- Sporting Goods & Equipment

- Consumer Drones Market

Consumer Drones Market Size, Share, and Growth Forecast, 2026 - 2033

Consumer Drones Market by Product Type (Multi-Rotor, Nano, Fixed-Wing, Hybrid), Application (Hobbyist, Prosumers, Mapping), Sales Channel (Online, Offline), and Regional Analysis for 2026-2033

Consumer Drones Market Share and Trends Analysis

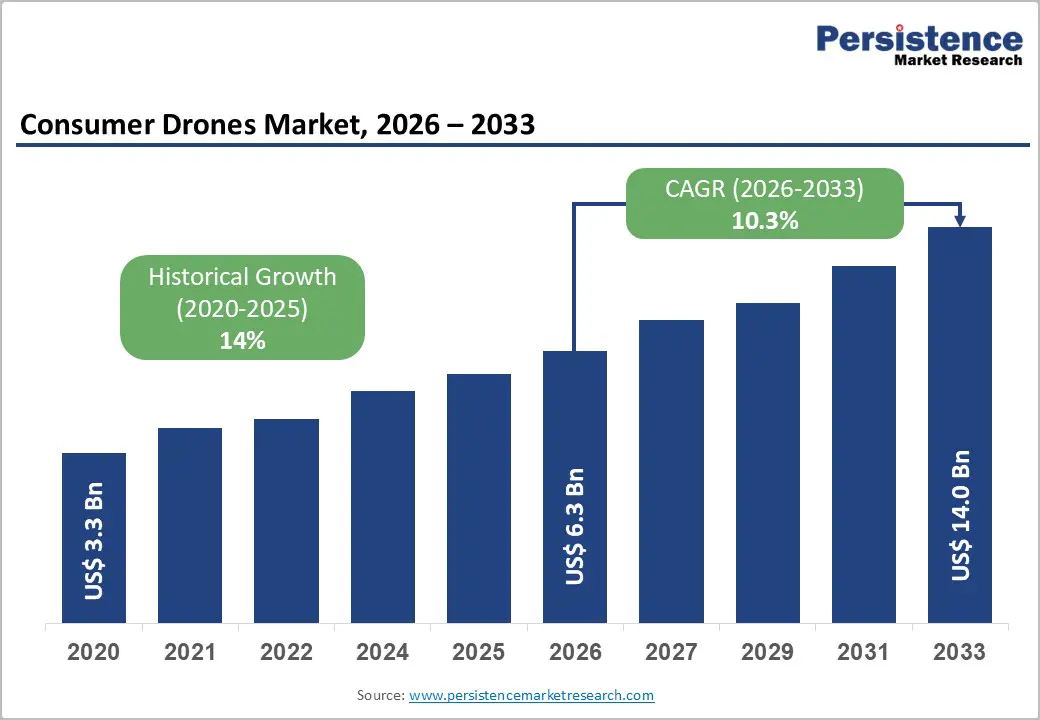

The global consumer drones market size is likely to be valued at US$ 6.3 billion in 2026, and is projected to reach US$ 14.0 billion by 2033, growing at a CAGR of 10.3% during the forecast period 2026−2033. With drone technology becoming more accessible to mainstream users due to declining component costs and improved manufacturing scale, market growth is set to accelerate sharply.

Consumers are adopting drones not only for recreational flight but also for aerial photography, content creation, travel documentation, and real estate visualization. Manufacturers are enhancing product appeal through longer battery life, improved flight stability, obstacle avoidance systems, and high-resolution integrated imaging platforms. Autonomous flight features such as waypoint navigation and object tracking are simplifying operation for non-technical users. These improvements are lowering entry barriers and expanding the addressable customer base across hobbyists, prosumers, and small business users. Regulatory clarity is further supporting market development. Authorities in major regions are harmonizing operational guidelines and registration frameworks, which is improving consumer confidence and encouraging responsible usage. Emerging applications in last-mile delivery and light commercial logistics are expanding use case visibility, even within consumer-grade platforms. Software integration is enabling real-time video transmission, cloud storage connectivity, and mobile application control interfaces that enhance user experience. Retail distribution channels are broadening through e-commerce platforms, increasing product availability across urban and semi-urban markets.

Key Industry Highlights

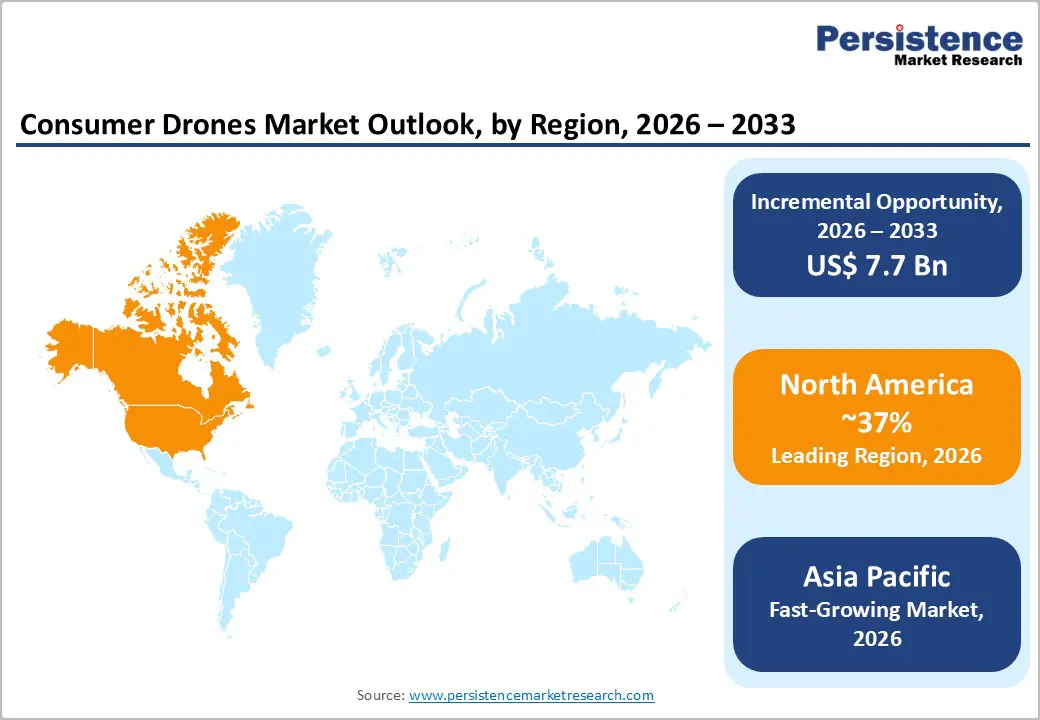

- Dominant Region: North America is expected to command about 37% market share in 2026, supported by technological sophistication and robust consumer spending power.

- Fastest-growing Regional Market: The Asia Pacific market is poised to be the fastest-growing through 2033, on account of manufacturing dominance and a rapidly expanding middle-class consumer base.

- Leading & Fastest-growing Application: Hobbyists are anticipated to hold nearly 58% revenue share in 2026, while prosumers are slated to be the fastest-growing segment during the 2026-2033 forecast period.

- Sales Channel Dominance: The online segment is likely to dominate with an approximate 60% market share in 2026, with offline channels se to grow the fastest over the 2026-2033 forecast period.

- November 2025: DJI launched the Neo 2, a 151-gram beginner-friendly camera drone with omnidirectional obstacle sensing, palm takeoff/landing, gesture/voice controls, and enhanced ActiveTrack for hands-free follow-me shots.

| Key Insights | Details |

|---|---|

| Consumer Drones Market Size (2026E) | US$ 6.3 Bn |

| Market Value Forecast (2033F) | US$ 14.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 14% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Aerial Photography and Videography

The rapid growth of social media platforms and content creation industries has reshaped demand patterns for consumer drones. Creators now rely on these devices to capture unique aerial footage that stands out on platforms such as Instagram, YouTube, and TikTok. Drones deliver professional-quality visuals through advanced features, including 4K video recording and high-resolution still photography. Content producers use this technology to craft compelling stories from above, which audiences find particularly engaging.

This trend reflects broader shifts in creative work and technology access. Employment in photography fields continues to rise as more people pursue careers in visual storytelling. Drones lower barriers to entry for aspiring professionals, who previously needed expensive equipment and training. The Federal Aviation Administration (FAA) tracks a surge in recreational drone registrations, with aerial imaging emerging as the dominant application. Businesses and creators benefit from this evolution, as drones enable cost-effective production of premium content. Strategic investments in drone technology now yield competitive advantages in content marketing and brand storytelling, positioning early adopters ahead of market trends.

Stringent Regulatory Environment and Airspace Restrictions

Complex regulatory frameworks create substantial operational hurdles for drone operators across major markets. The FAA requires registration for drones weighing more than two hundred fifty grams (250g). Remote identification rules mandate that aircraft broadcast their identity and position during flights. Governments designate extensive no-fly zones around sensitive locations such as airports and critical infrastructure. Operators face strict limits on flights beyond visual line of sight, which demand special approvals and certified pilots. These requirements add complexity for casual users and raise costs for commercial operators alike.

The European Union Aviation Safety Agency (EASA) enforces comprehensive standards that businesses must navigate carefully. Commercial operators need to register equipment, secure insurance coverage, and employ qualified pilots. Privacy concerns prompt authorities to strengthen oversight of aerial data collection practices. Public safety incidents accelerate enforcement actions against non-compliant operations. Manufacturers respond by embedding compliance features into new models, yet legacy equipment often requires costly retrofits. Companies that master these regulatory landscapes gain competitive advantages through streamlined operations and reduced legal exposure. Strategic compliance investments position firms to capitalize on market opportunities when regulatory clarity emerges.

Emerging Applications in FPV Racing and Competitive Sports

First-person view (FPV) drone racing is emerging as a specialized but commercially promising segment within the broader consumer drone market. Enthusiasts are piloting high-speed drones through complex obstacle courses while receiving live video feeds from onboard cameras, creating an immersive and skill-intensive experience. This format is attracting technology enthusiasts and gaming communities that value precision control and rapid decision-making. Manufacturers are engineering purpose-built FPV systems equipped with low-latency transmission modules, high-performance brushless motors, and reinforced lightweight frames. These technical enhancements are enabling sharper maneuverability and superior responsiveness compared with standard recreational models. Participants are prioritizing customization and performance tuning, which is expanding aftermarket component demand. As competitive leagues and organized tournaments are gaining visibility, the segment is building a structured ecosystem around specialized hardware and event participation.

Investors and industry stakeholders are recognizing opportunities to integrate FPV racing into mainstream sports and entertainment formats. Broadcasters are collaborating with event organizers to deliver live coverage and digital streaming content that appeals to younger audiences aligned with esports culture. Sponsors are targeting youth-centric demographics that engage with both gaming and emerging aerial technologies. Infrastructure investment is supporting the development of dedicated race tracks, training academies, and community hubs that foster long-term engagement. Hardware manufacturers are leveraging differentiated product design to command premium pricing and protect margins within this high-performance niche. Companies are pursuing partnerships with entertainment platforms and gaming brands to expand audience reach.

Category-wise Analysis

Product Type Insights

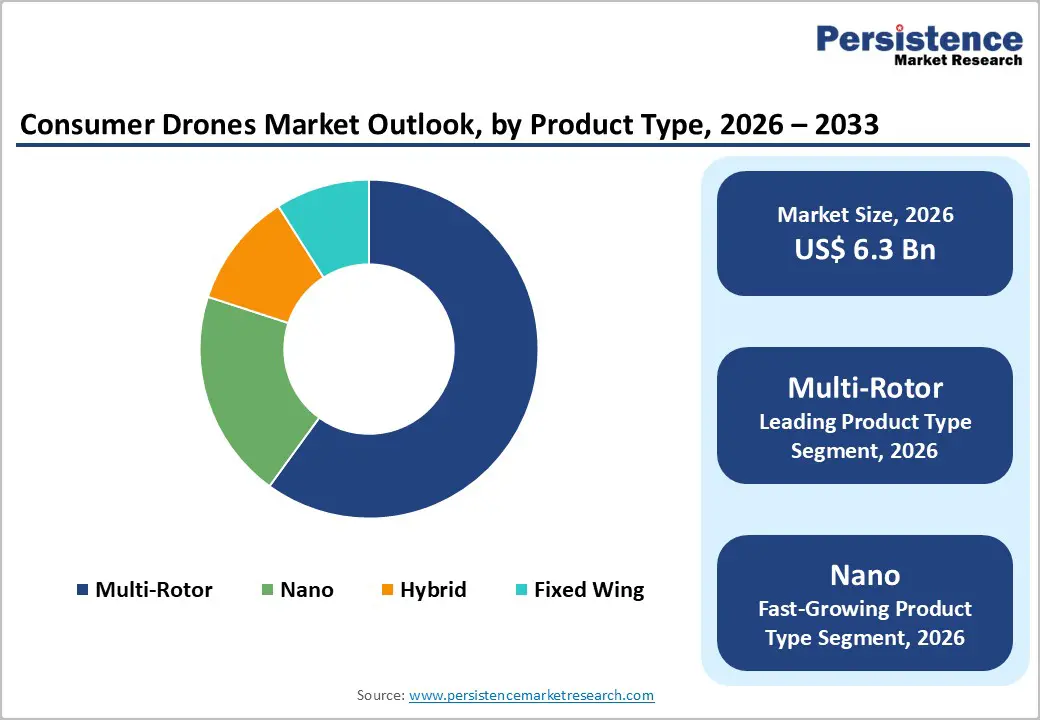

Multi-rotor drones are slated to maintain a dominant position in the market, with an estimated 2026 share exceeding 68%, owing to their superior versatility and operational characteristics. These drones generally use four or more rotors, which provide strong stability and precise control, making them well-suited for aerial photography, surveillance, and recreational flying. Their straightforward architecture simplifies manufacturing and assembly, enabling producers to scale output efficiently. This simplicity also reduces costs, supporting competitive pricing for a wide range of consumer and professional users. As a result, they have become widely accessible and continue to capture a growing share of the overall drone market.

Nano drones are likely to be the fastest-growing segment during the 2026-2033 forecast period. Miniature drones combine compact dimensions with lightweight construction, which enables safe indoor operation and effortless portability. These characteristics attract beginners, children, and urban residents facing space constraints. Recent technological innovations equip these small platforms with electronic image stabilization, forward-vision obstacle sensors, and foldable designs. Manufacturers maintain weight compliance with regulatory thresholds while delivering advanced functionality. The accessibility of miniature drones positions them as the preferred entry point for new market participants, driving sustained adoption across demographics while establishing pathways for brand loyalty and product line expansion.

Application Insights

Hobbyists are expected to hold an estimated 58% of the consumer drones market revenue share in 2026. This segment encompasses casual users, aviation enthusiasts, and families seeking entertainment through drone flying experiences. Affordability and simplified operational controls make toy-grade drones accessible to mass-market consumers without specialized piloting skills. Manufacturers have optimized user interfaces with one-button takeoff/landing, automated stabilization, and smartphone pairing capabilities, eliminating traditional barriers to entry. Social media influence drives adoption as users seek to capture and share aerial perspectives of travel, family events, and recreational activities. The segment's resilience stems from its foundation in discretionary spending and experiential consumption.

Prosumers are poised to record the highest CAGR between 2026 and 2033. Prosumer drones target serious hobbyists, semi-professional photographers, small business owners, and content creators who need advanced capabilities beyond basic models. These platforms feature large sensors, sophisticated gimbal stabilization, professional image formats, and extended battery life that support demanding applications. Real estate agents, wedding videographers, and independent filmmakers increasingly adopt prosumer equipment for revenue-generating projects. These drones deliver commercial-quality results at accessible price points. The category bridges consumer convenience with professional performance, enabling creators to monetize aerial content without enterprise-level costs while maintaining flexibility for diverse creative applications.

Sales Channel Insights

The online segment is slated to lead with an approximate 60% of the consumer drones market share in 2026. Online channels dominate drone distribution due to their convenience and extensive product selection. Consumers prefer e-commerce platforms for competitive pricing, detailed specifications, and authentic customer feedback that guide purchase decisions. These digital marketplaces streamline the buying process with fast delivery options and flexible returns. E-commerce continues to strengthen its leadership position as digital shopping habits solidify across demographics. Mobile-optimized platforms and subscription services for accessories enhance customer retention. Manufacturers leverage online channels for direct-to-consumer strategies that bypass traditional retail margins while building brand relationships through data-driven personalization.

Offline channels are anticipated to be the fastest-growing segment during the 2026-2033 forecast period. Physical retail stores provide hands-on product evaluation that digital channels cannot replicate. Customers examine drone design, weight distribution, and build quality before committing to purchase. Store associates deliver immediate technical guidance and demonstrate key features such as flight controls and camera functionality. Specialty retailers strengthen their competitive position through instant inventory availability and personalized service. Expert staff address technical concerns and recommend accessories tailored to specific use cases. As consumer drone adoption accelerates, brick-and-mortar locations expand product ranges and enhance training programs. These investments create customer loyalty and position retail partners as trusted advisors in the increasingly complex drone ecosystem.

Regional Insights

North America Consumer Drones Market Trends

North America is forecasted to account for an estimated 37% of the consumer drones market share in 2026, fueled by strong purchasing power and advanced technology adoption. The United States is driving regional performance due to a well-established recreational aviation culture and high disposable income levels that support premium drone purchases. Canada is contributing through vast open spaces suitable for recreational flying and public initiatives that promote innovation and digital adoption. Companies are benefiting from mature electronic commerce infrastructure and a strong content creation ecosystem that accelerates product distribution and consumer awareness. Regulatory oversight from the FAA is providing operational clarity through mandatory registration systems and remote identification requirements, which are improving airspace coordination and consumer confidence. These regulatory measures are supporting structured market growth while maintaining safety standards.

Demand drivers are expanding beyond hobbyist applications into professional and semi-commercial use cases. Aerial photography is gaining traction in real estate marketing, tourism promotion, and social media content production. Organized drone racing leagues and enthusiast communities are broadening engagement across competitive segments. Major retailers are testing last-mile delivery pilots, signaling gradual expansion toward light commercial deployment. Domestic manufacturers such as Skydio are emphasizing autonomous navigation capabilities and data security features to differentiate from international competitors. Consumer adoption patterns are shifting as middle-aged buyers are representing one of the fastest-growing ownership segments, expanding market appeal beyond early technology adopters.

Europe Consumer Drones Market Trends

Europe is poised to maintain a strong position in the global market for consumer drones through 2033, owing to harmonized regulatory frameworks and mature consumer electronics infrastructure. Germany leads with engineering excellence, while the United Kingdom, France, and Spain contribute through creative industries and tourism sectors. The EASA establishes continent-wide standards that require registration, insurance, and certified pilots for commercial operations. Manufacturers benefit from reduced compliance complexity across member states, which facilitates cross-border distribution and service provision. Growth accelerates through tourism marketing and outdoor sports applications. Businesses leverage aerial videography for destination promotion and adventure content creation, particularly in Alpine and coastal regions.

Privacy-focused regulations build public trust, though they impose data protection and geo-fencing requirements that exceed North American standards. Strategic manufacturers such as Parrot emphasize regulatory compliance and data sovereignty, creating competitive advantages against Asian import leaders facing geopolitical scrutiny. Environmental consciousness drives demand for sustainable designs with repairable components and extended product lifecycles. Investors recognize Europe's balanced approach combines innovation enthusiasm with precautionary governance, positioning the region for steady expansion as regulatory clarity strengthens consumer confidence.

Asia Pacific Consumer Drones Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for consumer drones during the 2026-2033 forecast period, due to manufacturing dominance and rapidly broadening base of middle-class buyers. China drives regional leadership with vertically integrated production ecosystems and government initiatives that prioritize drone industry development. India accelerates as the fastest-growing national market, supported by regulatory simplification through the Digital Sky Platform and domestic manufacturing incentives. Japan contributes through precision agriculture and disaster response applications, while Southeast Asian countries such as Indonesia, Vietnam, and Thailand emerge as high-potential consumer markets. Strategic companies capitalize on urbanization trends and rising disposable incomes that fuel recreational and content creation demand.

E-commerce platforms deploy drones for rural last-mile delivery, demonstrating commercial logistics viability. Agricultural operators across vast farming regions adopt prosumer equipment for precision monitoring. Cultural enthusiasm for technology and gaming communities creates natural demand for FPV racing and advanced recreational platforms. Regulatory environments balance industry promotion with airspace management China opens low-altitude corridors, India streamlines approvals, and Japan facilitates beyond visual line of sight operations. Investors recognize manufacturing cost advantages and supply chain integration position the region to challenge North American market leadership within the decade.

Competitive Landscape

The global consumer drones market is exhibiting a moderately consolidated structure in 2026, with a group of established manufacturers collectively controlling around 40-45% of the total revenue. Competition is remaining intense as leading brands and agile entrants are accelerating product innovation cycles to meet evolving consumer expectations. Companies are differentiating through advanced flight stabilization systems, artificial intelligence (AI)-enabled navigation, higher-resolution imaging sensors, and durable lightweight materials. Build quality, after-sales service, firmware updates, and user-friendly software ecosystems are influencing purchasing decisions alongside hardware specifications. Rapid technology refresh timelines are requiring continuous investment in research and development to maintain competitive positioning. As feature parity is narrowing across mid-range models, manufacturers are strengthening brand loyalty through ecosystem integration, application support, and cloud connectivity services. This environment is rewarding firms that can balance performance innovation with cost discipline.

Strategic consolidation and partnership activity are shaping competitive dynamics. Market leaders are pursuing targeted mergers and acquisitions to expand technological capabilities, diversify supply chains, and improve component sourcing efficiency. Collaborations with software developers, mapping platforms, and content creation ecosystems are expanding product functionality and enhancing user engagement. Partnerships are also supporting faster entry into specialized segments such as enterprise-grade imaging and light commercial deployment, while distributing regulatory compliance costs across aligned stakeholders. Companies are also integrating hardware, analytics platforms, and cloud services to create defensible competitive moats.

Key Industry Developments

- In September 2025, Skydio introduced the R10 indoor drone for public safety missions, featuring consumer-like ease of use with enterprise integrations, and the F10 autonomous fixed-wing drone targeting high-speed pursuits and long-endurance inspections with over 90-minute flights.

- In July 2025, Insta360 launched Antigravity, a new consumer drone brand focused on 360-degree aerial capture, targeting creators seeking immersive spherical videography. The platform integrates Insta360's signature 360° imaging technology with drone autonomy for seamless full-sphere content production.

- In June 2025, Walmart and Wing announced their largest drone delivery expansion, rolling out 30-minute service to 100+ stores across Atlanta, Charlotte, Houston, Orlando, and Tampa by mid-2026, building on Dallas-Fort Worth operations.

Companies Covered in Consumer Drones Market

- SZ DJI Technology Co., Ltd.

- Parrot Drones SAS

- Skydio, Inc.

- Autel Robotics Co., Ltd.

- Yuneec International Co., Ltd.

- GoPro, Inc.

- Hubsan Technology Co., Ltd.

- Holy Stone Innovation Technology

- BetaFPV Technology Co., Ltd.

- Walkera Technology Co., Ltd.

- EHang Holdings Limited

- Ryze Tech Co., Ltd.

- Syma International

- Garuda Aerospace

- Potensic Technology Co., Ltd.

Frequently Asked Questions

The global consumer drones market is projected to reach US$ 6.3 billion in 2026.

Technological advancements in imaging, battery life, and autonomous flight capabilities drive consumer drone adoption across recreational, content creation, and emerging commercial applications are driving the market.

The market is poised to witness a CAGR of 10.3% from 2026 to 2033.

Last-mile delivery commercialization, Drone-as-a-Service software monetization, and emerging market penetration in Asia Pacific represent the highest-value growth opportunities.

SZ DJI Technology Co., Ltd., Parrot Drones SAS, Skydio, Inc., Autel Robotics Co., Ltd., and Yuneec International Co., Ltd. are some of the key players in the market.