- Energy Storage Solutions

- Flow Battery Market

Flow Battery Market Size, Share, and Growth Forecast 2026 - 2033

Flow Battery Market by Battery Type (Redox, Hybrid), by Battery Material (Vanadium, Zinc Bromine, Iron, Others), Storage Type (Small Scale below 500kW, Large Scale above 500kW), by Application (Grid/Utility, Commercial & Industrial, EV Charging Stations, Residential, Others), and Regional Analysis, 2026 - 2033

Flow Battery Market Size and Trend Analysis

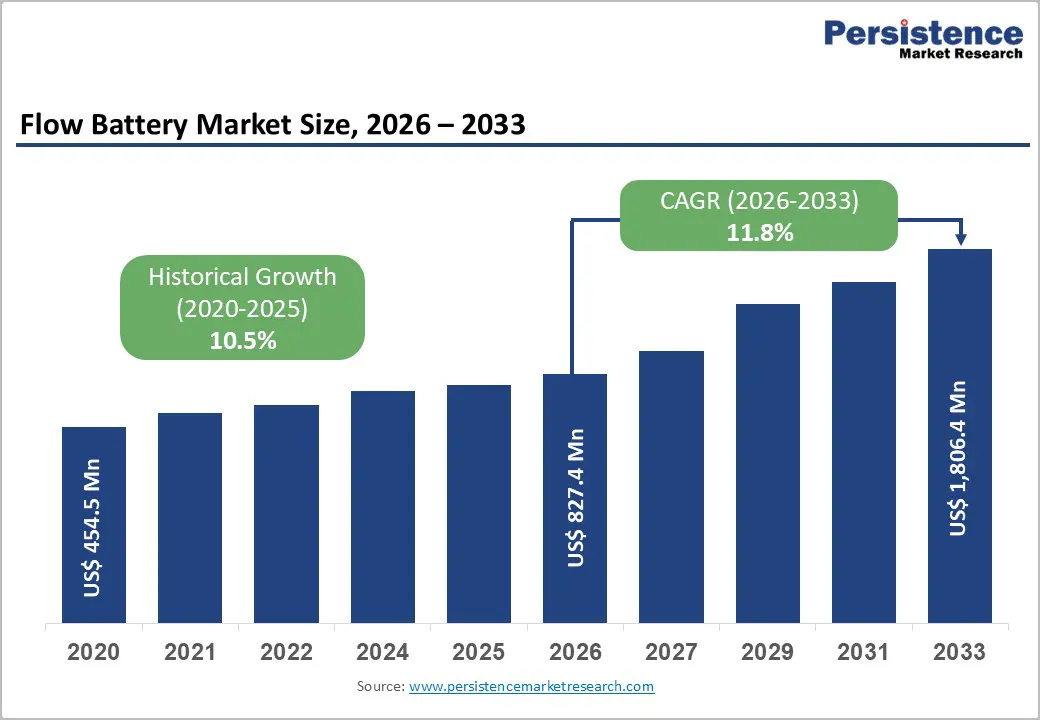

The global flow battery market size is likely to be valued at US$ 827.4 million in 2026 and projected to reach US$ 1,806.4 million by 2033, growing at a CAGR of 11.8% between 2026 and 2033.

The market’s expansion is fundamentally driven by the escalating integration of renewable energy sources such as solar and wind power, which generate electricity intermittently and require extended-duration energy storage to stabilize grid operations. As governments globally enforce increasingly stringent decarbonization mandates and invest heavily in grid modernization infrastructure, the deployment of long-duration energy storage systems has become strategically essential.

Key Industry Highlights:

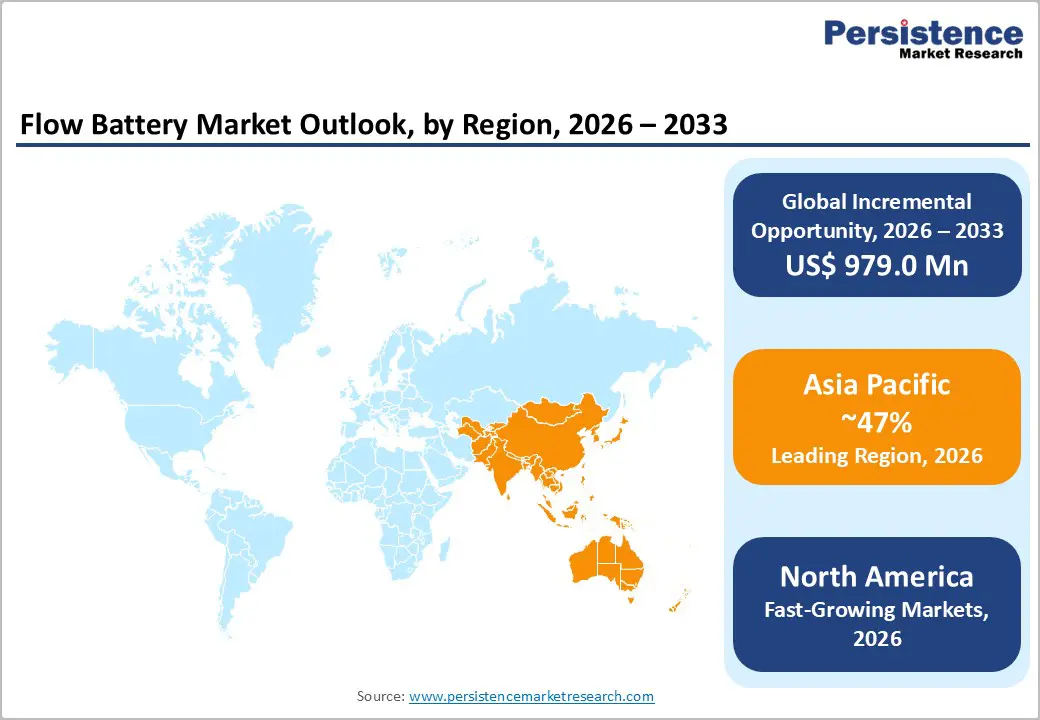

- Leading Region: Asia Pacific is the leading region in the global flow battery market with about 47% revenue share due to major utility-scale deployments and accelerating renewable integration initiatives.

- Fastest Growing Region: North America is the fastest-growing regional market for flow batteries, expanding at an estimated 18% CAGR driven by clean energy incentives and utility grid modernization investments.

- Dominant Segment: Vanadium redox flow batteries represent the dominant segment, accounting for roughly 65% of the market due to long cycle life, safety advantages, and proven commercial readiness.

- Fastest Growing Segment: Large-scale systems exceeding 500 kW capacity form the fastest-growing segment, projected to expand at about 13% CAGR, supported by increasing demand for grid services requiring multi-hour duration storage.

- Key Market Opportunity: The most significant market opportunity lies in long-duration energy storage systems enabling renewable-dominant grids targeting large-scale deployment through 2030 to enhance stability and manage intermittency.

| Key Insights | Details |

|---|---|

| Flow Battery Market Size (2026E) | US$ 827.4 million |

| Market Value Forecast (2033F) | US$ 1,806.4 million |

| Projected Growth CAGR (2026 - 2033) | 11.8% |

| Historical Market Growth (2020 - 2025) | 10.5% |

Market Dynamics

Drivers - Renewable Energy Integration and Grid Stabilization Requirements

The increasing penetration of renewable energy sources including solar photovoltaic (PV) and wind power generation, represents the primary growth catalyst for the flow battery market. Unlike conventional power plants that provide continuous baseload generation, renewable sources exhibit inherent intermittency-solar generation concentrates during midday hours while wind capacity fluctuates based on meteorological conditions. This variability creates substantial challenges for grid operators tasked with maintaining stable frequency and voltage across transmission networks.

Flow batteries, particularly vanadium redox flow battery (VRFB) systems, provide a solution through their capability to store excess renewable generation during periods of oversupply and discharge stored energy during peak demand intervals. The International Energy Agency reports that utility-scale battery storage capacity surged from 17.6 GW in 2022 to 41.5 GW in 2023, with flow batteries capturing an increasing market share. Major deployment projects, including China’s 200MW/1GWh vanadium flow battery facility in Xinjiang and Japan’s multiple 1MW × 8-hour redox flow battery installations in Kashiwazaki City, demonstrate institutional confidence in flow battery technology for grid-scale applications.

Government Support and Regulatory Framework Advancement

Supportive regulatory environments and targeted government incentives substantially accelerate flow battery market adoption. The European Union’s Net-Zero Industry Act (NZIA), adopted in May 2024, designates batteries and storage technologies as strategic net-zero technologies eligible for simplified permit procedures and manufacturing support targeted at achieving 40% domestic manufacturing capacity of net-zero technologies by 2030. The United States Department of Energy has actively promoted flow battery development, including a $2.6 million award to Quino Energy in January 2025 for developing scalable quinone redox flow batteries utilizing oil-field tanks.

India’s government has allocated USD 241 million under the PM E-DRIVE Scheme to support nationwide deployment of energy storage charging networks, creating demand for stationary energy storage systems that can support EV charging infrastructure. Additionally, viability gap funding and extended transmission charge waivers until 2028 have made standalone battery energy storage projects economically viable for utilities and independent power producers, resulting in over 20 GWh of energy storage projects awarded between April 2024 and October 2025 in India alone.

Restraints - High Capital Expenditure and Installation Complexity

Despite substantial technological maturity, flow battery systems remain capital-intensive relative to competing storage technologies, particularly lithium-ion batteries for applications requiring less than four hours of discharge duration. The engineering complexity of flow battery installations-encompassing large external electrolyte storage tanks, circulation pumps, power conversion systems, and sophisticated battery management controls-translates into elevated balance-of-system costs.

While energy density remains lower than lithium-ion alternatives (typically 20-50 Wh/liter for vanadium systems versus 250+ Wh/liter for lithium-ion), this characteristic, though advantageous for safety and longevity, necessitates larger physical footprints and more complex site preparation. The upfront total capital cost for flow battery installations ranges from USD 200-600 per kilowatt-hour, creating economic headwinds particularly in small-scale distributed applications where simpler battery chemistries dominate market segments.

Supply Chain Constraints and Material Availability Concerns

Flow battery technology, especially vanadium redox flow batteries, exhibits vulnerability to supply chain disruptions affecting vanadium electrolyte procurement. While vanadium availability has improved with China controlling approximately 60% of global production capacity and Australia emerging as a secondary source, geopolitical concentrations create strategic risk for manufacturers.

The European Union’s Critical Raw Materials Act (CRMA), implemented in May 2024, emphasizes securing supply diversification and establishing extraction processing benchmarks, potentially increasing raw material costs. Additionally, materials science innovations-such as graphene-enhanced electrodes and advanced ion-exchange membranes-remain cost-intensive to manufacture at production scale, limiting deployment of performance-enhanced systems in price-sensitive markets.

Opportunity - Long-Duration Energy Storage for Renewable-Dominant Grid Architecture

The transition toward grids powered predominantly by renewable sources necessitates long-duration energy storage systems capable of storing energy for 8-12+ hours and cycling daily. Flow batteries uniquely satisfy this requirement through their architectural advantage of decoupling power and energy capacity-allowing power rating determination by cell stack quantities while energy capacity scales with electrolyte volume. The Flow Batteries Europe industry association targets deployment of 20 GW and 200 GWh cumulative capacity by 2030, from current levels of approximately 1.4 GW globally as of mid-2024.

Emerging markets, including India, where renewable energy capacity additions are projected to contribute 35% of total generation by FY2030, create substantial opportunities for flow battery deployment. The Central Electricity Authority estimates incremental 200 GW renewable capacity additions between FY2025-FY2030, with corresponding requirements for supporting storage infrastructure to ensure transmission reliability and frequency stability.

Commercial and Industrial Behind-the-Meter Energy Storage Expansion

Commercial and industrial enterprises increasingly deploy behind-the-meter (BTM) energy storage systems to optimize electricity consumption, reduce demand charges, and participate in energy markets. Flow batteries provide unique value for C&I applications requiring extended discharge durations, particularly for facilities with consistent daily load profiles and exposure to time-of-use electricity rates. Regulatory evolution, notably the UK’s P415 code modification permitting BTM batteries to trade in energy markets equivalent to front-of-meter systems, increased BTM battery value by 400% or more in select locations by enabling aggregation for wholesale market participation.

Manufacturing facilities, data centers requiring uninterruptible power supplies, and commercial properties supporting EV charging infrastructure represent primary target segments, with flow batteries offering 25-30 year asset life and minimal degradation compared to cycling-limited lithium alternatives. Invinity Energy Systems has expanded commercial deployments of vanadium flow batteries for industrial applications in Europe and North America, with system configurations ranging from 4-80 MWh tailored to specific facility requirements.

Category-wise Analysis

Battery Type Insights

Redox Flow Batteries as Dominant Technology Category

Redox flow batteries, comprising approximately 62% market share, maintain leadership status driven by the proven performance and commercial maturity of vanadium redox flow battery (VRFB) systems. The dominant redox category encompasses vanadium-based systems where the same vanadium electrolyte circulates through cell stacks on both positive and negative sides, eliminating cross-contamination risks inherent in competing chemistries. VRFB technology demonstrates exceptional durability through unlimited cycle life without degradation, validated by field deployments exceeding 25 years of operational service.

The technology delivers round-trip efficiency of 70-85%, adequate for long-duration applications where annual cycling frequencies remain moderate. Sumitomo Electric Industries, a primary global VRFB manufacturer, received orders for multiple grid-scale installations, including eight consecutive 1MW × 8-hour systems across Japan between 2024 and 2025, demonstrating institutional confidence in redox chemistry viability. The vanadium redox battery market specifically is growing at 17% CAGR through 2033, supported by declining electrolyte costs and improved membrane technologies.

Battery Material Insights

Vanadium-Based Systems Command Highest Market Adoption

Vanadium chemistries capture approximately 65% of material-based market segmentation, cementing vanadium as the preferred electrolyte substance for commercial flow battery deployment. Vanadium’s advantages, including four accessible oxidation states enabling electron transfer, high chemical stability, environmental recyclability, and commercial availability in geographically distributed production regions, create compelling technical and economic advantages over competing materials.

China’s dominant position as a global vanadium supplier, combined with Australia’s emerging production capacity, provides manufacturers with regional sourcing flexibility. The rapid growth in the vanadium redox flow battery market is reflecting strong deployment momentum, particularly across the Asia Pacific. Conversely, zinc-bromine and iron-based flow batteries face market penetration constraints due to lower energy density, complex handling requirements for bromine species, and less mature commercialization compared to vanadium systems.

Storage Type Insights - Large-Scale Systems Above 500kW Dominate Utility Deployments

Large-scale flow battery installations exceeding 500 kilowatt power ratings represent approximately 72-75% market value, driven by utility and grid operator preference for consolidated battery systems serving regional transmission and distribution requirements. Systems rated from 1-5 megawatt power capacity paired with 4-12 megawatt-hour energy ratings address grid operator needs for frequency regulation, peak shaving, and renewable smoothing services.

The China Huaneng Group’s recently completed 200MW/1GWh vanadium redox battery facility in Xinjiang exemplifies large-scale deployment targeting regional grid stability across renewable-intensive generation zones. Large-scale systems benefit from economy-of-scale cost reductions and enable participation in wholesale energy arbitrage markets where revenue opportunities justify elevated capital expenditures.

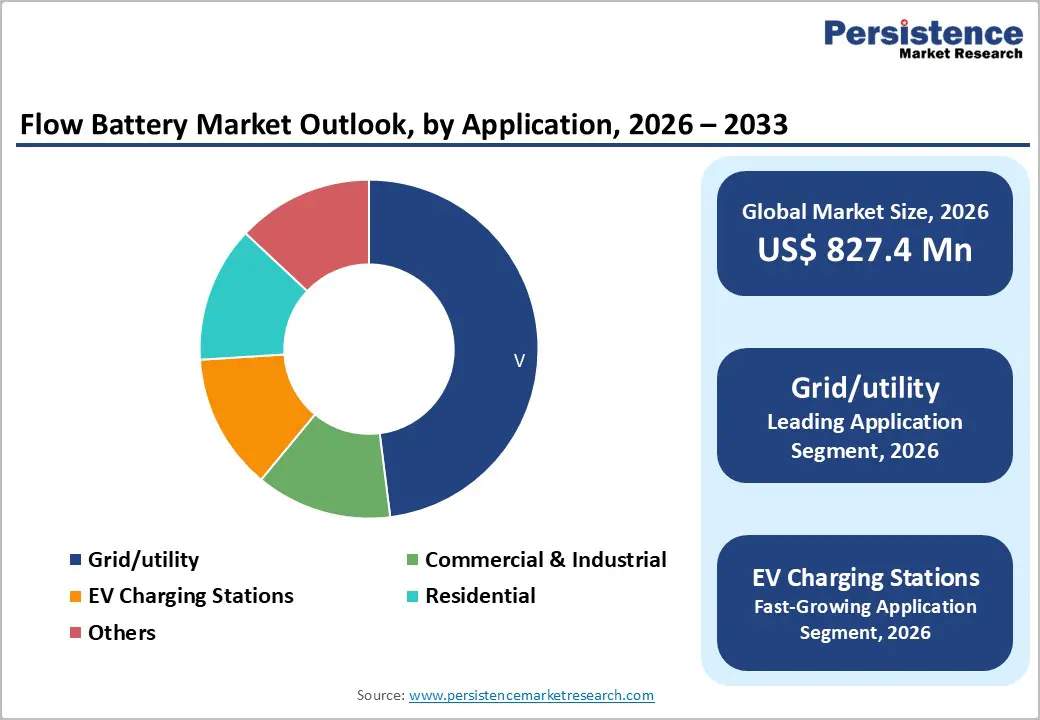

Application Insights- Grid/Utility Segment Commands Largest Application Category

The grid/utility application segment captures approximately 47% market share, representing the principal revenue driver across installed capacity and projected deployments through 2033. Utilities deploy flow batteries for multifaceted grid services including renewable energy integration, frequency regulation, peak shaving, demand response, and black start capability following grid outages.

The load-shifting application specifically accounted for largest grid/utility demand, enabled by flow battery capability to store low-cost energy during periods of renewable oversupply or off-peak electricity pricing for discharge during peak demand intervals. EV charging station energy storage, while nascent, represents the fastest-growing application segment at 18% CAGR, as charging network operators deploy flow batteries to support fast-charging infrastructure during peak utilization periods, reducing grid interconnection upgrade requirements and managing electricity costs during peak pricing intervals.

Regional Insights

North America Flow Battery Market Trends and Insights

The North America flow battery market is experiencing rapid expansion supported by strong federal and state-level policy frameworks aimed at accelerating grid modernization and long-duration storage deployment. Federal funding programs, clean energy tax incentives, and procurement mandates are enabling utility adoption of multi-hour storage technologies to complement rising wind and solar penetration across major electricity markets. States such as California and Texas continue to lead market adoption due to higher renewable integration and the increasing value of frequency regulation, peak-shifting, and capacity services in competitive wholesale markets.

Market participants pursue commercialization through pilot-to-utility-scale deployments, service-based contracts, and domestically manufactured system strategies aligning with supply chain resilience objectives. Modular system configurations and standardized containerized platforms are increasingly positioned for both front-of-the-meter and behind-the-meter applications. As wholesale power markets evolve to recognize storage monetization pathways, North America is expected to remain the fastest-growing developed region for flow battery deployments through 2030.

Europe Flow Battery Market Trends and Insights

Europe represents a strategic regional market benefiting from comprehensive regulatory The Europe flow battery market is supported by an integrated regulatory ecosystem prioritizing net-zero infrastructure deployment and enhanced grid flexibility through long-duration energy storage systems. The region benefits from strong policy alignment under EU decarbonization frameworks, including initiatives that support simplified permitting, demonstration project funding, and accelerated manufacturing capacity. National-level capacity markets and grid code reforms increasingly recognize value streams for multi-hour storage assets, enabling flow batteries to participate in ancillary services, congestion management, and renewable integration markets.

Sustainability and circular economy regulations, including mandatory recycling requirements and carbon footprint traceability for battery systems, shape manufacturing strategies and encourage regional electrolyte and material sourcing. Market participants emphasize partnerships with utilities, technology licensing, and hybrid energy infrastructure integration to accelerate commercialization. Demonstration-scale installations continue to expand, positioning Europe as a leading technology validation environment, while supportive electricity market reforms are expected to increase adoption through the next decade.

Asia Pacific Flow Battery Market Trends and Insights

Asia Pacific represents the largest regional market for flow battery deployment, driven by accelerated renewable energy expansion, strong government-directed industrial policies, and increasing investment in storage-integrated grid infrastructure. The region’s dominance is anchored by large-scale utility deployments in China, long-duration demonstration programs in Japan, and emerging procurement policies in India and Southeast Asia. Regional governments are prioritizing flow batteries as enabling technologies to reduce renewable curtailment, integrate distributed solar and wind assets, and enhance grid stability in systems experiencing rising intermittency pressures.

Rapid industrialization and uneven transmission infrastructure create emerging opportunities for high-capacity standalone and hybrid renewable-storage deployments, particularly in remote and industrial microgrid settings. Market strategies emphasize scaling manufacturing capacity, developing cost-competitive electrolyte supply chains, and deploying modular systems that reduce engineering complexity and accelerate grid-connected commissioning timelines. Asia Pacific is expected to maintain long-term leadership through 2033 as multi-gigawatt storage tenders support technology scale-up and cost reduction.

Competitive Landscape

The global flow battery market demonstrates a moderately fragmented competitive structure, with leadership concentrated among vertically integrated manufacturers supported by advanced chemical formulation and system integration capabilities. Companies compete by differentiating long-duration storage performance, lowering levelized cost of storage, and scaling manufacturing to capture incentive-linked utility and industrial deployments. Business strategies are increasingly emphasizing the expansion of domestic production footprints to strengthen supply chain resilience and meet regional content requirements, which are tied to policy support. Several players pursue modular, containerized system architectures tailored for utility-scale, microgrid, and behind-the-meter applications to accelerate project timelines and reduce engineering complexity.

Cost optimization efforts focus on enhancing membrane performance, electrolyte stability, and stack durability, while enabling deep discharge without degradation, extending asset life cycles, and improving operational safety through the use of aqueous chemistries. Service-based models, including electrolyte leasing and long-term maintenance contracts, are gaining traction as customers seek predictable lifecycle costs and reduced upfront capital expenditure. Strategic partnerships, technology licensing agreements, and cross-industry collaborations remain essential for accelerating commercialization and accessing diverse global markets.

Key Market Developments

- July 2025: Sumitomo Electric Industries, Ltd. received its third consecutive order from Kashiwazaki IR Energy Co., Ltd. for 1,000 kW × 8-hour vanadium redox flow battery systems, bringing total municipal capacity to 24 MWh, supporting Kashiwazaki City’s decarbonization initiative through renewable energy storage and load shifting capabilities.

- March 2025: Sumitomo Electric’s redox flow battery was selected by SHIN-IDEMITSU Co., Ltd. (IDEX) for a power system stabilization project in Kumamoto, marking the first redox flow battery approval under Japan’s Ministry of Economy, Trade and Industry subsidy program with 8,000 kWh (2,000 kW × 4 hours) capacity scheduled for October 2026 completion.

- January 2025: The U.S. Department of Energy awarded Quino Energy USD 2.6 million federal funding to develop scalable quinone-based redox flow batteries leveraging oil-field tanks for cost-effective long-duration energy storage, reflecting federal prioritization of alternative flow battery chemistries addressing vanadium supply chain dependencies.

Companies Covered in Flow Battery Market

- ESS Tech, Inc.

- Redox One

- WattJoule Corporation

- Invinity Energy Systems

- Largo Inc.

- Primus Power

- Sumitomo Electric Industries, Ltd.

- CellCube Energy Storage GmbH

- Redflow Ltd.

- VRB ENERGY

- Elestor

- Jena Flow Batteries GmbH

- Lockheed Martin Corporation

- EverFlow

- Stryten Energy

- Quino Energy,

- China Huaneng Group

Frequently Asked Questions

The global flow battery market is expected to reach approximately US$ 827.4 million in 2026.

Rising renewable energy integration needs, policy incentives, and declining system costs are the key demand drivers.

Asia Pacific holds the largest share of the flow battery market in 2025.

Long-duration energy storage for renewable-dominant grids represents the most significant opportunity.

Key market players include Sumitomo Electric, Invinity, ESS Tech, Lockheed Martin, VRB Energy, and other emerging innovators.