- Aerospace & Defense

- Cargo Drone Market

Cargo Drone Market Size, Share, and Growth Forecast 2026 – 2033

Cargo Drone Market by Payload (10–49 Kg, 50–149 Kg, 150–200 Kg, above 200 Kg), by Drone Type (Fixed Wing, Rotary Wing, Hybrid), by Industry (Retail, Healthcare, Agriculture, Défense, Maritime), and Regional Analysis for 2026–2033

Cargo Drone Market Size and Trend Analysis

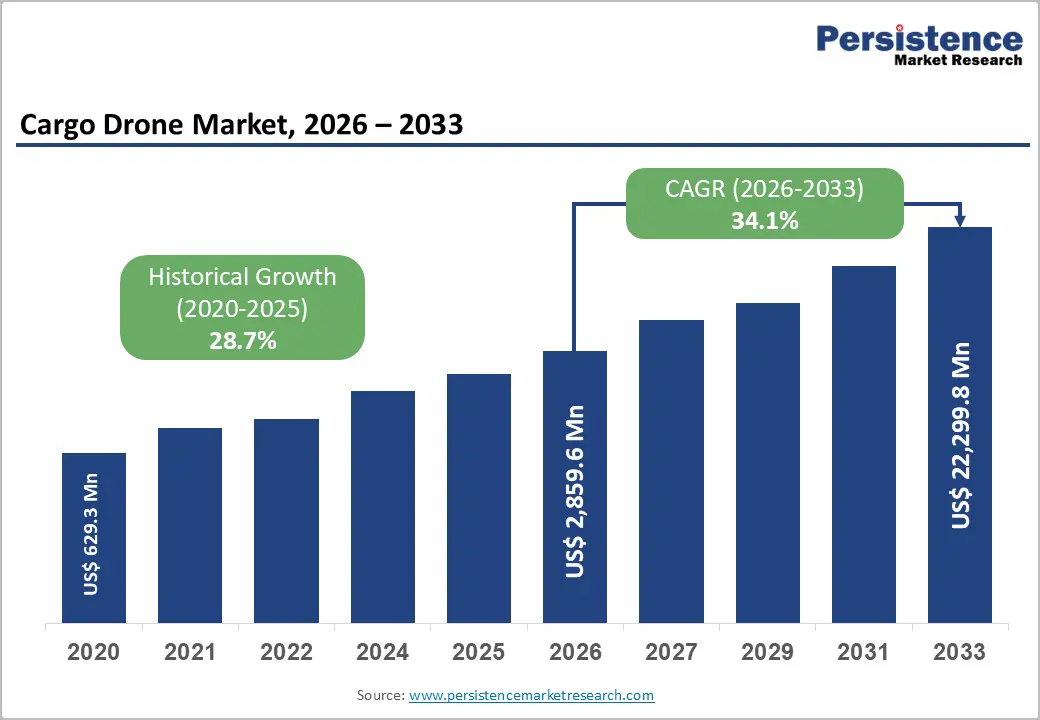

The global Cargo Drone market size is valued at US$ 2.9 billion in 2026 and is projected to reach US$ 22.2 billion by 2033, growing at a CAGR of 34.1% between 2026 and 2033. The cargo drone market is entering an exponential growth phase, driven by converging forces of regulatory liberalization, transformative advances in autonomous flight technology, and the structural imperative of last-mile logistics decarbonization across e-commerce, healthcare, and Défense supply chains.

The U.S. Federal Aviation Administration (FAA)'s progressive Beyond Visual Line of Sight (BVLOS) rulemaking, the European Union Aviation Safety Agency (EASA)'s U-Space regulation, and national drone delivery approvals across China, Japan, India, and Australia are collectively opening commercial airspace to scalable cargo operations at an unprecedented pace.

Key Market Highlights

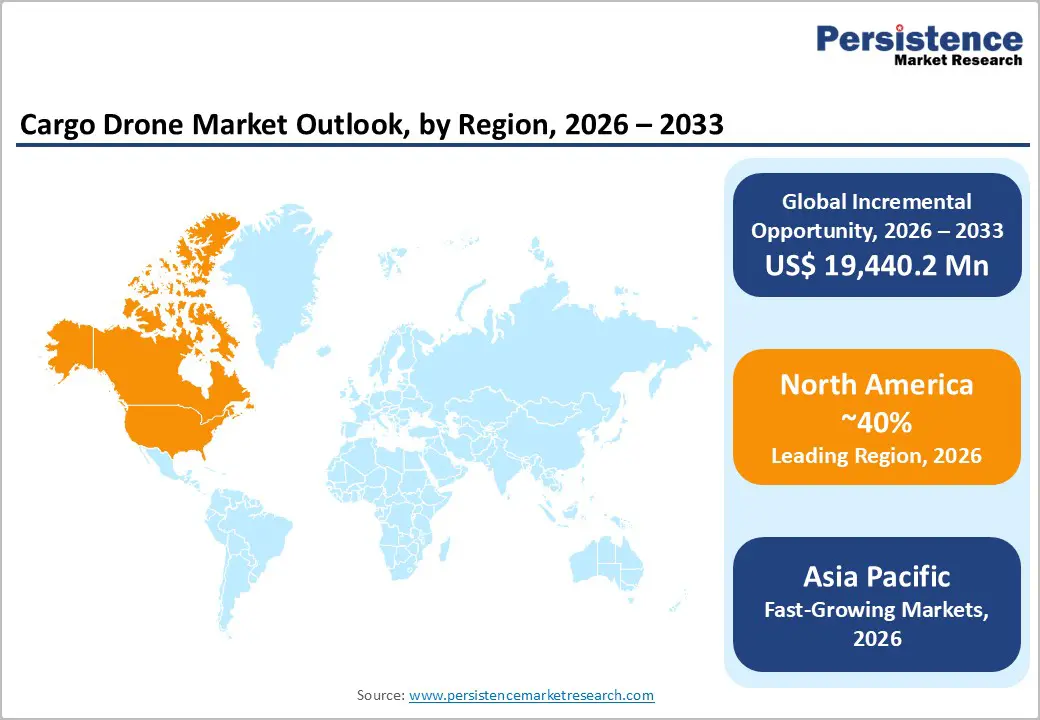

- Leading Region: North America leads the global Cargo Drone market with approximately 38% revenue share in 2026, anchored by the U.S.'s unmatched regulatory ecosystem FAA Part 135 certificates, LAANC airspace authorization, and the FAA Reauthorization Act 2024 BVLOS mandate supporting the world's densest concentration of active commercial cargo drone operators.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, propelled by China's CAAC-licensed e-commerce drone delivery networks serving 300+ rural communities, India's DGCA Drone Rules 2021 framework, Japan's Level 4 BVLOS law, and Southeast Asia's rapidly expanding healthcare and logistics drone adoption.

- Leading Segment: Rotary Wing drones dominate the Type segment with approximately 52% market share in 2026, driven by VTOL capability essential for urban last-mile delivery the dominant near-term commercial use case, and the commercial maturity of multi-rotor platforms deployed by Zipline, Wing, Matternet, and DJI at operational scale.

- Fastest Growing Segment: Above 200 Kg payload drones represent the fastest-growing payload segment, driven by DoD procurement programs including U.S. Army autonomous logistics contracts, DARPA ARES, and NATO exploration of autonomous battlefield cargo platforms validated by Ukraine conflict operational learnings, accelerating heavy cargo drone Défense procurement globally.

- Opportunity: The most compelling market opportunity lies in healthcare drone logistics in underserved geographies with 2 billion people lacking essential medicine access (WHO) where Zipline's 1 million+ delivery track record proves commercial viability, and temperature-controlled medical payload drone systems address the highest willingness-to-pay segment in global logistics.

DRO Analysis

Drivers - Regulatory Liberalization and BVLOS Approvals Enabling Commercial Cargo Drone Operations at Scale

The systematic opening of national airspaces to beyond visual line of sight (BVLOS) cargo drone operations is the single most consequential regulatory development enabling market commercialization. In the United States, the FAA's BEYOND program and Part 135 air carrier certifications granted to Wing (Alphabet), Amazon Prime Air, and Zipline have established legal frameworks for routine commercial drone delivery operations.

The FAA Reauthorization Act of 2024 mandated accelerated BVLOS rulemaking timelines, with final rules expected to unlock full commercial deployment across urban and suburban corridors. In Europe, EASA's U-Space Regulation (Commission Implementing Regulation 2021/664) provides a harmonized traffic management framework across EU member states, enabling multi-operator cargo drone networks.

E-Commerce Last-Mile Logistics Economics Compelling Drone Delivery Investment

The structural economics of last-mile delivery which accounts for 53% of total shipping costs according to the Business Insider Intelligence supply chain report is compelling e-commerce operators and logistics companies to invest in autonomous aerial delivery as a cost reduction and service differentiation strategy. Amazon's commitment to Prime Air represents a multi-billion- dollar investment targeting sub-30-minute delivery within a 5-mile radius, a service level unachievable with conventional road-based logistics.

Walmart has partnered with Drone Up and Wing to operate drone delivery from store-to-door in multiple U.S. markets. The World Economic Forum (WEF) estimates that drone delivery in urban areas could be up to 70% cheaper per parcel than van delivery on a per-mile basis at scale, creating a compelling unit economics case that is accelerating commercial deployment decisions across the global logistics industry.

Restraints - Airspace Management Complexity and Urban Integration Challenges Constraining Scalability

The absence of fully operational and universally adopted unmanned traffic management (UTM) systems capable of safely coordinating high-density cargo drone flights in complex urban airspace represents a critical operational bottleneck. While frameworks including NASA's UTM research program, FAA's Low Altitude Authorization and Notification Capability (LAANC), and EASA's U-Space provide foundational architectures, real-time deconfliction of hundreds of simultaneous cargo flights over densely populated areas has not yet been demonstrated at an operational scale.

Urban obstacle mapping, interference with manned aviation, and emergency protocol standardization each add layers of regulatory and technical complexity that extend commercialization timelines and increase compliance costs for operators seeking city-wide deployment permits.

Battery Energy Density and Payload-Range Trade-offs Limiting Operational Utility

Current lithium-ion and lithium-polymer battery technology imposes fundamental constraints on cargo drone payload capacity and operational range that limit commercial viability beyond light-parcel delivery use cases. State-of-the-art batteries achieve energy densities of approximately 250–300 Wh/kg, which translates to effective cargo ranges of 15–30 km for payloads in the 2–5 kg range, sufficient for pharmaceutical and small-package delivery but inadequate for heavier industrial or humanitarian cargo.

Scaling payload capacity to 50 kg+ requires either hydrogen fuel cell propulsion, which carries its own handling and infrastructure complexity or hybrid configurations that add mechanical complexity and maintenance cost, constraining market penetration in the commercially important 50–200 kg payload segments.

Opportunities - Healthcare and Medical Supply Chain Drone Delivery in Underserved and Remote Geographies

The healthcare sector represents one of the highest-value and most structurally compelling near-term growth applications for cargo drones, where the premium on delivery speed and the catastrophic cost of supply chain failure create the strongest economic case for aerial logistics.

Zipline has executed over one million commercial drone deliveries of blood products, vaccines, and medications across Rwanda, Ghana, Nigeria, and the United States has empirically validated the healthcare drone delivery model at scale, demonstrating that autonomous aerial logistics can deliver life-saving supplies to remote facilities in 30 minutes compared to 3–4 hours by road.

The World Health Organization (WHO) estimates that 2 billion people globally lack reliable access to essential medicines, with geographic isolation and fragile cold chains identified as primary barriers both directly addressable by cargo drone networks.

Défense and Military Logistics Applications Driving Above-200 Kg Heavy Cargo Drone Demand

The Défense sector is emerging as one of the highest-value cargo drone end-users, with military logistics applications driving demand for heavy-payload platforms in the 150–200 kg and above 200 kg categories the fast-growing payload segments. The U.S. Department of Défense (DoD) has actively funded programs including DARPA's Aerial Reconfigurable Embedded System (ARES) and U.S.

Army's Autonomous Multi-Domain Operations programs that are developing autonomous cargo drones for battlefield logistics, combat casualty evacuation (CASEVAC), and forward base resupply without exposing personnel to hostile fire. The Ukraine conflict has further demonstrated the operational value of autonomous aerial cargo in contested environments, accelerating Défense procurement timelines globally and validating the strategic case for heavy cargo drone investment.

Category-wise Analysis

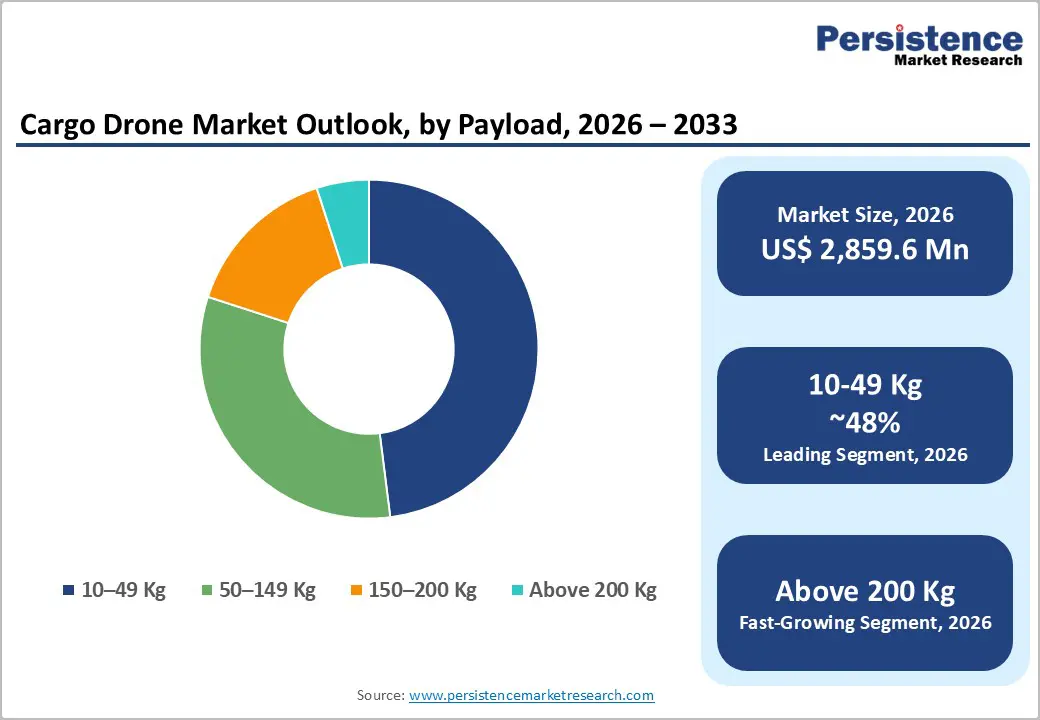

Payload Insights

The 10–49 Kg payload segment dominates the global cargo drone market, accounting for approximately 48% of total market share in 2026. This leadership reflects the commercial maturity of light-payload delivery operations particularly in pharmaceutical, e-commerce parcel, and agricultural input delivery where drone platforms in this weight class offer the optimal balance of operational range, flight endurance, and regulatory compliance with current BVLOS frameworks.

Wing's delivery drone operates at sub-2 kg payload, Zipline's Platform 2 targets 3–4 kg payloads, and Matternet's M2 carries up to 2 kg all within the practical commercial sweet spot below 50 kg that dominates current deployment volumes. However, the Above 200 Kg segment is the fastest-growing payload category, driven by Défense and industrial logistics procurement programs demanding heavy autonomous cargo platforms with operational ranges and payload capacities that bridge the gap between traditional helicopter logistics and ground transport.

Drone Type Insights

The rotary wing configuration leads the cargo drone market by type, commanding approximately 52% of total market share in 2026. Multi-rotor and coaxial rotary wing platforms dominate because their vertical take-off and landing (VTOL) capability is essential for urban last-mile delivery where the absence of dedicated runways is a fundamental operational constraint and their hover capability enables precise payload delivery in confined spaces.

Platforms including DJI Agras, Matternet M2, Zipline Platform 2, and Joby Cargo (rotary VTOL configurations) represent the dominant commercial deployment format globally. However, the Hybrid VTOL segment which combines fixed-wing range efficiency with rotary-wing VTOL capability is the fastest-growing configuration type, driven by Défense and long-range logistics applications requiring endurance and range beyond what pure rotary systems can achieve.

Industry Insights

The Healthcare industry segment leads cargo drone market revenue, representing approximately 29% of total market share in 2026, reflecting the sector's uniquely favorable combination of time-critical delivery requirements, premium willingness-to-pay, and supportive regulatory environments that have historically fast-tracked humanitarian and medical use cases.

Zipline's documented delivery of over one million medical consignments spanning blood products, vaccines, antivenoms, and surgical supplies across Africa and the United States has established healthcare as the most commercially proven cargo drone application globally. The Retail/E-commerce sector is the fastest-growing industry segment, driven by Amazon Prime Air, Wing, Walmart-DroneUp, and JD.com's drone delivery program actively scaling operations following FAA and CAAC approvals.

Regional Analysis

North America Cargo Drone Market Trends & Analysis

North America leads the global cargo drone market, holding approximately 38% of revenue in 2026, underpinned by the most advanced regulatory framework for commercial drone operations globally including FAA Part 135 air carrier certificates for commercial drone delivery, the LAANC system enabling real-time low-altitude airspace authorization, and the FAA Reauthorization Act of 2024's BVLOS mandate. The U.S. hosts the world's highest concentration of cargo drone OEMs and technology developers, from Zipline and Wing to Amazon Prime Air and Matternet, creating a deep innovation ecosystem that reinforces market leadership.

U.S. Cargo Drone Market Size

The U.S. Cargo Drone market is valued at approximately US$ 890 Mn in 2025, anchored by active commercial drone delivery operations in Texas, Virginia, North Carolina, Arkansas, and Florida under FAA-approved frameworks. The DoD's active cargo drone procurement programs including the U.S. Army's autonomous logistics contracts and DARPA's ARES program combined with Amazon Prime Air's multi-city rollout and Wing's expanding U.S. residential delivery network collectively make the U.S. the world's single most active cargo drone commercial deployment market.

Europe Cargo Drone Market Trends

Europe holds approximately 18% of global Cargo Drone market revenue in 2025, with demand shaped by EASA's U-Space regulatory framework enabling harmonized multi-operator cargo drone networks across EU member states and the region's strong emphasis on sustainable urban logistics as part of the European Green Deal transport decarbonization agenda.

The UK Civil Aviation Authority (CAA)'s progressive BVLOS sandbox programs and Germany's active drone delivery pilot programs in rural healthcare supply chains represent the most advanced deployment activities, with Switzerland's Matternet-Swiss Post operation the world's longest-running certified medical drone delivery network serving as the European benchmark for regulatory integration.

Germany Cargo Drone Market Trends

Germany's Cargo Drone market is valued at approximately US$ 118 Mn in 2026, driven by the Federal Ministry for Digital and Transport (BMDV)'s drone delivery innovation programs and Deutsche Post DHL Group's active investment in autonomous aerial logistics for last-mile parcel delivery in rural and suburban environments. Germany's U-Space implementation timeline mandated under EASA's framework and the German Aerospace Center (DLR)'s cargo drone research programs position the country as Europe's most active cargo drone technology development market.

U.K. Cargo Drone Market Size

The U.K. Cargo Drone market is valued at approximately US$ 88 Mn in 2025, with the UK CAA's Project Skyways and BVLOS sandbox programs enabling systematic commercial testing of cargo drone delivery across urban and island routes. Windracers' long-range fixed-wing cargo drone operations in the Scottish Highlands and the NHS blood-type delivery drone trials in the East of England represent the UK's leading commercial cargo drone deployment use cases, with healthcare logistics serving as the primary near-term commercial pathway.

France Cargo Drone Market Size

France's cargo drone market was approximately valued at US$ 62 million in 2025, supported by the Direction Générale de l'Aviation Civile (DGAC)'s regulatory sandbox for advanced urban air mobility and cargo drone operations. France's leadership in the Single European Sky initiative and Airbus's engagement in urban air mobility and cargo drone R&D including the Airbus CityAirbus NextGen platform position France as a technology development centre with growing commercial deployment momentum, particularly in humanitarian supply chain and rural healthcare delivery applications.

Asia Pacific Cargo Drone Market Drivers & Analysis

Asia Pacific is the fast-growing cargo drone market, projected to expand at the highest regional CAGR through 2033, with China dominating current deployment volumes and India, Japan, and Southeast Asia representing the most dynamic emerging growth frontiers. China's Civil Aviation Administration of China (CAAC) has issued commercial drone delivery licenses to JD.com (JD Logistics), SF Express, and Meituan, with JD.com's cargo drone network delivering millions of packages across rural provinces in Jiangxi, Sichuan, and Shaanxi.

China Cargo Drone Market Size

China's Cargo Drone market is valued at approximately US$ 428 Mn in 2025, reflecting the country's position as the world's most active cargo drone commercial deployment environment. JD.com's drone delivery network serving over 300 villages across multiple provinces and SF Express's CAAC-approved cargo drone operations represent the world's largest commercial cargo drone logistics programs outside healthcare.

India Cargo Drone Market Size

India's Cargo Drone market is valued at approximately US$ 142 Mn in 2025 and is among the fastest-growing country-level markets globally, driven by the Directorate General of Civil Aviation (DGCA)'s progressive drone policy framework including the Drone Rules 2021 and the Drone Promotion Council and ICMR (Indian Council of Medical Research)'s blood and vaccine delivery drone programs piloted across Telangana, Manipur, and Meghalaya.

Japan Cargo Drone Market Size

Japan's Cargo Drone market is valued at approximately US$ 98 Mn in 2025, sustained by the country's 2022 Civil Aeronautics Act amendments enabling Level 4 BVLOS operations over populated areas among the most permissive urban cargo drone frameworks globally. Yamato Holdings (TA-Q-BIN), Japan Post, and NTT Docomo are operational cargo drone delivery program participants, while the government's Digital Garden City Nation initiative explicitly identifies drone delivery as a solution for elderly population supply chain challenges in rural and mountainous depopulated communities creating a socially mandated demand channel with direct government support.

Competitive Landscape

The global cargo drone market is highly fragmented and rapidly evolving, with a diverse ecosystem of dedicated cargo drone OEMs, logistics-operator-led programs, and technology platform developers competing across payload class, geography, and vertical application. No single company commands dominant market share across all segments Zipline leads in healthcare, Wing (Alphabet) in retail delivery, JD.com in e-commerce logistics, and Sabrewing/Joby in Défense-adjacent heavy cargo.

Key competitive differentiators include autonomous flight software maturity, FAA/CAAC/EASA certification status, battery or hybrid propulsion performance, and vertical integration of logistics software with fleet hardware.

Key Developments:

- In April 2025, Piasecki Aircraft announced the acquisition of Kaman Air Vehicles' Kargo UAV, expanding its helicopter and drone portfolio. Piasecki Aircraft is committed to accelerating the development of the Kargo UAV and aims to deliver a production-ready model by late 2026.

- In September 2024, Dufour Aerospace, the forward-thinking Swiss drone and eVTOL manufacturer, Areion, a leading U.S. drone innovator and successor to Spright, renewed their partnerships. As a part of the agreement, Areion purchased 40 Aero2 drones, with an option to buy up to another 100 aircraft.

Global Cargo Drone Market – Key Insights & Details

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 629.3 Mn |

|

Current Market Value (2026) |

US$ 2,859.6 Mn |

|

Projected Market Value (2033) |

US$ 22,299.8 Mn |

|

CAGR (2026-2033) |

34.1% |

|

Leading Region |

Asia Pacific, 45% share |

|

Dominant Application |

10-49 Kg, 48% share |

|

Top-ranking Product |

Rotary Wing, 52% |

|

Incremental Opportunity |

US$ 19,440.22 Mn |

Companies Covered in Cargo Drone Market

- Zipline International Inc.

- Wing Aviation LLC (Alphabet)

- Amazon Prime Air

- JD Logistics (JD.com)

- Matternet Inc.

- DroneUp LLC

- Sabrewing Aircraft Company

- Joby Aviation Inc.

- EHang Holdings

- DJI

- Windracers Limited

Frequently Asked Questions

The global Cargo Drone market is valued at US$ 2.9 Bn in 2026 and is projected to reach US$ 22,299.8 Bn by 2033, expanding at an extraordinary CAGR of 34.1% during the forecast period.

The primary drivers are FAA, EASA, and CAAC regulatory liberalization enabling BVLOS commercial operations including FAA Part 135 certifications and EASA U-Space implementation and the compelling unit economics of drone delivery versus road-based last-mile logistics, with the WEF estimating drone delivery can be up to 70% cheaper per parcel at scale, driving investment from Amazon, Walmart, JD.com, and Zipline in commercial fleet deployment.

The 10–49 Kg payload segment leads with approximately 48% market share in 2025, reflecting the commercial maturity of light-payload delivery platforms deployed by Zipline, Wing, Matternet, and DJI across healthcare, e-commerce, and agricultural applications.

North America leads with approximately 38% revenue share in 2025, anchored by the U.S.'s unmatched regulatory ecosystem, including FAA Part 135 air carrier certificates, the LAANC airspace authorization system, and the FAA Reauthorization Act 2024 BVLOS mandate. The U.S. market is valued at approximately US$ 890 Mn in 2025 and hosts Wing, Zipline, Amazon Prime Air, and Matternet as operationally active commercial cargo drone operators.

The cargo drone market is led by Zipline International (1M+ deliveries across Africa and the USA), Wing Aviation LLC (Alphabet subsidiary with FAA Part 135 certification and 500,000+ commercial deliveries), and JD Logistics (China's largest rural e-commerce drone delivery network serving 300+ communities).