- Biotechnology

- Electrolyte Reagents Market

Electrolyte Reagents Market Size, Share and Growth Forecast, 2026 - 2033

Electrolyte Reagents Market by Product Characteristics (Potassium, Calcium, Magnesium, Chloride, Lithium, Phosphorus, Others), Diagnostics Application (Bone Diseases, Renal Diseases, Metabolic Disorders, Bipolar Disorders, Hyperkalemia & Hypokalemia, Others), End-User Channel (Hospitals, Diagnostic Labs, Specialty Clinics, Academic & Research Institutes, Industrial Labs, Distributors), and Regional Analysis for 2026 - 2033

Electrolyte Reagents Market Share and Trends Analysis

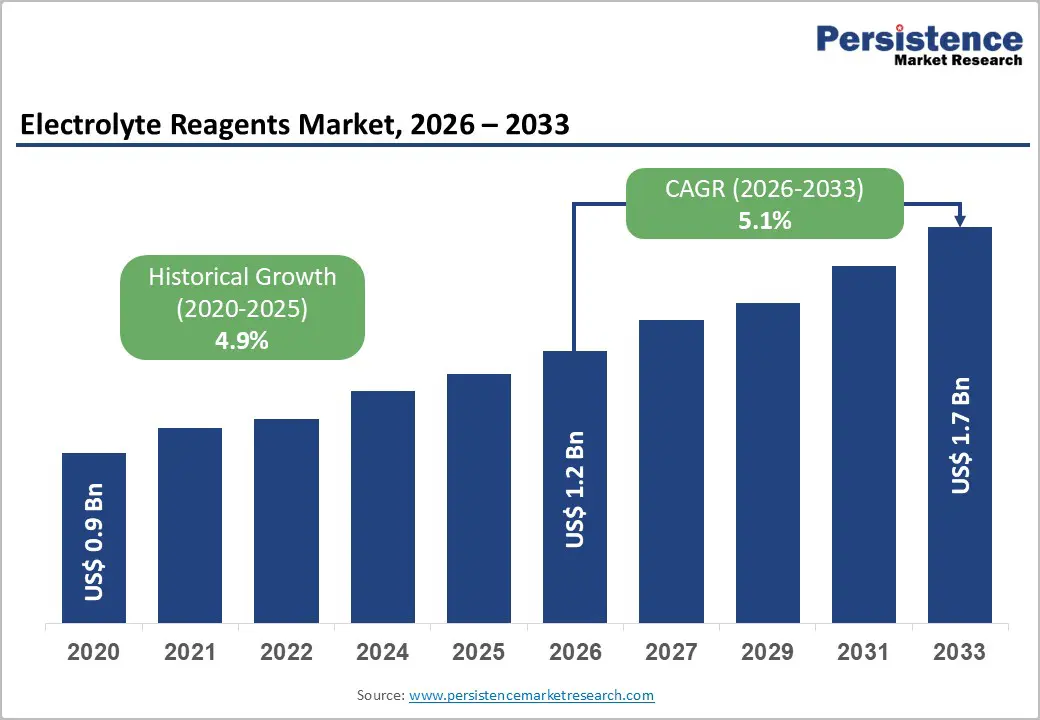

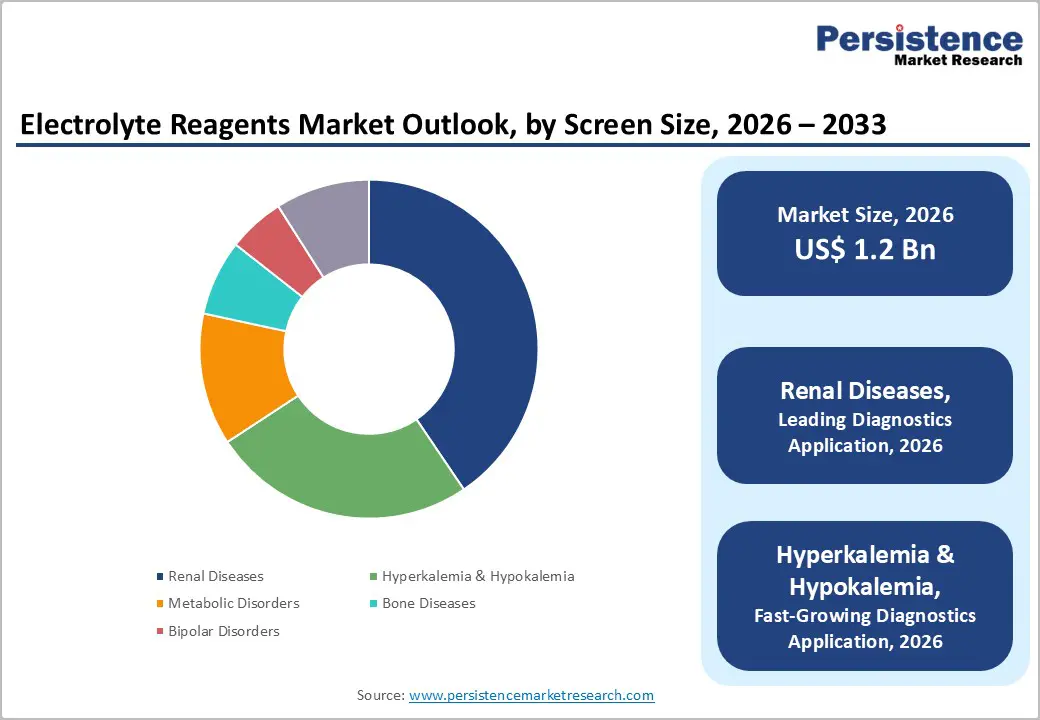

The global electrolyte reagents market size is likely to be valued at US$1.2 billion in 2026 and is projected to reach US$1.7 billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026 - 2033.

The market is growing due to rising demand for clinical diagnostics and electrolyte testing, driven by the increasing prevalence of chronic diseases, including renal and metabolic disorders. Healthcare providers are prioritizing rapid, accurate biochemical analysis, boosting adoption of automated analyzers that rely on high-quality reagents.

Expanding diagnostic laboratory networks and the trend toward outsourcing further increase testing volumes. Additionally, urbanization, higher healthcare spending, and improving access to medical services in emerging markets are accelerating routine screening and preventive care. The functional advantage of electrolyte reagents, enabling precise, real-time monitoring of critical body functions, supports their essential role across hospitals, labs, and research applications.

Key Industry Highlights

- Dominant Product Types: Potassium electrolyte reagents are set to command around 32% of the revenue share in 2026, while lithium electrolyte reagents are likely to grow the fastest at 6.4% CAGR through 2033, driven by increased therapeutic monitoring needs.

- Leading Diagnostic Applications: Renal testing is set to hold about 34% share in 2026, while hyperkalemia and hypokalemia monitoring are expected to grow the fastest at a 5.9% CAGR through 2033, supported by rising cases of electrolyte imbalance.

- Dominant End-User Channels: Hospitals are set to account for nearly 39% of the market share in 2026, while diagnostic laboratories are likely to grow the fastest at a 6.1% CAGR through 2033, reflecting increasing test outsourcing.

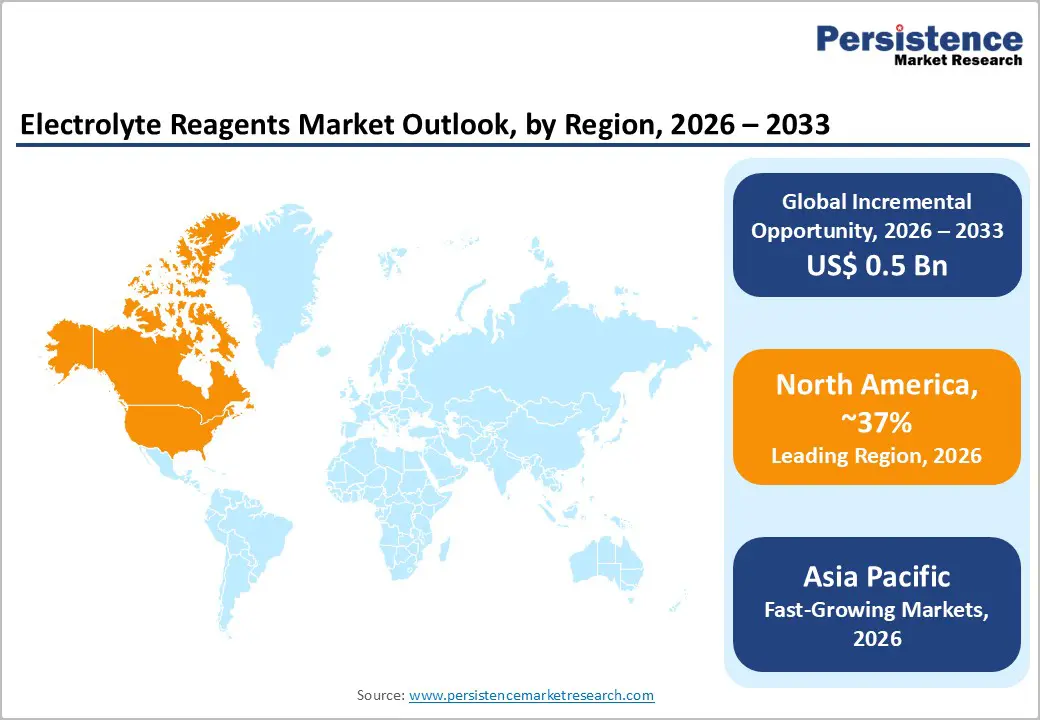

- Regional Leadership: North America is set to command around 37% share in 2026, while Asia Pacific is likely to grow the fastest at 6.7% CAGR through 2033, driven by expanding healthcare infrastructure.

- Competitive Environment: Competitive dynamics include continuous product innovation, strategic partnerships, and mergers and acquisitions, with companies focusing on expanding their global presence and strengthening their diagnostic capabilities.

| Key Insights | Details |

|---|---|

| Electrolyte Reagents Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 1.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

DRO Analysis

Driver - Rising Burden of Chronic Diseases and Electrolyte Imbalances

The rising global incidence of renal diseases, metabolic disorders, and electrolyte imbalance conditions (e.g., hyperkalemia, hypokalemia) is driving consistent demand for clinical electrolyte reagent testing. Chronic conditions such as kidney failure, diabetes-related complications, and cardiovascular disease require regular electrolyte monitoring (e.g., potassium, calcium, magnesium) to guide treatment protocols. According to global health bodies, chronic kidney disease affects over 10% of the adult population in many regions, intensifying diagnostic throughput in hospitals and labs. This has translated into a growing need for reagent kits used in automated blood chemistry analyzers that quantify electrolytes rapidly and accurately within clinical workflows. Enhanced screening initiatives in preventive care programs further sustain testing volumes across diagnostic settings, reinforcing reagent demand.

In 2026, global awareness initiatives such as World Kidney Day 2026, supported by international nephrology organizations, emphasized early detection and routine screening through blood and urine tests, accelerating diagnostic testing volumes worldwide. Additionally, multiple FDA-approved kidney disease treatments in 2025 have expanded patient management pathways, increasing the need for continuous electrolyte monitoring to track treatment response and disease progression. These developments highlight a clear shift toward proactive disease management, directly increasing the frequency of electrolyte testing and reinforcing long-term reagent demand.

Advancements in Diagnostic Technologies and Expansion of Healthcare Infrastructure

Innovation in ion-selective electrode (ISE) and photometric technologies has significantly improved the performance of electrolyte reagent testing, reducing assay times and improving accuracy. Integration with automated analyzer platforms has accelerated adoption by reducing manual errors and supporting high-volume workflows in hospitals and independent laboratories. Several regulatory approvals and ISO-aligned quality standards for advanced reagent formulations and analyzer systems have enhanced market credibility, driving replacement cycles and equipment upgrades that, in turn, boost reagent consumption. Analysts highlight that integrating digital calibration and built-in quality controls enhances reliability, fostering greater clinical trust and expanding their use in critical care diagnostics.

The healthcare systems are rapidly scaling diagnostic capacity, particularly in emerging economies. Governments and healthcare institutions are investing in nephrology services and laboratory infrastructure to address rising disease burdens and improve access to diagnostic testing. In parallel, 2025 - 2026 industry trends show growing adoption of point-of-care and portable electrolyte analyzers, enabling faster decision-making in emergency and critical care settings. These advancements are complemented by increasing integration of digital health technologies and real-time monitoring solutions, which enhance testing efficiency and expand use cases. Thus, infrastructure expansion and technological innovation are significantly increasing reagent consumption across hospitals, diagnostic labs, and decentralized care settings.

Restraints - High Cost of Advanced Reagents and Regulatory Compliance Challenges

Developing high-performance electrolyte reagents involves significant R&D and validation costs, which can raise prices and limit adoption in cost-sensitive markets. Compliance with stringent international standards (e.g., ISO 15189 for medical laboratories, FDA/CE marking) increases production overheads and time to market for new products. Particularly in emerging economies, the price barrier can deter small labs and clinics from adopting advanced reagents, slowing penetration. Moreover, frequent regulatory updates necessitate ongoing modifications to formulations and documentation, adding complexity and cost. These cumulative factors create entry barriers for new players and limit scalability for smaller manufacturers in highly regulated environments.

Recent industry developments reinforce this constraint. In 2025, new tariffs on medical and laboratory imports, ranging from baseline levels to over 100% in certain trade corridors, significantly increased the cost of diagnostic supplies, including reagents and lab equipment. Additionally, healthcare systems are moving toward value-based care models that emphasize cost control and reimbursement efficiency, further pressuring pricing for diagnostic consumables. These combined pressures are limiting manufacturers' pricing flexibility and slowing the adoption of premium reagent solutions, particularly in price-sensitive healthcare systems. As a result, companies are being forced to optimize cost structures while maintaining compliance and quality standards.

Supply Chain Vulnerabilities and Raw Material Constraints

Specialized electrolyte reagent manufacturing is reliant on precise raw materials and chemical reagents. Disruptions in global supply chains, such as geopolitical tensions, transportation bottlenecks, or sudden regulatory export restrictions, can constrain reagent availability. Lead times for raw chemical precursors have become more volatile in recent years, which risks inventory shortages for reagent manufacturers and downstream lab facilities. Any degradation in reagent purity due to supply inconsistency can adversely affect test accuracy, posing a risk to brand credibility. These uncertainties make it difficult for manufacturers to maintain consistent production cycles and meet growing demand reliably.

A significant proportion of healthcare providers reported ongoing or worsening supply chain disruptions in 2025, directly affecting the availability of reagents and diagnostic materials. In parallel, geopolitical trade tensions have driven a shift toward local sourcing of reagents in countries such as China to mitigate cost and supply risks. While this improves resilience in the long term, it introduces short-term challenges related to regulatory consistency and quality validation. These evolving dynamics underscore the persistent vulnerability of global reagent supply chains and their impact on market stability, underscoring the need for supply chain resilience as a critical strategic priority.

Opportunities - Rising Adoption of Point-of-Care Testing and Decentralized Diagnostics

The accelerated adoption of point-of-care (POC) testing devices that deliver rapid electrolyte results presents a significant growth avenue. POC platforms, widely used in emergency departments and outpatient clinics, depend on ready-to-use reagent cartridges formulated for ease of handling and minimal processing time. Projections suggest that integrating rapid electrolyte testing into routine health screenings could capture a notable share of hospital and clinic budgets, enhancing early diagnosis of metabolic shifts and acute conditions, particularly in decentralized care environments. This shift toward near-patient testing is transforming how diagnostic services are delivered across both urban and remote healthcare settings. It is also enabling healthcare providers to reduce patient wait times and improve overall treatment efficiency.

In 2025, the U.S. Food and Drug Administration (FDA) granted multiple clearances for rapid point-of-care diagnostic systems that deliver results within minutes, reinforcing regulatory support for decentralized testing models. Additionally, clinical lab leaders in 2026 indicate that a growing share of diagnostic testing is moving outside traditional laboratories, with point-of-care solutions expanding across population health programs and outpatient settings. These advancements highlight a clear industry shift toward faster, accessible diagnostics, directly increasing demand for compatible electrolyte reagents used in portable and high-frequency testing environments. This trend is expected to further accelerate as healthcare systems prioritize efficiency and patient-centric care delivery.

Growth in Clinical Research, Laboratory Outsourcing, and Regulatory Alignment

Growth in pharmaceutical research, clinical trials, and academic studies creates demand for specialized electrolyte reagents to support metabolic profiling and biomarker research. Partnerships between reagent manufacturers and research institutions can unlock tailored solutions for high-throughput testing, driving volume growth. Additionally, the trend of outsourcing diagnostics to specialized laboratories opens opportunities for reagent suppliers to establish long-term contracts and capture stable recurring demand streams. These collaborations are increasingly critical in advancing precision medicine and improving diagnostic accuracy across therapeutic areas. They also enable laboratories to scale operations efficiently while maintaining high testing standards.

The evolving regulatory and innovation ecosystems are accelerating global market expansion. In 2025, the FDA approved 46 novel drugs, expanding clinical pipelines and increasing the need for ongoing diagnostic monitoring, including electrolyte testing, throughout treatment lifecycles. Furthermore, new regulatory initiatives aimed at accelerating clinical approvals and improving trial efficiency are streamlining product development and encouraging innovation in diagnostics and associated reagents. Thus, rising research activity, supportive regulatory frameworks, and increased outsourcing are creating a robust foundation for sustained growth opportunities in the electrolyte reagents market. This environment is also encouraging new entrants and investments across both developed and emerging markets.

Category-wise Analysis

Product Characteristics Insights

Potassium electrolyte reagents are expected to dominate with an estimated 32% market share in 2026. This leadership is closely aligned with clinical practice, where potassium testing is a core component of routine diagnostic panels used across hospitals and laboratories. Potassium levels play a critical role in assessing cardiac rhythm stability, kidney function, and metabolic balance, making it one of the most frequently tested electrolytes. High testing frequency ensures consistent reagent consumption, particularly in emergency care and intensive care units.

Additionally, standardized testing protocols across healthcare systems further reinforce demand stability. For example, in 2025, the American Heart Association updated its acute cardiac care guidance, emphasizing routine electrolyte monitoring, especially potassium, for patients at risk of arrhythmia, thereby directly increasing testing frequency in hospital settings.

In contrast, lithium electrolyte reagents are projected to be the fastest-growing segment, expanding at a CAGR of approximately 6.4% by 2033. Growth is primarily driven by increasing use in therapeutic drug monitoring, especially for psychiatric conditions such as bipolar disorder. Lithium has a narrow therapeutic range, requiring precise and frequent monitoring, thereby increasing dependence on high-quality reagents.

Expanding mental health awareness and improved access to psychiatric care are further supporting demand growth. In 2026, the National Health Service expanded its community mental health programs under the Long Term Plan, increasing lithium prescriptions and mandating regular serum monitoring. Additionally, lithium assays are gaining traction in specialized research applications, including neurochemical studies, reinforcing their growth trajectory.

Diagnostics Application Insights

Within diagnostic applications, renal diseases are expected to lead the market with an estimated 34% share in 2026. Electrolyte testing is fundamental in evaluating kidney function, fluid balance, and metabolic activity, making it indispensable in both routine and critical care diagnostics. Tests measuring sodium, potassium, calcium, and chloride levels are widely used in renal panels, driving consistent reagent demand.

The high global prevalence of chronic kidney disease and metabolic syndromes further strengthens this segment’s dominance. Notably, in 2025, India’s Ministry of Health and Family Welfare expanded screening under the National Program for Prevention and Control of Non-Communicable Diseases (NPCDCS), increasing routine electrolyte testing across public health facilities. This has reinforced sustained demand for electrolyte reagents across hospitals and diagnostic laboratories.

Hyperkalemia and hypokalemia monitoring is poised to be the fastest-growing application segment, with a positive CAGR. The increasing incidence of electrolyte imbalances linked to cardiovascular diseases, diabetes, and critical care conditions is driving frequent testing in this category. Emergency departments and cardiac care units, in particular, require rapid and repeated potassium assessments to prevent life-threatening complications.

In 2026, the European Society of Cardiology updated its emergency cardiovascular care recommendations, highlighting rapid electrolyte correction protocols for acute cardiac events, thereby increasing diagnostic testing frequency. Additionally, advancements in diagnostic technologies are enabling faster and more accurate detection of electrolyte abnormalities, supporting broader clinical adoption.

Regional Insights

North America Electrolyte Reagents Market Trends

North America is likely to dominate the global electrolyte reagents market, accounting for an estimated 37% share in 2026, supported by advanced healthcare infrastructure and strong diagnostic capabilities. The region benefits from high per capita healthcare expenditure and early adoption of automated laboratory technologies across hospitals and diagnostic centers. The United States leads regional revenue generation due to its well-established insurance coverage systems and extensive clinical laboratory networks. High prevalence of chronic kidney disease and metabolic disorders continues to drive consistent testing volumes.

Preventive healthcare programs and routine screening initiatives further contribute to sustained reagent demand. Notably, in 2025, the U.S. Department of Health and Human Services expanded funding under national chronic disease programs, increasing access to routine diagnostic testing, including electrolyte panels.

Regulatory frameworks such as CLIA and CAP ensure strict quality and performance standards, compelling manufacturers to invest in high-precision reagent formulations. While compliance requirements increase operational costs, they also enhance product reliability and market trust. Strategic collaborations between healthcare providers and reagent manufacturers are expanding access to advanced diagnostic solutions. Investment trends remain strong, with continuous funding directed toward laboratory automation and research in clinical diagnostics.

In 2026, the Biomedical Advanced Research and Development Authority announced new investments in diagnostic preparedness, strengthening laboratory capabilities, and reagent demand. Additionally, targeted acquisitions and partnerships are helping companies strengthen their regional footprint.

Europe Electrolyte Reagents Market Trends

Europe represents a stable and mature electrolyte reagents market, characterized by well-established healthcare systems and harmonized regulatory standards across EU countries. Germany, the U.K., France, and Spain are key contributors, with Germany leading due to its advanced hospital infrastructure and high diagnostic testing volumes. The region benefits from consistent demand driven by chronic disease management and preventive healthcare practices. Diagnostic outsourcing and widespread adoption of clinical testing services further support reagent consumption.

Public healthcare systems across Europe ensure broad access to routine electrolyte testing. In 2025, the European Medicines Agency advanced implementation of the In Vitro Diagnostic Regulation (IVDR), strengthening quality standards and increasing demand for compliant, high-performance reagents.

European market growth is supported by early disease detection initiatives and increasing integration of digital diagnostic technologies. Regulatory harmonization across the EU simplifies cross-border product approvals, enabling manufacturers to expand efficiently. Investment in research and development is rising, particularly for reagents tailored to regional clinical workflows. Public-private partnerships are playing a critical role in strengthening diagnostic networks and improving testing efficiency.

In 2026, Germany’s Federal Ministry of Health expanded funding for hospital digitalization under national health programs, accelerating the adoption of automated diagnostic systems. Additionally, the region is witnessing the gradual modernization of laboratory infrastructure, enhancing testing capacity.

Asia Pacific Electrolyte Reagents Market Trends

Asia Pacific is projected to be the fastest-growing regional market, to expand at a CAGR of approximately 6.7% through 2033, driven by rapid healthcare development and increasing diagnostic demand. Countries such as China, India, Japan, and key ASEAN nations are witnessing significant expansion in healthcare infrastructure and laboratory networks. The rising prevalence of chronic diseases and growing awareness of preventive healthcare are increasing testing volumes across the region.

Large patient populations and improving access to medical services further amplify demand. Additionally, the expansion of private diagnostic chains is strengthening service availability in urban and semi-urban areas. In 2025, India’s Ayushman Bharat Digital Mission accelerated integration of digital health records and diagnostic services, supporting higher testing volumes across public and private labs.

Government initiatives aimed at improving healthcare access, particularly in rural and underserved areas, are accelerating diagnostic adoption. Regulatory frameworks are gradually evolving, with several countries simplifying approval processes to attract foreign investment and encourage local manufacturing. Regional companies are increasingly collaborating with global players to develop cost-effective reagent solutions tailored to local needs. Investments in training, distribution networks, and laboratory modernization are enhancing market penetration across tier-2 and tier-3 cities.

In 2026, Japan’s Ministry of Health, Labor and Welfare introduced expanded funding for advanced diagnostic technologies in aging population care, increasing demand for routine electrolyte testing.

Competitive Landscape

The global electrolyte reagents market is moderately consolidated, with key players such as Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and Danaher Corporation holding a significant revenue share. These companies leverage strong hospital and laboratory networks along with integrated analyzer-reagent ecosystems. Continuous R&D investments focus on improving reagent accuracy, automation compatibility, and workflow efficiency. Their scale and regulatory expertise provide a strong competitive advantage globally.

Players such as Sysmex Corporation and Randox Laboratories focus on niche applications and regional expansion strategies. High entry barriers, including regulatory compliance and analyzer integration requirements, limit the number of new entrants. However, growth in point-of-care and decentralized diagnostics is enabling smaller, technology-driven firms to enter selectively. Market consolidation is expected to increase through strategic partnerships, acquisitions, and geographic expansion initiatives.

Key Developments:

- In May 2025, Siemens Healthineers announced a US$ 150 million investment in U.S. infrastructure, including Varian manufacturing expansion in California and new logistics depots to strengthen supply chain resilience. This move focuses on precision therapy and operational efficiency, while parallel strategic discussions around a potential diagnostics division restructuring indicate a more selective approach to its diagnostics portfolio.

- In May 2025, Roche committed US$ 550 million to expand its Indianapolis diagnostics manufacturing hub, with continued developments into 2026. The investment strengthens large-scale production of diagnostic technologies and supports long-term capacity expansion, reinforcing reagent supply capabilities within its broader multi-billion-dollar U.S. manufacturing strategy.

Companies Covered in Electrolyte Reagents Market

- Abbott Laboratories

- Siemens Healthineers

- Roche Diagnostics

- Beckman Coulter

- Sysmex Corporation

- Randox Laboratories

- Merck KGaA

- Thermo Fisher Scientific

- Horiba Ltd.

- Nova Biomedical

- BioMérieux

- Ortho Clinical Diagnostics

- Abbexa Ltd

Frequently Asked Questions

The global market is projected to reach US$ 1.2 billion in 2026.

Rising demand for clinical diagnostics, chronic disease monitoring, and automated laboratory testing drives market growth.

The market is expected to grow at a CAGR of 5.1% from 2026 to 2033.

Growth opportunities include point-of-care testing expansion, diagnostic outsourcing, and increasing healthcare access in emerging markets.

Key players include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and Thermo Fisher Scientific.