- Technology

- Drone Payload Market

Drone Payload Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Drone Payload Market By Type (EO/IR, Cameras, Search and Rescue, Signal Intelligence, Electronics Intelligence, Communication Intelligence, Maritime Patrol Radar, Laser Sensors, CBRN Sensors, Optronics), End-user (Defence, Commercial) and Regional Analysis for 2026 - 2033

Drone Payload Market Size and Trends Analysis

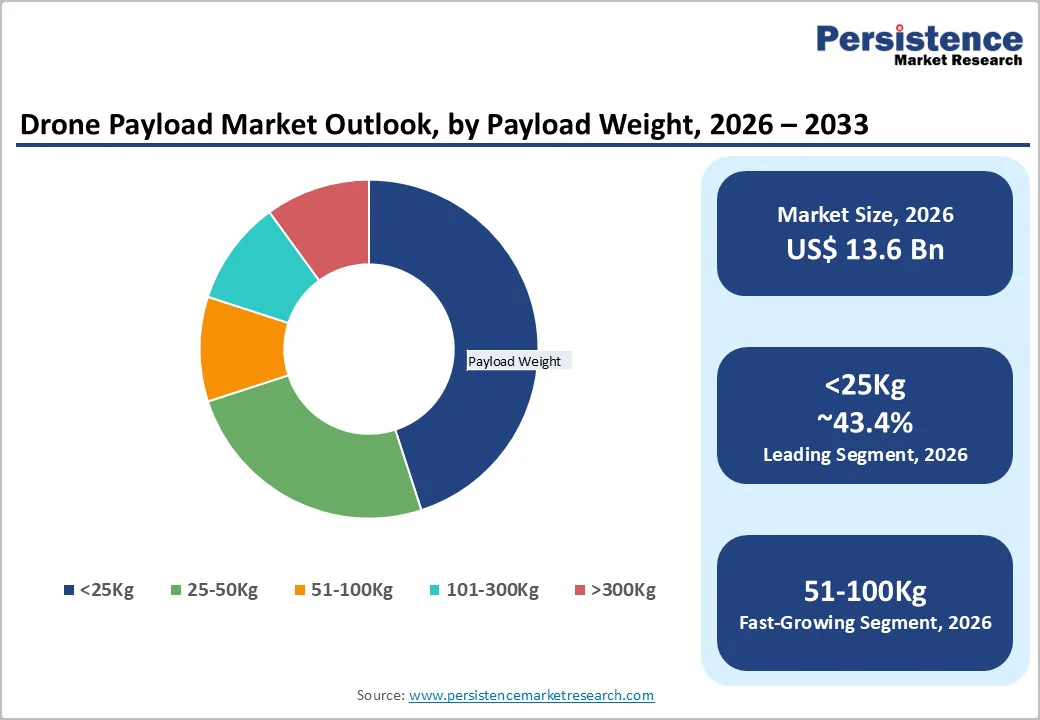

The global drone payload market size was valued at US$ 13.6 billion in 2026 and is projected to reach US$ 32.4 billion by 2033, growing at a CAGR of 13.2% between 2026 and 2033.

The market's acceleration is propelled by three primary catalysts: escalating global defense expenditures, driving advanced ISR (Intelligence, Surveillance, and Reconnaissance) payload procurement, rapid technological advancement in sensor miniaturization and AI-powered data analytics, and expanding commercial drone applications across agriculture, infrastructure inspection, logistics, and emergency response sectors.

Key Industry?Highlights:

- Product Segment Leadership: EO/IR (Electro-Optical/Infrared) payloads lead the market with 25.4% share, supported by strong defense surveillance demand, ISR missions, and multi-spectrum target tracking. Camera payloads emerge as the fastest-growing product category at 16% CAGR, driven by rapid adoption in commercial drones, mapping, inspection, and real-time imaging applications.

- Payload Capacity Dynamics: The <25 kg class maintains dominance with 43.4% share, enabled by widespread deployment in tactical surveillance drones, commercial UAVs, and small-platform reconnaissance missions. The 51-100 kg segment records the fastest growth at 16% CAGR, reflecting increasing procurement of medium-altitude UAV systems and expanding defense modernization programs.

- End-Use Application Patterns: Defense remains the leading end-user segment, accounting for 65% of total demand, driven by ISR expansion, border surveillance, and strategic intelligence missions. The commercial segment grows fastest at 18% CAGR, supported by BVLOS regulation progress, industrial inspection, agriculture monitoring, and growing commercial drone fleets.

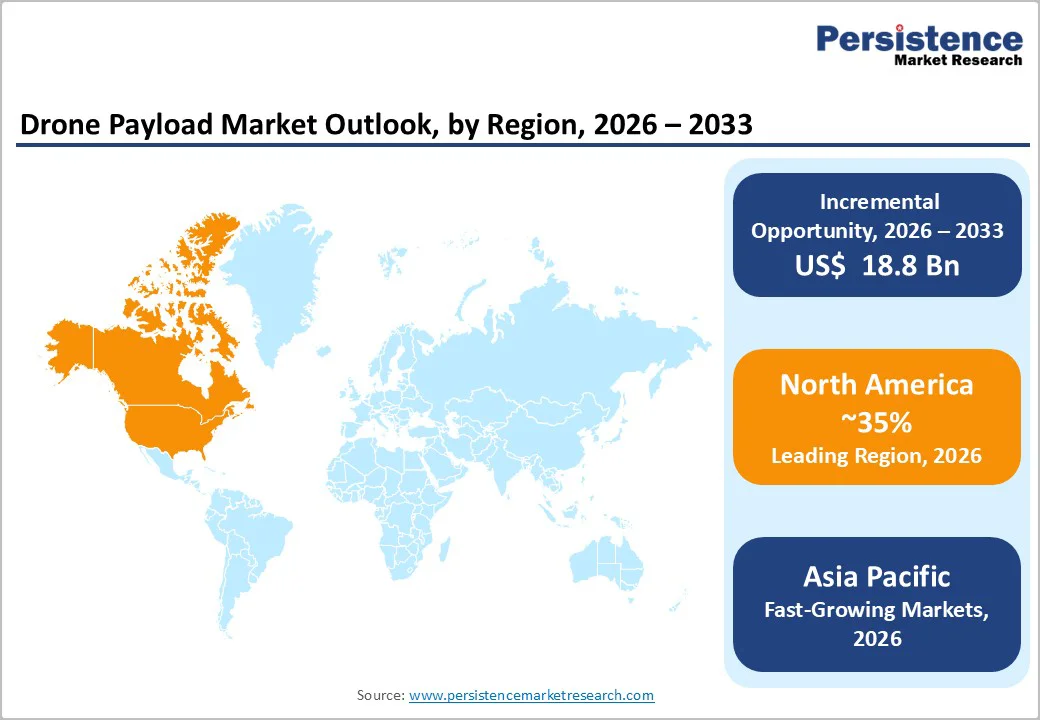

- Regional Growth Patterns: North America retains market leadership with 36% share, attributed to strong defense budgets, ISR program continuity, and early UAV technology adoption. Asia Pacific is the fastest-growing region at 15% CAGR, led by China’s manufacturing scale advantage and India’s rapidly modernizing defense procurement ecosystem.

- Competitive Landscape Trends: Major defense contractors including Lockheed Martin, Northrop Grumman, BAE Systems, and L3Harris control 55% of the defense payload market, supported by vertically integrated supply chains and technological scale advantages. Industry consolidation continues to elevate entry barriers, reinforcing leadership positions despite emerging competition.

| Key Insights | Details |

|---|---|

| Drone Payload Market Size (2026E) | US$ 13.6 Bn |

| Market Value Forecast (2033F) | US$ 22.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.2% |

| Historical Market Growth (CAGR 2020 to 2024) | 12.7% |

Market Dynamics

Drivers - Rising Global Defense Expenditures and Military ISR Modernization

Escalating geopolitical tensions and military modernization programs represent the primary market expansion catalyst, with global defense spending reaching US$ 2.24 trillion in 2022 (3.7% year-on-year increase according to Stockholm International Peace Research Institute), driving substantial procurement of advanced drone payload systems.

Modern military operations increasingly depend on unmanned systems equipped with sophisticated payloads for intelligence, surveillance, reconnaissance (ISR), and precision targeting capabilities.

The U.S. Department of Defense maintains the largest UAV budget globally, with substantial allocations toward advanced EO/IR sensors, SIGINT systems, and weapon payloads enabling enhanced situational awareness and combat effectiveness.

Defense segment commands 65% of total market revenue in 2024 - 2025, reflecting sustained government procurement prioritization. NATO member nations accelerate UAV payload investments following lessons learned from contemporary conflicts, with drone-based reconnaissance and electronic warfare systems demonstrating operational superiority.

Technological Advancement in Sensor Miniaturization and AI-Powered Analytics

Continuous innovation in MEMS (Micro-Electro-Mechanical Systems), sensor fusion technology, and edge computing enables lighter, more capable payloads supporting expanded drone operational envelopes and mission complexity.

Miniaturization advances have reduced payload weights by 40-50% over five years while simultaneously enhancing sensor resolution, spectral range, and data processing capabilities. Modern EO/IR gimbals deliver stabilized high-definition imaging across visible and infrared spectra with weights under 2kg, enabling deployment on small commercial platforms previously limited to basic camera payloads.

Artificial intelligence integration transforms raw sensor data into actionable intelligence; AI-powered target recognition, anomaly detection, and automated threat assessment reduce operator workload while improving response times. On-board edge computing eliminates the latency inherent in cloud-based processing, enabling real-time decision-making critical for time-sensitive military and emergency response applications.

Restraints - Regulatory Complexity, Airspace Restrictions, and Privacy Concerns

Fragmented regulatory frameworks governing drone operations, airspace access limitations, and data privacy concerns create structural adoption barriers constraining commercial market expansion velocity. National aviation authorities maintain divergent operational requirements, certification standards, and airspace access policies, creating compliance complexity for multinational operators and payload manufacturers.

BVLOS operations essential for commercial logistics, agricultural, and infrastructure applications-remain restricted in most jurisdictions, limiting payload deployment scenarios and addressable market potential.

Privacy regulations concerning aerial surveillance create operational constraints in populated areas; European GDPR requirements and emerging data protection frameworks impose data collection, storage, and processing restrictions affecting commercial ISR applications.

High Development Costs, Integration Complexity, and Supply Chain Constraints

Advanced payload system development requires substantial R&D investment, specialized engineering expertise, and complex integration processes, creating cost barriers and lengthening product development cycles.

Sophisticated EO/IR, SIGINT, and electronic warfare payloads require specialized optical components, precision gimbal systems, and proprietary signal processing algorithms with development costs ranging from US$10 to-50 million per payload family. Platform integration complexity, adapting payloads to diverse drone airframes with varying power, weight, and communication architectures, creates engineering challenges extending deployment timelines by 12-24 months.

Supply chain dependencies on specialized semiconductors, precision optical components, and rare earth materials create procurement vulnerabilities; recent geopolitical tensions affecting semiconductor supply chains impacted payload production schedules across major manufacturers.

Tariff impacts between U.S. and international suppliers increase costs for precision gimbal systems and optical sensors, with 15% cost rise for surveillance and delivery drone applications.

Market Opportunities

Autonomous Drone Operations and AI-Powered Swarm Capabilities

Next-generation autonomous drone systems incorporating AI-enabled swarm coordination, autonomous mission execution, and multi-platform payload integration represent a high-growth opportunity segment commanding premium pricing and substantial R&D investment.

Swarm technology enables coordinated multi-drone operations where payload data fusion provides comprehensive situational awareness, impossible with single-platform deployments. Military applications include distributed ISR coverage, electronic warfare saturation, and coordinated strike operations leveraging synchronized payload activation.

Commercial applications encompass agricultural coverage optimization, large-scale infrastructure surveys, and search-and-rescue operations coordinating thermal, visual, and communication payloads across drone formations. Research indicates that autonomous operation capabilities drive 35-50% price premiums versus manually controlled systems, reflecting substantial value creation.

Emergency Response and Public Safety Payload Integration

Emergency response applications, including search and rescue, disaster assessment, law enforcement, and firefighting represent high-value commercial segment with critical operational requirements demanding advanced payload capabilities.

Search and rescue operations require thermal imaging, infrared sensors, and communication relay payloads enabling victim detection in challenging environments; current SAR drones reduce average rescue response times by 45% versus traditional ground-based search methodologies.

Disaster assessment applications leverage high-resolution imaging and 3D mapping payloads for rapid damage evaluation and resource allocation. Law enforcement agencies increasingly deploy surveillance and communication payloads for crowd monitoring, traffic management, and tactical operations. Market research indicates emergency response drone deployments growing at 18 % CAGR, substantially exceeding overall commercial segment growth.

Category Analysis

Product Insights

EO/IR sensor systems hold the largest market share at around 25.4%, retaining dominance into 2025 with a 23.29% share. Their leadership is driven by wide applicability in military ISR, commercial surveillance, and industrial inspection.

These payloads offer high-resolution visual and thermal imaging for day and night operations, enabling detection, tracking, and targeting. Stabilized gimbal-mounted EO/IR units with multi-spectral capability remain essential across defense and commercial sectors. Key players include FLIR Systems (Teledyne), L3Harris, and Leonardo.

Camera payloads are the fastest-growing segment, expanding at 16% CAGR due to rising commercial drone use in agriculture, construction, real estate, and media. Advancements in CMOS sensors, onboard processing, and lower pricing are accelerating adoption across consumer and professional markets.

Payload Weight Insights

Lightweight drone payloads under 25kg hold the largest market share at 43.4%, driven by widespread use of small multi-rotor and fixed-wing platforms. This weight class covers most commercial payloads, including cameras, multispectral sensors, LiDAR, and communication modules, benefiting from miniaturization that allows advanced EO/IR imaging, multisensor gimbals, and AI-enabled processing within compact units.

Their dominance is further supported by affordability, with compatible platforms priced around US$2,000-US$50,000, making them accessible for inspection, mapping, and imaging applications.

Medium-weight payloads (51-100kg) represent the fastest-growing category, powered by rising demand for MALE-class UAVs used in defense ISR missions. These platforms support multi-sensor fusion EO/IR, radar, and SIGINT offer greater endurance and mission capability than lightweight systems and are projected to grow at a strong 15% CAGR.

End-user Insights

The defense sector leads the drone payload market with around 65% share, driven by high-value government procurement and advanced ISR, electronic warfare, and combat requirements.

Defense payloads carry a significant price premium 300-500% above commercial systems due to ruggedization, security certification, and mission-critical performance. Major programs across the U.S., NATO, Asia Pacific, and the Middle East continue to reinforce segment dominance, with combat and combat-support missions holding the largest share.

In contrast, the commercial segment is the fastest-growing, expanding at 19% CAGR. Adoption is rising across agriculture, infrastructure inspection, logistics, cinematography, and public safety, supported by falling sensor prices and increasing performance parity with military systems. Regulatory progress like FAA Part 107 and BVLOS initiatives is expected to lift commercial share to 45% by 2033.

Regional market insights

North America Drone Payload Market Trends

North America commands 36% of the global drone payload market, representing an estimated market value of US$ 4.5 billion in 2026, with projected expansion to US$ 12 billion by 2033 at approximately 12% CAGR.

The United States dominates regional market with estimated US$ 3.51 billion market value in 2025, driven by substantial Department of Defense procurement, advanced commercial adoption, and innovation ecosystem concentration. Canada represents a secondary market with growing commercial drone deployment across agriculture, mining, and infrastructure sectors.

North American market demonstrates a consolidated competitive structure dominated by Lockheed Martin, Northrop Grumman, General Atomics, L3Harris, and Teledyne, collectively commanding 50-60% of the defense payload market.

FAA oversight framework emphasizes safety, security (counter-drone concerns), and airspace integration, with "Blue sUAS" initiatives promoting American-manufactured payloads addressing supply chain security concerns. Export control regulations (ITAR, EAR) constrain international market access but reinforce domestic manufacturing positioning.

Europe Drone Payload Market Trends

Europe represents approximately 22% of global drone payload market, estimated at US$ 3.0 billion in 2026 with projected expansion to US$ 7-8 billion by 2033 at approximately 12% CAGR.

Germany, United Kingdom, France, and Italy collectively represent 70-75% of European market value, with Germany maintaining largest market share driven by defense industry concentration and advanced manufacturing capabilities. European market demonstrates slower growth relative to Asia Pacific reflecting regulatory complexity and procurement cycle delays.

Germany dominates through defense industry concentration (Airbus, Hensoldt) and advanced manufacturing expertise; UK follows with substantial defense procurement and commercial innovation. France maintains strong position through defense industrial base (Thales, Safran) and Eurodrone program participation.

Eurodrone program joint development by Germany, France, Italy, and Spain represents substantial European payload opportunity, with June 2024 collaboration announced between Airbus and Thales Group advancing sensors and data processing capabilities. Spain and emerging Eastern European markets demonstrate defense modernization momentum following NATO alliance commitments.

Asia Pacific Drone Payload Market Trends

Asia Pacific represents approximately 25% of the global drone payload market, estimated at US$ 3.5 billion in 2026, with projected expansion to US$ 10 billion by 2033, reflecting 15% CAGR substantially exceeding the global average (13.2%).

The region demonstrates the highest absolute growth velocity driven by substantial defense procurement (China, India), commercial drone manufacturing dominance, and emerging agricultural applications. China commands approximately 40% of the value, while India represents the fastest-growing country market, driven by defense modernization and commercial expansion.

Asia Pacific manufacturing ecosystem provides substantial cost advantages: Chinese component suppliers, Taiwanese semiconductor fabrication, and regional assembly operations enable 25-40% cost reduction versus Western-manufactured equivalents. This cost advantage supports commercial payload accessibility, enabling mass-market adoption, though security concerns (DJI restrictions in U.S. government applications) create market fragmentation.

Competitive Landscape

Global companies are making significant R&D investments to create payloads that are lighter, more capable, and more efficient. To stay competitive, innovations like AI integration, longer-lasting batteries, and more accurate sensors are essential. They are also working on growing their footprints in important areas, including Asia Pacific, Europe, and North America.

Commercial segment demonstrates greater fragmentation, with DJI dominating consumer/prosumer categories while specialized manufacturers (FLIR/Teledyne, Headwall Photonics, Phase One) capture professional imaging segments. Defense contractors leverage long-standing government relationships, proprietary technology portfolios, and security certifications, creating formidable competitive barriers.

Key Industry Developments:

- In August 2025, Terra Drone Corporation, a prominent company specializing in drone technology and Urban Air Mobility (UAM), based in Japan, entered into a sales partnership agreement (hereinafter referred to as "the agreement") with PT. Yanmar Diesel Indonesia (hereinafter referred to as "Yanmar Diesel Indonesia"), a subsidiary of Yanmar Holdings Co., Ltd., is for the distribution of its internally developed agricultural drones.

- In June 2025, the International Rice Research Institute (IRRI) and Davao Unmanned Aerial Payload Type (DUAS) have reinforced their enduring collaboration by formalizing a Memorandum of Agreement (MOA) at the IRRI Headquarters located in Los Baños, Laguna.

Companies Covered in Drone Payload Market

- Elbit Systems Ltd

- IMSAR LLC

- BAE Systems PLC

- Parrot SA

- Draganfly Inc

- Teledyne FLIR LL

- Northrop Grumman Corporation

- Israel Aerospace Industries Ltd

- DJI Technology

- Lockheed Martin Corp.

- AeroVironment Inc

- Autel Robotics

- Others Key Players

Frequently Asked Questions

The Drone Payload market is estimated to be valued at US$ 13.6 Bn in 2026.

The primary demand driver for the Drone Payload market is the expanding adoption of unmanned aerial vehicles (UAVs) across commercial, defense, and industrial applications, driven by the need for enhanced data collection, surveillance, and operational efficiency.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Drone Payload market.

Among the End-use, Defence holds the highest preference, capturing beyond 65% of the market revenue share in 2026, surpassing other End- use type.

The key players in Drone Payload are Elbit Systems Ltd, IMSAR LLC, BAE Systems PLC, Parrot SA and Draganfly Inc.