- Food Ingredients & Additives

- Flower-Based Essence Market

Flower-Based Essence Market Size, Share and Growth Forecast, 2026-2033

Flower-Based Essence Market by Product Form (Liquid, Powder), Source (Bleeding Heart, Aspen, Centaury, Chamomile, Cherry Plum, Chicory, Crab Apple, Gentian, Willow, Wild Oat), End-Use Industry (Food & Beverages, Fragrance Industry, Cosmetics, Pharmaceuticals) and Regional Forecast for 2026-2033

Flower-Based Essence Market Share and Trends Analysis

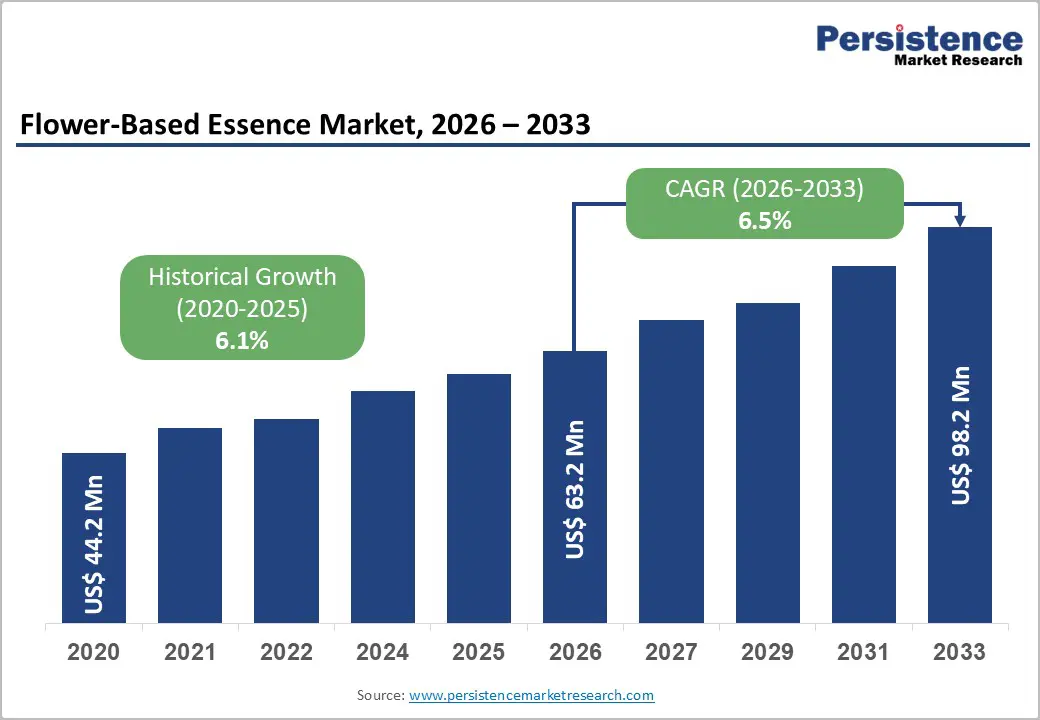

The global flower-based essence market size is likely to be valued at US$ 63.2 million in 2026, and is projected to reach US$ 98.2 million by 2033, growing at a CAGR of 6.5% during the forecast period 2026-2033. This growth is driven by the increasing demand for natural botanical ingredients in food, fragrance, cosmetic, and pharmaceutical products, reinforced by clean-label trends and regulatory support for plant-derived inputs. Consumers have shown a rising preference for flower-based extracts, with aromatherapy use and expanded applications beyond perfumery further broadening the market's reach.

Long-term expansion is expected to remain resilient, supported by stable historical performance and sustained innovation in extraction and formulation technologies. As consumer awareness of botanical benefits grows, and as industries diversify their product portfolios, flower-based essences have continued to gain traction across multiple sectors. Companies that have aligned their offerings with evolving consumer preferences, regulatory frameworks, and application-specific requirements will position themselves for continued growth and market share gains in the years ahead.

Key Industry Highlights

- Dominant Product Form: Liquid essences are projected to dominate with around 68% revenue share in 2026, supported by their extensive use in fragrances and beverages

- Fastest-growing Product Form: Powdered essences are expected grow the fastest at roughly 7.6% CAGR through 2033 due to their longer shelf life and handling efficiency.

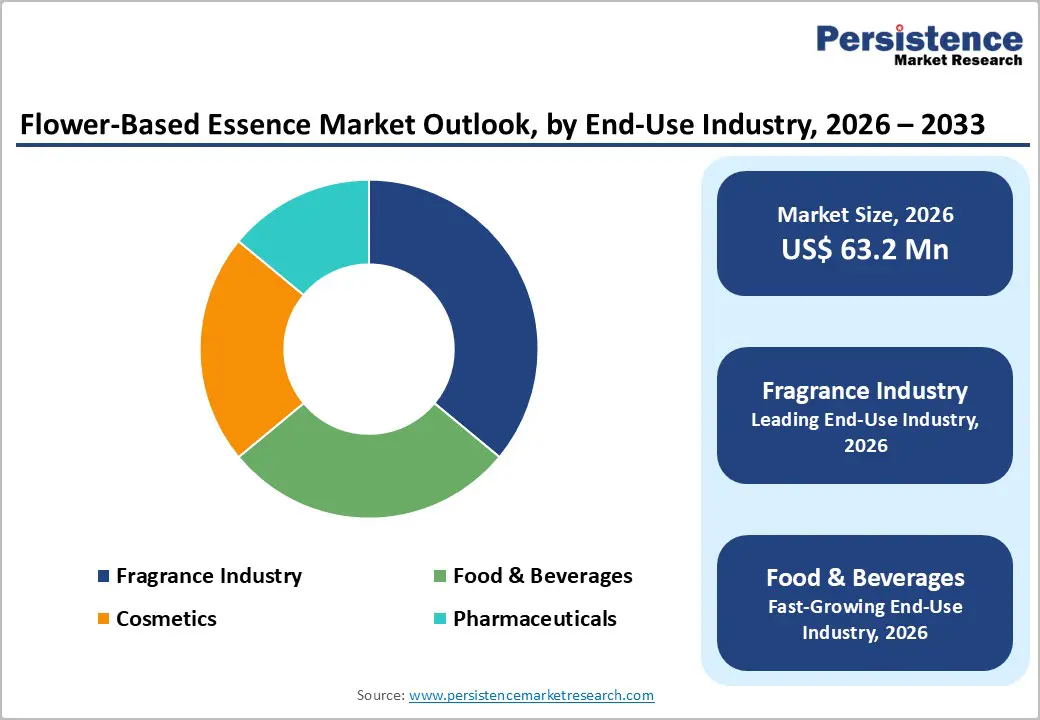

- Leading End-Use Industry: The fragrance industry is expected to lead with approximately 36% share in 2026, whereas food & beverages are projected to grow the fastest at a 7.2% CAGR through 2033, driven by clean-label and botanical flavor demand.

- Source Dynamics: Chamomile is expected to lead with a 42% share in 2026 due to its widespread adoption across applications, while bleeding heart is set to grow at a 2026-2033 CAGR of 8%, owing to premium positioning and functional differentiation.

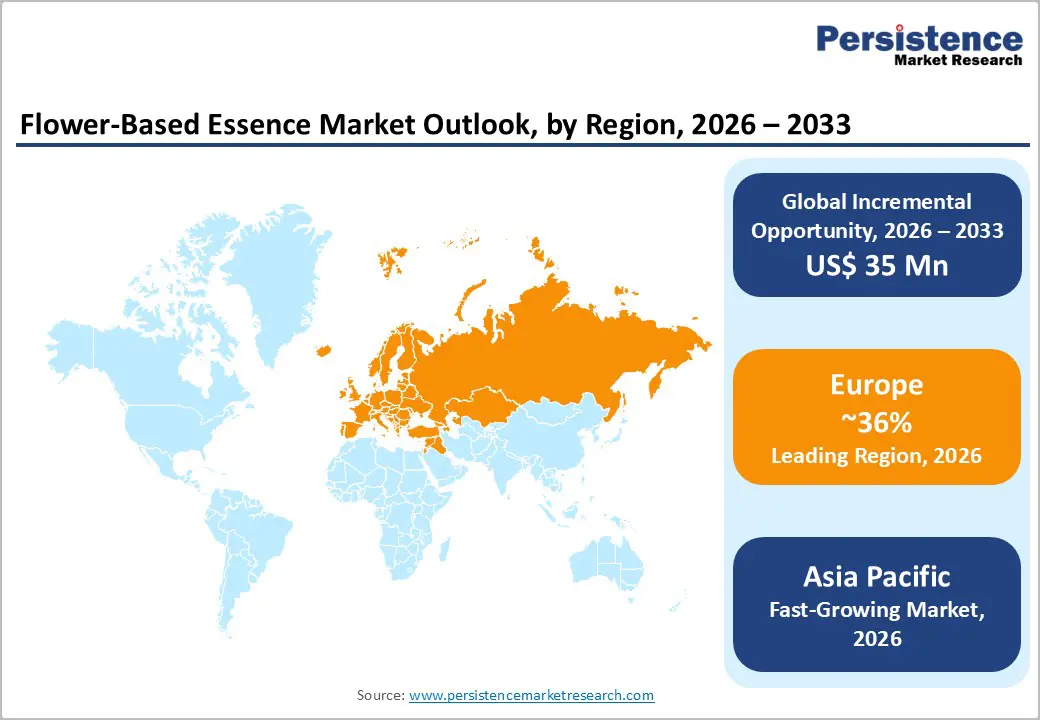

- Regional Growth Dynamics: Europe is likely to dominate at 36% in 2026, aided by a strong fragrance and cosmetics base, while Asia Pacific is expected to be the fastest-growing market at 7.4% CAGR during 2026–2033, driven by robust botanical sourcing.

- Competitive and Innovation Landscape: Competitive strategies increasingly focus on sustainable sourcing and advanced extraction technologies, with such initiatives influencing major strategic investments by top players.

- May 2025: Goldfield & Banks expanded its Pacific Rock Iris fragrance lineup with rare Tasmanian Boronia and Iris essences, capturing coastal floral notes in a unisex eau de parfum that evokes Australian ocean air.

| Key Insights | Details |

|---|---|

| Flower-Based Essence Market Size (2026E) | US$ 63.2 Mn |

| Market Value Forecast (2033F) | US$ 98.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Adoption of Natural Flower-Based Essences across Consumer Industries

The flower-based essence market growth is benefiting from the global shift toward natural, plant-derived, and clean-label ingredients across food, cosmetics, and fragrance products. Regulatory authorities such as the U.S. Food and Drug Administration (FDA), European Food Safety Authority (EFSA), and World Health Organization (WHO) emphasize transparency, safety, and traceability, favoring botanical inputs. Guidance from EFSA and Codex Alimentarius indicates that responsibly sourced natural flavoring and fragrance substances face fewer compliance barriers than synthetic alternatives. This has encouraged manufacturers to replace petrochemical-based aroma compounds with flower-derived essences. The trend is driving portfolio reformulation and long-term sourcing agreements with growers. Premium pricing potential further supports commercial adoption.

Demand is also reinforced by expanding applications in cosmetics, fragrance, and food & beverages. Flower essences such as chamomile, cherry plum, gentian, and wild oat are increasingly used for their aromatic, calming, and wellness-linked attributes. In cosmetics and fragrances, they support sensory differentiation and emotional wellness positioning. In food and beverages, floral notes enable flavor innovation in teas, functional drinks, confectionery, and bakery products. Clear regulatory frameworks across major markets have supported broader commercialization. These applications provide balanced volume growth and value creation.

Supply Chain Vulnerability and Quality Standardization Constraints

Entities operating in the market for flower-based essences are heavily dependent on agricultural performance, exposing the supply chain to multiple external risks. Flower cultivation is highly dependent on climatic conditions, seasonal harvesting cycles, and availability of skilled labor, all of which can disrupt raw material supply. Geographic concentration of certain flower species further limits sourcing flexibility. The Food and Agriculture Organization (FAO) of the United Nations has highlighted the growing impact of climate variability on specialty crop production. These factors contribute to input cost volatility and procurement uncertainty for manufacturers. The risk is particularly elevated for niche sources such as bleeding heart and wild oat, affecting short-term margin predictability.

Ensuring consistent quality and standardization has also erected significant barriers for the growth of this market. Natural variations in soil composition, weather patterns, and extraction processes can result in sensory and compositional inconsistencies. Regulatory requirements for food and pharmaceutical applications mandate strict traceability and quality documentation. Compliance with these frameworks increases production complexity and ongoing quality control costs. Smaller and mid-sized producers face greater pressure to meet these standards. These challenges can slow capacity expansion and limit competitive scalability.

Unlocking Growth through Wellness Integration and Processing Innovation

New avenues for growth in the flower-based essence market are emerging from their expanding use in pharmaceutical and wellness-oriented formulations and rising consumption across developing economies. Manufacturers are incorporating flower-derived essences into calming, digestive, and emotional wellness applications. Extracts such as chamomile and chicory align with established herbal references recognized by the WHO. Despite stringent validation requirements, integration into regulated wellness categories offers high-value, low-volume opportunities. Rising disposable incomes in Asia Pacific and Latin America are fueling the demand for premium personal care products. In China, policies promoting Traditional Chinese Medicine (TCM) encourage standardized cultivation and industrialization of botanical raw materials, boosting local production and regional market growth.

Advances in extraction and processing technologies are further supporting market expansion. Methods such as cold extraction and solvent-free distillation improve yield efficiency while preserving aromatic quality. These innovations enhance scalability and reduce environmental impact, aligning with global sustainability objectives. Improved processing efficiency also supports cost optimization and margin resilience. Technology adoption has enabled producers to maintain consistent quality while meeting regulatory and environmental standards, positioning the market for sustained, long-term growth

Category-wise Analysis

Product Form Insights

Liquid essences are forecasted to be the leading product form, expected to hold around 68% of market revenues in 2026. This dominance is driven by their extensive use in fragrances, beverages, and cosmetic products where solubility, rapid integration, and consistent sensory dispersion are critical. Manufacturers prefer liquid formats for perfumery applications and ready-to-use beverage infusions. For example, premium floral teas often use liquid chamomile or cherry plum extracts to achieve uniform aroma and taste without additional processing. Liquid essences also facilitate large-scale blending in personal care and wellness formulations, maintaining product consistency and consumer satisfaction.

Powdered flower essences are likely to be the fastest-growing form, projected to register an estimated 7.6% CAGR through 2033. They are increasingly adopted due to improved shelf stability, ease of transport, and applicability in dry food mixes, nutraceuticals, and pharmaceutical applications. For instance, powdered chamomile or wild oat extracts are now commonly incorporated into functional drink mixes and dietary supplements, offering both convenience and longer storage life. This growth is fueled by the rising demand for on-the-go wellness products and products requiring dry formulations, which benefit from the flexibility and reduced moisture sensitivity of powder formats.

Source Insights

Chamomile is the projected to be the top source, anticipated to account for approximately 42% of the flower-based essence market revenue share in 2026. Its stable cultivation, recognized therapeutic properties, and wide acceptance in fragrance, cosmetic, and food & beverage applications reinforce its leadership. Chamomile extracts are widely used in calming skincare products, herbal teas, and aromatherapy solutions, offering a consistent aroma and functional benefits. For example, chamomile-infused face masks and lip balms are popular globally for their soothing properties, illustrating the source’s versatility and strong consumer preference.

Niche sources such as bleeding heart are likely to emerge as the fastest-growing, projected to grow at 8% CAGR during the 2026-2033 forecast period. These ingredients are increasingly valued for premiumization, functional differentiation, and wellness applications. For example, wild oat extract is being adopted in stress-relief supplements and high-end skincare serums, positioning these niche botanicals as specialty ingredients. Growth in this segment is supported by rising consumer awareness of unique botanical benefits and the willingness to pay a premium for differentiated floral products.

End-Use Industry

The fragrance industry is anticipated to hold approximately 36% of the flower-based essence market share in 2026. Strong demand for natural floral aromas in fine fragrances, personal care products, and scented wellness items has sustained this leadership position. Leading perfumeries have integrated chamomile and cherry plum essences into signature collections, creating distinctive floral profiles that resonate with consumers. The reliable sensory characteristics and excellent solubility of liquid essences have enabled both mass-market and premium brands to achieve consistent scent quality across production batches, which reinforces brand trust and repeat purchase behavior.

The food and beverage sector is expected to register the highest growth through 2033, expanding at a CAGR of around 7.2%. This acceleration has been driven by premiumization trends and consumer interest in botanical flavor innovation across teas, functional beverages, confectionery, and bakery goods. Manufacturers have increasingly incorporated chamomile and gentian extracts into herbal drinks and gourmet chocolates, enhancing both taste profiles and perceived wellness benefits. As shoppers prioritize natural, clean-label ingredients that deliver sensory appeal alongside health value, formulators that have aligned essence selections with these preferences will have strengthened competitive positioning in high-growth product categories.

Regional Insights

North America Flower-Based Essence Market Trends

North America is a leading regional market for flower-based essences, with the United States anchoring demand, supported by clear FDA regulatory frameworks and high consumer preference for natural, botanical ingredients. The mature fragrance and cosmetic ecosystem of the region drives the extensive use of flower-derived essences in premium perfumery, skincare, and beverage formulations. Ashland’s launch of Perfectyl chamomile extract, sourced from Oregon-grown flowers using sustainable extraction technology, exemplifies innovation in botanical actives tailored to sensitive skin applications. This aligns with industry trends toward environmentally friendly processing and clean-label product portfolios. Botanical suppliers collaborate with multinational brands to ensure traceability and formulation reliability. Investment emphasis remains on sustainable sourcing, advanced extraction, and supply chain partnerships.

Regional market trends are further boosted by premium wellness and advanced extraction adoption, with demand increasing across aromatherapy, personal care, and functional beverages. Cold distillation and solvent-free techniques are gaining traction to preserve aroma integrity and functional properties. Botanical essences are being integrated into products targeting mental well-being, hydration, and skin repair. Consumer demand for botanical-infused formulations amplifies product diversification. For instance, Lilit Botanicals’ Chamomile + Oat skincare formulations combine chamomile oil with oat extract, meeting demand for calming natural products. Continued investment in sustainable cultivation and quality control strengthens competitive positioning and supports market expansion.

Europe Flower-Based Essence Market Trends

Europe is expected to lead in 2026, likely to capture around 36% of the flower-based essence market share, driven by Germany, the U.K., France, and Spain. Regulatory harmonization under the European Union (EU) cosmetic and food safety frameworks encourages plant-based ingredient adoption while sustainability certification and traceability remain key differentiators. European brands emphasize ethical sourcing and organic certification to align with consumer expectations. For example, Weleda, known for its biodynamic and natural formulations, integrates botanical extracts in skincare and holistic wellness products, reinforcing regional preference for grounded, plant-based solutions. This cultural affinity for botanicals supports stable consumption and premium positioning.

Market outlook in Europe is broadening on account of the premium wellness and functional beverage applications of essences extracted from flowers, additionally supported by the rising demand for safe, natural ingredients across product categories. Cosmetic companies are expanding portfolios with functional botanical extracts to address sensitive skin and wellness trends. Symrise’s launch of SymCalmin® Avena from certified organic German oats, which soothes sensitive skin and received COSMOS certification, highlights innovation rooted in sustainability and traceability. Traceably sourced essences are increasingly used in high-value skincare and food & beverage products. This dynamic underscores the region’s commitment to quality, compliance, and environmental stewardship.

Asia Pacific Flower-Based Essence Market Trends

Asia Pacific is projected to be the fastest-growing regional market for flower-based essences, projected to expand at roughly 7.4% CAGR through 2033, with China, India, and ASEAN economies driving expansion through rising disposable incomes and strong demand for premium personal care, functional beverages, and wellness products. Government initiatives such as India’s botanical manufacturing support under AYUSH frameworks are actively promoting botanical industries and encouraging standardized cultivation and processing of flower-based extracts. These policies bolster local production, reduce import dependency, and accelerate regional value-chain development. Cost-competitive manufacturing and abundant raw material availability strengthen the region’s strategic role in global supply chains.

The market here is also being aided by traditional medicine integration and functional product innovation. Producers are tapping into high-value ingredients such as wild oat and bleeding heart extracts for wellness and cosmetic formulations. A notable development is Jiaherb’s expansion of its lab and R&D facility in Xi’an, China, enhancing local capabilities in natural ingredient research, extraction, and quality control. This investment enables faster development of regionally relevant botanical solutions and supports export-oriented production. Enhanced extraction technologies and sustainable cultivation practices help deliver consistent quality, making Asia Pacific an innovation and growth hub in the global flower-based essence market.

Competitive Landscape

The global flower-based essence market structure is moderately consolidated, with leading players such as Symrise, Givaudan, Firmenich, Mane, and Takasago collectively controlling a significant portion of market revenue. These established companies leverage extensive supplier networks, deep expertise in botanical extraction, and integrated flavor, fragrance, and cosmetic solutions. They also invest heavily in R&D and sustainable sourcing initiatives, focusing on advanced extraction technologies, solvent-free distillation, and standardized quality processes to maintain a competitive edge in premium natural ingredients.

At the same time, regional and niche players such as Jiaherb, Lilit Botanicals, and Weleda are targeting specialty flower extracts and functional wellness applications, often focusing on high-value segments and localized production. Barriers such as agricultural dependency, regulatory compliance, and quality standardization limit new entrants, but innovations in extraction technology and sustainable cultivation allow smaller players to differentiate. Market consolidation is expected to continue gradually, driven by strategic acquisitions, partnerships between global leaders and local suppliers, and collaborations with wellness and food & beverage brands to expand geographically and technologically.

Key Industry Developments

- In October 2025, Givaudan expanded its partnership with LBB Specialties to distribute a broader range of ingredients across the Midwest and Eastern U.S., covering skin, hair, makeup, and body care. Simultaneously, both Givaudan and IFF strengthened their India operations through factory expansions and a new scent creative center in Mumbai, housing advanced labs and over 100 employees.

- In May 2025, the International Horticulture Goyang Korea 2025 festival was hosted under the theme “Flower, Fantasy, and Fragrance”, highlighting horticultural innovation, smart farming solutions, and flower-based ingredients such as teas and extracts. The event provided small & medium enterprises (SMEs) with commercial channels for botanical products in beauty and wellness industries.

- In March 2025, Starbucks Reserve unveiled its 2025 spring menu, featuring botanical flavors such as chamomile-infused lattes and cherry plum essences in limited-edition beverages. The collection highlights natural flower extracts for sophisticated, wellness-inspired taste profiles available at Reserve Roasteries.

Companies Covered in Flower-Based Essence Market

- Givaudan

- Firmenich

- Symrise

- International Flavors & Fragrances

- Robertet Group

- Takasago International

- Mane SA

- Sensient Technologies

- Döhler Group

- Kerry Group

- Treatt Plc

- Synthite Industries

Frequently Asked Questions

The global flower-based essence market is projected to reach US$ 63.2 million in 2026

Rising consumer preference for natural, clean-label ingredients, expanding applications in cosmetics, fragrances, and functional beverages, and technological advancements in extraction and processing methods are key growth drivers.

The market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Opportunities include increasing adoption in pharmaceutical and wellness formulations, rising demand from emerging markets, and improvements in extraction efficiency and sustainability, enabling premium product development.

Some of the key players in the market include Symrise, Givaudan, Firmenich, Mane, and Takasago.