and tablets, meeting evolving consumer preferences. Flexible substrates, in particular, open doors to curved displays, foldable panels, and integrated automotive dashboards, enhancing design versatility. With rising demand for premium home entertainment systems and digital signage in commercial spaces, these advancements allow LCD manufacturers to compete effectively with OLED and Micro-LED technologies in certain applications.

Flexible and thinner substrates support growth in emerging markets where consumers seek larger screens and innovative display formats without the premium cost of OLED panels. The automotive sector benefits significantly, as curved and flexible panels are increasingly integrated into EV cockpits, infotainment systems, and multi-display dashboards. Investments in R&D and precision manufacturing are enabling glass suppliers to achieve higher durability, scratch resistance, and thermal stability, which are critical for large-format and high-resolution displays. These advancements not only enhance the value proposition of LCD panels but also enable manufacturers to tap new applications across the industrial, commercial, and automotive sectors, sustaining long-term demand for advanced glass substrates.

Category-wise Analysis

Product Type Insights

The Gen 8 LCD glass segment is expected to lead the LCD glass substrate market, accounting for approximately 50% of the total revenue share in 2026, driven by large-panel production for televisions and monitors. These high-generation substrates enable manufacturers to maximize panel output per sheet, reducing production costs and improving efficiency in mature LCD fabs, particularly in Asia Pacific. The dominance of Gen 8 LED glass is reinforced by sustained consumer demand for large-screen televisions and commercial displays in emerging and developed markets, where cost-effective large-panel production remains critical. These substrates support high-resolution formats such as 4K and 8K, enabling better visual experiences for end-users.

Gen 8 LCD glass is also likely to represent the fastest-growing segment in 2026, driven by increasing demand for ultra-large televisions and commercial displays. Manufacturers are investing in advanced substrate lines to produce panels above 75 inches efficiently, reducing material wastage while maintaining high optical clarity. For example, Corning Incorporated supplies ultra-thin Gen 8 substrates that enable premium large-format TVs to achieve higher resolution and energy efficiency, meeting both consumer and commercial requirements. Urbanization in emerging markets and rising disposable incomes contribute to the uptake of large-screen home entertainment systems, while businesses adopt large-format displays for offices and digital signage.

Application Insights

Television is expected to dominate the market, accounting for approximately 40% of total revenue in 2026, driven by the ongoing high-volume production of large-screen LCD TVs for global markets. Major panel manufacturers, such as Innolux Corporation, produce a wide variety of TFT-LCD panels for both household and commercial television products, reflecting the steady demand for cost-effective large displays that rely on high-generation LCD glass substrates for enhanced performance and size scalability.

Innolux’s LCD panels are widely distributed to global television brands, ensuring consistent orders for substrates as the LCD TV segment remains a key component of consumer electronics, even as display technologies evolve. The use of Gen 7 and Gen 8+ substrates enables manufacturers to produce larger panels with better yield, fueling growth in both mainstream and premium TV categories.

The automotive display segment is projected to be the fastest-growing application, driven by the increasing integration of larger and more sophisticated visual interfaces in vehicles. Automotive display manufacturers such as LG Display provide advanced automotive LCD modules for digital instrument clusters, center consoles, and infotainment systems, which require high-performance LCD panels capable of functioning reliably in automotive conditions.

LG Display’s automotive LCD offerings feature enhanced brightness and wider viewing angles, essential for cockpit environments, reflecting the growing demand from automotive OEMs for premium display technologies. The rise of electric vehicles (EVs) and connected car features is further boosting demand for multi-screen dashboards, creating new opportunities for LCD glass substrate suppliers.

Regional Insights

North America LCD Glass Substrate Market Trends

North America is expected to be a key market for LCD glass substrates in 2026, driven by a wide range of display applications across consumer electronics, commercial systems, and industrial sectors. Strong demand for large-screen televisions, monitors, and automotive displays, which rely on high-quality substrates for performance and durability, is a significant factor. Televisions and computer monitors continue to be major contributors to substrate consumption, fueled by the ongoing demand for high-resolution panels in both homes and workplaces.

The growth of commercial displays for digital signage and corporate use further boosts substrate utilization. North America's focus on advanced display technologies, including thin, high-precision glass for superior visual performance, continues to drive demand as consumer expectations evolve toward better clarity and energy efficiency.

The region is also seeing a growing use of LCD substrates in automotive displays, reflecting the increasing adoption of digital cockpits in vehicles. Automotive manufacturers are integrating more sophisticated infotainment and instrument cluster displays, requiring robust, high-performance glass substrates that can endure harsh environmental conditions.

For instance, Planar Systems, Inc., a U.S.-based display manufacturer, produces a variety of large-format and specialized LCD displays for commercial, industrial, and automotive applications, underscoring North America's role in providing advanced display solutions that rely on quality glass substrates. With continued investments in R&D and innovation, these trends indicate steady regional growth for LCD glass substrates as manufacturers meet both traditional and emerging display demands.

Europe LCD Glass Substrate Market Trends

Europe is expected to be a major market for LCD glass substrates in 2026, driven by diverse end uses across automotive, industrial, and commercial sectors. The region's automotive industry, particularly in countries such as Germany and France, is increasingly incorporating advanced display systems into modern vehicles, such as digital instrument clusters and central infotainment panels. This trend is boosting demand for high-quality LCD glass substrates that meet stringent performance and durability standards. Europe’s strong industrial automation sector contributes to substrate demand, as human-machine interface (HMI) screens become more common in manufacturing plants and logistics hubs.

Europe's investment in digital infrastructure, including smart transportation systems and public information displays, further fuels the demand for larger, more reliable LCD panels. The growing use of LCD solutions tailored for automotive and specialized industrial displays, which prioritize longevity and performance in demanding environments, is also driving market growth.

For instance, Tianma Europe GmbH, based in Germany, supplies advanced TFT-LCD modules for industrial, medical, and automotive applications across Europe, showcasing how local integration and customization are shaping regional display demand and supporting the substrate market. This focus on high-value sectors highlights Europe's strength in specialized display applications, even as OLED and other technologies gain traction in consumer electronics.

Asia Pacific LCD Glass Substrate Market Trends

The Asia Pacific region is expected to lead the LCD glass substrate market, capturing a 70% share in 2026, driven by its robust manufacturing ecosystem and high-volume consumer electronics production. The region is home to key display panel manufacturing hubs in China and Japan, which significantly boost substrate consumption through extensive fabrication facilities and advanced production lines supporting Gen 8 and higher substrates for large televisions and monitors. Strong demand for smartphones, consumer laptops, and automotive display panels further accelerates substrate uptake, fueled by rising disposable incomes and rapid urbanization.

The integration of LCD glass substrates into automotive and specialized industrial displays reflects the industry's diversification beyond traditional televisions and monitors. Companies such as BOE Technology Group, a leading Chinese display manufacturer, are expanding their portfolios to include automotive LCD panels with high brightness and durability, driving demand for advanced glass substrates that meet stringent automotive quality standards. With its scale, technological expertise, and cost efficiencies, Asia Pacific remains the fastest-growing and most influential region in the LCD glass substrate market.

Competitive Landscape

The global LCD glass substrate market is moderately fragmented, shaped by the presence of several established multinational manufacturers alongside emerging regional players, all of which influence the competitive dynamics. The industry is marked by high technological intensity and significant capital investment, making scale and proprietary manufacturing processes critical competitive advantages. Leading companies have developed advanced production technologies, such as proprietary fusion draw and high-precision float processes, to create ultra-thin, high-quality glass substrates essential for large-format LCD panels used in televisions, monitors, and other display devices.

Key industry leaders, including Corning Incorporated, AGC Inc., Nippon Electric Glass (NEG), Tunghsu Optoelectronic, and IRICO Group New Energy, dominate the competitive landscape, holding the largest share of production and technological innovation. These companies compete by continually advancing ultra-thin and flexible substrates, forming strategic partnerships with major display panel manufacturers, and expanding their manufacturing capacity across regions.

Key Industry Developments:

- In July 2025, Absolics, a subsidiary of SKC, accelerated its glass substrate production ramp-up in preparation for full-scale mass production by the end of 2025. The company began prototype production at its Georgia, U.S. facility, which has an annual capacity of 12,000 square meters, and is nearing the pre-qualification stage with major customers, including AMD and Amazon Web Services (AWS). The expansion is backed by strong financial support, including US$50 million in debt financing and a $40 million manufacturing subsidy under the U.S. CHIPS Act, with further capital increases planned through a rights offering involving SKC and Applied Materials.

- In May 2025, Corning Incorporated reinforced its leadership in the LCD glass substrate market through its Gen 10.5 LCD glass manufacturing facility in Hefei, China, co-located with BOE Technology Group’s production plant. The facility enables Corning to manufacture the world’s largest TFT-grade Gen 10.5 glass substrates, designed to optimize production of 65-inch and 75-inch large-screen televisions using Corning® EAGLE XG® Slim glass. With substrate sizes of 2,940 mm × 3,370 mm, the Hefei plant supports cost-efficient large-panel manufacturing and aligns with rising global demand for large-format LCD TVs.

Companies Covered in LCD Glass Substrate Market

- Corning Incorporated

- Asahi Glass Co., Ltd. (AGC)

- Nippon Electric Glass Co., Ltd.

- Schott AG

- LG Chem

- Samsung Corning Precision Materials Co., Ltd.

- AvanStrate Inc.

- IRICO Group New Energy Company Limited

- Planar Systems, Inc.

- BOE Technology Group Co., Ltd.

- NEG (Nippon Electric Glass)

- TCL China Star Optoelectronics Technology Co., Ltd.

- Shenzhen Laibao Hi-Tech Co., Ltd.

- Hefei Xinsheng Optoelectronics Technology Co., Ltd.

- Visionox Technology Inc.

Frequently Asked Questions

The global LCD glass substrate market is projected to reach US$30.9 billion in 2026.

Rising demand for large-screen televisions, monitors, and automotive displays supported by cost-efficient, high-generation LCD panel manufacturing.

The LCD glass substrate market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

Advancements in ultra-thin and high-generation glass substrates, expanding automotive and industrial display applications, and rising demand for large-format LCD panels in emerging markets.

Corning Incorporated, Asahi Glass Co., Ltd. (AGC), Nippon Electric Glass Co., Ltd., Schott AG, LG Chem, and Samsung Corning Precision Materials Co., Ltd are the leading players.