- Biotechnology

- DNA Modifying Enzymes Market

DNA Modifying Enzymes Market Size, Share, and Growth Forecast, 2026-2033

DNA Modifying Enzymes Market by Product Type (DNA Ligases, Alkaline Phosphatases, Exonucleases, Endonucleases, Terminal Transferases, Poly(A) Polymerases, T4 Polynucleotide, Kinases, Ribonucleases), Application (Pharmaceutical & Biotechnology Research, Diagnostics, Animal Feed, Food & Beverage, Biofuel Industry, Others), End-User (Pharmaceutical & Biotechnological Companies, Research Centers, Others), and Regional Analysis for 2026-2033

DNA Modifying Enzymes Market Share and Trends Analysis

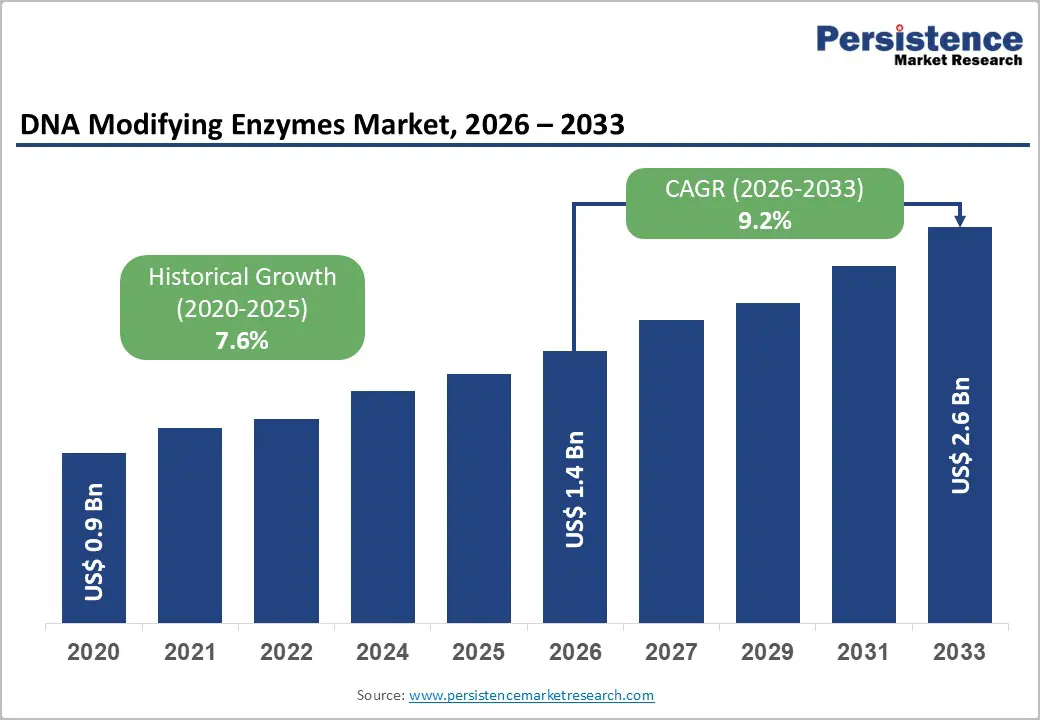

The global DNA modifying enzymes market size is likely to be valued at US$ 1.4billion in 2026, and is projected to reach US$ 2.6billion by 2033, growing at a CAGR of 9.2% during the forecast for 2026-2033. This growth is primarily following the significant increase in biotechnology and genomic research funding across both public and private sectors. Research institutions are presently intensifying their focus on advanced molecular diagnostics to identify genetic markers for chronic and infectious diseases.

The rising demand for sophisticated gene editing tools and next-generation sequencing workflows is currently catalyzing the adoption of high-fidelity enzymes in clinical settings. Healthcare providers are presently integrating these tools into personalized therapy protocols to tailor medical treatments to individual genetic profiles. Furthermore, the expansion of pharmaceutical pipelines is driving the need for specialized enzymes that can facilitate complex recombinant DNA technology. These advanced molecular tools are transforming drug discovery processes and refining the accuracy of diagnostic assays globally. As a result, DNA-modifying enzymes have emerged as leaders in the precision medicine revolution.

Key Industry Highlights

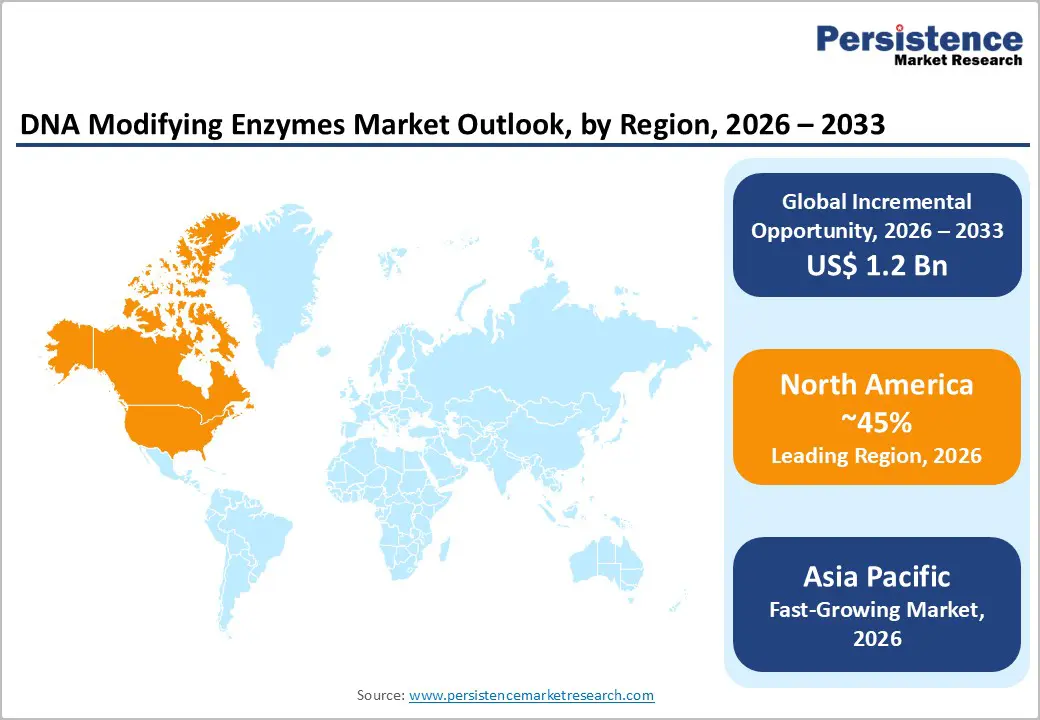

- Regional Leadership: North America is projected to hold about 45% share in 2026, fueled by well-established biotech infrastructure and funding, while the Asia Pacific market is likely to grow fastest at 12% CAGR, aided by low-cost manufacturing.

- Dominant Product Type: DNA ligases are expected to account for about 25% of revenue in 2026 due to their widespread use in gene cloning and sequencing workflows.

- Fastest-growing Product Type: Exonucleases are projected to grow at the fastest rate, 11.8% CAGR through 2033, driven by advancements in synthetic biology and precision genome editing.

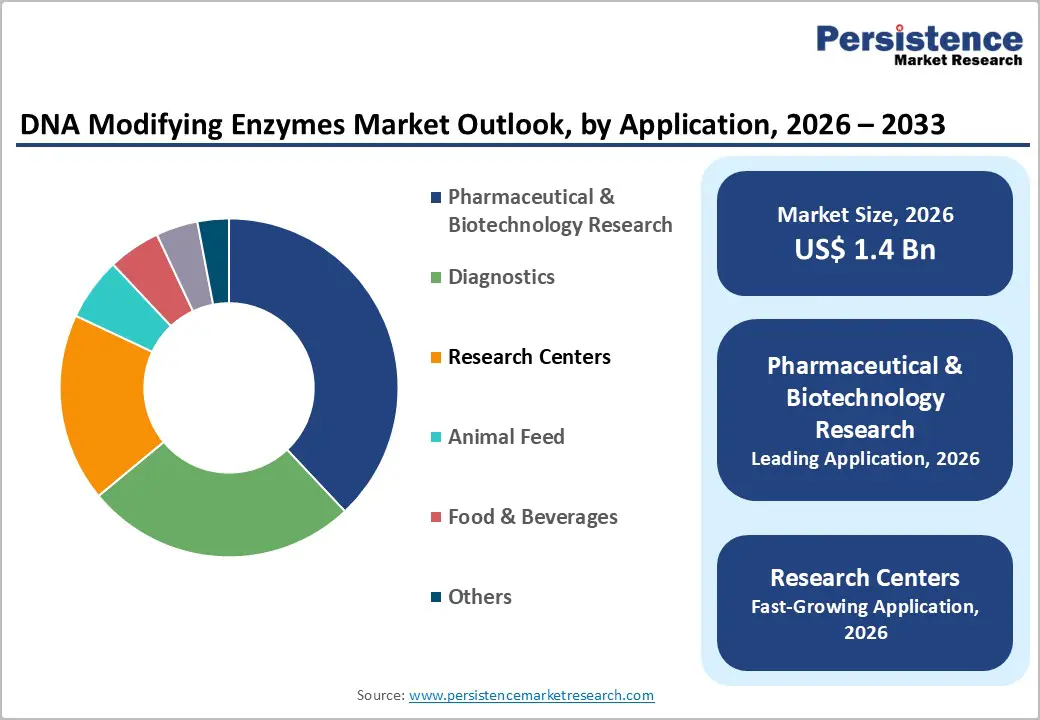

- Leading Applications: Pharmaceutical & biotechnology research is expected to hold 38% market share in 2026, driven by high R&D budgets, while diagnostics are projected to grow fastest at 10.7% CAGR, boosted by the rising demand for molecular testing.

- Primary End-Users: Pharmaceutical & biotech companies are projected to control roughly 42% of market revenues in 2026 owing to clinical and commercial gene editing pipelines, while research centers are likely to grow the fastest at 9.5% CAGR on the back of increased genomics funding.

- Competitive Environment: Licensing, facility expansions, and high-fidelity enzyme launches are intensifying competition by enhancing production capacity and innovation pipelines.

- May 2025: Baby KJ received the world’s first personalized CRISPR treatment for a rare metabolic disorder, demonstrating the feasibility of individualized gene editing and validating DNA-modifying enzymes as practical tools in precision medicine.

| Key Insights | Details |

|---|---|

| DNA Modifying Enzymes Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Genomic Research and Advanced Gene Editing Technologies

Public and private investment in genomics and molecular biology has surged over the past decade, with countries such as the United States, China, and Europe funding multi-billion-dollar initiatives for precision medicine, synthetic biology, and genomic research. For instance, the U.S. All of Us Research Program collects genetic and health data from millions to support individualized therapies, increasing demand for high-precision modifying enzymes in research workflows. This investment has expanded the use of DNA ligases, exonucleases, and endonucleases in sequencing, gene editing, and synthetic biology. Rising research throughput and adoption of enzyme-based workflows improve experimental speed and reproducibility. Institutional support further drives innovation and adoption across diagnostics and biopharmaceutical R&D segments globally.

The rapid adoption of advanced gene editing technologies, including CRISPR/Cas systems, next-generation sequencing (NGS), and high-fidelity amplification, is boosting enzyme demand. DNA ligases play a central role in CRISPR library construction and NGS preparation, supporting precision workflows. As these technologies become standard in therapeutic pipelines, demand for specialized modifying enzymes grows steadily. The combined impact of funding expansion and technology adoption is driving robust double-digit market growth for modifying enzymes in both research and clinical applications worldwide.

High Cost Structures and Regulatory Complexity Limiting Market Adoption

Manufacturing high-purity DNA-modifying enzymes requires advanced bioprocessing infrastructure, validated cleanroom environments, and specialized technical expertise, significantly increasing production costs. In recent years, enzyme manufacturers have made substantial capital investments to upgrade facilities to comply with stricter quality, traceability, and regulatory standards. For example, Thermo Fisher Scientific expanded and upgraded its bioprocess design centers across Asia to support regulatory-ready enzyme and biologics production, underscoring the scale of the required infrastructure. These investments translate into higher-priced enzyme products, creating affordability challenges for academic institutions and price-sensitive emerging markets. Budget constraints in publicly funded research environments further limit large-scale adoption.

The regulatory and ethical scrutiny of DNA modification technologies has intensified, particularly for gene editing and clinical applications. Regulatory authorities increasingly require comprehensive safety documentation, validated production processes, and extended approval timelines, raising compliance costs. Ethical debates surrounding genome manipulation influence policy frameworks and slow decision-making in several regions. These regulatory pressures delay commercialization and create uncertainty for enzyme-enabled diagnostic and therapeutic pipelines. As a result, adoption remains slower in clinical end-use segments. These elevated cost structures and regulatory complexity continue to constrain near-term market expansion.

Expanding Clinical Adoption of Gene Editing, Diagnostics, and Synthetic Biology Platforms

Emerging regional markets, particularly Asia Pacific, offer significant growth potential as governments increase investment in genomic infrastructure and biotechnology research across China, India, and Japan. Public initiatives supporting precision medicine and synthetic biology, combined with cost-effective manufacturing ecosystems, are expanding access to enzyme-enabled workflows. In parallel, advancements in molecular diagnostics, including rapid polymerase chain reaction (PCR) and NGS technologies, are increasing demand for reliable modifying enzymes. Healthcare systems are increasingly integrating predictive and preventive genetic testing, supporting long-term enzyme replacement therapy. These trends collectively broaden the use of enzymes beyond research-only settings. As adoption expands, demand shifts toward higher-performance and application-specific enzymes.

Clinical validation of gene-editing therapies further strengthens long-term market opportunity for DNA modifying enzymes. In 2023, the UK approved its first CRISPR-based medicine, Casgevy, for treating sickle cell disease and β-thalassemia, with NHS availability beginning in early 2025. The successful use of personalized gene-editing approaches, such as mutation-specific treatments, demonstrates the scalability of CRISPR platforms. Platform-based editing models allow modification of only select components to target diverse mutations. Regulatory agencies are increasingly recognizing such approaches, enabling faster approval pathways. This convergence of clinical success and regulatory adaptation creates a strong growth runway for specialized modifying enzymes.

Category-wise Analysis

Product Type Insights

DNA ligases are anticipated to capture 25% of product revenues in 2026, driven by their central role in DNA repair, library preparation, and gene editing workflows. Recent portfolio expansions through engineered DNA ligase variants optimized for CRISPR workflows and NGS prep have reinforced this leadership. For example, Thermo Fisher Scientific introduced high-efficiency ligases tailored for CRISPR-Cas9 editing, enhancing precision in therapeutic research, while New England Biolabs expanded its high-fidelity ligase suites for complex genomics tasks. ArcticZymes also launched R2D Ligase™, enabling DNA-to-RNA ligation with expanded sequencing utility. These developments strengthen ligases’ foundational role in research and clinical workflows.

Exonucleases are projected to be the fastest-growing product type, projected to grow at 11.8% CAGR through 2033, as demand rises for editing verification, synthetic biology, and high-precision genome workflows. Enhanced exonuclease variants with improved specificity are increasingly incorporated in genome editing quality control and assembly verification. The growth is accelerated by the broader adoption of high-performance enzyme toolkits optimized for complex constructs and long-read sequencing workflows. The expanding use of engineered enzymes in advanced editing applications positions exonucleases for above-average segment growth.

Application Insights

The pharmaceutical & biotechnology research segment is expected to command around 38% of the DNA modifying enzymes market revenue share in 2026, reflecting extensive enzyme use in therapeutic discovery, translational R&D, and complex construct assembly. Expanded enzyme use for high-fidelity DNA assembly and long-range PCR workflows including new polymerase formulations optimized for gene therapy vector production has reinforced this segment’s leadership. For instance, Thermo Fisher Scientific introduced high-fidelity DNA polymerases in 2025 to support downstream therapeutic development and large-genome analysis, enhancing enzyme integration in regulated research environments. These developments sustain robust enzyme deployment in advanced drug discovery workflows.

The diagnostic application segment is poised to grow at 10.8% CAGR through 2033 as modifying enzymes underpin PCR, NGS, and genomic pathogen surveillance workflows. Public health initiatives such as the CDC Advanced Molecular Detection (AMD) Pathogen Genomics Centers of Excellence and the International Pathogen Surveillance Network (IPSN) have increased demand for high-performance enzymes in real-time outbreak analysis and routine clinical testing. Enzyme-enabled diagnostic kits tailored for rapid and predictive genetic testing, combined with expanded genomic surveillance programs, are accelerating diagnostic enzyme adoption across healthcare systems.

End-User Insights

Pharmaceutical and biotechnological companies are projected to account for approximately 42% of the end-user enzyme volume share in 2026, driven by reliance on enzyme modification across R&D, validation, and regulated production processes. In 2025–2026, major industry players expanded enzyme portfolios with high-fidelity enzyme solutions optimized for regulatory environments. For example, QIAGEN launched integrated enzyme kits compatible with real-time PCR platforms and advanced genomic assays, reinforcing enzyme deployment in therapeutic and clinical workflows. These tailored solutions meet strict quality needs in regulated development pipelines, sustaining enzyme consumption.

Research centers and academic institutions are expected to grow at an estimated 9.5% CAGR through 2033, supported by increasing funding for large-scale genomic studies, synthetic biology research, and collaborative projects. The academic labs have broadened the use of specialized enzyme kits for high-resolution epigenetics and multi-omic research, such as New England Biolabs’ NEBNext Enzymatic 5hmC-seq Kit for single-base methylation mapping. This enzymatic method enables high-quality data generation and expands research capabilities in epigenetic studies. Universities and genomic institutes driving such advanced workflows are early adopters of next-generation modifying enzymes, catalyzing future commercial uptake.

Regional Insights

North America DNA Modifying Enzymes Market Trends

North America is projected to hold an estimated 45% of the DNA modifying enzymes market share in 2026, serving as the leading regional market due to deep biotechnology infrastructure, robust federal research investment, and high adoption of advanced molecular tools. The U.S. remains a global R&D epicenter with major precision medicine initiatives such as the All of Us Research Program’s Genome Centers at institutions such as Baylor College of Medicine, The Broad Institute, and the Northwest Genomics Center, accelerating large-scale genomic sequencing and enzyme usage in research workflows. Market demand is further supported by high engagement in multi-omics research events such as NextGen Omics & Spatial Biology US 2025 in Boston, which focuses on cutting-edge sequencing and clinical genomics methods.

The significant regional developments include expanded sequencing collaborations and technology showcases by Complete Genomics at the American Society of Human Genetics (ASHG) 2025, highlighting new DNBSEQ platforms that support oncology and rare disease research, reinforcing enzyme-dependent workflows. NIH funding increases for precision medicine genomics research also continue to broaden enzyme adoption in both public and private sectors. Innovation density across Cambridge and expanding clusters in San Diego and Seattle sustain high throughput enzyme consumption. Regulatory support and ecosystem maturity ensure North America’s sustained leadership position.

Europe DNA Modifying Enzymes Market Trends

Europe represents a significant and well-established regional market for DNA-modifying enzymes, supported by strong biotechnology participation across Germany, the U.K., France, and Spain. The region benefits from harmonized regulatory frameworks, including coordinated EU research standards and cross-border clinical trial mechanisms, which facilitate streamlined adoption of modifying enzymes in collaborative genomic research and diagnostics. Germany’s advanced pharmaceutical and biotech manufacturing base, the U.K.’s globally recognized genomics research ecosystem, and France’s sustained investments in translational medicine collectively deepen enzyme utilization across both academic and commercial pipelines. Widespread multi-omic research and genomic profiling activities across European genomic centers further sustain consistent demand.

Europe’s genomic research momentum was reinforced by the broader application of Illumina’s 5-base multiomic sequencing solution, enabling simultaneous genomic and epigenomic analysis within disease research workflows. The EU-funded collaborations under Horizon Europe continued to expand shared research infrastructure and cross-institutional data generation. While Europe maintains a strong emphasis on ethical oversight, data protection, and clinical validation, these structured regulatory frameworks provide clarity for enzyme adoption in regulated settings and support long-term growth in diagnostics and therapeutic research applications.

Asia Pacific DNA Modifying Enzymes Market Trends

Asia Pacific is projected to be the fastest-growing regional market, expanding at an approximate 12% CAGR between 2026 and 2033. The growth is propelled by large-scale genomics and precision medicine initiatives, supportive government policies, and increasing research capacity. China’s massive genomic investments continue fueling sequencing and biotech programs across Beijing, Shanghai, and Shenzhen, while Japan’s Japan Genomic Medicine Initiative targets mapping genomes of 100,000 individuals to improve healthcare outcomes. South Korea’s Korean Genome Project and Singapore’s focused genomic initiatives further enhance regional sequencing adoption.

In India, the Genome India Project has completed whole-genome sequencing for over 10,000 diverse individuals and is building a reference dataset that underpins population-specific diagnostics and research platforms. These programs significantly increase the use of DNA-modifying enzymes for both discovery and translational research. Growing networks of genomic medicine departments in hospitals across Japan and South Korea, and partnerships between clinical labs and sequencing technology providers, boost routine use. Regulatory progress toward safe gene-editing frameworks and expanding public-private collaborations reduces barriers for enzyme suppliers. The dynamic pharmaceutical and biotechnology ecosystem of the Asia Pacific positions it as a key driver of long-term market growth.

Competitive Landscape

The global DNA modifying enzymes market structure is moderately consolidated, with leaders such as Thermo Fisher Scientific, New England Biolabs, QIAGEN, Roche, Merck, and Takara Bio capturing significant revenue. They rely on broad enzyme portfolios, technical expertise, and strong pharma and academic relationships. Heavy investment in enzyme engineering, quality systems, and application-specific optimization ensures consistent performance. Platform-compatible kits and integrated solutions strengthen market leadership. Innovation and reliability drive customer retention and recurring demand.

Regional players and niche enterprises are focusing on high-fidelity ligases, synthetic biology, and epigenetics, targeting specialized research needs. High entry barriers arise from quality standards, regulatory oversight, and production complexity. Smaller firms compete via engineered variants, automation-ready formats, and workflow integration. Partnerships and licensing expand capabilities in gene editing and multi-omics. Market consolidation is expected as leaders acquire complementary technologies or expand portfolios.

Key Industry Developments

- In January 2026, Basecamp Research, with NVIDIA and Microsoft, developed the EDEN AI model to design precise genome-editing enzymes using data from over one million species. The AI created large serine recombinases capable of targeted DNA insertions without double-strand breaks. Lab tests showed successful insertion of cancer-fighting DNA into T-cells and antimicrobial peptides with 97% effectiveness.

- In November 2025, ToolGen and GenEditBio partnered to combine ToolGen’s CRISPR-Cas9 platform with GenEditBio’s lipid nanoparticle delivery for in vivo gene therapies. Their lead candidate, GEB-200, targets lipoprotein(a) to treat cardiovascular disease and has shown efficacy in non-human primates. The collaboration aims for IND submission and “once-and-done” treatment development.

- In May 2025, ICAR launched DRR Rice 100 (Kamla) and Pusa DST Rice 1, India’s first genome-edited rice varieties using CRISPR-Cas and SDN1 techniques. These varieties improve yield, drought tolerance, and performance on saline soils without foreign DNA, avoiding GMO restrictions. The crops enhance resource efficiency and climate resilience, supporting sustainable agriculture and positioning India as a leader in agricultural genome editing.

Companies Covered in DNA Modifying Enzymes Market

- Thermo Fisher Scientific

- New England Biolabs

- Takara Bio

- Qiagen

- Promega Corporation

- Agilent Technologies

- Sigma Aldrich

- Bio Rad Laboratories

- Integrated DNA Technologies

- GenScript

Frequently Asked Questions

The global DNA modifying enzymes market is projected to reach US$ 1.4 billion in 2026.

Rising genomic research, adoption of CRISPR and NGS, and expanding pharmaceutical and diagnostic R&D, supported by government funding and public health genomics programs, are key market drivers.

The market is poised to witness a CAGR of 9.2% from 2026 to 2033.

Major opportunities lie in synthetic biology, personalized medicine, and growing diagnostic and multi-omics applications.

Thermo Fisher Scientific, New England Biolabs, QIAGEN, Roche, Merck (MilliporeSigma), Takara Bio, and Codexis are some of the leading players.