- Animal Feed & Additives

- Feed Processing Market

Feed Processing Market Size, Share, and Growth Forecast, 2026 - 2033

Feed Processing Market by Equipment Type (Grinding, Mixing, Pelleting, Extrusion, Cooling), Form (Pellets, Mash, Crumbles, Others), Operation (Manual, Semi-Automatic, Automatic) and Regional Analysis for 2026-2033

Feed Processing Market Share and Trends Analysis

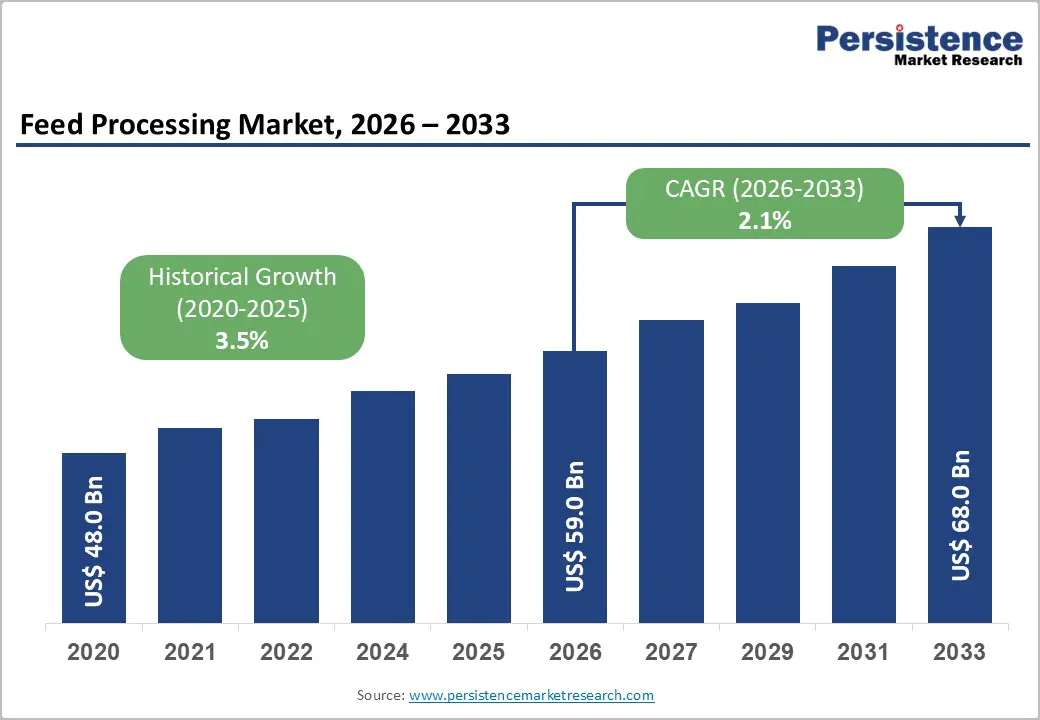

The global feed processing market size is likely to be valued at US$ 59.0 billion in 2026, and is projected to reach US$ 68.0 billion by 2033, growing at a CAGR of 2.1% during the forecast period 2026−2033. This market is encompasses machinery and integrated systems that convert raw agricultural inputs into nutritionally balanced feed for livestock, poultry, and aquaculture. Demand is increasing as global protein consumption is rising due to population growth and expanding middle-class purchasing power, particularly in emerging economies. Livestock producers are scaling operations to meet higher meat, dairy, and egg output targets, which is sustaining steady investment in feed mill capacity.

Equipment suppliers are supporting this demand through grinding, mixing, pelleting, extrusion, and drying technologies that improve throughput consistency and feed quality. Technological advancement is strengthening production efficiency and compliance across feed processing facilities. Automation systems are optimizing batching precision and reducing raw material loss, while precision formulation platforms are enabling accurate nutrient calibration aligned with species-specific growth requirements. Regulatory authorities are enforcing stricter feed safety and traceability standards, which is compelling producers to modernize infrastructure and implement quality monitoring systems. Energy-efficient machinery and digital monitoring tools are enhancing cost control and operational transparency.

Key Industry Highlights

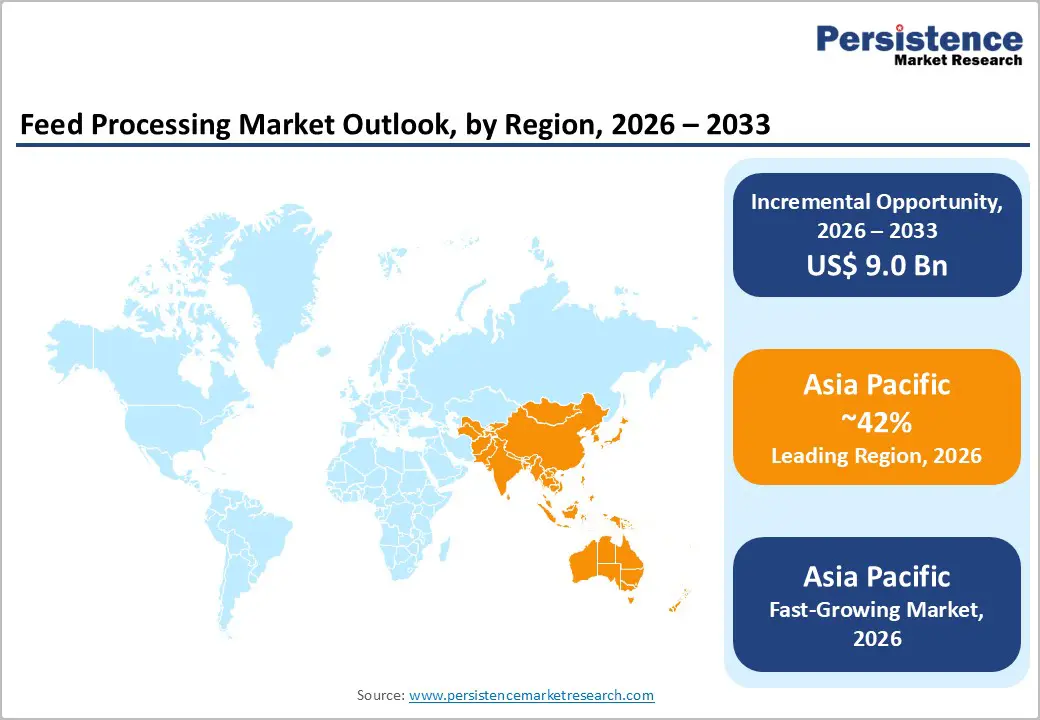

- Regional Dominance: Asia Pacific is likely to be the dominant and the fastest-growing market through 2033, accounting for approximately 42% share, driven by a massive livestock population.

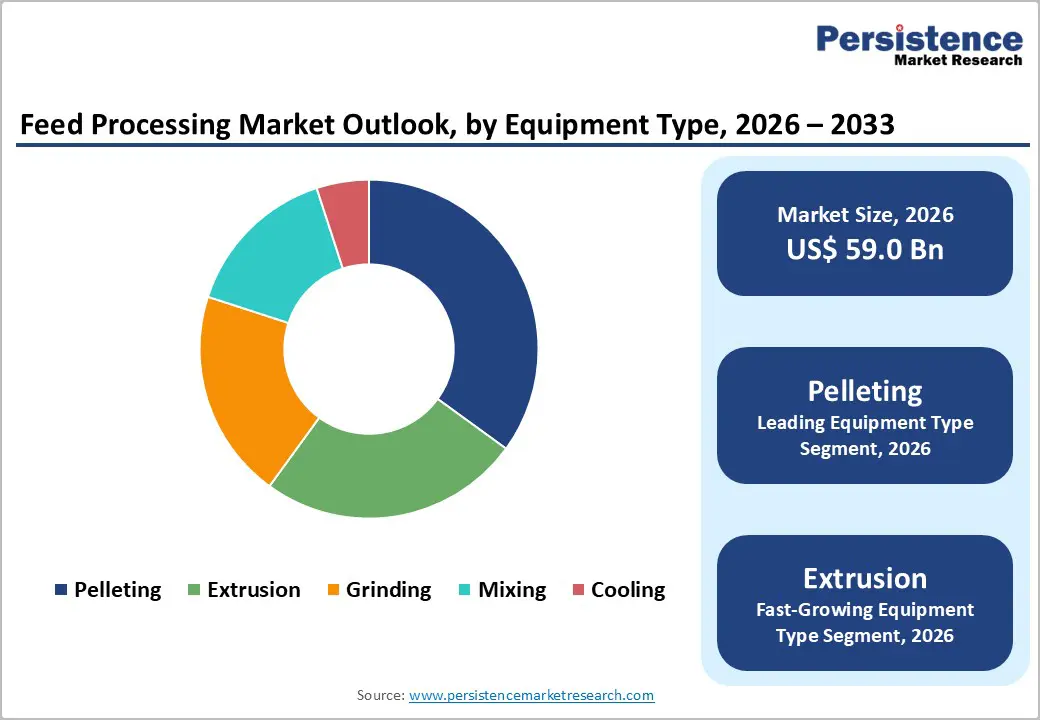

- Equipment Leadership: Pelleting is set to command around 35% revenue share in 2026, while extrusion is likely to be the fastest-growing segment from 2026 to 2033.

- Leading & Fastest-growing Form: Pellets are expected to capture roughly 65% of the revenue share in 2026, whereas mash is slated to record the highest 2026-2033 CAGR.

- December 2025: Fiji's Ministry of Agriculture and Waterways received agricultural machinery worth US$ 453,000 from the Republic of Korea to boost livestock feed production and pasture management.

| Key Insights | Details |

|---|---|

| Feed Processing Market Size (2026E) | US$ 59.0 Bn |

| Market Value Forecast (2033F) | US$ 68.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 2.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancement in Feed Processing Automation

The feed processing industry is actively integrating Industry 4.0 technologies into core production operations to enhance precision and efficiency. Manufacturers are deploying Internet of Things (IoT) sensors, artificial intelligence (AI) driven formulation software, and automated quality control systems across grinding, mixing, and pelleting lines. These digital tools are enabling continuous monitoring of temperature, moisture levels, particle size distribution, and blending consistency in real time. Predictive maintenance models are analyzing equipment performance data to detect wear patterns and schedule servicing before mechanical failures disrupt output. Precision dosing systems are regulating ingredient inclusion down to micro-additive levels, which is minimizing raw material loss and improving cost control.

Regulatory compliance is further accelerating adoption of advanced processing technologies. The United States Food and Drug Administration (FDA) Food Safety Modernization Act (FSMA) is establishing stringent preventive control requirements that compel feed mills to implement traceability and hazard monitoring systems. Comparable regulatory frameworks across Europe and Asia are reinforcing similar standards for feed hygiene and quality assurance. Producers are applying controlled thermal treatment, pelleting, and extrusion techniques to improve pathogen reduction, digestibility, and nutrient bioavailability. Enhanced processing efficiency is contributing to stronger livestock growth rates and improved feed conversion ratios. These measurable productivity gains are justifying capital investment in automation, data analytics, and energy-efficient machinery.

High Capital Investment Requirements and Financial Barriers

Feed processing facilities are requiring substantial capital outlays to establish complete production lines. Even small-scale mills must invest in grinding, mixing, and pelleting systems before achieving commercial viability. Large integrated plants are allocating significantly higher budgets to support continuous throughput, automated batching, and digital monitoring infrastructure. This capital intensity is creating high entry barriers for new participants and limiting expansion among smaller operators. Small and medium-sized enterprises (SMEs) in developing markets are encountering restricted access to formal financing channels, which is slowing modernization efforts. Many operators are relying on internal funds or informal credit structures, which is constraining scale upgrades and prolonging dependence on manual processing techniques. As a result, industry consolidation is progressing gradually in regions where funding ecosystems remain underdeveloped.

Operators are also managing ongoing operational costs that influence profitability. Equipment maintenance requires routine procurement of spare parts and preventive servicing schedules. Advanced systems are demanding skilled technicians who require specialized training programs to ensure optimal performance. Commodity price volatility is exerting pressure on already narrow profit margins, increasing investment risk sensitivity. Workforce development expenses are emerging as an additional adoption barrier in regions with limited technical education infrastructure. Modern automation platforms are requiring consistent technical oversight, which is raising human capital requirements. To address these challenges, suppliers and financial institutions are exploring structured financing arrangements and modular equipment designs that reduce upfront cost burdens.

Aquaculture Feed Segment Expansion and Specialized Processing Requirements

Global aquaculture production is expanding steadily as farmed fish output is surpassing traditional capture fisheries in overall volume. The sector is supplying the majority of seafood consumed worldwide, and projections are indicating continued growth as pressure on wild fish stocks is increasing. Aquafeed is representing the largest cost component for fish farmers, frequently accounting for the dominant share of operating expenditure in commercial aquaculture systems. Producers are prioritizing feed formulations that remain stable in water to prevent nutrient leaching and feed loss. Advanced processing technologies are ensuring structural durability, controlled buoyancy, and consistent nutrient dispersion during prolonged submersion. These quality attributes are directly influencing fish growth rates, feed conversion efficiency, and overall farm profitability.

Manufacturers are investing in extrusion systems, surface coating technologies, and pellet stabilization processes to enhance water resistance and species-specific nutrient delivery. Processing equipment is accommodating variable pellet diameters and density profiles to produce both floating and sinking feeds tailored to distinct aquaculture practices. Floating pellets are supporting surface-feeding species, while sinking variants are serving bottom-dwelling fish and shrimp operations. Major economies such as China, India, Indonesia, and Vietnam are leading aquaculture expansion, creating strong demand for industrial-scale feed manufacturing infrastructure. Equipment suppliers are strengthening their presence in these markets by offering modular production systems and localized technical support services.

Category-wise Analysis

Equipment Type Insights

Pelleting is poised to dominate in 2026, commanding approximately 35% of the feed processing market revenue share, driven by the pelleting process's critical role in improving feed digestibility, reducing ingredient segregation, and facilitating handling and transportation. Pelleted feed adoption accelerates across poultry, swine, and ruminant sectors, driving sustained demand for pelleting equipment. Manufacturers increasingly specify pelleted formulations for superior storage stability, transportation efficiency, and feed conversion performance. Advancements in pelleting technology amplify this growth trajectory. High-capacity pellet mills deliver greater throughput for large-scale operations. Energy-efficient designs reduce operational costs while maintaining consistent pellet quality. These innovations enable feed producers to meet expanding livestock production requirements with optimized processing capabilities.

Extrusion is likely to be the fastest-growing segment during the 2026-2033 forecast period, propelled by increasing demand for aquafeed and pet food requiring high-temperature, high-pressure processing. Twin-screw extruders enable precise control over cooking parameters, starch gelatinization, and protein denaturation, producing highly digestible feeds with superior water stability essential for aquaculture applications. The segment is further supported by growing adoption of extrusion technology for specialty ingredients including fish meal alternatives, rendering plant proteins more nutritionally available through the modification of molecular structures.

Form Insights

Pellets are slated to be the dominant application segment, capturing an estimated 65% of the feed processing market share in 2026. This is attributed to superior handling characteristics, reduced dust generation, improved feed conversion ratios and minimized ingredient segregation during storage and distribution. Pelleting also enables inclusion of heat-sensitive ingredients like enzymes and probiotics when applied post-pelleting via liquid coating systems. The pelleted segment serves diverse livestock sectors including poultry, swine, ruminants, and increasingly, aquaculture, with pellet specifications customized for species-specific requirements ranging from 2mm diameter for aquaculture to 10mm for ruminant applications.

Mash is expected to be the fastest-growing segment over the 2026-2033 forecast period, driven by cost considerations and suitability for young animals with underdeveloped digestive systems. Mash feed eliminates pelleting energy costs and associated equipment capital investment, making it economically attractive for price-sensitive markets and operations with limited processing infrastructure. The segment is experiencing renewed interest from organic and pasture-based livestock producers who prioritize natural feeding behaviors and minimal processing, aligning with consumer preferences for less processed animal products.

Operation Insights

Semi-automatic is anticipated to lead with an approximate 45% market share in 2026. Semi-automatic equipment experiences steady growth due to its optimal balance of cost-effectiveness and operational flexibility. Operators maintain manual control over critical process variables such as ingredient ratios and final quality checks, while automated components handle repetitive tasks including material conveying, grinding, and initial mixing. This hybrid approach appeals particularly to small and medium-sized feed mills serving regional livestock producers. These operations seek substantial productivity gains without committing capital to fully automated systems that require extensive technical infrastructure.

Automatic is projected to be the fastest-growing segment between 2026 and 2033, with its growth trajectory being charted by the superior efficiency, precision dosing, and simplified operations that such equipment offers. Large-scale feed manufacturers prioritize fully automated systems that eliminate manual intervention across grinding, mixing, pelleting, and quality control stages. Rising automation adoption accelerates this dominance as producers achieve substantial labor cost reductions and error elimination. Advanced systems incorporate programmable logic controllers, real-time process monitoring via sensors, and automated cleaning cycles between batches. These capabilities ensure consistent product quality and regulatory compliance while enabling 24/7 production schedules.

Regional Insights

Asia Pacific Feed Processing Market Trends

Asia Pacific market is likely to be both the leading and fastest-growing regional market for feed processing in 2026, accounting for approximately 42% of market share. China maintains regional dominance as the world's largest feed producer. The country processes massive volumes across poultry, swine, dairy, and aquaculture operations. India emerges as the fastest-growing secondary market. Dairy and poultry sector expansion drives substantial equipment demand. Vietnam, Thailand, and Indonesia contribute meaningfully through aquaculture leadership and livestock intensification. Regional manufacturers benefit from proximity to agricultural commodities. Established supply chains support efficient equipment component sourcing. Government initiatives accelerate modernization across the region. China advances its Rural Revitalization Strategy (RRS). India implements the National Livestock Mission (NLM).

These programs prioritize commercial feed production over traditional backyard farming. Urbanization shifts protein consumption patterns toward industrially processed feeds. Middle-class population growth creates sustained demand pressure. Manufacturers favor cost-effective, durable equipment designs. These solutions accommodate diverse operational scales from cooperative facilities to integrated agribusiness complexes. Strategic suppliers position for success by balancing premium automation capabilities with regionally competitive pricing. Local service networks prove essential for sustained market penetration. Aquaculture processing specialization creates distinct high-margin opportunities. The region's manufacturing cost advantages position Asia Pacific as the global hub for feed processing machinery production and technology adaptation.

Europe Feed Processing Market Trends

Europe is foreseen to occupy a prominent position within the global market for feed processing through 2033 on the back of technological sophistication and regulatory leadership. Germany leads regional performance with extensive compound feed production capacity. France, Spain, and the United Kingdom contribute meaningfully to market value. European Union (EU) regulatory frameworks establish industry benchmarks worldwide. The EU Feed Hygiene Regulation mandates rigorous contamination controls. Manufacturers invest heavily in advanced processing technologies. Sustainability imperatives shape equipment procurement decisions across the continent. The European Green Deal's Farm to Fork Strategy accelerates this transformation.

Processing systems prioritize traceability from raw materials through finished product. Cross-contamination prevention receives particular emphasis. Specialized equipment supports medicated, organic, and precision nutrition formulations. Circular economy principles gain widespread adoption. Facilities utilize food industry byproducts and former foodstuffs effectively. Energy-efficient technologies align with carbon reduction commitments. Western Europe's premium pet food sector drives demand for sophisticated extrusion and coating capabilities. Regional manufacturers excel with integrated solutions featuring advanced automation and Industry 4.0 connectivity. Strategic equipment suppliers establish competitive advantage through regulatory compliance expertise and sustainability-focused innovation.

North America Feed Processing Market Trends

North America commands a leading position in the feed processing market through unmatched industrialization and technological sophistication. The United States maintains regional dominance with extensive livestock operations requiring vast feed volumes. Commercial poultry, swine, and dairy sectors drive continuous equipment demand. United States FDA regulations establish rigorous safety standards across North American facilities. The FSMA mandates preventive controls and supplier verification programs. Innovation ecosystems accelerate processing technology advancement throughout the region. Equipment manufacturers collaborate with land-grant universities and industry associations.

These partnerships are focused on developing automation solutions, precision nutrition systems, and sustainable processing methods. Facility operators prioritize modernization investments over capacity expansion. Energy-efficient upgrades reduce operational expenses significantly. Flexible manufacturing lines accommodate specialty formulations such as organic, non-genetically modified organism (non-GMO), and antibiotic-free products. Pet food manufacturers require premium extrusion and coating capabilities. Regional suppliers gain competitive advantage through integrated automation platforms and Industry 4.0 connectivity. Strategic equipment providers succeed by combining regulatory compliance expertise with customized innovation roadmaps tailored to North American operational priorities.

Competitive Landscape

The global feed processing market structure is moderately consolidated, dominated by leading players such as Bühler AG, ANDRITZ Group, Van Aarsen International, Zheng Chang Group, and Henan Richi Machinery Co., Ltd. These companies capture 35-40% of the market share in 2026. Several major players compete vigorously within the feed processing market to capture market share. Technological innovation, product development, strategic alliances, and mergers and acquisitions define the competitive dynamics.

Manufacturers prioritize advanced equipment that delivers superior efficiency and cost-effectiveness. Their solutions address rising demand for premium feed formulations across livestock and aquaculture sectors. Research and development investments accelerate integration of automation systems and digital technologies. These enhancements improve processing precision, operational productivity, and quality consistency. Companies establish competitive differentiation through comprehensive service networks and customized engineering capabilities tailored to regional production requirements.

Key Industry Developments

- In December 2025, Tetra Pak Processing Equipment SIA acquired Bioreactors.net, a Latvian firm with nearly 30 years of expertise in bioreactor systems for biomass and precision fermentation in the "New Food" category. The acquisition enhances Tetra Pak's fermentation capabilities, integrating Bioreactors.

- In November 2025, FAMSUN launched its premium pet food equipment brand FAMSCEND at a global ceremony in Yangzhou, China, marking its entry into the pet food and healthy human food equipment market with a mission to "Innovate to nourish a better world."

- In September 2025, Tanmiah Food Company launched a state-of-the-art poultry processing plant in Al Majmaa and a 40 MT/hour automated feed mill in Dahna, Saudi Arabia, to enhance food security and operational efficiency as part of Vision 2030.

Companies Covered in Feed Processing Market

- Bühler AG

- ANDRITZ Group

- CPM (California Pellet Mill Company)

- Van Aarsen International

- Zheng Chang Group

- Alapala Group

- Ottevanger Milling Engineers

- Wenger Manufacturing

- Muyang Group

- Anderson International

- SKIOLD A/S

- Fragola SpA

- Wynveen International

- Henan Richi Machinery Co., Ltd.

- GEA Group

Frequently Asked Questions

The global feed processing market is projected to reach US$ 59.0 billion in 2026.

The market is driven by rising livestock production and aquaculture expansion, which necessitate advanced processing equipment for consistent feed quality and nutritional optimization.

The market is poised to witness a CAGR of 2.1% from 2026 to 2033.

Emerging market mechanization, aquaculture feed specialization, and sustainability-focused processing technologies targeting Asia Pacific economies can open up several lucrative opportunities.

Bühler AG, ANDRITZ Group, Van Aarsen International, Zheng Chang Group, and Henan Richi Machinery Co., Ltd are some of the key players in the market.