- Pharmaceuticals

- Enteral Feeding Formula Market

Enteral Feeding Formula Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Enteral Feeding Formula Market by Product (Standard Formula and Disease Specific Formula), by Flow Type (Intermittent Feeding Flow and Continuous Feeding Flow), by Stage (Adult and Pediatric), by Indication (Alzheimer’s, Nutrition Deficiency, Cancer Care, Diabetes, Chronic Kidney Diseases, and Others), by End-user (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, Home Care Settings, and Others), and Regional Analysis from 2026 to 2033

Enteral Feeding Formula Market Share and Trends Analysis

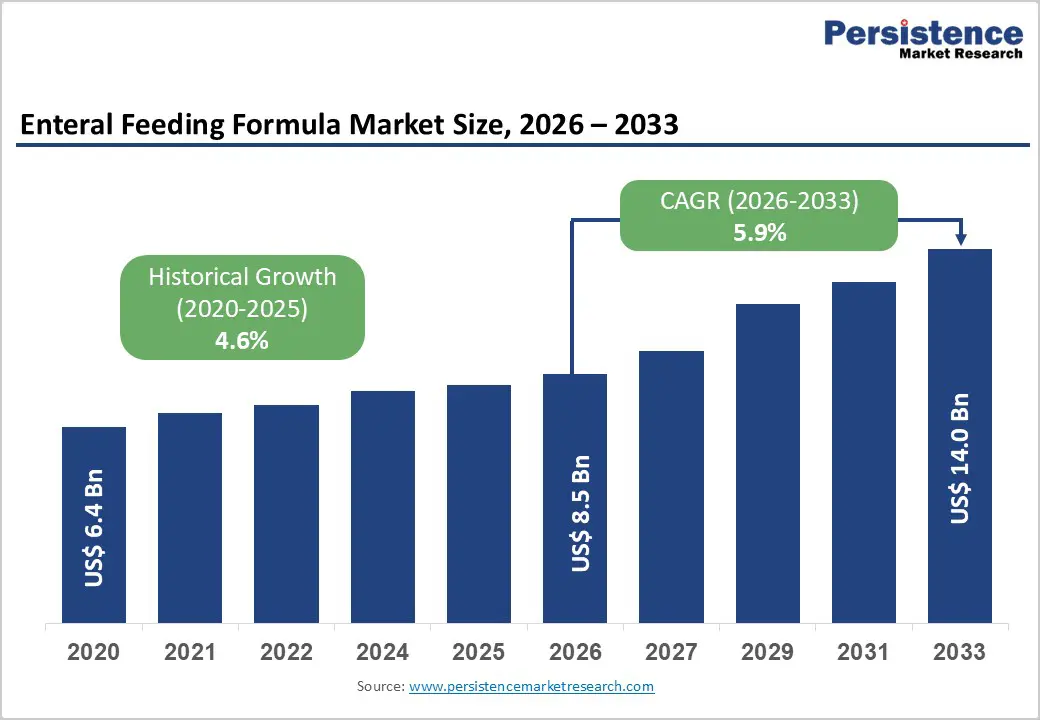

The global enteral feeding formula market size is estimated to grow from US$ 8.5 billion in 2026 to US$ 14.0 billion by 2033. The market is projected to record a CAGR of 5.9% during the forecast period from 2026 to 2033.

Global demand for enteral feeding formula is rising steadily, driven by the increasing prevalence of chronic diseases, neurological disorders, gastrointestinal conditions, cancer, and age-related illnesses that impair normal oral nutrition intake. Growing volumes of surgical procedures, trauma cases, and intensive care admissions are expanding the patient pool requiring enteral nutritional support across hospitals and long-term care facilities.

The rapidly aging global population is further increasing demand for enteral feeding formulas to manage malnutrition, dysphagia, and mobility-limited patients. Growth in home healthcare and post-acute care services is accelerating adoption of both standard and disease-specific enteral formulas outside traditional hospital settings. Advancements in product formulation, including disease-targeted nutrition, improved digestibility, immune-enhancing ingredients, and enhanced packaging formats, are improving patient tolerance, safety, and clinical outcomes. Increasing emphasis on clinical nutrition, infection prevention, and cost-effective patient management is supporting broader adoption. Rising healthcare investments, expanding hospital infrastructure, and improved access to nutritional therapy in emerging markets continue to drive long-term global market expansion.

Key Industry Highlights

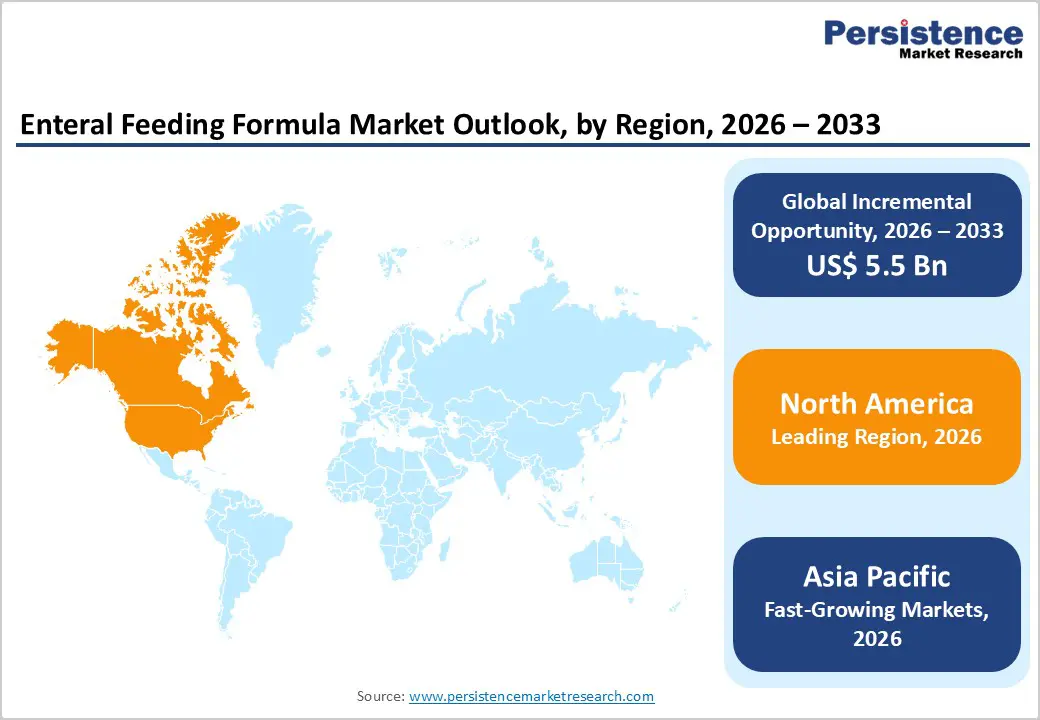

- Leading Region: North America holds the largest market share at 48.5%, supported by advanced healthcare infrastructure, high diagnosis rates of chronic and critical illnesses, strong reimbursement frameworks, and widespread adoption of clinical nutrition protocols.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to a large patient pool, rising surgical and critical care volumes, rapid expansion of hospitals and long-term care facilities, and increasing government investment in healthcare infrastructure.

- Leading Product Segment: Standard formulas dominate the market due to their broad applicability, cost-effectiveness, and widespread use across hospitals, intensive care units, and long-term nutritional support settings.

- Fastest-Growing Product Segment: Disease specific formula are witnessing rapid growth as demand increases for targeted nutritional management in chronic disease care, oncology, metabolic disorders, and homecare settings.

- Leading Flow Type Segment: Intermittent feeding flow remains the largest usage segment due to its flexibility, lower cost, and extensive adoption across hospitals and long-term care facilities.

- Fastest-Growing Flow Type Segment: Continuous feeding flow products are expanding rapidly, driven by improved patient tolerance, enhanced nutritional delivery, and increasing adoption in critical care and home healthcare environments.

| Key Insights | Details |

|---|---|

| Enteral Feeding Formula Market Size (2026E) | US$ 8.5 Bn |

| Market Value Forecast (2033F) | US$ 14.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rising Chronic Disease Burden and Advancements in Enteral Nutrition Formulations Driving Market Growth

The rising prevalence of chronic and critical diseases is a major factor accelerating demand for enteral feeding formulas globally. Increasing incidence of cancer, neurological disorders such as stroke and Parkinson’s disease, gastrointestinal conditions, and metabolic disorders is significantly expanding the patient population unable to meet nutritional needs through normal oral intake. These conditions often require long-term or repeated nutritional intervention to prevent malnutrition, support immune function, and improve treatment outcomes. Growing numbers of intensive care admissions, complex surgical procedures, and prolonged hospital stays further reinforce reliance on enteral nutrition as a preferred and clinically effective feeding route. Additionally, aging populations worldwide are more vulnerable to chronic illness and swallowing difficulties, increasing sustained demand for enteral feeding across hospitals, long-term care facilities, and homecare settings.

Additionally, technological advancements in enteral feeding formula development are strengthening clinical adoption and improving patient outcomes. Innovations such as immune-enhancing ingredients, peptide-based and elemental formulations, optimized macronutrient profiles, and improved fiber composition are enhancing digestibility and nutrient absorption, particularly for critically ill and compromised patients. Advances in formulation stability, taste masking, and ready-to-use packaging are improving tolerance and ease of administration. These developments enable more personalized and disease-specific nutritional management, increase clinician confidence, and support broader use of enteral feeding formulas across diverse care settings, collectively driving sustained market growth.

Restraints - Cost Constraints and Feeding-Related Clinical Risks Limiting Market Adoption

The high cost of disease-specific and specialty enteral feeding formulas remains a significant restraint on market growth, particularly in cost-sensitive regions and healthcare systems with limited reimbursement coverage. Specialized formulations designed for oncology, renal, diabetic, or critical care patients often carry premium pricing due to advanced ingredients, targeted nutrient profiles, and stringent manufacturing standards. In many emerging markets, healthcare budgets are constrained, and reimbursement for clinical nutrition products is either partial or absent, leading providers to favor lower-cost standard formulas or alternative nutritional approaches. Even in developed markets, cost containment pressures on hospitals and long-term care facilities can limit widespread adoption of premium enteral products, especially for long-term use.

In addition to cost barriers, the risk of feeding-related complications can influence clinician preference and restrict enteral feeding utilization in certain patient populations. Complications such as aspiration pneumonia, gastrointestinal intolerance, diarrhea, bloating, and tube-related issues including blockage or dislodgement may occur, particularly among critically ill or neurologically impaired patients. These risks require careful patient selection, monitoring, and staff training, increasing clinical workload. In cases where complication risks are elevated, clinicians may opt for alternative nutrition methods, thereby moderating overall adoption and acting as a restraint on market expansion.

Opportunity - Expansion of Personalized Nutrition and Home Enteral Feeding Creating New Growth Avenues

The growing demand for disease-specific and personalized nutrition is creating significant growth opportunities in the enteral feeding formula market. Increasing clinical emphasis on targeted nutritional therapy for oncology, diabetes, renal, and neurological patients is driving the development and adoption of specialized formulations tailored to specific metabolic and therapeutic needs. Personalized enteral nutrition helps improve treatment tolerance, reduce complications, and support better clinical outcomes, particularly in patients requiring long-term nutritional support. Advances in nutritional science, including optimized protein profiles, immune-modulating ingredients, and condition-specific micronutrient blends, are enabling more precise nutritional management. As awareness of the role of nutrition in disease recovery continues to rise, healthcare providers are increasingly integrating personalized enteral feeding strategies into standard care protocols.

Furthermore, increasing adoption of home enteral nutrition (HEN) is opening new demand channels beyond traditional hospital settings. Growth in homecare services, early discharge programs, and patient preference for at-home treatment are accelerating the use of enteral feeding formulas in residential environments. HEN offers benefits such as improved quality of life, reduced hospitalization costs, and greater patient comfort, making it an attractive option for long-term nutrition management. Expanding availability of user-friendly feeding systems, caregiver training programs, and improved reimbursement support in select markets is further encouraging adoption, supporting sustained market growth.

Category-wise Analysis

By Product, Standard Formulas Maintain Market Leadership through Broad Clinical Applicability

The standard formula segment is projected to dominate the global enteral feeding formula market in 2026, accounting for a revenue share of 54.0%. Segment leadership is driven by the extensive clinical use of standard enteral formulas across acute care hospitals, post-operative recovery settings, intensive care units, and long-term care facilities. These formulas are widely prescribed for patients experiencing malnutrition, dysphagia, neurological impairment, gastrointestinal disorders, and critical illness where normal oral intake is compromised. Standard formulas offer balanced nutritional profiles, consistent caloric density, and broad compatibility with feeding tubes, making them suitable for a wide range of patient populations. High clinician familiarity, established clinical guidelines, and standardized hospital procurement policies further support widespread adoption. Continuous improvements in formulation stability, nutrient absorption, fiber content, and packaging formats are enhancing patient tolerance and safety. The availability of multiple caloric concentrations and ready-to-use liquid formats supports use across diverse care settings, reinforcing the dominant position of standard formulas within the overall market.

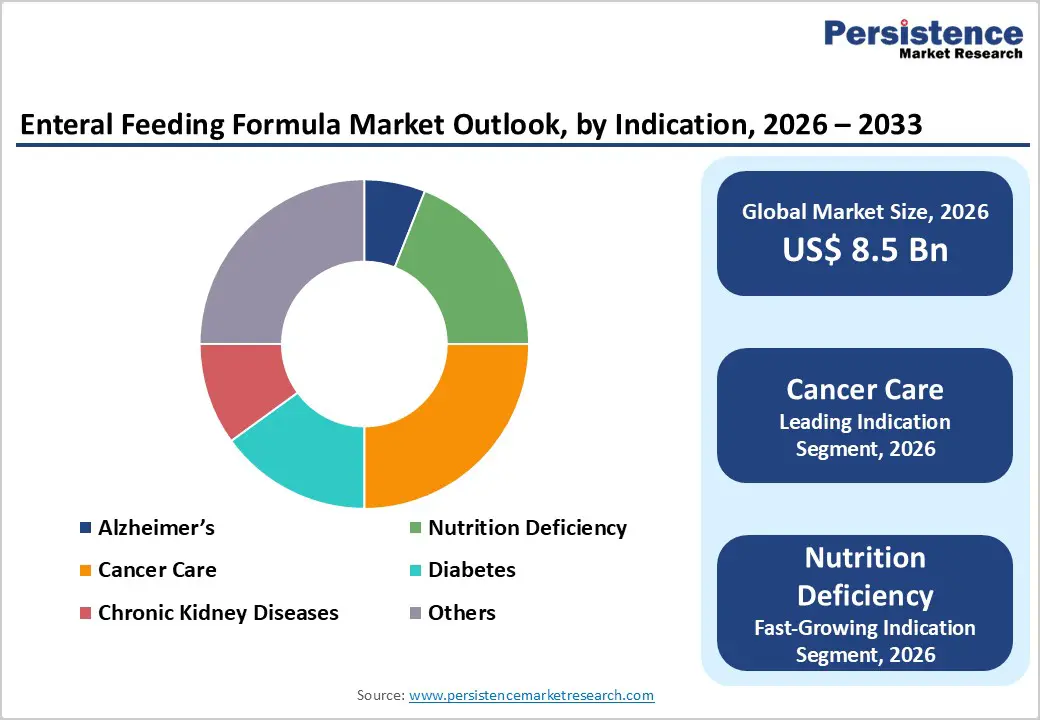

By Indication, Cancer Care Emerges as the Largest Application Segment

The cancer care segment is projected to dominate the global enteral feeding formula market in 2026, accounting for a revenue share of 25.0%. This leadership is driven by the high prevalence of cancer-related malnutrition resulting from chemotherapy, radiotherapy, surgical interventions, and disease-associated metabolic changes. Enteral feeding formulas play a critical role in maintaining nutritional status, supporting immune function, and improving treatment tolerance in oncology patients. Long treatment durations and repeated nutritional interventions increase reliance on enteral nutrition across hospitals, oncology centers, and homecare settings. Growing global cancer incidence, coupled with aging populations, continues to expand the patient pool requiring sustained nutritional support. Advances in disease-specific formulations, including high-protein, immune-modulating, and energy-dense formulas, are improving clinical outcomes and patient compliance. Additionally, increasing emphasis on early nutritional intervention in oncology care pathways and supportive reimbursement frameworks in developed markets are reinforcing the dominant position of cancer care within the enteral feeding formula market.

By End-user, Hospitals Lead Demand Due to High-Acuity and Critical Care Utilization

The hospitals segment is projected to dominate the global enteral feeding formula market in 2026, accounting for a revenue share of 60.0%. Hospitals remain the primary demand centers due to high volumes of surgical procedures, trauma admissions, oncology treatments, and critically ill patients requiring enteral nutritional support. Intensive care units, emergency departments, and specialized wards rely heavily on enteral feeding formulas to ensure accurate, continuous, and clinically monitored nutrition delivery. Centralized procurement systems, standardized feeding protocols, and availability of trained clinical nutrition teams support consistent utilization across hospital settings. While specialty clinics and ambulatory surgery centers increasingly use enteral nutrition for short-term support, hospitals continue to dominate due to their role in managing complex, high-acuity cases and long hospital stays. Ongoing investments in critical care infrastructure, clinical nutrition programs, and patient safety initiatives further strengthen hospital leadership within the global enteral feeding formula market.

Region-wise Insights

North America Enteral Feeding Formula Market Trends

The North America enteral feeding formula market is expected to dominate globally with a value share of 48.5% in 2026, led primarily by the United States. The region benefits from a highly advanced healthcare infrastructure, widespread availability of clinical nutrition services, and strong integration of enteral feeding protocols across hospitals and long-term care facilities. High prevalence of chronic diseases such as cancer, neurological disorders, diabetes, and gastrointestinal conditions is driving sustained demand for enteral nutrition. A rapidly aging population further increases reliance on enteral feeding formulas to manage age-related malnutrition, dysphagia, and post-acute care needs.

North America demonstrates strong adoption of both standard and disease-specific formulas, supported by favorable reimbursement policies and well-established clinical guidelines. The presence of leading enteral nutrition manufacturers, robust research activity, and continuous product innovation strengthens regional leadership. Growth in home healthcare and post-acute care services is expanding usage beyond hospitals, particularly for long-term nutrition management. Strong regulatory oversight, emphasis on patient safety, and high awareness of clinical nutrition benefits continue to support stable market dominance across the region.

Europe Enteral Feeding Formula Market Trends

The Europe enteral feeding formula market is expected to grow steadily, supported by a rapidly aging population and rising prevalence of chronic diseases, cancer, and neurological disorders. Countries such as Germany, the U.K., France, Italy, and the Nordic nations are major contributors due to well-developed public healthcare systems and strong access to hospital and long-term care services. European healthcare systems emphasize early nutritional assessment, clinical nutrition integration, and cost-effective patient management, supporting consistent adoption of enteral feeding formulas.

The region shows increasing utilization of standardized and disease-specific formulas aligned with clinical guidelines and evidence-based care pathways. Growth in rehabilitation centers, elderly care facilities, and outpatient services is further expanding demand. Strong regulatory oversight, focus on product quality, and preference for clinically validated formulations support stable procurement patterns. Additionally, increasing investments in homecare services, chronic disease management, and integrated care models are expected to sustain long-term market expansion across Europe, despite pricing pressures within public healthcare systems.

Asia Pacific Enteral Feeding Formula Market Trends

The Asia Pacific enteral feeding formula market is expected to register a relatively higher CAGR of around 7.9% between 2026 and 2033, driven by rapid healthcare infrastructure development and improving awareness of clinical nutrition. Countries including China, India, Japan, South Korea, and Southeast Asian nations are witnessing rising diagnosis rates of cancer, neurological disorders, gastrointestinal diseases, and critical illnesses requiring enteral feeding support. Expanding geriatric populations and increasing surgical volumes are significantly increasing demand for enteral nutrition across hospitals and long-term care facilities.

Government investments in healthcare modernization, hospital expansion, and nutrition-focused care programs are accelerating market adoption. Growth of private hospitals, medical tourism, and improving availability of enteral nutrition products are enhancing market penetration across urban and semi-urban areas. Rising affordability of standard formulas, increasing clinician awareness, and growing acceptance of home-based enteral nutrition are expected to sustain strong long-term growth across the Asia Pacific region.

Competitive Landscape

The global enteral feeding formula market is highly competitive, with strong participation from companies such as Danone, NESTLÉ S.A., Abbott, Mead Johnson & Company, LLC, Fresenius Kabi AG, and B. Braun SE. These companies leverage broad clinical nutrition portfolios, strong relationships with hospitals and long-term care providers, advanced manufacturing capabilities, and extensive global distribution networks.

Competitive strategies focus on expanding disease-specific formulations, improving nutritional efficacy and digestibility, and supporting clinical nutrition across critical care and chronic disease management. Ongoing product innovation, clinical validation, professional education, and geographic expansion in emerging markets continue to intensify competition and drive market evolution.

Key Developments:

- In January 2026, Protara Therapeutics, Inc. (TARA) announced that the U.S. FDA granted Breakthrough Therapy and Fast Track designations to TARA-002 for pediatric patients with macrocystic and mixed cystic lymphatic malformations. Pediatric patients undergoing treatment for rare lymphatic disorders often experience feeding challenges and post-treatment nutritional deficiencies, increasing reliance on enteral nutrition as supportive care. The designation highlights growing focus on pediatric rare diseases and reinforcing the importance of hospital-based and home enteral feeding formula utilization as part of comprehensive patient management.

- In June 2025, Elgan Pharma Ltd. and Chiesi Farmaceutici S.p.A. announced the dosing of the first infants in FIT-PIV, a Phase 3 clinical study evaluating ELGN-2112 for the treatment of intestinal malabsorption in preterm infants. Intestinal malabsorption is a condition that frequently necessitates specialized pediatric enteral feeding formulas to ensure adequate nutrient absorption and growth. The study highlights the persistent clinical need for targeted nutritional support in vulnerable neonatal populations, indirectly supporting demand for disease-specific and elemental enteral feeding formulas used alongside pharmacological interventions.

Companies Covered in Enteral Feeding Formula Market

- Danone

- NESTLÉ S.A.

- Abbott

- Mead Johnson & Company, LLC

- Fresenius Kabi AG

- B. Braun SE

- Otsuka Holdings Co., Ltd.

- Nutritional Medicinals, LLC

- Kate Farms

- Medtrition Inc.

- Victus

- Global Health Products, Inc.

- Meiji Holdings Co., Ltd.

- Reckitt

- Others

Frequently Asked Questions

The global enteral feeding formula market is projected to be valued at US$ 8.5 Bn in 2026.

Rising prevalence of urological disorders, aging populations, increasing surgical volumes, and growing demand for long-term catheterization across hospital and homecare settings are driving the global Enteral Feeding Formula market.

The global enteral feeding formula market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Expansion of home healthcare, rising adoption of disposable and infection-control drainage systems, and growing demand from emerging markets present key growth opportunities.

Danone, NESTLÉ S.A., Abbott, Mead Johnson & Company, LLC, Fresenius Kabi AG, and B. Braun SE are some of the key players in the enteral feeding formula market.